Category: Education

From Prediction Markets to Decision Markets and Beyond!

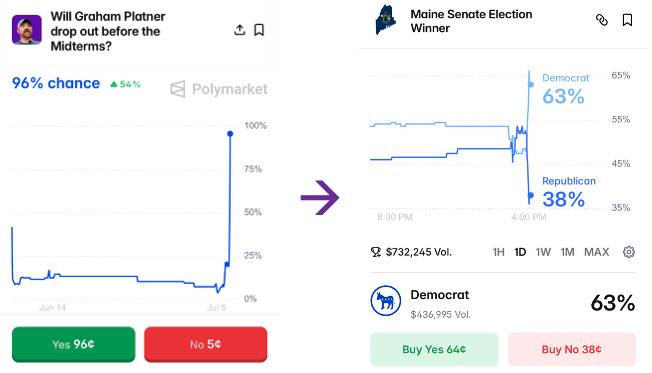

Arin Dube points to a great illustration of the power of prediction markets. Yesterday due to a new scandal the probability that Graham Platner would drop out of the Maine Democratic primary exploded from 9% to 96% (+87 percentage points). At the same time, the probability that the Democrats would win the election jumped by about 9 percentage points, from 54% to 63%. What does this tell you?

The market is signaling that Platner reduces the Democrats’ chances of victory. We can be more precise. If an 87-point increase in the probability of dropping out gets you 9 points of winning, then a 100% chance of dropping out implies a gain of 9/0.87 ≈ 10.3 percentage points.

The market is signaling that Platner reduces the Democrats’ chances of victory. We can be more precise. If an 87-point increase in the probability of dropping out gets you 9 points of winning, then a 100% chance of dropping out implies a gain of 9/0.87 ≈ 10.3 percentage points.

Thus the market’s best estimate is that Platner is reducing the Democrats’ chance of winning by about 10 percentage points (compared to an unknown replacement). That’s a pretty big number! Democrats should surely use this information to make better decisions.

Now, I have been a bit loose. We have implicitly assumed that the news mainly moved the probability of Platner dropping out, rather than independently changing the Democrats’ general-election prospects. The issue is we are trying to reverse engineer two conditional prices, P(win|drop) and P(win|stay), from one unconditional price, P(win), and its comovement with P(drop). It works pretty well here as an illustration but Robin Hanson’s idea is that we can do better yet by trading the conditionals instead of inferring them.

Hanson’s decision markets would run contracts of the form “pays $1 if Democrats win, conditional on Platner dropping out — bet refunded if he stays.” Plus the mirror contract conditioned on staying. The refund provision makes the price a conditional probability: a trader pricing the first contract doesn’t need any view on whether Platner drops out, only on how the race goes if he does. With this structure we would get cleaner estimates of the conditional probabilities–in this case whether the Democrats do better with Platner in or out–which is exactly what a decision maker needs.

We were able to plausibly reverse engineer our estimate because the market happened to move 87 points in a single day. But a decision market would have posted the number continuously, no scandal required. In other words, with decision markets in play, not just prediction markets, we could have seen how much Platner was costing the Democrats before the latest scandal hit—which is precisely when the information would have been most useful.

It’s been fun to see prediction markets catch on with the public but the world is still decades behind Hanson’s decision markets—let alone futarchy!

What should I ask Michael Moritz?

Yes I will be doing a Conversation with him, based around his new book Ausländer: One Family’s Story of Escape and Exile. Mike of course was a pioneering venture capitalist through Sequoia, and before that had a distinguished career as a journalist, which included books on Chrysler, Apple (the first such book I believe?), and soccer coach Alex Ferguson of Manchester United. Here is his Wikipedia page.

So what should I ask him?

A scientific benefit (and cost) of AI innovation

What changed was that the cost of preliminary exploration collapsed. I could sketch an argument, identify the first serious objections, test whether they were fatal, and reach a provisional verdict in an afternoon rather than a fortnight. This sounds like a simple acceleration, and the more profound effect was on what I was willing to abandon. Dropping a question after an afternoon’s work feels nothing like dropping one after three weeks. When the exploration costs are low, the sunk cost attachment disappears, and you find yourself dropping bad questions earlier and more often, which means the questions you keep are better. I explored far more ideas, and my working portfolio became both larger and better curated. I arrived at this outcome not through any deliberate plan but simply through sustained engagement with a tool that changed what exploration cost.

The skill that improved most, and the one I would never have thought to look for, was something I can only describe as question-identification – the ability to find problems that are both tractable and important. This is the thing an academic career is substantially built on and which nobody, so far as I know, has ever tried to teach directly.

