Category: Law

Estimating the Economic Value of Zoning Reform

We estimate the economic value of zoning reform in São Paulo, which altered maximum permitted construction along transportation corridors. Developers increased filings for multifamily construction in blocks affected by the reform, leading to more housing supply and lower housing prices in neighborhoods that allow more densification. Our equilibrium model of housing markets estimates an aggregate 1.6 percent increase in housing stock and a 0.4 percent reduction in prices, resulting in large housing wealth transfers from current to future homeowners. The reform produced welfare gains of 0.65 percent of city GDP, mostly due to developer profits and consumer gains from the newly built environment.

That is from the AEA policy journal, by Santosh Anagol, Fernando Ferreira, and Jonah Rexer.

The economics of H-1B immigration

We study the effects of H-1B immigration on U.S. industries that employ H-1B workers and their trading partners. Using a novel cross-industry design and the 1999–2003 expansion of the H-1B visa cap for identification, we find that H-1B exposure raised incomes for natives and pre-existing immigrants, with gains concentrated in non-STEM occupations. Income gains propagate forward through supply chains to downstream industries but not backward to upstream industries, consistent with a productivity shock rather than a labor supply shock. We find no direct effect on patenting, suggesting that productivity gains arise from better task execution rather than patentable invention.

That is from a new NBER working paper by

The Apples and Oranges Tribunal

Suppose that apples sell for more than oranges and Parliament in it’s wisdom decides that, at last, apples and oranges must be compared. Not by shoppers — shoppers are biased, they merely reveal what they are willing to pay — but by a tribunal, which will determine whether apples and oranges are of truly equal value and thus must sell at the same price.

What would the tribunal need to know?

Start with land. Orange groves sit on Florida real estate with one set of alternative uses; apple orchards occupy Washington hillsides with another. The opportunity cost of an orange includes the housing development, the solar farm, the tourist attraction not built on that grove. How is the tribunal to value what was never built? Perhaps you answer: look at land prices. Brilliant suggestion, I reply. Keep going.

Next, capital. Orchards take years to mature, so today’s fruit embodies investments made under yesterday’s expectations about today, financed at interest rates the tribunal must somehow incorporate. Then storage: apples keep, oranges rot, so an apple and an orange in April are different goods than the “same” fruits in October. Add transportation, refrigeration, frost, pests, crop insurance, the option to divert fruit into juice, cider, marmalade, or pie, substitution with every other item in the produce aisle, and the shifting preferences of millions of consumers, each of whom knows things about his own breakfast that he could not articulate to a tribunal. It all matters.

To determine the “just” price of apples and oranges, the tribunal would need the entire general-equilibrium system.

Market prices are necessary to compare alternative uses of resources, as Mises taught us in 1920. In 1945, Hayek added the knowledge problem: the relevant knowledge is dispersed, local, tacit, and fleeting. Free markets are the only institution that aggregates that knowledge, articulates it in prices and gives people a reason to listen and respond. A price is a signal wrapped up in an incentive. Apples and oranges can be compared but only by the incomparably complex operations of the price system. There is a reason we call it the super-market.

Britain is now running this experiment in the labor market–Is a retail worker equal to a warehouse worker? A canteen worker equal to a coal miner? A dinner lady equal to a gravedigger?

Under the Equality Act’s “equal value” provisions, tribunals compare jobs by scoring their intrinsic properties — effort, skill, responsibility, working conditions — the labor theory of value applied to labor. How is it going? The Tesco litigation began in 2018; the tribunal’s fact-finding hearing ran 36 days, its judgments run to more than 900 pages resting on some 19,000 pages of training manuals, and the independent experts have yet to begin the report that will actually say whether a shelf-stacker’s job equals a warehouse worker’s. Eight years, and the calculation has not started. Apples and oranges, adjudicated but not, as Orwell or Marx or Stafford Beer might have imagined, by a industrial bureaucracy or by an all-knowing artificial intelligence but by lawyers and commissions and tribunals. The worst of all worlds.

And having discovered that the tribunal cannot price two jobs in a decade, the government now proposes to add race and disability comparisons and an enforcement unit to publish official guidance on which reasons for a wage difference are permissible. A bureau of allowable scarcities.

