What are you people thinking?

Today’s suggested packing lists for seven-week camps can include a light blanket and warm comforter, two sets of sheets, six towels, three pairs of sneakers, 25 pairs of underwear, 25 pairs of socks, sports equipment and toiletries. Then, there are clothes for most every weather scenario, including a raincoat and boots, fleece jacket, more than 20 tops and shorts, and 10 pairs of pajamas—split between lightweight and heavy.

Miscellaneous items include foldable Crazy Creek chairs, a kaboodle to hold hair ties, makeup and nail polish, flashlights, decorative pillows for optimal bunk coziness, family photos to fend off homesickness, games and personalized lockboxes for, say, smuggled-in candy.

“Color War” is its own sartorial challenge. At this epic end-of-summer tournament, campers sport their team’s color and compete in events. But since the kids don’t know what color they’ll be assigned, parents often pack for four possibilities.

For the buying, many families make a “camp appointment” with a personal shopper at Denny’s, a children’s boutique in New York, New Jersey and South Florida. Associates greet them with their camp’s packing list printed out. Spencer Klein, whose family has owned Denny’s since 1978, says the average spend for a new camper appointment is $1,500 to $2,000. (A coveted perk: the store labels everything for free.)

As for those new service sector jobs:

This year, for the first time, Dara Grandis, a Manhattan mom of three, hired professional organizer Meryl Bash to pack for her three children, who head off in late June for seven weeks at camp.

Here is the full WSJ article by Tara Weiss, via the excellent Samir Varma.

Derek Gripper, Cape Town guitarist

How many hottest days of the year? (so far)

- The average number of days in a year which can be called ‘hottest day of the year so far’ is 20.0

- If we want to restrict the number of ‘noteworthy hottest days of the year so far’ to 3/year, we can restrict noteworthiness to days which are at least 20˚C and at least 1.6˚C hotter than the previous hottest day

- The places which set the most ‘hottest day of the year so far’ records are in the south east of England

Here is the full post by Eliot Fosong, via Sam Enright.

RIP, David Boaz

Here is notice from Cato.

The Marginal Revolution Theory of Innovation

A FDA panel voted against approving MDMA (ecstasy) for post-traumatic stress disorder. Putting aside the specifics of the case, I was vexed by this statement on innovation from one of the experts voting no:

“I absolutely agree that we need new and better treatments for PTSD,” said Paul Holtzheimer, deputy director for research at the National Center for PTSD, a panelist who voted no on the question of whether the benefits of MDMA-therapy outweighed the risks.

“However, I also note that premature introduction of a treatment can actually stifle development, stifle implementation and lead to premature adoption of treatments that are either not completely known to be safe, not fully effective or not being used at their optimal efficacy,” he added.

A textbook example of making the perfect the enemy of the good. But the problem is even worse. Holtzheimer seems to think that treatments spring from the lab perfectly formed like Athena springing from the brow of Zeus. Indeed, Holtzheimer suggests that treatments should be kept in the lab until they are perfect. News flash: there are no perfect treatments–no drug or device in use today is completely known to be safe, fully effective, and used at its optimal efficacy. Not one. If we follow Holtzheimer’s counsel, we will never approve a new drug.

Innovation is a dynamic process; success rarely comes on the first attempt. The key to innovation is continuous refinement and improvement. A firm with sales gains greater resources to invest in further research and development. Additionally, they benefit from customer feedback, which provides valuable insights for enhancing their products and processes. Learning by doing requires doing. But if imperfect treatments are never approved, scientists often don’t return to the lab to refine and improve them. Instead, the project dies. Thus, when considering innovation today, it’s essential to think about not only the current state of technology but also about the entire trajectory of development. A treatment that’s marginally better today may be much better tomorrow.

Small steps toward a much better world.

Updating the Drake equation?

Planetary scientists Robert Stern from the University of Texas at Dallas and Taras Gerya from ETH-Zurich, the two co-authors on the study, suggest that the presence of both continents and oceans, along with long-term plate tectonics, is critical for the emergence of advanced civilizations. They consequently propose the addition of two factors into the equation: the fraction of habitable planets with significant continents and oceans and the fraction of those planets with plate tectonics operating for at least 500 million years. This adjustment, however, significantly reduces the value of N in the Drake Equation…

According to the new study, plate tectonics are crucial for developing complex life and advanced civilizations. Earth’s plate movements create diverse habitats, recycle nutrients, and regulate climate—all vital for life. It’s important for plate tectonics to last for 500 million years, Gerya explained, because biological evolution of complex multicellular life is extremely slow. “On Earth, it took more than 500 million years to develop humans from the first animals, which appeared around 800 million years ago,” he said.

Here is more from George Dvorsky, via the excellent Samir Varma.

Resurrecting some form of CAPM?

