The binding constraint is we the people

This Michael Rosenwald article is entitled “Smartphones get more sophisticated, but their owners do not,” here is one excerpt:

Some of the most highly touted smartphone innovations are barely used at all. A 2012 Harris Interactive poll showed that just 5 percent of Americans used their smartphones to show codes for movie admission or to show an airline boarding pass. Whether that’s because of a lack of interest or lack of know-how (or both) is not entirely clear, but experts who study smartphone use, as well as tech-support professionals who work with the confused, say they see smartphone obliviousness at all ages and for all kinds of reasons.

The article is interesting throughout. By the way, while I am not sure of the exact definition of an “app,” in general I do not use them.

Airport Congestion and Value Pricing

Major airports are often congested which leads to an inefficient allocation of resources. For example, some planes carry low-value packages that are not time-sensitive. Other planes carry high-value, time-sensitive packages. You don’t want to delay the plane carrying the heart for transplant so that a plane carrying 3-day mail can land a bit early. Vernon Smith and co-authors created and tested a combinatorial auction market to allocate airport slots and improve efficiency. In an auction market when there is congestion the high-value packages can outbid the low-value packages so not every package pays the same freight. Prices in an auction market are also valuable signals telling us where congestion is most severe and expansion most warranted. Revenues from pricing can be used to fund expansion.

Some people, however, are against prioritizing package delivery because they argue that treating every package equally will increase innovation.

Addendum: Don’t take these points as the only or determining considerations but I would like to see more attention given to analysis and less to slogans.

Savings lotteries

The idea of rewarding savings with prizes dates from at least 1694, when Britain, desperate to pay off war debt, lured savers with a jackpot. Prize-linked savings exist in some form in at least 18 countries today. Perhaps the experience most relevant for the United States is Britain’s Premium Bonds, established in 1956. The interest on the bonds isn’t repaid to the holders. Instead, it goes into a prize fund. Every pound savers put in (to a maximum of £30,000) gives them a chance to win a monthly £1 million jackpot plus a million different smaller prizes — all tax free. The program was begun as “Savings With a Thrill,” and the winning numbers were announced each month by celebrities.

At the program’s 50th anniversary, there was £32 billion in bonds — providing the government with capital at a cheaper rate than borrowing. Nearly 40 percent of Britain’s population — 23 million people — hold Premium Bonds. They are sometimes, but not always, the best savings deal — there is often a product whose return is better than the odds of what you’d win with Premium Bonds with average luck. But that’s the point: even though they might not be the left-brain choice, they get people to save.

In America, banks can’t run raffles or lotteries. They can run sweepstakes. The difference is a sweepstakes can’t require entrants to put in money — people must be able to enter by simply sending in their names. That effectively kills the idea for banks.

D2D, which is short for Doorways to Dreams, works to change federal and state laws to allow banks to offer prize-linked savings. But it is also collaborating with institutions that can do this right now: credit unions. In some states, credit unions can hold raffles. Michigan has long been one of them, and in 2008 D2D approached the Michigan Credit Union League about trying it out. Eight credit unions joined a pilot.

…For each deposit of $25, savers got normal interest, plus one entry to the annual grand prize and monthly smaller prizes of between $25 and $100. More deposits meant more chances to win, up to $250 – 10 chances — a month.

From Tina Rosenberg, there is more here. The perceptive reader will note that insofar as you get to keep your money, no lottery payment is possible. The seller of the lottery therefore must skim some off the top, one way or another. So think of this as a savings component bundled with a lottery component but of course the buyers can spend more from their other sources of funds. Perhaps if this “savings program” ends up looking virtuous enough, it could bring new, otherwise responsible customers to the idea of playing the lottery.

For the pointer I thank sellmejunk, a loyal MR reader.

Arrived in my pile

1. Big Ideas in Macroeconomics: A Nontechnical View, by Kartik B. Athreya.

2. Why Government Fails So Often and How it Can Do Better, by Peter H. Schuck, the author is largely a Democrat by the way.

3. Handbook of the Digital Creative Economy, edited by Ruth Towse and Christian Handke.

4. Dinner Party Economics: The Big Ideas and Intense Conversations About the Economy, by Eveline J. Adomait and Richard G. Maranta. I don’t yet see this one on Amazon.