Moreover, let us say that one day the tribunal reaches its conclusion and finds the truly just apple to orange price. At last, nirvana. The next day the public learns that vitamin C really does combat cancer–the demand for orange juice skyrockets. To encourage more orange juice production we need a higher price but wait…nothing about oranges or apples or the labor required to produce them has changed. We need to attract more labor to the orange juice industry but the effort, skill, responsibility and working conditions of orange juice workers has not changed. How can we justly pay them more than their apple juice brethren? Blank out.

The market compares apples and oranges every day. It is the only institution that can. But there is a deeper error here than computation. Suppose the tribunal succeeded. Suppose that after another decade it delivered the true and final score, shelf-stacker versus warehouseman. What would it have found? Not justice. A wage is not a grade on your character or a measure of your worth as a human being. A wage is a price — a report on how scarce your skills are relative to the desires of people you will never meet. Nurses are not morally less worthy than plumbers should they earn less than plumbers or vice-versa, and no one thinks otherwise except the tribunals.

Hayek nailed it in The Mirage of Social Justice: justice is about conduct — how one person treats another. An employer who defrauds his workers, an employee who steals from the till, a product sold under false pretenses — condemn them, take them to court. But the pattern of prices that emerges from millions of voluntary trades is nobody’s conduct. No one chose it, no one designed it, no one can be guilty of it. The constellation of prices is, in Ferguson’s phrase, the result of human action but not of human design. Demanding that prices be just is a category error, like suing the weather. Prices don’t grade our merit; they guide our actions. Ask them to do the first and they can no longer do the second.

Judge Anthony Kennedy said it well in the Ninth Circuit ruling that (mostly) killed comparable worth in the US: “neither law nor logic deems the free market system a suspect enterprise.”

Talk Therapy is Speech

IJ: On Wednesday, the United States District Court for the District of Columbia struck down a D.C. law that barred therapists from other jurisdictions from doing online teletherapy visits with clients in D.C. The decision comes nearly six years after Virginia-based counselor Elizabeth Brokamp teamed up with the Institute for Justice (IJ) to file a lawsuit arguing the law violated the First Amendment.

“This decision is a victory for anyone who speaks for a living,” said IJ Deputy Director of Litigation Robert McNamara. “Elizabeth’s victory here confirms that the First Amendment protects useful speech, including counseling, and that licensing boards can’t censor speech simply because someone doesn’t have their permission to talk.”

Congrats to the IJ! Now, we need to get rid of all the other bans on patients hiring physicians from other states. As I wrote last year:

During the pandemic, many restrictions on telemedicine were lifted, making it far easier for physicians to treat patients across state lines. That window has largely closed. Today, unless a doctor is separately licensed in a patient’s state—or the states have a formal agreement—remote care is often illegal. So if you live in Virginia and want a second opinion from a Mayo Clinic physician in Florida, you may have to fly to Florida, unless that Florida physician happens to hold a Virginia license.

The standard framing says this is a problem of physician licensing. That leads directly to calls for interstate compacts or federalizing medical licensure. Mutual recognition is good. Driver’s licenses are issued by states but are valid in every state. No one complains that Florida’s regime endangers Virginians. But mutual recognition or federal licensing is not the only solution nor the only way to think about this issue.

The real issue isn’t who licenses doctors. It’s that patients are forbidden from choosing a licensed doctor in another state. We can keep state-level licensing, but free the patient. Let any American consult any physician licensed in any state. That’s competitive federalism—no compacts, no federal agency, just patient choice.

Hat tip: Joel Selanikio.

European Fact of the Day, Again

This year, like last year, “the European Union will again make more money from fining US tech companies Than from the total tax income from Europe’s own public tech companies!”

Alex Tabarrok on the Economic Analysis of Crime

I tell my Gary Becker story, why I like police more than prisons, how criminals are like children and more.

Alec Stapp on the new Science report from Michael Kratsios

Major new report from the White House Office of Science and Technology Policy. Five things in the report I really liked:

1. Proposes metascience units as a way to advance experimentation in science agencies. IFP recommended OSTP take this forward in our response to a 2025 RFI.

2. Advocates for a portfolio approach to federal science funding. Right now, basic research funding largely goes to incremental, project-based grants. While important, they can’t be the only mechanism we use to fund science.

3. Recognizes the need to launch new institutions. It specifically highlights X-Labs as an experiment with independent labs that can take on ambitious challenges. This is a bipartisan idea whose time has come.

4. Focuses on a mix of innovation funding mechanisms, including fast grants, prizes & challenges, and advance market commitments. We described and contextualized these ideas in the Atlas of Innovation, which can help policymakers design and implement these approaches.

