Wednesday assorted links

1. Andy Partridge update. What is it like to enter your “withdrawal years”? And what if you had to choose between Partridge and Roy Lichtenstein?

2. Benjamin Yeoh on Talent and the Unconference. And Benjamin does a podcast with Saloni.

3. How is the “Young Right” evolving in Britain?

4. Nurse accused of amputating man’s foot for her family’s taxidermy shop. “Mary K. Brown wanted a sign next to the foot — ‘wear your boots kids’ — other nurses told investigators.”

5. I am excited and hopeful about the new British organisation Civic Future. Next week in London I am doing a dialogue with John Gray for them.

6. More on the problems with the current system of clinical trials.

7. Ed Prescott still underrated! But understood by many.

The election results

I have no interest in discussing them, other than to note the median voter theorem is alive and well. But if your mood affiliation needs yet another outlet, the comments section is open.

Switzerland markets in everything

Switzerland, one of the world’s richest nations, has an ambitious climate goal: It promises to cut its greenhouse gas emissions in half by 2030.

But the Swiss don’t intend to reduce emissions by that much within their own borders. Instead, the European country is dipping into its sizable coffers to pay poorer nations, like Ghana or Dominica, to reduce emissions there — and give Switzerland credit for it.

Here is an example of how it would work: Switzerland is paying to install efficient lighting and cleaner stoves in up to five million households in Ghana; these installations would help households move away from burning wood for cooking and rein in greenhouse gas emissions.

Then Switzerland, not Ghana, will get to count those emissions reductions as progress toward its climate goals.

Here is more from Hiroko Tabuchi at the NYT. Note that most of Swiss energy already is renewable, through hydroelectric and nuclear, yet of course there are many people complaining about this scheme.

Austrian business cycle theory today

That is the topic of my latest Bloomberg column, excerpt:

One reason the current economic situation is so fraught is that the world is facing three kinds of business-cycle mechanisms at the same time. The first two are well-known, but the third — known as the Austrian theory of the business cycle — is not.

And in more detail:

When the combination of high inflation and pending disinflation came along, real interest rates spiked upwards. It is difficult to estimate the current level of expected future real interest rates, because market participants disagree about the likely future course of inflation. Nonetheless, market prices are indicating that traders expect higher interest rates to continue through the decade, if not longer. Anecdotal evidence from secondary capital markets, such as venture capital, is strongly consistent with the notion of capital being harder and more costly to obtain.

The more significant issue concerns a decline in long-term building and long-term projects.

The decline in asset prices came first to crypto in late 2021. Crypto was originally marketed as a hedge against inflation, but the data have refuted that idea. Instead, crypto has become a project to build out a new and different kind of financial system. That project has been years in the making, and even true believers admit that the revolution is years away, if it comes at all.

In fact, at higher real interest rates — in essence, higher rates of discount — the project looks less appealing. It is striking that crypto prices, which are about the least “establishment-determined” of all major classes of asset prices, were to first to register this change in market expectations.

Major tech companies have also seen their valuations fall significantly due to higher interest rates. Whatever else they may be, Meta, Alphabet and Amazon are also some of America’s more promising corporate research labs, and now they don’t have the resources they did less than two years ago. Their successors will have a hard time as well, due to rising capital costs, again at the expense of innovation and America’s collective future.

I am always struck by both a) how many economists will badmouth the Austrian theory, and b) how many of the same will resort to some partial version of it to explain current events.

Matt Levine on the events of the day

Do black NBA players play better without the fans?

In the NBA, predominantly Black players play in front of predominantly non-Black fans. Using the ‘NBA bubble’, a natural experiment induced by COVID-19, we show that the performance of Black players improved significantly with the absence of fans vis-\`a-vis White players. This is consistent with Black athletes being negatively affected by racial pressure from mostly non-Black audiences. We control for player, team, and game fixed-effects, and dispel alternative mechanisms. Beyond hurting individual players, racial pressure causes significant economic damage to NBA teams by lowering the performance of top athletes and the quality of the game.

That kind of causal mechanism is difficult to demonstrate, but perhaps there is something to this. Alternatively, how about the “fewer distractions in the bubble effect”? Entourage effect? etc. How could they miss this possibility? Here is the full paper by Mauro Caselli, Paolo Falco, and Babak Somekh. Via the excellent Kevin Lewis.

Tuesday assorted links

1. James Broughel on classical liberalism and anti-intellectualism (and me).

2. History of private turnpikes in 19th century Britain.

3. Native Americans and adoption law — the whole mess doesn’t make much sense. Does that mean it is more likely or less likely to persist?