I want to be honest about the costs. My ability to hold together a complex position verbally, under pressure, in a seminar or a conversation, has probably not improved and may have declined somewhat. When preliminary exploration is cheap, you spend less time grinding through arguments from first principles, a grinding that builds fluency that shows up in live exchange. Friends have pressed me on this, and they are right to worry.

That is from Carlo Cordasco, and there is more, via Conor Friedersdorf.

Rent Control: The Ceiling Trap

Rent control is in the news again. Check out my new website, Rent Control: The Ceiling Trap. Here is just one bit:

Norway abolished its rent control in 1982, and the economist Are Oust realized the newspapers had been quietly recording the whole experiment. He collected housing classifieds from Oslo’s Aftenposten from 1970 to 2008 and watched the market turn inside out.

Under rent control, Oslo’s listings pages looked nothing like a housing market. It was tenants who advertised, pleading their qualities to landlords — “housing wanted” ads outnumbered “housing for rent.” Ten to fifteen percent of those ads were placed by the tenant’s employer, vouching for them the way a bank vouches for a borrower. Tenants offered babysitting, gardening, snow-shoveling, and janitorial work on the side to sweeten the deal. Landlords, for their part, could demand a tenant of a particular gender, age, occupation, region of origin — some ads specified “strong Christian beliefs.” Deposits commonly ran to 50 or 60 months’ rent, occasionally 100 or more: tenants effectively lent the landlord the equity of the flat, interest free. And only about 20 percent of “for rent” ads dared print the rent, much of which would have been illegal.

Then the ceiling lifted. Within a few years the page flipped: landlords advertised to tenants, roughly 80 percent of listings printed an asking rent, the mega-deposits vanished, and the demands for snow-shoveling Christians of specified gender dwindled to nothing. The price went back to doing the rationing — so nothing else had to.

Check out the whole thing–it’s fabulous.

Emergent Ventures India, 17th cohort

This is all from Shruti:

Aryamman Bhatia is part of the team building HackerFab IITB, an open-source student-built chip microfabrication lab. He received his grant to build what he hopes will become the world’s cheapest fabrication tools and to inspire bottom-up contributions to India’s Semiconductor Mission.

Yashi Garg, 17, received her grant for Neurosole, a smart shoe designed to detect and prevent diabetic neuropathy. She is also a poet and emerging entrepreneur focused on purposeful innovation.

Fahad Hasin received his grant for the Kerala Growth Series, articles and policy memos to improve economic growth in the state. He thinks of the project as publicly building “the M document” of today.

Shafquat Aman, founder of NexuSelf, received his grant to build an AI wellness platform syncing women’s nutrition, workouts, hydration, and menstrual cycles to drive 2x adherence and lasting health outcomes. The company is a Delaware C-Corp in beta with users across the United States and India.

Kevin Wilson, founder and director of Tala Education, received his grant to scale play-based music pedagogy programs that train teachers and turn early childhood classrooms across India into spaces of creativity, inquiry, and joyful learning.

Yogesh Ostwal and Ayush Ranawade received their grant to build a generative AI model for discovering novel oncolytic viruses.

Priyansh Kumar, from Delhi, received his grant to work on an autonomous aerial defense system.

Gowtham Y is an instrumentation, electronics, and chemical engineer. He received his grant to work on synthetic fuel production, starting with cooking gas, at large scale using solar power.

Yash Mandlik, 18, received his grant to create a decentralized hostel network for solo and budget travelers, empowering every house to host the world.

Khush Mahajan, 22, received his grant to build a hyper-personalized AI storytelling app that helps kids grow curious. He is focused on learning by building consumer AI products and turning those lessons into useful tools.

Suraj Tripathi, 17, received his grant for Xorbital, a space-based solar power system that collects sunlight in orbit and wirelessly transmits clean energy to Earth, aiming to provide 24/7 power for defense, disaster response, and remote regions.

Jenil Gandhi, 22, founder of Avinya Vegan Leather, received his grant to develop 100 percent compostable, plant-based vegan leather made from agricultural waste, reducing crop burning and animal cruelty.

Tanay Lohia received his grant for Mandrake Bioworks, which is building what he hopes will be the world’s smallest and most efficient gene editors for breakthrough cures, crops, and more.

Krishna Kant, 20, received his grant to develop a novel type of quantum dots for applications in science and technology.

Vaibhav Dabas, 20, received his grant to develop a smart ramp for train boarding.