5. Seeks to reduce burden for American scientists, who face mountains of paperwork. Scientists should spend more time doing science and less time writing/reporting on grant proposals and working to meet regulatory requirements.

Here is the link, here is the report itself, by Michael Kratsios, Science a New Golden Age. Overall, less money will be given to universities and more will be spent on AI-assisted science. Here are further observations from Seth Bannon.

Words of wisdom on Chinese AI and our responses

The strategy for China is obvious: commoditize your complements. Note that Xi explicitly ties openness to AI “moving from the digital world into the physical world”; the physical world is the world dominated by China, and the country’s lead in areas like robotics is going to massively benefit from widely available AI models.

Along the same lines, China does not want the U.S. to gain an asymmetric advantage in AI; to the extent that China can weaken the U.S. frontier labs while strengthening any and all potential U.S. adversaries so much the better, and it can benefit from the innovation that will attach itself to an open ecosystem.

And in sum:

The better course is clear: first, loosen Fable and Sol restrictions on cybersecurity, and second, ensure that U.S. open weight model makers are on an equal playing field with China. Yes, the frontier labs will kick and scream about this, but the Administration should realize that listening to their histrionics has led the U.S. to a position where U.S. companies are dependent on China for their defenses. Let the frontier labs win by being better; don’t let them define safety or security, or pull up the ladder of humanity’s collective knowledge. China is already hard enough to compete with; letting them carry the standard for openness and innovation is simply giving away our biggest advantage.

That is from Ben Thompson’s Stratechery (gated, but ungated link here).

Building luxury homes is good for the poor

Tej Parikh writing in the FT:

…high-end developments unlock long housing chains. As higher-income households move into newly built units, they free up older properties, raising supply and slashing prices for middle- and lower-end housing through a process known as filtering. Numerous international studies underscore this positive ripple effect.

One published last year tracked households that moved into a newly built 512-unit condominium tower in Honolulu, Hawaii. It found that the building created at least 557 vacancies in older and cheaper apartments across the city in just three years, with market-rate units more likely to release the largest chains.

Filtering can also be widespread. A 2021 study in Helsinki using geo-coded population data found that every 100 new market-rate units in the city centre led to around 60 units becoming available in the city’s bottom half of neighbourhoods by income. An analysis across all homes in Sweden over several decades concluded that “new homes, even those initially primarily inhabited by rich people, lead to substantial trickle-down effects that also benefit the poor”.

Other US studies highlight how market-rate developments benefit less well-to-do local residents by lowering housing costs. In San Francisco, a 2021 paper found new developments lowered the risk of eviction notices for residents in rent-stabilised housing. Even “luxury” developments in New York City — which Mamdani has criticised — have been shown to contribute to lower local rents and sales prices.

or David Attenborough:

What should I ask Luis Garicano?

Yes I will be doing a Conversation with him. From Wikipedia:

Luis Garicano Gabilondo (pronounced [ˈlwis ɣaɾiˈkano]; born 1967) is a Spanish economist and politician who was a Member of the European Parliament (MEP) from 2019 to 2022. He was also vice president of Renew Europe and vice president of the European political party Alliance of Liberals and Democrats for Europe (ALDE Party). Before entering politics, he was a professor of strategy and economics at IE Business School in Madrid and at the London School of Economics (LSE). After leaving the European Parliament he has returned to academia as a visiting professor at Columbia Business School and at the University of Chicago Booth School of Business. In 2023, returned to LSE as full professor at the School of Public Policy.

He is one of the leading European economic liberals, here is his home page. Here is his Google scholar page. Here is Luis on Twitter. he also has a very good book coming out called Messy Jobs, co-authored with Jim Li and Yanhui Wu. So what should I ask him?

Why crime will decline in (most of) Brazil

The system, introduced in 2024, uses facial recognition to spot people wanted by police on São Paulo’s streets. It issues alerts and officers are dispatched to pick them up. The system can also locate people who have been reported missing, identify stolen vehicles and provide footage to police investigations. Streamed to its control room in the city centre, information flows not just from lenses on street corners but in health centres, on buses and mounted on police motorbikes. By 2028 the number of cameras in the network is supposed to double, to 100,000.

São Paulo is one of many Brazilian cities spending big on crime-fighting technology. As in other countries, police are investing in body-worn cameras and networks of microphones that detect the sound of gunshots. What sets Brazil apart from many democracies is its enthusiasm for face-spotting tech. Researchers for O Panóptico, a watchdog, count 560 active facial-recognition projects in more than 20 Brazilian states. These include police-run initiatives but also experiments in schools, for example, where cameras are increasingly being used to take attendance. They gaze upon some 99m people, more than 47% of Brazil’s population.