We find that procyclical stocks, whose returns comove with business cycles, earn higher average returns than countercyclical stocks. We use almost a three-quarter century of real GDP growth expectations from economists’ surveys to determine forecasted economic states. This approach largely avoids the confounding effects of econometric forecasting model error. The loading on the expected real GDP growth rate is a priced risk measure. A fully tradable, ex-ante portfolio formed on this loading generates a procyclicality premium that is statistically significant, economically large, long-lasting over a few years, and independent of the size, book-to-market, and momentum effects.

That is from a recent NBER working paper by William N. Goetzmann, Akiko Watanabe, and Masahiro Watanabe.

Thursday assorted links

1. Good thread on AI and national security.

2. NYT on South African jazz. Here is one cut.

4. Finland will offer bird flu vaccinations to select groups of people.

5. Andrew Stuttaford on my GOAT dialogue. And the transcript from the Dominic Pino chat.

Mark Lutter reports on the Bahamas (from my email)

I won’t double indent, this is all Mark:

“The Prime Minister of the Bahamas recently gave a speech on revitalizing Grand Bahama. He called out the current asset owners of Intercontinental Diversified Corporation, a holding company for Freeport, for not re-investing and for selling off various pieces of the asset. He wants a world class partner to develop Grand Bahama. Half his cabinet attended the speech in person. It is the strongest stance a Prime Minister has taken in 50 years with respect to Grand Bahama.

Here is some additional background reading on Grand Bahama and Freeport. The Prime Minister has two years left in his term and has made revitalizing growth on Grand Bahama his political legacy. Some key facts about Freeport

- 70k+ acres of developable land under Grand Bahama Development Company

- Infrastructure to support 250k residents, current population is 50k

- 25 minute flight to Miami

- Existing legal framework for a charter city, though some of the rights of the Grand Bahama Port Authority, the city government, have been eroded over time

I hope you find this interesting enough to blog about and would appreciate a shout out. Happy to answer any additional questions you might have.”

TC again: Here Mark comments on Twitter.

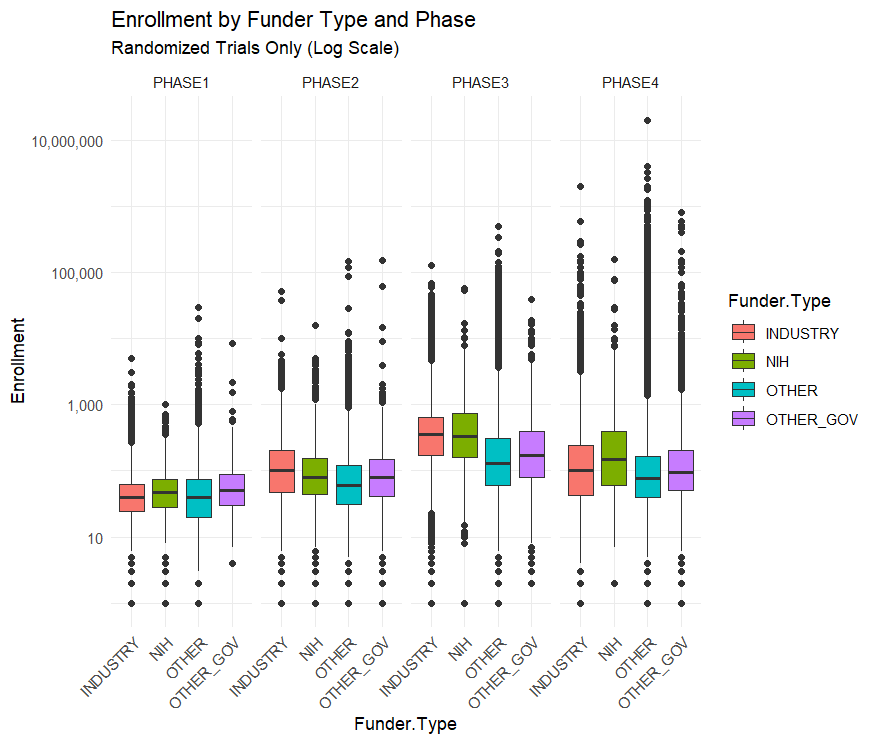

The NIH Doesn’t Fund Small Crappy Trials

A nice catch by Max at Maximum Progress:

[A common critique] is that the NIH funds too many “small crappy trials.” That quote is from a FDA higher up, but the story has been repeated by many others…I downloaded all of the clinical trial data from ClinicalTrials.gov to find out….The median NIH funded trial has 48 participants while the median industry funded trial has 67. The average NIH funded trial has 288 participants while the average industry trial has 335 and the average “Other” funded trial (mostly universities and the associated hospitals) has 923 participants.

By median or by average NIH trials are the smallest out of all the funders. This seems to confirm the “small crappy trials” narrative

…This narrative is reversed, however, when you split up the trials by phase.

Across all trials NIH funded ones are the smallest, but within each phase NIH trials are the largest or second largest. Their overall small enrollment average is just due to the fact that they fund more Phase I trials than Phase III. But NIH Phase I trials have a bigger sample size than industry funded trials on average.

This is an example of Simpson’s Paradox in the wild!