4. Japanese government seeks the power to turn down private home air conditioners remotely.

5. The Disciple is quite a good movie, and a good introduction to Indian classical music, at least on the vocal side.

Three Billion Dollars Found in a Popcorn Tin

In September of 2012 James Zhong used a hack to steal approximately 50,000 bitcoin from the dark web’s Silk Road. Yesterday the US Attorney announced that just last year they had arrested Zhong and recovered almost all of the stolen bitcoin. Here’s the amazing bit:

On November 9, 2021, pursuant to a judicially authorized premises search warrant (the “Search”), IRS-CI agents recovered approximately 50,491.06251844 Bitcoin of the Crime Proceeds from ZHONG’s Gainesville, Georgia, house. Specifically, law enforcement located 50,491.06251844 Bitcoin of the approximately 53,500 Bitcoin Crime Proceeds (a) in an underground floor safe; and (b) on a single-board computer that was submerged under blankets in a popcorn tin stored in a bathroom closet.

At the time the Bitcoin was worth $3 billion dollars. Lots to think about here. Are they going to give the money back to Silk Road users? Will they burn it? If not isn’t this just seignorage going to the US government? How can you walk by $3 billion in your closet every day and not spend it? What willpower! Why didn’t Zhong move to say Morocco?

Requests from Benedikt

4. James Steuart- overrated or underrated

5. Do border regions have above average cuisines (Sechuan, Bourgogne)

6. Zurich- overrated or underrated

Are there some great ethnic restaurants I haven’t heard of?

7.Would you have been a pagan or a Christian In the third century AD roman empire?

12. How would you compare the Swiss to the Irish enlightenment?

13. What is your Swiss take in general?

With numbers:

4. James Steuart was a Scottish economist and a precursor of Adam Smith, though more of a mercantilist. He had a good understanding of market structure, competition as a process of dynamic rivalry, and outlined how increasing competition would cause monopolistic prices to fall. He put forward a rudimentary understanding of supply and demand in his 1767 treatise. His macroeconomics is sometimes considered a precursor of Keynes, as it was demand side-oriented. He also put forward the idea of a purely abstract unit of account. Yet he isn’t talked about much, so definitely underrated.

5. Do border regions have better food? What exactly counts as a border region? The parts of the United States near Canada? The best food in Italy is not obviously at the (rather skimpy) borders. China and India might be the best food countries in the world, but because they are so large most of their cuisine is not “border cuisine.” So I say no.

6. Zurich is underrated, by everyone and everything, except the market prices for the real estate. The underrated side of the city includes the art scene (most of all the Kunsthaus), good ethnic food in the nooks and crannies, proximity to many good Swiss and German opera houses, proximity to the southern Schwarzwald, proximity to Basel, and proximity to Wallensee and many other wonderful short drives in Switzerland.

7. I still have the choice to be either a pagan or a Christian, and I am neither. Perhaps the same would be true for 3rd century AD Roman Empire Tyler.

12. I see the Swiss Enlightenment as centered in Albrecht von Haller, a mid-18th century poet (Die Alpen), scientist, polymath, and naturalist. I see the Swiss Enlightenment as focusing on two themes: a) coming to terms with a naturalistic rather than theological understanding of the beauties and world around them, and b) constructing an idealized narrative about Switzerland itself and its history and lifestyles. See also Salomon Gessner and Johann Jakob Bodmer. Can you count the Rousseau of this period as Swiss? Geneva had not yet joined the Swiss Confederation, but that is possibly another angle. How about the influence of Switzerland on Edward Gibbon?

13. My Swiss take in general is that the country and its success is radically understudied by outsiders.

China fact of the day (with the usual grain of salt)

Nucleic Acid Testing 'Now Accounts for 1.3% of China’s GDP' https://t.co/sFw8zdNdk1

— That's Shanghai (@ThatsShanghai) November 7, 2022

Lu Wei Peter Zhang

If you want to open a new Peter Chang restaurant in Fairfax, but not quite tell people it is Peter Chang…call it Peter Zhang! (Isn’t that a bit like hiding the kid from Anakin Skywalker and calling him Luke Skywalker?)

This is the most casual outpost in the Chang empire, by far. You order from a screen and there are only a few tables. Many of the dishes are marinated meats from central China, with some hot pot, noodles, and semi-Sichuan options. It is the “most Chinese” of the current Chang portfolio. Here is some basic information. I’ve only been once, and haven’t yet figured out the best dishes, but you should all know about this right away. It is near the intersection of Rt.50 and 123, centrally located for Fairfax.

