Category: History

Narva, Estonia (speculative)

Michael Ben-Gad, a professor at London’s City University who has studied the credibility of long-term promises by governments, questions whether Nato’s commitment to collective defence is absolute and asks what would happen if Russia’s border guards crossed the bridge that separates Narva from Ivangorod and took the Estonian town.

“Would the US and western Europe really go to war to defend the territorial integrity of Estonia? I think Estonia has reasons to worry. Narva is the most obvious place; it is almost completely Russian-speaking,” he says.

More than 82 per cent of Narva’s residents are ethnic Russians and 4 per cent are ethnic Estonians. More than a third have Russian citizenship.

Here is the FT article, here are photos of Narva. Here is a map of Narva:

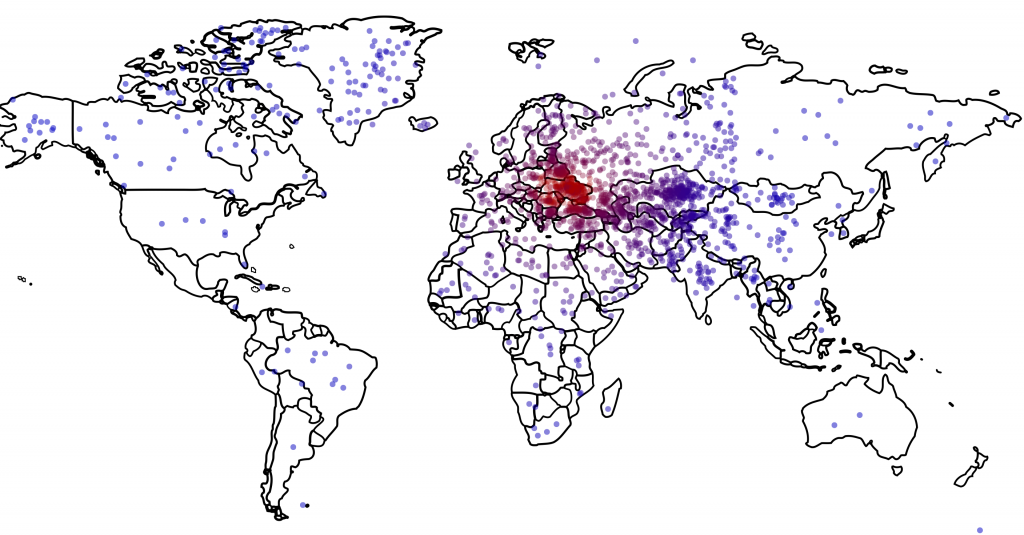

How much do Americans know about Ukraine?

We found that only one out of six Americans can find Ukraine on a map, and that this lack of knowledge is related to preferences: The farther their guesses were from Ukraine’s actual location, the more they wanted the U.S. to intervene with military force.

…the median respondent was about 1,800 miles off — roughly the distance from Chicago to Los Angeles — locating Ukraine somewhere in an area bordered by Portugal on the west, Sudan on the south, Kazakhstan on the east, and Finland on the north.

That is from Monkey Cage, there is more here. The guesses look like this:

For points I thank Kevin Lewis and Samir Varma.

Vox is up!

You will find the introductory video here.

Here is an explainer for Game of Thrones.

Here is Ezra on how politics makes us stupid.

Those two articles are very good, and “work” in the intended manner. Here is the regular home page www.vox.com.

Is it possible their real competition is Coursera?

Going Postal: My First Job

In this article some Nobel prize winners talk about their first jobs and the lessons they learned. One of my first jobs was as a scab.