Arguing that the NIH should stop funding unusually small trials is easy but arguing that they should shift from funding the Phase I trials closest to basic research towards later stage trials is less clear.

The NIH’s clinical trial strategy is certainly not perfect and improving it is valuable. But a systematic bias towards “small crappy trials” doesn’t really seem like it’s an important problem facing the NIH.

Rhino capital markets in everything?

In 2022 the World Bank priced the world’s first wildlife bond, raising $150 million that will be partially used for the conservation of black rhinos at two reserves in South Africa. Returns on those five-year bonds will be determined by the rate of population growth. It said at the time that it hoped that the structure would be emulated…

Under the rhino bond’s structure the issuer makes contributions toward conserving the animals instead of paying coupons and the buyers of the bond receive a payment based on preset targets for population growth. Black rhino numbers have dropped to about 2,600 from 65,000 in 1970, and may once have been as high as 850,000, according to documentation from the World Bank. They are smaller than the more common white rhino.

Here is more from Antony Sguazzin at Bloomberg. As the article notes, Rand Merchant Bank is considering issuing wild dog and lion bonds as well, with the exact structure still being discussed.

What if investors overextrapolate from small samples?

We build a model of the law of small numbers (LSN)—the incorrect belief that even small samples represent the properties of the underlying population—to study its implications for trading behavior and asset prices. In our model, a belief in the LSN induces investors to expect short-term price trends to revert and long-term price trends to persist. As a result, asset prices exhibit short-term momentum and long-term reversals. The model can reconcile the coexistence of the disposition effect and return extrapolation. In addition, it makes new predictions about investor behavior, including return patterns before purchases and sales, a weakened disposition effect for long-term holdings, doubling down in buying, a positive correlation between doubling down and the disposition effect, and heterogeneous selling propensities to past returns. By testing these predictions using account-level transaction data, we show that the LSN provides a parsimonious way of understanding a variety of puzzles about investor behavior.

That is from a new NBER working paper by Lawrence J. Jin and Cameron Peng. A nice sequel would be “what if non-investors overextrapolate from small samples?”

The best business books aren’t in the management section

I expand on this theme in my latest Bloomberg column, here is one excerpt from that:

I thus have a modest proposal for anyone interested in business books: Read books about specific businesses or industries that you already know a lot about. That way, you will have enough contextual knowledge for the book to be meaningful. Of course many people don’t work at a company or industry big or famous enough that there are books about it, so I have a corollary proposition: You will learn the most about management by reading books about sports and musical groups.

And this:

Many music and sports books are not only written for obsessed fans, but also written by obsessed fans. Traditional business books, in contrast, are frequently written to get consulting work or on to the speaker’s circuit. The incentive is not to offend anybody and to put forward some “least common denominator” insights, rather than say anything truly original that might be complicated to explain. The end result is a bookstore section that would be mind-numbing to have to read.

There is much more of interest at the link, recommended.

Wednesday assorted links

1. Retrospective by Jack Clark of Anthropic.

2. How will AI alter worker bargaining power? (as distinct from shifting the demand for labor in various ways)

3. Tony Morley doing Progress Studies in Australia.

4. Teles and Saldin on where is the political room for an abundance agenda?

The Danish Mortgage System Avoids Lock-In

Tyler and I have been promoting the Danish mortgage system for years. Recall that in the Danish system each mortgage is backed by a matching bond. As a consequence, mortgage holders have two ways to pay a mortgage: 1) hold the mortgage and pay the monthly payments or 2) buy the matching bond and, in effect, extinguish the mortgage. The latter option is valuable because when interest rates rise, the price of mortgages fall. As I wrote earlier:

Thus, if a Danish borrower takes out a 500k mortgage at 3% interest and then rates rise to 6%, the value of that mortgage falls to $358k and the borrower could go to the market, buy their own mortgage, deliver it to the bank, and, in this way, extinguish the loan. Since the value of homes also falls as interest rates rise this is also a neat bit of insurance. Remarkable!

James Rodriguez writing at Business Insider points out another advantage of the Danish system, it avoids lock in:

When mortgage rates shoot up, as they did over the past two years, many would-be sellers decide they don’t want to move after all. Sure, a new home could be nice, but trading up would mean parting ways with a cheap mortgage rate. What may have been a welcome change suddenly sounds like a painful, expensive divorce. So they sit tight. A gummed-up housing market is good for nobody: First-time buyers can’t find enough homes for sale, and wannabe sellers remain trapped in places that are either too big or too small. This is called the lock-in effect — and it could linger for decades.

… One estimate (here, AT) suggests the lock-in effect prevented more than 1 million people from selling their homes in the span of just a year and a half, a steep toll considering about 5 million homes exchange hands in a typical year. I used to think of these golden handcuffs as an inevitable side effect of the magical 30-year fixed mortgage. But it doesn’t have to be this way. The answer to our problems may lie thousands of miles away … in Denmark.

…Danish sellers are able to earn a profit when they trade in their low mortgage rates for more-expensive ones, making it easier to move even when rates rise.