Anne Enright on plot and writing

AE: Plot is a kind of paranoia, actually. It implies that events are connected, that characters are connected, just because they are in the same book. I like the way Pynchon exposed the essential paranoia of plot in The Crying of Lot 49. When I read that book as a student, I realized that if you bring coincidence or the mechanics of plotting into a book, it begs all the questions about who is writing this book and why, or why you’re making this mechanical toy do these things. That, to me as a reader, is slightly alienating. But, you know, things do happen in real life. People die in car accidents. There are connections and coincidences.

She is an Irish writer, there is more here, interesting throughout. I also liked this sentence:

The unknowability of one human being to another is an endless subject for novelists.

And this bit about writing:

It’s like getting a herd of sheep across a field. If you try to control them too much, they resist. It’s the same with a book. If you try to control it too much, the book is dead. You have to let it fall apart quite early on and let it start doing its own thing. And that takes nerve, not to panic that the book you were going to write is not the book you will have at the end of the day.

Hat tip goes to The Browser.

Assorted links

1. One look at the court’s new net neutrality ruling, and another take here. I’d like to see less talk about what this “could” mean and more talk about what it likely will mean.

2. Malaysian fast food restaurants face foreign worker ban.

3. Is the future of on-line education in Africa?

4. Top books of 2013 at the New York Public Library.

5. Is ACA death spiral risk over? And new health care policy think tank.

More thoughts on which countries will be having the next financial crises

Many loyal MR readers have been asking me, since my post from yesterday, whether all those countries listed are likely to have financial crises in the next few years.

I say that most of these countries are quite unlikely to have major financial crises anytime soon. Let us return to the distinction between a recession and a financial crisis. When the U.S. real estate bubble burst in the late 1980s, there was a downturn in output and employment but no financial crisis. No capital markets froze up for instance and risk premia never deviated much from normal in the first place. And if that late 1980s-like path is what someone is predicting for the Nordics, Canada, or Singapore, well maybe so. I’m not predicting it myself but I certainly can see that within the realm of the plausible. (In any case, here is the Singaporean defense of their own economic prospects.)

Why then was the American carnage of 2007-2009 so much worse? Well, for at least two reasons. First, after the relative prosperity and stability of most of the 1990s, so many people thought “the great moderation” had arrived, so investors were much more overextended that time around.

More importantly, the bursting of the real estate bubble overlapped with previously unrecognized, massive systemic risk in the shadow banking system. All of a sudden people realized that U.S. financial institutions, far from being the world’s finest, were in some serious trouble. Risk premia shot up and in some ways they have stayed stubbornly high. Our whole theory of the financial system behind the world’s premier “riskless” asset required a radical and rapid revision.

There were other differences too, but those will suffice for now.

Now let us ask, do any comparable phenomena — in terms of very significant and deeply frightening systemic risk at the global level — exist when it comes to Singapore, Canada, and the Nordics? I don’t see it, so I think if those economies have troubles they will be a relatively moderate set of recessions, a bit like America in the late 1980s. You could make the “China is going to blow and take everyone else down with it” argument. I still see a very good chance of that blow-up happening, but not as soon as 2014, and furthermore its fallout would take a while to travel too. Note also that event probably would not devastate the Nordics, though it would hurt Singapore and Canada more.

You also could try the “the taper will kill us all and reveal the emerging economies to have been bigger bubbles than we thought” line of reasoning. Maybe so, but again that won’t crush Singapore, Canada, or the Nordics. Furthermore the taper already is expected, already has done some of its damage, and the emerging economies already have begun to adjust. Or not.

I do see the global implications of the taper as a real issue. I also see current account deficits for badly run indebted governments as a real issue. I see political instability as a real issue, in part because it may prevent economies from adjusting to the taper and loss of liquidity as they ought to. And when you put those pieces together, you come to the view that Turkey and Thailand and Indonesia are the most vulnerable potential victims for the financial crises to come.

