Month: December 2005

Alex on the Beeb

I will be on the BBC, BBC Radio Five Live, on Sunday night 9-10 pm EST talking about pensions, global warming and other topics with the host and other guests. It’s a call-in, email-in show so it should be fun.

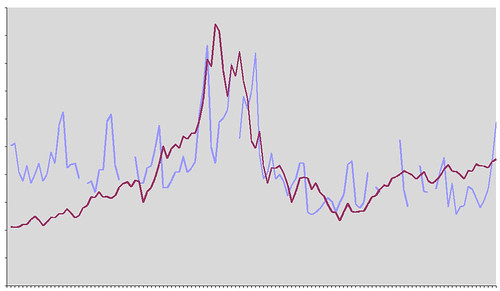

Wired Ads a Leading Indicator?

Is it time to invest in technology stocks again? Mark Frauenfelder at Boing Boing Blog points us to this graph (before getting too excited, however, I would want to detrend for seasonality, i.e. the Christmas effect):

Rich Giles made a graph that compares the page counts of past issues of Wired

with the the rise and fall of Nasdaq over the years.You’ll note that the Nasdaq (red) lags Wired’s page count (blue) by a

few months [No longer true, in the updated graph -see below – although they do seem to move together, AT]. I’m not suggesting you go an buy technology shares, but gee, I’m

thinking the reports of money pumping back into technology companies might just

be true given the big up-tick in this months page count (294).

Addendum: There were some problems with the author’s original graph. He corrected and I have reposted. The data are available here. Thanks to the Stalwart and Paul N for pointing me to the problem.

Worthy excerpts from face transplant articles

Clint Hallam, the man he selected for the world’s first hand

transplant, refused to keep up with the lifelong drug regimen required

to suppress immune responses, along with regular exercises to train the

new hand. After three years he had the hand removed.

And then:

Brain-dead patients in France are presumed to be organ donors unless

they have made explicit provisions to the contrary, and approval by

next of kin is not normally required.

Here is the full story.

Wisdom about upward-sloping demand curves

MR has had especially good comments lately:

The problem with this thought experiment is that even if every

individual (or all but one) have an upward-sloping individual demand

curve, the market demand curve will still be downward-sloping. The

reason is, when people who seek higher prices will run out of money

faster, thus buying fewer units. So higher prices still lead to fewer

units sold — i.e., a downward-sloping market demand curve.

Or how about this:

Your curve slopes upward until it reaches the point where quantity

times price equals your wealth. From there on, it slopes down (you buy

as much as you can afford, which is less and less at higher prices).So everyone would quickly spend all their money.

Oddly, some goods might end up with demand curves that slope down in

the relevant price range– in spite of the buyers’ preferences!

Perhaps you’ve already spoken your mind, but comments are open again, in case you would like to take another crack at the problem. And remember, spent funds are recycled to sellers and do not represent the destruction of real resources.

10:30 p.m.

Tim Harford and I will be on C-Span, also with Sebastian Mallaby and Bob Hahn. And here is Tim, channeling Thomas Schelling, on why you should burn your Christmas card lists.

Nick Szabo’s blog

One of my main interests is the history of institutions, and in

particular the patterns that recur in successful institutions. These

organizational structures and security mechanisms allow naturally

suspicious strangers to interact with integrity.These patterns include tamper evidence, shared time, unforgeable costliness, separation of duties, the principle of least authority, risk sharing, and learning from our ancestors,

among many others. These patterns have been useful for centuries, and

(I can report after having spent many years working in the computer

network security field) continue to be useful in the Internet era.

Here is the blog. Here are Nick’s essays. The pointer comes from Brad DeLong. Here is Nick on The Playdough Protocols.

How fast is the economy growing?

Arnold Kling, teaming up with Robert Fogel, has the answer.

Does capital taxation hurt an economy?

Following my Econoblog debate with Max Sawicky, Kevin Drum writes:

Basically, I’m on Max’s side: I think taxation of capital should be at roughly the same level as taxation of labor income. However, I believe this mostly for reasons of social justice, and it would certainly be handy to have some rigorous economic evidence to back up my noneconomic instincts on this matter. Something juicy and simple for winning lunchtime debates with conservative friends would be best. Unfortunately, Max punts, saying only, "As you know, empirical research seldom settles arguments."

Let me repeat the chosen comparison: capital taxes vs. gasoline taxes and no subsidies for housing. That is a no-brainer. But still you might be interested in the question of capital taxes vs. labor taxes. Here are some points:

1. Supply-siders writing on capital taxation often make exaggerated claims. Even if you like their conclusions, beware.

2. Taxing dividends, corporate income, returns to savings, and capital gains all involve separate albeit related issues. I am willing to consider zero for the lot. Of that list, the corporate income tax is probably the biggest mess. The capital gains tax is the least harmful. The tax on dividends is the least well understood (in perfect markets theory, the level of dividends should not matter at all). By the way, if you are worried about noise traders, a transactions tax is a better way to address this problem than a capital gains tax.

3. The U.S. currently lacks exorbitantly high levels of capital taxation. Joel Slemrod estimates a rate of about fourteen percent, albeit with many complications and qualifications. N.B.: We lower the rate of tax on capital by engaging in crazy-quilt and distortionary adjustments. Nonetheless it is incorrect to argue "we have high rates of capital taxation and are doing fine, better than Europe." Do not confuse real and nominal tax rates.