Anindyadeep Sannigrahi, founder of LiteFold, received his grant to build infrastructure for drug discovery. The platform helps researchers iterate on experiments faster and move findings to the wet lab with greater confidence.

Chitra Singh, a visual computing graduate from MPI Germany, received her grant to build an AI copilot that streamlines radiology imaging workflows. She has spent a decade building and scaling imaging AI at deep-tech startups and GE Healthcare.

Shreyansh Diwakar, 18, from Jhansi, received his grant for the 1825 Fund, a micro-grant initiative offering equity-free capital to ambitious young builders and hackers across India.

Aditya Jha, 16, founder of Workithm, received his grant to build an AI-powered system designed to protect attention rather than merely manage tasks. He is focused on the future of human-AI collaboration, especially deep work and cognition.

Jeya Kalis, 18, from Madurai, Tamil Nadu, received his grant to develop AI for scientific discovery by exploring combinatorial possibility space.

Chetan Bhattacharji, a journalist and climate communications consultant, received his grant for Earth Chakra, where he writes and produces videos and a podcast that place science, solutions, and experts on air pollution, climate change, and sustainability center stage.

Nithish Kumar, 26, received his grant to build the computational layer for portable nuclear fission reactors to power the next frontiers of humankind.

Sparsh Agarwal, a tea planter based in Darjeeling, received his grant for Alter Magazine, a Works in Progress-style monthly publication featuring new writing on science, technology, and progress from South Asia.

Those unfamiliar with Emergent Ventures can learn more here and here. The EV India announcement is here. More about the winners of EV India second, third, fourth, fifth, sixth, seventh, eighth, ninth, tenth, eleventh, twelfth, thirteenth, fourteenth, fifteenth and sixteenth cohorts. To apply for EV India, use the EV application, click the “Apply Now” button and select India from the “My Project Will Affect” drop-down menu.

And here is Nabeel’s AI engine for other EV winners. Here are the other EV cohorts.

If you are interested in supporting the India tranche of Emergent Ventures, please write to me or to Shruti at [email protected].

How to ask for help from a stranger

The next heuristic is to make your request easy to accept. Making something easy to accept largely is about reducing the cost of acceptance. One clear kind of cost is the magnitude. Do ask someone for twenty minutes of their time, but don’t ask them to read your five-hundred-page manuscript in a week. Another is to make it specific: asking for a resource to start with is better than “can I pick your brain?”. When you’ve made your request, make it low friction for them. If you’re asking for an introduction, write a blurb about yourself which they can forward. If you have a question, ask it in writing rather than over a call. And last on cost, make your ask bounded. Don’t ask for recurring obligations like being your mentor for your whole life, but do keep it limited to asking them to read a blog post. If that instance goes well, they’ll gladly read more.

My last heuristic is stranger: make it easy to say no. You might think that the worst outcome is a no, but the worst outcome is a pressured, begrudging yes. Your coercion will have poisoned your relationship with this person while you feel the false glow of a hard-won victory. A person who helps you with gritted teeth is one who will never help you again. And even then, the help will be a half-hearted effort to get rid of the obligation you manufactured. By contrast, help freely given is effortless, the way you’d hold the door open for someone. Help willingly given keeps your conscience clear, free from the burden of having pressured someone. And help, when given from the heart, is the foundation of a relationship where both of you contribute to what you’re building.

Here is more from Pradyumna Prasad.

Jackson Dahl podcasts with me and Nabeel on aesthetics

Filmed at home, this ran about two hours, and yes that is Nabeel Qureshi, with a cameo from Spinoza toward the very end. From Jackson:

From the episode summary:

Tyler and Nabeel are good friends, and given how prolific Tyler is, I decided to use Nabeel as an entry point and interview them together. We discuss sacred commitments, AI acceleration, mentorship, friendship, and more, but I focused the majority of the conversation on art and aesthetics. Tyler and Nabeel are unlikely aesthetes given their day jobs, but in fact take art deeply seriously. They have a shared love for and similar tastes in art, music, and film, in particular. We discuss strange and beautiful art, aesthetic stagnation, and a wide range of favorites: The Beatles, Mozart, Mondrian, Springsteen, Lana Del Rey, Kanye West, Cassavetes, The Sopranos, Apichatpong Weerasethakul, and more.

https://www.youtube.com/watch?si=wC78q_BeD27XDnLN&v=qPHV-BezoIc&feature=youtu.be

Excerpt:

Tyler: (18:31) I think I’m very mundane in many ways. When Marc Andreessen had that famous tweet about not being too introspective, I know he got slammed for that, but I sympathize with that in many ways. I have my work. I focus on it. I want to go see places I haven’t seen before. That really drives me. I feel pretty well motivated. I do think all kinds of deep thoughts, but to me those deep thoughts feel more superficial than my so-called superficial urges to go around doing things. And I’m fine with that.

