Month: May 2004

Cognitive Liberty

Freedom of thought is the most fundamental right. Fortunately, it has been nearly impossible to invade the mind. New technologies, however, do threaten freedom of thought, raising many difficult problems. Should children diagnosed with ADHD who refuse to take Ritalin be refused an education? Should a mentally-ill person be drugged so that they can stand trial? Is hypersonic advertising an invasion of mental privacy?

Here’s an interesting interview on these and related issues with Richard Glen Boire co-founder of the Center for Cognitive Liberty and Ethics.

Index funds, still the way to go

If the market is efficient then without an information advantage (non-public information) you can’t expect to beat the market and thus index funds are a good way for the average investor to invest. Behavioral finance has put some dents in efficient markets theory but just because a market is inefficient that doesn’t mean that beating the market is easy. Even if you knew that firm X was way overvalued, for example, shorting the stock would expose you to great risk – the price could become irrationally higher before the bubble bursts, unexpected events could increase the fundamental value to match the bubble, your capital could run out before the price drops and, of course, you could be wrong.

When you hear the term inefficient market don’t think $500 bills lying on the sidewalk, think $500 bills swirling around you in a vortex of wind…at night. Inefficiency is out there but it’s hard to find.

The bottom line remains that most professional money managers don’t beat the market. Here’s a recent reminder from James Glassman of this fact:

Charles Allmon points out that last year the poorly rated stocks of many research services outperformed their highly rated stocks. For example, Standard & Poor’s one-star stocks returned 57 percent while its five-star stocks returned 43 percent. Merrill Lynch’s sell-rated stocks returned 46 percent while its buy-rated stocks returned 30 percent. Schwab’s F-rated stocks returned 70 percent while its A-rated stocks returned 66 percent. The biggest discrepancy came with Value Line, whose 5-rated stocks (the 100 companies with, supposedly, the worst prospects for the year ahead) returned an incredible 90 percent while the 1-rated stocks (the top prospects) returned 40 percent.

The latest hypothesis about sexual selection

Read here, to learn why many women prefer prominent cheekbones.

Radical Prescription

A recent Rand study of 25 large firms found that raising the co-pay for pharmaceutical claims by just $5 reduced yearly drug costs per worker by $163.*

An interesting piece in the WSJ (“A Radical Prescription,” May 20, 04, R3) suggests that this logic does not always hold. Higher co-pays can cause consumers to cut back on prophylactic and maintenance medicines. Pitney Bowes, for example, found that high-prices caused their diabetic and asthmatic workers to take their medicines irregularly resulting in sudden and expensive attacks. So Pitney Bowes took a counter-intuitive strategy – to save money they would pay for more of their workers prescriptions.

On the new plan workers began to switch to more expensive but more convenient and thus easier to maintain drugs and within a year the company was saving money.

the company was paying more for maintenance medications… [but] it was spending significantly less on rescue medicines…

[S]ignficant saving has come from fewer emergency room visits, which dropped 35% among diabetes patients and 20% among asthma patients…there were also fewer hospital admissions and doctor’s office visits.

The strategy won’t work for all drugs but it shows how much care must be taken in devising optimal insurance plans.

* Originally, I had said this implies a cost to benefit ratio in excess of 30 (163/5). Robert Ayers pointed out, however, that the co-pay is per drug while the savings are per year. Thus the cost-benefit ratio must be lower than 30. The original source doesn’t provide the data to calculate it exactly, however. Thanks Robert!

Indian voters reject high-tech

India appears to take a turn for the worse:

The government in Andhra Pradesh state, headed by the coalition’s second-largest member and a leading proponent of India’s technology revolution, was routed by the Congress party, which is also the main opposition on the national stage.

Besides signalling that high-tech prowess had not impressed the millions of rural poor, the result suggested the national election could end in a hung parliament and likely political turmoil as parties searched for new allies.

Votes from the marathon national election will be counted on Thursday but financial markets have already tumbled on fears that India’s crucial economic reforms could be delayed if a weak government comes to power.

Here is the full story.

Let us not forget that India remains a badly messed-up economy. I found the following passage, from William Lewis’s The Power of Productivity, illuminating:

…India has a special problem. It is not clear who owns land in India. Over 90 percent of land titles are unclear…Unclear land titles most affect industries which use a lot of land. These industries are housing construction and retailing. The result is that there is huge demand for the very little land with clear titles. Not surprisingly, the ratio of land costs to per capita income in New Delhi and Bombay is ten times that ratio in the other major cities of Asia…Also not surprisingly, India has very few supermarkets and large-scale single-family housing developments.