Here is more from The Economist.

Governing agentic AI

From a new paper by Shruti Rajagopalan:

AI agents now transact, publish, and act on external systems without contemporaneous human approval, creating new regulatory challenges. A growing literature has responded with proposals for legal personhood. This Article argues that personhood is neither necessary nor sufficient, shifting the question from status to enforcement. The Article first shows that for two millennia, nonhuman legal personality, from the Roman universitas to the corporation, the Hindu idol, the waqf, and the river, has operated through human officeholders the law can locate, question, prosecute, and replace. Agentic AI inverts that design, exercising practical agency without legal status, sometimes with no identifiable human in the responsibility-bearing role. The Article then sorts deployments into three categories: first, where one firm builds and deploys the agent; second, where the developer and deployer are separate but known; and third, where there is no identifiable developer or deployer. The Article stress tests each agent deployment category against five liability doctrines: agency law, products liability, enterprise liability, negligence, and strict liability. It demonstrates that each fails at different points in the third category for the same reason: the absent responsibility-bearer. Bare personhood would supply a caption without a representative, assets, or a mechanism for cessation. Finally, the Article assembles an alternative from regimes governing aircraft, ships, drones, driverless cars, and motor carriers. It develops a six-layer stack—registration, identification, verification, financial responsibility, lifecycle traceability, and suspension—so a responsibility-bearer can be identified, liability imposed, and the activity suspended. These layers place the human back at the end of the chain.

I would say that social science now has new frontiers, let us hope it blossoms in response.

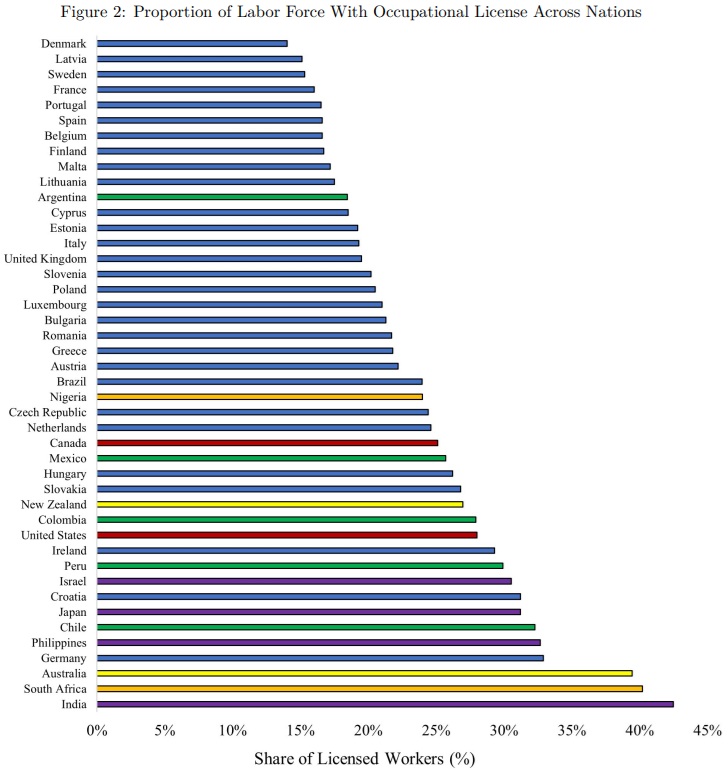

Occupational Licensing Around the World

Hartley and Kleiner have a new Fed Minneapolis working paper surveying workers around the world to measure occupational licensing by country. In the United States, occupational licensing has increased substantially over time, so one might expect licensing to rise with income. Their headline result is the opposite: occupational licensing is negatively correlated with GDP per capita. Many developing countries such as India, South Africa, and the Philippines have a lot of occupational licensing while Denmark, Sweden and France have relatively little. Similarly, countries which rate poorly in measures of government quality, such as regulatory quality, political stability, the rule of law, and corruption have more occupational licensing.