One summer when I was a teenager, the Canadian postal union workers went on strike and I was hired to deliver the mail. The pay was astounding, something like $25 an hour plus benefits when I was earning $4 an hour as a stock boy. The first day was disorganized and we never got out of the depot where we were supposed to be assigned to a postal station. The second day we were taken in a van to a station but the striking workers rocked and shook the van violently and we barely made it in. The company feared for our safety so we spent the entire day twiddling our thumbs. It was boring sitting around for 8 hours but I was thrilled to head home with $200. The third day we were again trucked to a postal station but there was no mail to deliver and by early afternoon it was clear we were going nowhere and doing nothing. I decided to leave. The guy in charge looked at me incredulously but said it was my call. I slipped out a back door but several burly postal workers saw me and started to chase. I hopped over a fence into, of all places, a graveyard. I ran through the graveyard and eluded a beating. The strike ended the next day. For several years afterwards I collected some kind of pension/overtime benefit.

The summer after that I ran away and joined the circus. I worked selling tickets and cleaning up after the elephants. That was also fun.

I learned a lot from both jobs.

When was the great age of migration?

Jürgen Osterhammel writes:

Between 1815 and 1914 at least 82 million people moved voluntarily from one country to another, at a yearly rate of 660 migrants per million of the world population. The comparable rate between 1945 and 1980, for example, was only 215 per million.

That is from The Transformation of the World: A Global History of the Nineteenth Century. Here is my first post on the book.

The falling market share of General Motors

The General Motors market share in the US fell from 62.6% to 19.8% between 1980 and 2009, noticed Susan Helper and Rebecca Henderson. Helper is now the chief economist at the US commerce department, and Henderson is a management professor at Harvard.

The article is by Heidi Moore. The market here is working, but oh so slowly. I would like to see behavioral economics papers on why so many people continued to buy General Motors (and here I mean the standard cars) for as long as they did.

Here is a timeline of GM recalls.

Jürgen Osterhammel on the Crimean War

The Crimean War, which it lost, and resistance to its great-power pretensions at the Congress of Berlin in 1878, drove the Tsarist Empire to look farther eastward. Siberia acquired a new luster in official propaganda and the national imagination, and a major scientific effort was made to “appropriate” it. Great tasks seemed to lie ahead for this redeployment of national forces. The conviction that Russia was expanding into Asia as a representative of Western civilization — an idea that had originated in the first half of the century — was now turned in an anti-Western direction by currents inside the country. Theorists of Pan-Slavism or Eurasianism sought to create a new national of imperial identity and to convert Russia’s geographical position as a bridge between Europe and Asia into a spiritual advantage. The Pan-Slavists, unlike the milder, Romantically introverted Slavophiles of the previous generation, did not shrink from a more aggressive foreign policy and the associated risks of tension with Western European powers. That was one tendency. But after the 1860s, after the Crimean War, also witnessed the strengthening of the “Westernizers,” who made some gains in their efforts to make Russia a “normal” and, by the standards of the day, successful European country. Reforms introduced by Alexander II seemed to restore this link with “the civilized world.” But the ambiguity between the “search for Europe” and the “flight from Europe” was never dissolved.

That is from the just-published The Transformation of the World: A Global History of the Nineteenth Century. Here is my previous post on the book.

Here is Bryan Caplan “You Don’t Know the Best Way to Deal with Russia.” Here is a short piece on how much sympathy some Germans have for the Russians.

Was Marx right?

Here is an NYT forum, involving myself, Michael Strain, Brad DeLong, and others. My piece is here, excerpt:

Marx pointed out, again perceptively, that capitalism might be subject to a declining rate of profit, and indeed the rate of productivity growth generally has been lower since the 1970s. But why? I would cite energy price shocks, greater investments in environmental goods (which may well be optimal), political dysfunction, the difficulty of topping the amazing achievements of the early 20thcentury, a bit of cultural complacency, and a generally greater aversion to risk, failure and also the new NIMBY “not in my backward” mentality. Most of Marx’s analytical constructs are convoluted, replete with contradictions, and in any case not ideally suited toward analyzing those problems.

We should always be willing to learn from the past, and I do count Marx, for all his flaws, among the great economists. But we should not forget that he was in fact wrong about most things, not just about the totally impractical nature of his communist alternative.