But it gets worse: Stamp taxes on land sales run at least ten percent. Furthermore you are often expected to pay real estate taxes, even if you will never be granted title to the actual land. It is said that the money is accepted “without prejudice.” Here is a short article on how to make things better.

Question of the day

Click here, from the ever-effervescent Jane Galt.

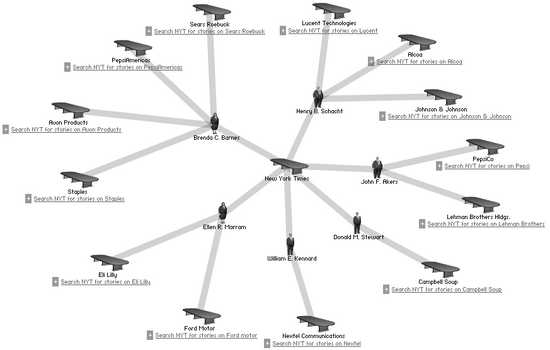

Map the Power Elite

They Rule is a very cool website that uses flash player as a front-end to a database on corporate boards. Find out who is on the board of any of the largest publicly held corporations, choose two firms and find the connections between their boards (ala six degrees of separation), map the power-elites. The map below (click to expand) gives an idea of what the site is all about.

The author, Josh On, is an odd-mix of old-style lefty and cutting edge technologist. When he’s not putting together websites like this what does he do?

Twice a week I stand outside on a street corner and try to engage strangers in conversations about politics. This would be much harder without a copy of Socialist Worker in my hand.

Hat tip to Boing Boing Blog.

Will Google’s Dutch auction go well?

It sounds great: cut out the investment banking fees and just offer a straight Dutch auction on the stock. After all, aren’t auctions the perfect market institution?

Co-blogger Alex thinks that the investment banks have had a comeuppance due for a long time; he may well be right.

Under standard practice, the underwriters give underpriced shares to favored investors and executives. The value of those shares rises on opening day. The insiders are happy but the company has left money on the table. In extreme and indeed pathological cases the discount can be as high as eighty percent. So why have companies tolerated this practice for so long?

Under one apologetic view, the kickbacks, underpriced shares, and payola are necessary. Someone has to produce reputation for the stock. The investment bank is paid to do this. The underwriter, in turn, gives insiders good deals to get them to boost the stock. If you own some shares you will do your best to talk up the issue. The efficient markets hypothesis? Well, it may be true at the margin, but how do we get to this margin in the first place?

I heard another point from one industry insider. Investors feel better about a stock if it goes up on day one. For the long-run good of the stock, it is important to have a price rise in the beginning. If investors sour on the stock in its early days, it may never recover its reputation.

Other skeptics wonder how the results of the auction can be predicted? How many people will show up with bids? What if we gave an auction and nobody came? Other worriers fear the temptation for untutored investors to bid too high at first, pushing the shares to unsustainable levels. After all, no single investor will have the final price much with his or her bid.

There is yet another fear. If the auction is fair, the stock will sell at roughly the same price on day one and day two. So if there is some uncertainty surrounding the initial auction, why not just hold off your buying until day two? But then how do liquid markets get established in the first place? How can you get concentrated buying interest on day one, but without violating either fairness or the efficiency of markets?

The resolution: …will have to wait for the facts and thus the actual auction. But my suspicion is the following. Some percentage of the original underpricing, but by no means all, is in fact a legitimate return to the investment banks. I thus worry that Google will not see strong demand on day one. On top of that, there is a puzzle. Unless you think all of the initial share underpricing is an legitimate fee for services rendered, why have markets tolerated this practice for so long?

By the way, David Levy informs me that used book dealer ALibris will try a share auction as well. For whatever reasons, except for Google, only small companies have shown an interest in these alternative institutions. France uses such auctions more commonly; it seems that the first-day price run-up is smaller but still present. On one hand, these other examples suggest that the auctions are a viable institution. On the other hand, it makes you wonder why the practice is not used more often.

Addendum: Here is a very good piece on the auction of Salon.com stock.