…Jackson: (23:25) Do you experience art primarily by thinking or by feeling?

Tyler: (23:29) I don’t even know what those words mean. I experience it by looking at it. I don’t think I have very deep emotional responses. I think it’s pleasure and I feel I learn a lot from it. When I go out and look at other works of art or just the world, I see a lot more than people who don’t live with art. I don’t think I feel that much. I’ve never cried in front of a painting. When I read these accounts of someone seeing a Madonna and weeping, it makes no sense to me. It’s like people who do sports gambling. Why do you do that? There are positive-sum gambles for you. Here are a few.

There is much more of interest, self-recommending!

AI cheating on math econ at Brown

The temptation to use artificial intelligence (AI) to cheat is shaking up elite universities in the United States. Professor Roberto Serrano, who is the Harrison S. Kravis University Professor of Economics at Brown University, has detected a massive fraud in one of the classes he teaches, ECON 1170, an advanced undergraduate course in mathematical economics. He has conclusive evidence that at least 50 students cheated on the March midterm exam, making it the biggest known scandal at Brown and in the entire Ivy League, which brings together the East Coast’s eight most elite private universities, including Princeton, Harvard, Yale, Columbia, Cornell, Dartmouth College and University of Pennsylvania.

When he reported the case to high-ranking officials at Brown, he got a cold reaction. The response from the president, he said, was absolute silence. The dean did not comment either until Serrano took the case before the Academic Code Committee.

Here is the full story, via Anecdotal.

Politically Incorrect Paper of the Day: The US Racial Wealth Gap

Writing in the QJE, Derenoncourt, Kim, Kuhn, & Schularick argue that today’s black-white wealth gap can be explained by differences in initial conditions from over a hundred and fifty years ago, i.e. slavery. But there is an important, and glaring objection: in the age of immigration (1850–1924) millions of whites immigrated to the United States with essentially no wealth and yet they caught up to the “heritage” whites quite quickly and indeed today are richer than heritage whites.

Brian Marein collects and carefully analyzes the data:

Persistent racial wealth inequality in the United States is often attributed to the intergenerational transmission of historical wealth disparities. However, inferring the determinants of long-run inequality from group-level data is complicated by the arrival of 30 million Europeans during the Age of Mass Migration (1850–1924), who are by construction included in average white wealth despite having no direct claim to the wealth accumulated by earlier Americans. This paper accounts for this compositional change in the white population by documenting wealth dynamics among European immigrants and their descendants. Cash-on-arrival data show that immigrants began with substantial wealth deficits relative to the native-born. Yet by the late twentieth century, these deficits had closed, as indicated by comparisons between the descendants of later-arriving Southern and Eastern Europeans and those of longer-established Northwestern Europeans. This pattern implies rapid intraracial wealth convergence, in contrast to the slower convergence observed across racial groups. A stylized model shows that these differences can be largely accounted for by income. These findings demonstrate that large wealth disparities do not mechanically persist when groups have access to comparable economic opportunities.

If initial conditions don’t explain the wealth gap then the most likely explanation is an income and/or savings gaps. I am reminded of an earlier politically incorrect paper of the year by Nathaniel Hilger and see also my review of his book The Parent Trap.

Translated from the Chinese

I think this is the Cursor moment for academia.

The Stanford REAP team has made their move, CoPaper.AI is mass-terminating the manual labor of traditional empirical papers. Link: copaper.ai/landing

If using large models to write papers before was just about polishing and compiling references for you, then this Project from Professor Ross Griebenow’s team at Stanford is like dropping a nuclear bomb in the empirical circles of social sciences and economics.

The greatest truth is the simplest; the heaviest sword has no edge. Its functions are straightforward. Feed in the raw dataset, and within 30 minutes, it can generate a complete DOCX paper complete with full Stata/R code and publication-quality charts.

It chains together EDA, variable definition, econometric model building (from OLS to advanced DID, regression discontinuity, causal forests) all using an Agent workflow.

Every chart it produces comes with 100% reproducible Stata, R, EViews source code underneath. How many low-quality paper mills and data drones’ jobs will this smash?