Self-recommending.

Monday assorted links

1. Are people in rice-farming areas less happy on average? (speculative)

2. Individualism and the decline of homicide (but does this hold in the broader cross-section?)

3. Earlier Twitter markets in everything.

4. The economics of writing crossword puzzles.

5. Andres Serrano “cancelled” again, this time for being (supposedly) pro-Trump.

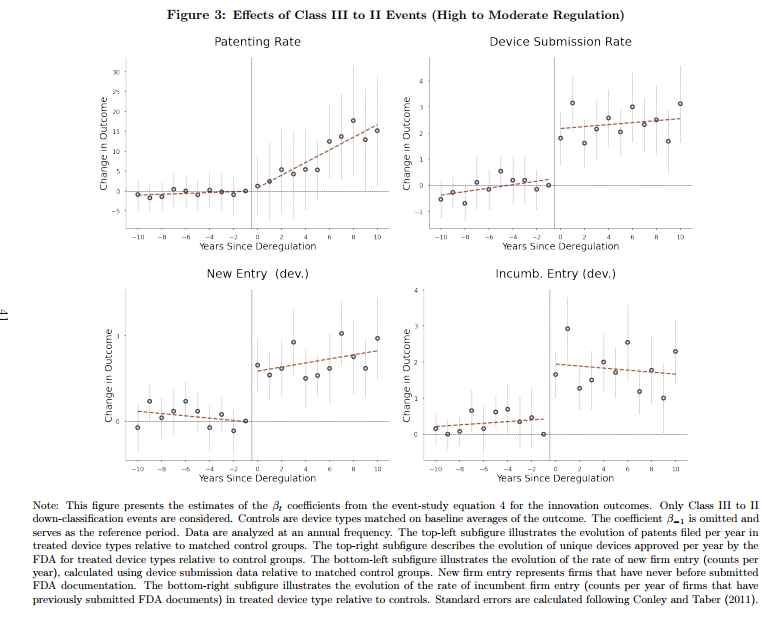

FDA Deregulation Increases Safety and Innovation and Reduces Prices

In an important and impressive new paper, Parker Rogers looks at what happens when the FDA deregulates or “down-classifies” a medical device type from a more stringent to a less stringent category. He finds that deregulated device types show increases in entry, innovation, as measured by patents and patent quality, and decreases in prices. Safety is either negligibly affected or, in the case of products that come under potential litigation, increased.

After moving from Class III (high regulation) to II (moderate), device types exhibited a 200% increase in patenting and FDA submission rates relative to control groups. Patents filed after these events were also of significantly higher quality, as measured by a 200% increase in received citations and market valuations. These effects do not spill over into similar device types.1 For Class II to I deregulations, the rate of patent filings increased by 50%, though insignificantly, and the quality of patent filings exhibited a significant 10-fold improvement, suggesting that litigation better promotes innovation.

…Down-classification yields considerable benefits, as the proponents of deregulation would predict, but what of product safety? Perhaps counterintuitively, I find that deregulation can improve product safety by exposing firms to more litigation. Despite some adverse event rates increasing after Class III to II events (albeit insignificantly), Class II to I events are associated with significantly lower adverse event rates.3 My analysis of patent texts also reveals that inventors focus more on product safety after deregulation. These results suggest that litigation encourages product safety more than regulation…

Some background. Medical devices are regulated under three categories. New types of devices (new, not necessarily high risk) are highly regulated Class III devices which must go through a pre-market approval process to prove safety and efficacy (like new drugs). The pre-market approval process is time-consuming and expensive but it comes with one significant benefit, federal preemption of state tort action, i.e. these devices are shielded from product liability. Class II devices are devices that are judged to be substantially equivalent to an already approved device–proving equivalence also takes time and money but it’s less onerous than proving safety and efficacy de novo. Note that device manufacturers often make their devices less innovative so they can be approved as Class II devices rather than as Class III devices. Class II devices are mostly also protected against tort litigation. Class I devices are not FDA-approved and are subject to tort litigation.