Austrian business cycle theory refuses to die

There is a new paper from Princeton by Matthew Baron and Wei Xiong (pdf), preliminary draft but the results are striking:

This paper examines financial instability associated with bank credit expansion in a set of 23 developed countries over the years 1920-2012. We find that credit expansion, measured by the three-year change in bank credit to GDP ratio, predicts a significantly increased crash risk in the returns of the bank equity index and equity market index in the subsequent one to eight quarters. Despite the increased crash risk, credit expansion predicts both lower mean and median returns of these indices in the subsequent quarters, even after controlling for a host of variables known to predict the equity premium. Furthermore, conditional on credit expansion of a country exceeding a modest threshold of 1.5 standard deviations, the predicted excess return for the bank equity index in the subsequent four quarters is significantly negative, with a magnitude of nearly -20%, while the positive predicted excess return subsequent to a credit contraction of the same size is substantially more modest. These findings present a challenge to the views that credit expansions are simply caused by either banks acting against the will of shareholders or by elevated risk appetite of shareholders, and instead suggest a role for optimism of bankers and stock investors.

The pointer is from Hyun Song Shin. I would continue to stress, however, that Austrian approaches still need more Hyman Minsky and should cease putting all of the “blame” — causal, moral, or otherwise — on the monetary expansion of the central bank. Don’t forget my banana point:

Let’s say that the government subsidized the price of bananas, you bought so many bananas, put them on your roof, and then the roof collapsed. Is that government failure or market failure? The price was distorted, but I still say this is mostly market failure. No one made you put so many bananas on your roof.

*Asia’s Cauldron*

That is the new book by Robert D. Kaplan, and the subtitle is The South China Sea and the End of a Stable Pacific. Since this is possibly the most important topic in the world right now, you should read this book. Here is one interesting excerpt of many:

According to Yale professor of management and political science Paul Bracken, China isn’t so much building a conventional navy as an “anti-navy” navy, designed to push U.S. sea and air forces away from the East Asian coastline. Chinese drones putting lasers on U.S. warships, sonar pings from Chinese submarines, the noisy activation of Chinese smart mines, and so on are all designed to signal to American warships that Beijing knows about their movements and the United States risks a crisis if such warships get closer to Chinese waters. Because “relations with China are too important to jeopardize with a military confrontation,” this anti-access strategy has a significant political effect on Washington. “The strategic impact of China’s agility is not so much to tilt the military balance in its direction and away from the United States. Rather,” bracken goes on, “it introduces new risks into the American decision-making calculus.”

Some chapters of this book are deeper and better thought out than others, but still it is definitely worth reading.

The multiverse is looking more likely

Or so I am told:

…those gravitational wave results point to a particularly prolific and potent kind of “inflation” of the early universe, an exponential expansion of the dimensions of space to many times the size of our own cosmos in the first fraction of a second of the Big Bang, some 13.82 billion years ago.

“In most models, if you have inflation, then you have a multiverse,” said Stanford physicist Andrei Linde. Linde, one of cosmological inflation’s inventors, spoke on Monday at the Harvard-Smithsonian Center for Astrophysics event where the BICEP2 astrophysics team unveiled the gravitational wave results.

Essentially, in the models favored by the BICEP2 team’s observations, the process that inflates a universe looks just too potent to happen only once; rather, once a Big Bang starts, the process would happen repeatedly and in multiple ways.

There is more here. How should this change my behavior? Should I feel more or less regret? Take more or fewer risks?

For the pointer I thank Ami Evelyn.

Norman Borlaug was born 100 years ago today

In case you didn’t know.

My TLS review of Frederick Taylor and Felix Martin

The Frederick Taylor book is The Downfall of Money: Germany’s hyperinflation and the destruction of the middle class, and Martin’s is Money: The Unauthorised Biography.

On Taylor I wrote:

It’s about time we heard the classic Weimar hyperinflation story from the side of governance, just as it is indeed illuminating to reread Hamlet while omitting the parts about the Prince.