I don’t in general believe that countries with bad institutions are always the best picks for pending financial crises, but I see the current constellation of forces — namely a lot of advance time to adjust and prepare, on the heels of a global great recession and a well-signaled taper– as pushing us toward that view right now.

Or so I think today.

The correct framing of the Irish economic dilemma: guarantees vs. austerity

The policy of No Bondholder Left Behind, on which the European Central Bank insisted, has been staggeringly expensive. To put it in perspective, the European Union has just agreed to create a fund of $75 billion to deal with all future banking crises in its member states. Tiny Ireland has spent $85 billion bailing out its own banks [TC: with more to come, and note the bailouts are more to the creditors than to the banks themselves].

That is from Fintan O’Toole, who wrote a good paragraph there. Yet I do not agree with all of his framing, as he too often presents the Irish dilemma as a debate about austerity.

Let’s say that I, Tyler Cowen, accepted a debt obligation of $5 million, and in order to make some of the interest payments I cut back my spending on food, drink, and Amazon.com and my energy then so weakened that I could never write another book again. That would be bad for my income, since even at the individual level there may be “multiplier effects.” (Please note that by introducing this multiplier assumption I am restoring a kind of parity between the individual and collective cases, no need to snark on this point.)

One way to look at that episode would be to soft pedal the initial guarantee of the debt and focus on the consequences of my “austerity,” and attack the cuts in expenditure, while blaming the new commitments I took on only in passing. I would say that is a misleading interpretation of what happened.

A better way to look at the episode is to focus on the wisdom or foolishness of the guarantee of the $5 million. I would say such a guarantee would be foolish, either for me or for the much larger bank debt bailouts made by the Irish.

Another good and indeed scientific way to frame the question is to take the debt guarantee as given (albeit possibly mistaken), and ask whether my spending cuts should come quickly or be spread out more slowly over time. That is a perfectly fair question to ask and we should not expect the correct answer to be obvious, although of course postponing spending cuts would have meant, for the Irish, borrowing at double digit rates and also risking a full scale “sudden stop.” Furthermore, if we observe speedy rather than gradual spending cuts, the misery of the results does not in any way settle the question of which speed of adjustment would have been better. Pointing out “this isn’t going so well” does not — at all — militate against the speedier path of cuts or for that matter militate against “austerity.” At most it is an argument against the initial guarantee of debt (and even then we are not witnessing the counterfactual).

Nor does changing the topic by asserting “Germany should give Tyler the money” help us settle the right course of action in a world where Germany has no such intention. The same can be said for “Germany should tolerate three percent inflation,” even if that claim is correct.

These points are not even Econ 101, rather they are Propaedeutic to Logic.

Overall, it is amazing how the single largest extension in the responsibilities and fiscal obligations of the Irish state — ever — has been turned into a PR defeat for the idea of fiscal conservatism.

If nothing else, that is testament to how powerful an incorrect message can be if it is repeated enough times and without the proper context.

Addendum: Here is further information on the recent Irish ritual chess murder — Bishop takes lung? — involving by the way an aggressive Sicilian.

About that Medicare cost slowdown

Medicare today is in worse financial shape than was projected before the cost slowdown began. The recession had a more severe impact in depressing Medicare revenues than it had a helpful effect on Medicare cost growth.

That is from Chuck Blahous. It is tricky as to whether we are associating the recession with a one-time loss of output, or with an ongoing slowdown in the rate of economic growth (and which caused which?). Still, on the fiscal front, for the long-term projections, I would say the net bad news has been exceeding the net good news, even though the good news is very welcome indeed.

Which countries will have the next financial crisis?

Here, from Peter Levring, is a discussion of high private household debt in Sweden and Norway and Denmark, along with some remarks by Paul Krugman. Here is an excerpt from Levring:

In Denmark, consumers owe their creditors 321 percent of disposable incomes, a world record that the Paris-based OECD said in November demands a policy response. In Sweden, debt by that measure is close to 180 percent, a level the government and central bank say can’t be allowed to rise. Norway’s central bank has struggled to find a policy mix that addresses its 200 percent private debt burden.