Data drones and paper ghostwriters are collectively facing unemployment countdown. Because from now on, for social science papers, AI handles all the entropy-increasing drudgery—humans only need to define the problem.

Here is the link. Mostly that is not true, so perhaps the Chinese are trying to demoralize us. But will it never ever be true? In two years be true? Less?

Emergent Ventures winners, 55th cohort

Aliaksandr Melnichenka, Belarus/Kentucky, to support science and math writing.

Guilherme Pinho, Sao Paulo, real estate titling and transactions in Brazil.

Diyar Zhakpelov, Astana, Kazakhstan, 17, exam prep app for Kazakhs, general career support.

Randy Chang, AI policy writings, Ontario/Chapel Hill.

Jesse Casana, Dartmouth, archaeology tranche, “Drone-acquired synthetic aperture radar (SAR), a novel and experimental technology, reveals remarkable perspectives on buried archaeological landscapes in the desert southwest.”

Gia-Bao Dam, New Haven/Yale, longevity research.

Sasha Lempers, Annecy, France, 15, math and AI.

Ali-Mansur Valiyev, Harihar Rengan, Dubai, high school, general career support, educational testing.

Raiani Romanni-Klein, Boston/Cambridge, a non-profit on the implications of biological innovation.

Clara Collier, Oakland, Asterisk magazine.

Scott Ellis, Mississauga, science education tranche, biographies of scientists on YouTube.

Jim Olds, northern Virginia, writings on science policy, science education tranche.

My Conversation with Dave Baszucki

Dave is CEO and co-founder of Roblox, and here is the audio, video, and transcript. From the episode summary:

With over 100 million daily active users and projected revenue bookings of $7 billion this year, it is one of the largest gaming economies in the world—and one that has made millionaires out of teenage developers in Argentina, South Korea, and everywhere in between.

Tyler and Dave explore why Roblox decided early against prioritizing advertising revenue, why Dave thinks the main competition of Roblox is its own execution speed rather than Fortnite, whether every mega platform inevitably becomes an everything app, how falling token costs will change the platform, why he insists all the games on Roblox are beautiful, whether Robux should have a floating exchange rate, why admitting you have kids under 13 on your platform turns out to be a competitive advantage, why he’s skeptical of blanket social media bans, what his son’s experience with bipolar disorder taught him about metabolic health, his two-year sabbatical between companies that involved a motorhome trip across North America and a stint hosting talk radio in Santa Cruz, why Mutiny on the Bounty remains one of his favorite books, what he’ll learn next, and much more.

Excerpt:

COWEN: What percentage of your games now do you feel are beautiful?

BASZUCKI: All of them.

COWEN: Some look just quite ordinary. They might be fun, but I wouldn’t say they’re beautiful, right?

BASZUCKI: Well, I was trying to go a couple levels out of the box on you there. The reason I feel they’re beautiful is when you said that, I immediately went to look and feel, but then I tried to imagine the 12-year-old or the 18-year-old or the 30-year-old struggling to build something wonderful and the human connection to those games. By that definition, I think they’re all beautiful. They are all the efforts of creation of real people trying to pour their hearts out to make something that other people love to play.

On an artistic basis, I think you could ask me what percent of paintings in the MoMA do I think are beautiful. I’d probably say 20 percent. If I had to look at 1,000 Roblox games, I wouldn’t name which is more beautiful to me because I think that’s less important than really the heartfelt work of all the creators.

COWEN: I’ve been struck when I look at gaming at how much people don’t seem to care much about the visual beauty of their games. I would have expected something different, say, 15 years ago, and they just want a game that engages them somehow. Normal standards of visual beauty seem to have fallen away. Is that incorrect? Would you correct that impression in some manner?

BASZUCKI: I think you’re absolutely correct. What I feel you may actually be describing, if we looked into other disciplines, the evolution of story from the campfire to written to audio to a movie, and the increasing fidelity; all of those stories, in a way, are beautiful, but at the time, for the vast majority of the creators, it may be that writing is just easier than producing a 4K Hollywood movie. I feel that’s a little bit like the metaphor you’re talking about right now in gaming.

For the vast majority of people, their story or their idea for their game is actually pretty beautiful. Whether it’s a fashion game like Dress to Impress or it’s a grow garden game, the games are arguably beautiful, even if they don’t look photorealistic. What I think we’ll see is, over time, as AI helps accelerate the ability to make games look really polished in any style the creator wants—could be photorealistic, could be anime, could be a Warner Brothers 2D cartoon look—you and I might say that looks more beautiful, but the core gameplay is still somewhat the original gameplay. I think we are going to see games arguably look more beautiful, even though I think they’re all beautiful.

