Month: October 2014

Where is the external social value for marginal book reading?

Let’s assume books — at the margin of course — bring some external social value, perhaps by stimulating ideas production or by improving the quality of voting and citizenship. If that were the case, at which margin should we look for this external benefit? I can think of a few possibilities:

1. More books should be produced. Yet this hardly seems plausible, as there are so many books produced right now and most of them are largely ignored. In any case, Amazon clearly makes a larger number of books readily accessible, although its lower prices may discourage the number of books longer run.

2. Better books should be produced. Arguably this is true by definition, but it is not a useful means of evaluating most proposed changes to the book market. That said, Amazon creates an open forum for useful reviews. That may improve long-run book quality, or at least lead to a more useful matching of readers with books.

3. Books should be cheaper and thus purchased and read more often. Maybe so, but public libraries give books away for free — great books too — and their shelves are not stripped bare. So making commercial books cheaper will get us only so far. If all books were completely free, reading would go up by only so much, because time and attention would remain scarce. In any case, with reference to the recent debates, Amazon does in fact make books cheaper.

4. Books should be more vivid in the minds of readers. People would read more if the books meant more to them and that is a more effective lever than simply making books cheaper. You will note of course that “buzz” can make books more vivid, and so Piketty’s Capital became a vivid book for a large number of people. They bought it, though most of them did not read past page 26. So even making books more vivid will not necessarily bring about the desired end of additional interested readership. That said, Amazon does create various lists to try to boost the buzz around books, and Amazon tries to raise the relative status of reading and book-buying more generally.

It is in fact not so easy to specify how we might reap significant additional social benefits from the current book market. The real externality, if there is one, lies in improving the humans not the books.

In the meantime, Amazon, in its current configuration, seems to be producing some marginal social benefits.

Venezuela estimate of the day

Venezuela loses $728MM for each 1$ the oil price drops. Assuming oil @ $104 in 2014 and $96 in 2015 Vzla’s $ deficit in 2015 will be $27.8bn

That is from Moisés Naim on Twitter. Here is more on the same topic.

Evidence from opera on the efficacy of copyright

Michela Giorcelli and Petra Moser have a new paper, the abstract is this:

This paper exploits variation in the adoption of copyright laws within Italy – as a result of Napoleon’s military campaign – to examine the effects of copyrights on creativity. To measure variation in the quantity and quality of creative output, we have collected detailed data on 2,598 operas that premiered across eight states within Italy between 1770 and 1900. These data indicate that the adoption of copyrights led to a significant increase in the number of new operas premiered per state and year. Moreover, we find that the number of high-quality operas also increased – measured both by their contemporary popularity and by the longevity of operas. By comparison, evidence for a significant effect of copyright extensions is substantially more limited. Data on composers’ places of birth indicate that the adoption of copyrights triggered a shift in patterns of composers’ migration, and helped attract a large number of new composers to states that offered copyrights.

For the pointer I thank the excellent Kevin Lewis.

Assorted links

Wedding ring and ceremony expenditures predict shorter marriage duration

There is a new paper from Andrew M. Francis and Hugo M. Mialon:

In this paper, we evaluate the association between wedding spending and marriage duration using data from a survey of over 3,000 ever-married persons in the United States. Controlling for a number of demographic and relationship characteristics, we find evidence that marriage duration is inversely associated with spending on the engagement ring and wedding ceremony.

What is the mechanism? Are signal-requiring and financial commitment-requiring marriages more likely to be fragile? Or, to put forward a politically incorrect interpretation, do the high expenditures indicate the wife has too much bargaining power in the relationship? That hardly seems like a plausible explanation. By the way, weddings with a large number of attendees are likely to last longer, as are weddings accompanied by honeymoons. Those correlations are easier to understand.

This piece is by a factor of more than five the most frequently downloaded SSRN paper over the last two months.

What I’ve been reading

1. Doris Kearns, The Bully Pulpit: Theodore Roosevelt, William Howard Taft, and the Golden Age of Journalism. This Pulitzer-Prize winning book is compulsively readable and is most valuable on how the Roosevelt and Taft administrations fit together in American history. I wish it had more detail on economic issues.

2. Walter Isaacson, The Innovators: How a Group of Hackers, Geniuses, and Geeks Created the Digital Revolution. At first I was bored but the book picks up and is then interesting throughout, most of all I enjoyed the portrait of Bill Gates. It is a good overview of how some of the main pieces of today’s information technology world fell into place, starting with the invention of the computer and running up through the end of the 1990s.