As experience develops with new devices such that new devices turn out to be not especially risky, the FDA sometimes deregulates or down-classifies these devices from Class III to Class II or from Class II to Class I. Rogers studies these down-classifications by comparing what happens to the down-classified device category to a control group of similar devices that were not down-classified. The control group is critical and Rogers shows that his results are robust to defining the control group in a variety of plausible ways. Some of the key results are shown in the following figure:

Nicely we see that device submissions and new entry occur very quickly once a device is down-regulated which indicates that firms have ideas and products on-the-shelf but they are dissuaded from entering the market by the onerous pre-market approval process. Most likely, these are products and firms which produce devices for the European market which tends to be less regulated and they enter the US market only when costs are reduced. Patenting also increases in the down-regulated device category and–exactly as one would expect–this takes more time.

Nicely we see that device submissions and new entry occur very quickly once a device is down-regulated which indicates that firms have ideas and products on-the-shelf but they are dissuaded from entering the market by the onerous pre-market approval process. Most likely, these are products and firms which produce devices for the European market which tends to be less regulated and they enter the US market only when costs are reduced. Patenting also increases in the down-regulated device category and–exactly as one would expect–this takes more time.

Safety declines non-significantly if at all from Class III to Class II deregulations and increases for Class II to Class I deregulations. That makes the welfare comparisons easy because deregulation appears to be all benefit and no cost. Note, however, that I have always argued that drugs and devices are actually too safe–that, is we could save more lives on net by approving more drugs and devices even if safety went down. That’s a hard sell, however, but it’s clearly true that given the results here we should deregulate or down-classify many more products even if safety declined on the margin. Too much safety is risky. That’s also the upshot of my paper on off-label prescribing which shows that it’s often the FDA-unapproved off-label use which is the gold-standard treatment in fast moving fields of medicine.

Rogers argues that safety increases for Class II to Class I deregulations because liability is a stronger deterrent on the margin than regulation (and he provides some evidence for this view in that safety increases more among larger firms that are less judgment proof than small firms). Without denying that mechanism my view is that innovation itself increases safety. As I noted above, medical device manufactures often do not use the latest technology in their products because this would threaten the “substantial equivalence” test so you get devices that are actually less safe and also more costly to manufacture than necessary. In essence, substantial equivalence anchors new technologies to old technologies thus preventing movement, even movement towards safety and lower prices.

Rogers also has an excellent and unusual paper (with Jeffrey Clemens) on directed innovation in artificial limbs due to the civil war! That paper and this one show a real focus on digging deep into the data to unearth important and unusual sources of insight. N.B.! Parker Rogers is on the job market.

Addendum: See my many previous posts for more useful references on the FDA, especially Is the FDA Too Conservative or Too Aggressive.

Modeling persistent storefront vacancies

Have you ever wondered why there are so many empty storefronts in Manhattan, and why they may stay empty for many months or even years? Erica Moszkowski and Daniel Stackman are working on this question:

Why do retail vacancies persist for more than a year in some of the world’s highest-rent retail districts? To explain why retail vacancies last so long (16 months on average), we construct and estimate a dynamic, two-sided model of storefront leasing in New York City. The model incorporates key features of the commercial real estate industry: tenant heterogeneity, long lease lengths, high move-in costs, search frictions, and aggregate uncertainty in downstream retail demand. Consistent with the market norm in New York City, we assume that landlords cannot evict tenants unilaterally before lease expiration. However, tenants can exit leases early at a low cost, and often do: nearly 55% of tenants with ten-year leases exit within five years. We estimate the model parameters using high-frequency data on storefront occupancy covering the near-universe of retail storefronts in Manhattan, combined with micro data on commercial leases. Move-in costs and heterogeneous tenant quality give rise to heterogeneity in match surplus, which generates option value for vacant landlords. Both features are necessary to explain longrun vacancy rates and the length of vacancy spells: in a counterfactual exercise, eliminating either move-in costs or tenant heterogeneity results in vacancy rates of close to zero. We then use the estimated model to quantify the impact of a retail vacancy tax on long-run vacancy rates, average rents, and social welfare. Vacancies would have to generate negative externalities of $29.68 per square foot per quarter (about half of average rents) to justify a 1% vacancy tax on assessed property values.

Erica is on the job market from Harvard, Daniel from NYU. And they have another paper relevant to the same set of questions:

We identify a little-known contracting feature between retail landlord and their bankers that generates vacancies in the downstream market for retail space. Specifically, widespread covenants in commercial mortgage agreements impose rent floors for any new leases landlords may sign with tenants, short-circuiting the price mechanism in times of low demand for retail space.

I am pleased to see people working on the questions that puzzle me.

Ed Prescott has passed away

I have received multiple confirmations. Very sad, he was one of the true greats and ended up quite underrated. Here are some earlier MR posts about Prescott.