I do have some concerns, however. The figure for India of 42% of workers requiring a government license seems too high. Admittedly this is the home of the License Raj but I worry about the survey results. In order to mark a surveyed worker as requiring an occupational license HK require that the worker say that a) they have a license and b) a license is required to work in their profession. But in India there are many workers who do not have a license and a license is required to work in their profession–HK, however, consider these workers confused and drop them from the analysis. That is appropriate for a developed country where there aren’t many illegal unlicensed workers but, as the authors later discuss, informality is very high in India so working illegally is not uncommon.

Including these workers would make the true India figure even higher than HK report but I think with such a high degree of informality we also have to wonder whether survey responders in India really are responding the same way as in Germany. Perhaps they are reporting a license isn’t really required since very few workers have one. In India, for example, some 60% of “licensed” drivers have an fake or invalid license and many have no license at all so maybe workers are just reporting the facts on the ground.

Within the United States, professions are regulated in some states but not others—Louisiana, for instance, requires florists to be licensed. (Do license-holding Louisiana florists produce better, safer arrangements? I don’t think so.) Given this variation even within a single country, we’d expect considerable variation across countries too. Multiple independent surveys—not just HK—confirm that Denmark, Sweden, and even France have less occupational licensing than the United States. Since these countries have high state capacity, we can rule out the hypothesis that licensing exists for safety or quality. The implication is clear: occupational licensing is often about rent-seeking, not quality assurance.

Addendum: See also my review of Allensworth’s The Licensing Racket which finds that licensing board spend most of their time and effort on regulating entry rather than quality and my paper on the surprise delicensing of occupational licensing in the funeral industry in Colorado.

The Trump Administration’s Threat to Scientific Research

In The Nationalization of American Science I warned that the Trump administration’s rewriting of the seemingly mundane Regulation for Federal Financial Assistance was a tremendous threat to America’s historically successful decentralized system of science funding. Many others are now sounding the alarm.

It’s not surprising that organizations like the AAAS oppose the rule, albeit with unusually strongly worded dissents:

This latest move is a brazen power grab by the Director of the Office of Management and Budget to buck the will of Congress and the American people and will make future discoveries less likely. If this rule becomes final, Americans’ hopes for future cures, national security and economic strength will rely on the scientific sensibilities of the nation’s chief bureaucrat. Alzheimer’s disease will not be cured by a budget analyst from either political party.

But we are now seeing strong pushback from independent thinkers such as:

Grayson Logue writing at The Dispatch:

A sweeping new rule proposed by the Trump administration could remake how that money is awarded and give the president and his political appointees discretion to cancel funding or target recipients for virtually any reason—with little opportunity for recourse.

White House officials argue the new rule is necessary to assert more accountability over federal grantmaking, but observers fear the shift will expand opportunities for politicization, abuse, and even corruption for an administration that has already demonstrated a penchant for using the levers of the federal government to punish partisan enemies and reward ideological allies.

if I was trying to ruin American leadership in scientific research this is pretty much the kind of rule I would write…One of the genuine difficulties with observing the second Trump term is that the assault on state capacity and impartiality has been so multipronged that it is difficult to keep track of everything going on. But these proposed rule changes are monumental and catastrophic.

and Noah Smith:

MAGA’s attack on science is even worse than it looks…despite science’s overwhelming popularity and public trust, Trump and his administration are launching an unprecedented and devastating attack on American science — cutting funding, and forcing science projects to undergo ideological review by government commissars.

It may be that the Trump administration has pushed too far, but my real worry is that we are losing an equilibrium. Science was never completely independent of politics, of course, but even at the worst of times, funding was decentralized and the culture-war material that dominated the headlines was never more than a tiny fraction of the whole. Like an independent judiciary, independent science has been an American virtue. COVID policy, gender policy, and now the Trump administration’s weaponization of these mistakes may have destroyed that equilibrium.

As I wrote in my original post, we are adopting the loser policies of authoritarian nations but those policies are the norm elsewhere for a reason. Centralized control of science is the default because it serves the people in power of whatever party. Decentralization is the fragile exception—a historically unusual achievement that is easier to destroy than rebuild.

Addendum: And here is Andrew Gelman.

New space policy Substack from Mercatus

We are Rebecca, Max, and Aakrith. We are researchers at The Mercatus Center, a research organization dedicated to classical liberal ideas. Rebecca is a philosopher, Max is an economist, and Aakrith is a political scientist. Together, we are the Space Team, and this is our Substack.

We’re here to persuade you that space policy is increasingly important. And that getting space policy right offers humankind astonishing opportunities. In particular, we’re currently thinking hard about innovation, competition, federalism, property rights, and life in space.

Here is the link.