3. Russ Roberts, How Adam Smith Can Change Your Life: An Unexpected Guide to Human Nature and Happiness. The best and most readable introduction to Adam Smith’s Theory of Moral Sentiments.

4. Mark Metzler, Capital as Will and Imagination: Schumpeter’s Guide to the Postwar Japanese Miracle. More interesting on Japanese economic history, and in particular postwar economic planning, than on Schumpeter.

5. Jan Swafford, Beethoven: Anguish and Triumph. A consistently excellent and engaging treatment of a figure you cannot read too many books about. It does not seem like a book of 1000+ pages. The funny thing is, this book does not come close to exhausting Beethoven, in fact it barely scratches the surface. It’s as good as the classic Maynard Solomon biography.

From the comments, on secular stagnation

In “National Income and the Price Level,” Martin Bailey discussed the issues of the liquidity trap and secular stagnation.

He observed that at a zero real interest rate, it would be profitable to level the Rocky Mountains and fill in the Gulf of Mexico. The land created would have a rate of return over zero. Also, replacing all steel with stainless steel would pay off.

The examples get to the problem. If someone wanted to level a mountain and fill in the Gulf, it would take a decade to get EPA approval, if it ever came. At negative real interest rates, there are plenty of profitable investments. Maybe in the medical sector, or energy, or finance, or banking, or education, or transportation….where government approval can block the investment for a decade. Secular stagnation is feasible in a world of heavy regulations and taxes, regardless of technological opportunities or the productivity of capital. Keystone Pipeline, anyone?

In a regulated state, easy Fed policy might boost the stock market and lower bond yields without boosting investment much at all. Sound familiar?

Assorted links

1. How Facebook is shaping the news.

2. 1959 Isaac Asimov short essay on how to stimulate creativity.

3. “The Army is conducting a reverse auction for Catholic priest services.”

4. Another superb Michael Hoffman review, this time of Martin Amis on Auschwitz.

5. Ryan Avent on how bad is Amazon? And Joshua Gans on Krugman on Amazon.

6. Richard Preston on Ebola. And David Brooks on why Ebola has taken over our minds.

Hi future, competency-based learning

From Inside Higher Ed:

The University of Michigan’s regional accreditor has signed off on a new competency-based degree that does not rely on the credit-hour standard, the university said last week. The Higher Learning Commission of the North Central Association of Colleges and Schools gave a green light to the proposed master’s of health professions education, which the university’s medical school will offer. In its application to the regional accreditor, the university said the program “targets full-time practicing health professionals in the health professions of medicine, nursing, dentistry, pharmacy and social work.”

Optimal Journal Submission Strategy

Kevin Vallier, a philosopher, considers on Facebook the optimal journal submission strategy:

I was implicitly assuming the best strategy was to start with the best journals, receive rejections, and then work my way down, lest my piece get accepted by a sub-par journal first. But now I’m thinking it may make more sense to start from “the bottom” or at least mid-tier journals and work my way “up” if I can assume that my pieces will generally be rejected several times, even by the mid-tier journals. I think I was overestimating the risk of publishing my work in mid-tier journals and underestimating how much rejections can improve the quality of the paper. In light of this, I want to construct a “journal ladder” that political philosophers and political theorists can “climb” towards the best journals.

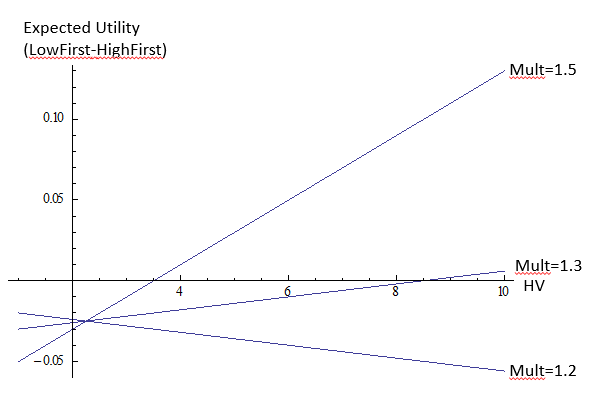

Let’s put some numbers on this to see what makes sense. The expected utility from submitting to a high quality journal first is:

HighFirst = Ph* HV + (1 – Ph)*(Pl*mult)* 1

The first term, Ph*HV is the probability of acceptance at a high quality journal times the value of acceptance at a high quality journal. If the paper is rejected, which happens with probability (1-Ph), then you go to a low-quality journal where the paper is accepted with probability Pl times the multiplier which you get because of suggestions and comments from the referees at the high quality journal. The value of the low-quality journal is set to 1 so HV>=1.