The dialogue is a bit slow to get underway, but there are many interesting parts.

A Cohort Perspective on Latin America’s Fertility Transition

Latin America’s momentous fertility transition is now in the domain of history, allowing a cohort perspective on the decline of completed fertility. Using census microdata from 17 Latin American countries, we track female birth cohorts from the 1920s to the 1970s by subnational region to document the extent to which cohort fertility decline coincided with other demographic and socioeconomic processes. Across cohorts within subnational regions, children ever born fell one-for-one with mortality decline. Expansions in urbanization, multigenerational living, women’s and husbands’ education, women’s employment, and the non-agricultural sector all predicted declines in ever-born and surviving fertility, but women’s education and sectoral composition were the dominant forces after covariate adjustment. Fertility decline was not systematically linked with improvements in children’s outcomes, including school enrollment, literacy, primary completion, and non-employment. These cohort facts challenge theories of fertility decline centered on women’s work and children’s education but support others emphasizing women’s education.

I fear that means the women think they are finding better and more fun things to do? Which is hardly bad per se, but…

That is from a new NBER working paper by Regina Calles and Tom Vogl.

Do teens regret their social media use?

A new study by Irish researcher Eoin Whelan attempts to answer this. Dr. Whelan told me he was specifically inspired by Haidt’s 2024 claims and sought to examine them rigorously and in the context of other regrets. This is a great use of science…testing dramatic public claims. So…do they hold up?

In Dr. Whelan’s study, 389 young adult participants (20-24) who were social media users as teens were asked about their regrets regarding their teenage years. A list of 20 possible teenage regrets was asked of all participants, with degree of regret marked on a 7-point Likert scale. This is an interesting design…testing social media regrets against other possible regrets, putting them in better context than the crude survey Haidt relied on.

So how did social media regrets hold up? Out of 20 possible regrets, too much time on social media ranked 13th. The top regrets were 1.) not sticking up for oneself, 2.) being too self-conscious, 3.) not documenting memories, 4.) not learning practical life skills and 5.) not getting help with mental health. Girls were slightly more likely to regret time on social media than boys (ranking 11th vs 13th) though this effect was very small (I estimated it at about r = .11) so hardly the big “vulnerable girls” narrative some have peddled.

Further, regrets over time spent on social media as a teen did not predict current young adult life satisfaction for either boys or girls. Thus such regrets may be more a symptom of current panics over social media than anything of actual life importance2. Of the regrets, only not working harder in school and not exercising negatively predicted young adult life satisfaction. Interestingly, having regrets over socializing with friends positively predicted life satisfaction.

As Dr. Whelan noted in his study, “The objective of this study was to critically examine the commonly held belief that social media use during teenage years is a significant source of regret and a predictor of diminished well-being in early adulthood…Contrary to dominant narratives in the public domain, our results suggest that regrets over time spent on social media are not among the most potent regrets reported by young adults…As such, these results align with prior research indicating that the harmful effects of social media may be overstated.”

Here is the full Chris Ferguson Substack.

Educational arbitrage?

Is it really all about the networking? Some people think so, and they are taking action:

Justin Helman didn’t get his dream acceptance from the University of Florida. But that isn’t stopping him from pursuing the classic college experience there.

The recent high-school graduate from Park Ridge, N.J., is set to move into a private apartment right by campus. He is enrolling in a UF online program for the first few semesters and paying an extra fee package to access services like the campus gym and student-section football-game tickets. He plans to study at the library, join clubs and might rush a fraternity.

“I’m going to get almost the entire same experience, and the only thing I’m really missing is going into class and dorming,” he said. “To me, it was just almost a no-brainer.”

More students like Helman are discovering there is another way into their dream schools.

Students who don’t get into major public flagships the traditional way are still participating in the social life of these campuses. The small-but-mighty group is moving to college towns, enrolling in online programs or nearby community colleges, living in private housing, joining Greek life, and attending game-day tailgates.

And it seems the arbitrage runs both ways:

The approach is sanctioned by the universities, which are expanding alternative-enrollment programs. “It’s a way to get what you want if the traditional, standard way doesn’t work,” said Beth Kraemer, a consultant for In College Consulting, who observed an uptick in this trend.

The programs can be a savvy way for universities to protect their rankings and generate revenue, said Adam Nguyen, founder of admissions-consulting firm Ivy Link. These are often students who narrowly missed the admissions cutoff.

Here is more from the WSJ, via Adam B.