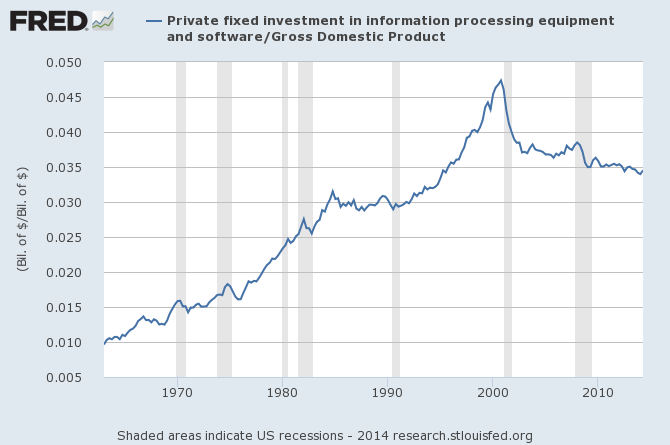

U.S. IT investment as a share of gdp

The pointer is from Matt Yglesias.

Addendum: Claudia Sahm refers us to this chart of declining IT prices. It also can be argued that IT spending moved into other, more general business categories.

The pointer is from Matt Yglesias.

Addendum: Claudia Sahm refers us to this chart of declining IT prices. It also can be argued that IT spending moved into other, more general business categories.