Now what about low first:

LowFirst = Pl*1 + (1 – Pl) (Ph*mult)*HV

if you submit to the low quality journal and are accepted you get Pl*1, if the low quality journal rejects which will happen with probability (1-Pl) you submit to the high quality journal which accepts with probability Ph*mult and if accepted you get HV.

Now let’s put some numbers on this. The probability of acceptance at a high quality journal is 5-10%. The rate at the AER in recent years, for example, has been about 7.5%. Let’s say 10% and for a low-quality journal 20%. These rates are conditional on being the type of paper that is submitted to the AER not any random paper. (These rates are also reasonable for philosophy journals.). What’s the value of HV, the high quality journal relative to the low quality journal? Let’s say between 1 (equally valuable) and 10. And the multiplier? 1.5 would be very generous. 1.1 might be reasonable on average, 1.2 if you are lucky. Given these numbers let’s consider LowFirst-HighFirst so positive numbers mean that the LowFirst strategy is better, negative numbers that the HighFirst strategy is better. Here’s what we get:

The way to read this is that if the multiplier is a hefty 1.5 then LowFirst is superior to HighFirst if a high quality journal has a value of at least 3.5 (relative to the low quality journal at 1). If the multiplier is 1.3, however, then LowFirst is optimal only if the high quality journal is more than 8 times as valuable as the low-quality journal. And for a multiplier of 1.2 LowFirst is never optimal.

Thus the LowFirst strategy is better the higher the relative value of a high-quality journal, the bigger the multiplier and also the lower the acceptance rate at the low quality journal . The lower the acceptance rate at the low-quality journal the lower the cost of submitting it there in order to earn the multiplier.

I conclude that the high-value first strategy is usually optimal. All the more so since there are good substitutes for submitting to a low quality journal. Namely, submit the paper to a conference, circulate the paper to friends, enemies (especially) and others to get comments. The multiplier with this approach will be at least as large as with the submission approach and the opportunity cost will be lower.

Does the Egertsson and Mehrotra model of secular stagnation work?

Their new paper is here, ungated here (pdf), here is the key passage:

We have shown that in the model with capital, the presence of productive assets carrying a positive marginal product does not eliminate the possibility of a secular stagnation. The key assumption is that capital has a strictly positive rate of depreciation. In the absence of depreciation, capital can serve as a perfect storage technology which places a zero bound on the real interest rate. It is straightforward to introduce other type of assets, such as land used for production, and maintain a secular stagnation equilibrium. For these extensions, however, it is important to ensure that the asset cannot operate as a perfect storage technology as this may put a zero bound on the real interest rate.

Let me recapitulate the basic problem. Secular stagnation models are supposed to exhibit persistent negative real rates of return, but how is this compatible with economic growth and positive investment? Just hold onto stuff if need be and of course the goverment can help you do this with safe assets, if need be. The earlier models had no capital, which ruled out this possibility. The new model assumes storage costs for capital are fairly high, or alternatively the depreciation rate for capital is high. Since you can’t sit on your wealth, you might as well invest it at negative real rates of return.

But at the margin, storage costs for goods (and some capital) are not that high. My cupboard is full of beans and cumin seed, but I eat the stuff only slowly. In the meantime it is hardly a burden, nor is it risky since I know it will be tasty once I make the right brew. Art has negative storage costs (for the marginal buyer it is fun to look at), although its risk admittedly makes this a more complicated example. Advances in logistics, and the success of Amazon, show that storage costs are getting lower all the time.

Secular stagnation might be a good model for Liberia and Venezuela and Mad Max, but not for the United States today or other growing economies with forward momentum. But a credible stagnation model for America needs to recognize that rates of return will be lower than usual but not negative in real terms. And there won’t be a long-run shortfall of demand because eventually market prices will adjust so that demand meets the supply we have. That is a supply-side stagnation model of the sort promoted by myself, Robert Gordon, Peter Thiel, Michael Mandel, and others. In the secular stagnation model as it is now being discussed by Keynesian macroeconomists, you end up twisting yourself in knots to force that real rate of return into permanently negative territory. Of course if you allow the real rate of return to be positive albeit low, the economy is not stuck in a perpetual liquidity trap as people move out of cash into investment assets. The demand-side stagnation mechanisms fade away into irrelevance once prices have some time to adjust.