Taylor has oddly little on monetary policy in his book, even though he clearly understands the core issues. On Martin’s book I wrote:

Like Taylor’s work, this is an excellent book to read, full of interesting history and insight, and very clear and well written. It is an overview of the history of money, and thought about money, yet through a more philosophical lens than is usually the case. It is not clear, however, if the central thesis of the book is either correct or relevant.

Martin tends to trace financial crises to the defects in underlying philosophies of money, such as whether money is viewed as a thing or as a sign. I also wrote this about the book:

Yet, to paraphrase Freud, sometimes a financial crisis is just a financial crisis.

If you click on the top link here and register for a trial period, you can read the review.

Facts about fame (in praise of college towns)

From Seth Stephens-Davidowitz in today’s NYT:

Roughly one in 2,058 American-born baby boomers were deemed notable enough to warrant a Wikipedia entry. About 30 percent made it through art or entertainment, 29 percent through sports, 9 percent through politics, and 3 percent through academia or science.

…Roughly one in 1,209 baby boomers born in California reached Wikipedia. Only one in 4,496 baby boomers born in West Virginia did. Roughly one in 748 baby boomers born in Suffolk County, Mass., which contains Boston, made it to Wikipedia. In some counties, the success rate was 20 times lower.

…I closely examined the top counties. It turns out that nearly all of them fit into one of two categories.

First, and this surprised me, many of these counties consisted largely of a sizable college town. Just about every time I saw a county that I had not heard of near the top of the list, like Washtenaw, Mich., I found out that it was dominated by a classic college town, in this case Ann Arbor, Mich. The counties graced by Madison, Wis.; Athens, Ga.; Columbia, Mo.; Berkeley, Calif.; Chapel Hill, N.C.; Gainesville, Fla.; Lexington, Ky.; and Ithaca, N.Y., are all in the top 3 percent.

Why is this? Some of it is probably the gene pool: Sons and daughters of professors and graduate students tend to be smart. And, indeed, having more college graduates in an area is a strong predictor of the success of the people born there.

But there is most likely something more going on: early exposure to innovation. One of the fields where college towns are most successful in producing top dogs is music. A kid in a college town will be exposed to unique concerts, unusual radio stations and even record stores. College towns also incubate more than their expected share of notable businesspeople.

African-Americans who grew up around Tuskegee did very well in achieving Wikipedia fame. Yet how much a state spends on education does not seem to matter. And this:

…there was another variable that was a strong predictor of Wikipedia entrants per birth: the proportion of immigrants. The greater the percentage of foreign-born residents in an area, the higher the proportion of people born there achieving something notable. If two places have similar urban and college populations, the one with more immigrants will produce more notable Americans.

The piece is fascinating throughout, and you will note that Seth is a Google data scientist with a Ph.d. in economics from Harvard. His other writings are here. Some of you may wish to see my book What Price Fame?

Mark Toma’s *Monetary Policy and the Onset of the Great Depression*

The subtitle is The Myth of Benjamin Strong as Decisive Leader. Here is a summary from the book’s back cover:

Monetary Policy and the Onset of the Great Depression challenges Milton Friedman and Anna Schwartz’s now-consensus view that the high tide of the Federal Reserve System in the 1920s was due to the leadership skills of Benjamin Strong, head of the Federal Reserve Bank of New York. In this new work, Toma develops a self-regulated model of the Federal Reserve, which stands in contrast to a conventional discretionary model. Given the easy redemption of dollars for gold and the competition among Reserve banks, the self-regulated model implies that the early Fed could control neither the money supply nor the price level. Exploiting an untapped data set, later chapters test the thesis of self-regulation by focusing on the monetary decisions of individual Reserve banks.

The micro-based evidence indicates that “Reserve banks really did compete” – and that Benjamin Strong as decisive leader during the 1920s is a myth. This finding, with its emphasis on monetary policy in the years leading up to the Great Depression, will be of interest to scholars, students, and sophisticated lay readers with an interest in macroeconomic and monetary economic policy issues, specifically to those with an interest in economic history.

I have not read it yet, but it is sure to be controversial.