Opening at Cannes

The Cannes film festival starts this week, despite a threatened labor disruption. Yesterday I learned that the term Asia Extreme, the hot style in world cinema right now, has been copyrighted. “Asia Extreme” movies view John Woo as a quaint forefather and go much further in terms of throwing the book away. Are you interested? I’ll recommend Battle Royale for horrific Hobbesian violence, and The Audition for shocking sexual drama. Both are Japanese, and neither is for the fainthearted. But if you feel jaded by most movies, a bit bored, and are looking for something conceptual, this is definitely the next step.

The most popular names

For 2003, the most popular baby names were Jacob and Emily, here is the whole list, including a comparison with 1903. Here is an earlier post by Alex (the link is now fixed), on how names affect our earning potential.

IQ hoax

A table purporting to show IQ by state swept through the blogosphere last week mostly because liberal bloggers enjoyed trumpeting the high correlation it showed between high-IQ and voting for Gore in 2000. Turns out that the table was a hoax. Steve Sailer has the whole story including some real data on education by state and IQ by nation.

Virus writers beware

Microsoft put a bounty on the head of the author of Sasser Internet worm and tips led to his arrest on Friday. With $250,000 at stake, virus writers need to understand that their chances of getting away with it are now slim. The long arm of the bounty hunter will find you.

Telephone history: lessons for today

Have you ever wondered how America became a world leader in mass media and telecom? Paul Starr’s excellent The Creation of the Media addresses this question. Here is one good bit from the book:

French policy was…unfavorable to the telephone. Unwilling to spend public funds on the medium, the French government, beginning in 1879, granted local concessions for telephone service lasting only five years. The idea was to let the private sector assume the risk of a new business, giving the state time to see if it was worth taking over. Private capital could lose money on the telephone, but if the medium proved profitable the government would step in: a policy nicely designed to depress investment. In 1885, the government itself began building long-distance lines but limited construction so as not to cause too rapid a depreciation of its investment in the telegraph. Four years later, it nationalized the local telephone carriers as well, not so much because of a positive commitment to improve telephone service as because of a defensive concern about the erosion of the state’s telegraph monopoly…

By 1895, while the United States had one telephone for every 208 people…France [had] one for every 1,216…In 1927, while Bell was reporting an average delay of 1.5 minutes in placing long-distance calls, it took, on average, more than an hour to put through a call from Paris to Berlin.

The bottom line: Keep this story in mind the next time you hear politicians talking about the regulation of VOIP.

Do dogs resemble their owners?

Yes, but only if the dogs are purebreds.

The researchers photographed 45 dogs and their owners at three dog parks and gathered information about the breeds and how long owners and pets had been together. They then asked 28 students to try to match the people to the pooches.

The students were able to match dogs to their owners, but only when the dogs were purebred.

“The results suggest that when people pick a pet, they seek one that, at some level, resembles them, and when they get a purebred, they get what they want,” the researchers wrote. “A nonpurebred puppy’s final appearance is unpredictable, and so the resemblance . . . should be confined to the much more predictable purebreds.”

There was no relationship between how long owners had lived with their dogs and the chance that their appearances would match.

“These results were consistent with the notion that the ability to match is due to selection rather than convergence,” they wrote. “However, it does appear that, as in the case of selecting a spouse, people want a creature like themselves.”

Here is more statistical information.

Not surprisingly, many commentators believe that we select Presidents on the same basis.

Mother’s day facts

Most Americans will remember to call their mothers or send cards for Mother’s Day tomorrow, but about one in four will forget [is that the right word?] the national holiday altogether, according to a new survey.

Here’s more:

Those who do remember Mom are expected to spend an average of $98.64 this year, according to a report by the National Retail Federation, a D.C. trade association.

The amount is slightly more than last year’s $97.37, said NRF spokeswoman Ellen Tolley.

“Mother’s Day saw a huge increase in consumer spending right after September 11, but since then it has stabilized to a gradual increase,” Miss Tolley said. In 2000 and 2001, the average spending per customer was less than $65.

Total spending for the holiday is estimated at over $10 billion. Here is the full story.

In a few days’ time, I’ll be up north in New Jersey and taking my mom (who reads this blog) out for food, movie, and museum. As for today, Yana and I are taking her mom to Thai food, the theater, and the superb Mayan exhibit at the National Gallery.

Happy Mother’s Day to all the moms!