Izabella Kaminska comments here. Josh Hendrickson has a very good blog post on the model here. I’ve already cited Stephen Williamson here, he notes the model is really about a credit friction and would be remedied with a greater supply of safe assets for savings, an easy enough problem to solve, for instance try the Bush tax cuts. Here is Ryan Decker on the model, and here is Ryan arguing that investment is aggregate demand also and many of us seem to have forgotten that, a very good post.

This is an important and interesting paper, but only because it shows the model doesn’t really hold and requires such contortions. The discussion of policy results is premature and way off the mark. The authors should have included sentences like “storage costs aren’t very high, and the economy as a whole does not exhibit negative real rates of return, so these policy conclusions are not actual recommendations.”

Alan Krueger has a new economics blog for teachers

What is the welfare cost of Amazon supply restrictions on books?

Maybe that welfare cost is not very high at all. After all, if Amazon does not carry a book you can sign up at the Barnes & Noble website and that takes a few minutes at most.

There is a tension in most criticisms of Amazon. On one hand, the critic wishes to argue that a “not carry” decision by Amazon has a big impact on how a book does. On the other hand, the critic wishes to argue that the loss of access to particular titles is a big deal. You cannot easily have it both ways. If readers won’t switch to B&N.com, they must not care very much about particular titles, in which case the Amazon refusal to carry (or delay in shipping) is small even relative to the size of the (small) trade in books.

Krugman’s column today, which covers Amazon vs. Hachette, appears terrible at first glance, but in fact he presents a new and original argument. Get past the mood affiliation and you come to this:

…what Amazon possesses is the power to kill the buzz. It’s definitely possible, with some extra effort, to buy a book you’ve heard about even if Amazon doesn’t carry it — but if Amazon doesn’t carry that book, you’re much less likely to hear about it in the first place.

If I may fill in some blanks, one possible version of the hypothesis — to pull an idea from Gary Becker and Steve Erfle — is that readers consume both “books” and “buzz around books” as complements. The marginal gains from books can be low but the marginal gains from the bundled package may be much higher and those higher gains will not be measured by the (high) price elasticity of book purchases.

In the early stages of this war, Amazon boycotts have often increased the buzz for a book, such as with Beth Macy’s Factory Man. But if these practices continue, they will cease to be news stories and an Amazon refusal to carry or promote plausibly will damage how books will do, without much potential for upside.

How much of the value in a book/buzz package is due to the buzz? 65 percent? That would explain the concentration of reading interest among bestsellers and books your peers are reading. But if Amazon won’t carry or promote a book, does the total supply of buzz fall? Or does the buzz simply transfer to other titles? In the latter case we are again back to small welfare costs from an Amazon refusal to carry. Krugman’s idea is fun, but I am still inclined to think the welfare cost of Amazon supply restrictions on individual books likely is small, again even relative to the size of the book sector, much less relative to gdp.

It is fine to argue that Amazon is being unfair to some authors and to object on ethical grounds. The economist also should add that readers don’t seem to mind very much. Most of the objections I am seeing are coming from authors and publishers, who of course in this sector are much less diversified in their interests than are readers.

Assorted links

1. The tallest cow in the world?

3. New learning on the speed and breadth of the Industrial Revolution (pdf).

4. China upgrade markets in everything. And interview with Marc Andreessen. Should China make its big cities bigger yet?

5. Do travel restrictions limit pandemics?

6. Contrary to a behavioral econ claim about threshold earnings, taxi drivers in fact have positive elasticity of supply.

7. Elisa New (wife of Larry Summers) has a poetry MOOC from Harvard, Larry will appear to discuss economics and poetry with her.

. . . and the Cross-Section of Expected Returns

There is a new NBER paper by Campbell R. Harvey, Yan Liu, and Heqing Zhu, and it is a startler though perhaps not a surprise:

Hundreds of papers and hundreds of factors attempt to explain the cross-section of expected returns. Given this extensive data mining, it does not make any economic or statistical sense to use the usual significance criteria for a newly discovered factor, e.g., a t-ratio greater than 2.0. However, what hurdle should be used for current research? Our paper introduces a multiple testing framework and provides a time series of historical significance cutoffs from the first empirical tests in 1967 to today. Our new method allows for correlation among the tests as well as missing data. We also project forward 20 years assuming the rate of factor production remains similar to the experience of the last few years. The estimation of our model suggests that a newly discovered factor needs to clear a much higher hurdle, with a t-ratio greater than 3.0. Echoing a recent disturbing conclusion in the medical literature, we argue that most claimed research findings in financial economics are likely false.

The emphasis is added by me. There are ungated versions of the paper here.

For the pointer I thank John Eckstein.