Take the capital gains tax. Once you consider bequests and options on loss offsets, the effective rate of tax is arguably no more than five percent. But it is still set up in a screwy way. Bruce Bartlett points me to this short piece on real tax burdens on capital.

4. Peter Lindert has good arguments that favorable capital taxation has helped European economies finance their welfare states.

5. Larry Summers did the best empirical work on how abolishing capital income taxation would boost living standards.

6. Encouraging savings will have a big payoff. If you tax capital at zero, in the long run you will have much more of it. This holds in most plausible views of the world. Max’s examples aside, the supply curve for savings does not generally slope downwards; nor need you write me about various strange counterexamples from Ramsey models. Sooner or later, more capital will kick in to mean a much higher standard of living.

7. Bruce Bartlett points me to this excellent CBO study. It shows how much capital is taxed unevenly; one virtue of a zero rate is to eliminate many of those distortions in a simple way.

8. Remember those arguments about how more money doesn’t make you happier? And we are all in a rat race where we work too hard to win a negative-sum relative status game? I’ve never bought into them, but it’s funny how they suddenly stop coming from the left once the topic is capital vs. labor taxation.

9. The same excellent Slemrod paper (and he is no right-wing supply-side exaggerator) also suggests that the revenue lost from a zero rate on capital would be small. N.B.: The references to this paper are the place to start your reading on this whole topic.

10. Kevin Drum’s belief in social justice should not necessarily lead him to look for arguments for taxing capital. Even if we accept his normative views, there is the all-important question of incidence. Taxing capital can hurt labor. If you are truly keen to tax capital, this is a sign of a high time preference rate, not concern for the poor.

11. Some forms of human capital also should receive favorable tax treatment. Vouchers for primary education and state universities are two examples. I am also happy — in part for equity reasons — to subsidize human capital acquisition through an Earned Income Tax Credit.

12. What is really the difference between capital and labor? Is it simply measured elasticities? The size of each potential tax base? The greater "future orientation" of capital and the possibility for compound returns? All of the above? How much does your answer depend on whether you view capital as a "fund" or as a "collection of capital goods"?

The bottom line: It all depends on the margin. If your levels of government spending allow you to keep labor rates of taxation below 40 percent, I don’t see comparable gains from lowering tax rates on labor. If you have equity concerns, express them through other policy instruments. But if your marginal tax on labor is 65 percent and your tax rate on capital is 15 percent, cut the tax on labor first.

I know it hurts, but all of you non-right-wingers out there should consider a zero rate of taxation on capital. Comments are open.

A crash course on spontaneous order

You will find the essay here, with comments, and yes it includes Smith and Mandeville up through the moderns.

How to choose a charity

MR reader Jeffrey Drucker writes:

I’ll be graduating college in just a few weeks and entering the real world. That is I’ll be a salaried employee making all budgetary decisions for myself. Aside from the necessary components of spending, saving, and repaying my college loans I’d like to set a portion of my earnings aside for charitable donation. I’ve always thought that charity was a crucial element of any caring libertarian’s mindset. Now that I will be able to spend my own money, I wondered if you could provide any insight into the economic considerations of charity.

Obviously, the decision to donate is based on personal considerations and evaluations of the relative merit of different organizations. But economically is it more sensible to donate to a wide number of worthy causes or champion just one. Should I focus on issues closer to home or those who are in the most need the world over? How large a percentage of my income is it reasonable to donate, what issues should I consider (value of investment opportunities, lifetime consumption)?

Putting political and intellectual non-profits aside, here are some principles for purely charitable giving:

1. Published information on budget ratios devoted to programs and fundraising expenses is not reliable. Many charities manipulate the data.

2. Consider neglected but long-simmering problems; read my earlier analysis of whether you should focus on the crisis of the day.

3. Hardly anyone gives enough to charity and you won’t either. Pick a cause or causes you will become addicted to. Tell others you won’t back down from your cause, so that you will lose face if you do.

4. My preferred approach is pure cash transfers to rural Mexicans, vis-a-vis Western Union. You don’t get the tax break but administrative expenses are very low. Think of Western Union as a for-profit charity.

5. In-kind aid sounds inefficient to the economist, but the commitment may make you happier. You are wasting most of your time anyway.

6. Don’t give money to beggars, the explanation is here.

The comments are open for other suggestions. Analytical principles are especially welcome.

Cautionary tales for smart alecks

Morales, who only months earlier had extolled True’s qualities when the Huichols were released from jail, now demonized him. He was up to no good, she insisted. The Huichols had issued an all points bulletin in their communities announcing that True was persona non grata because of previous forays into Huichol territory made without permission in search of agates and opals to enrich himself. He had been caught trading in gemstones before, she assured me, and on one such trip had been detained and held in a crude Huichol stockades.

That is from the new and excellent Trail of Feathers: Searching for Philip True, A Reporter’s Murder in Mexico and His Editor’s Search for Justice, by Robert Rivard.

Freakonomics Sells

The first signed copy of Freakonomics inscribed, "To Tim, The first book I’ve ever signed. You can probably get at least $9.50 on

eBay. Steve Levitt," sold on EBay for $610!

Congratulations to the winner of the auction, to Tim Harford who donated the funds to charity and to Steve who doubled the donation.

Tim Harford, by the way, will be speaking at GMU on Monday Dec. 5, 7:30 in the Johnson Center meeting room B. The Undercover Economist is a great read and Tim is a fun speaker so I invite all to come and enjoy. You can even ask him to sign your copy of the Undercover Economist!