Here is a sustained argument, from Jesse Colombo, that Singapore is due for a crash:

This chart from Nomura shows that Singapore’s loan growth has far outpaced its nominal GDP growth in recent years, making for the worst credit-GDP growth gap in Asia…

The optimistic stance of course is to focus on Singapore’s net asset position, quality governance, and its new and enhanced role in an “Average is Over” world. The same can be said for the Nordics as well.

Those inclined to pick on Malaysia can read the argument here, or try the Philippines.

China seems more like 2015 at this point, if that. And the Russian bailout bought some time for Ukraine.

Or, from Alen Mattich, Canada may be the next victim:

Canadian house prices are very clearly bubbly. By one estimate Canada’s house price to rent ratio–an important metric–is the furthest from historic trends than any country in the world right now. Various estimates have Canadian house prices at between a third and two-thirds over-valued.

I am myself inclined to think Thailand and Turkey are most vulnerable over say the next year, maybe Greece too, in part because of the accompanying political dysfunctions in each case. And is India’s recovery already over? Indonesia still has troubles ahead.

One key question is the relative worry weights you assign to private debt vs. bad institutions.

What about the rest of the world? The eurozone is seeing ongoing credit contraction and perhaps deflation too. Japan just announced a surprisingly large and apparently persistent current account deficit. And the United States? Things look pretty good, but in fact by the standards of historical timing we are soon due for another recession.

I’ll put my money on Turkey.

Assorted links

1. Zerocoin, a new Bitcoin competitor with anonymity.

2. Are immigrants really so anti-libertarian?

3. What do liberals get wrong about single payer?

4. The custom of the public deathbed.

5. William Chislett on where Spain stands now.

6. What scientific idea is ready for retirement? (Hint: most of the criticisms are wrong, even the attack on the law of excluded middle from Alan Alda.)

Inequality and the Masters of Money

This post isn’t about inequality and money it’s about inequality and the masters of monetary policy. Consider Janet Yellen, her recent confirmation to chair the Fed has made her the most powerful woman in the world, the most powerful woman in world history, the world’s second most powerful person, or the world’s most  powerful person depending on who you believe. In anycase, Yellen is powerful. Moreover, Yellen is married to Nobel prize winner George Akerlof. The fact that two such outstanding individuals should be married to one another is an illustration of assortative mating. Yellen-Akerlof are the 1% of the 1% and all that political and cultural achievement concentrated in one family is an example of the growth of inequality. Tellingly, one of the drivers of this inequality was greater equality of opportunity for women.

powerful person depending on who you believe. In anycase, Yellen is powerful. Moreover, Yellen is married to Nobel prize winner George Akerlof. The fact that two such outstanding individuals should be married to one another is an illustration of assortative mating. Yellen-Akerlof are the 1% of the 1% and all that political and cultural achievement concentrated in one family is an example of the growth of inequality. Tellingly, one of the drivers of this inequality was greater equality of opportunity for women.

Now consider, President Obama’s nomination for Fed vice-chairman, Stanley Fischer. Fischer was born in Zambia, holds dual Israeli-American citizenship and was most recently the governor of the Bank of Israel. In all of US history there is almost no precedent for a former major official of a foreign country to become a major official of the United States. Given all the economists in the United States one might have thought that a suitable candidate could be found without this peculiar history and yet it’s not hard to understand why President Obama has nominated Fischer–to wit, I wouldn’t be surprised if everyone President Obama asked for advice on this question to told him that Fischer would be one of the best people in the entire world for the job.

Indeed, many of the people Obama spoke to, including Ben Bernanke, would have been Fischer’s students, themselves a large subset of the tiny elite of the world’s top monetary economists. Perhaps the world of monetary economics is an inbred clique, a supplier-controlled cartel. Maybe so, but I see this as part of a larger story. Stanley Fischer, rather than thousands of other nearly equally-qualified people, is being nominated to the U.S. Federal Reserve for the same reasons that large firms, compete madly for a handful of CEO’s (in the process bidding up their wages to stratospheric levels).

Consider that even in the rarefied world of monetary policy Fischer’s appointment isn’t unique. In 2012, the British appointed Mark Carney, a Canadian, to be the Governor of the Bank of England, the first non-Briton to ever hold the role. When even Great Britain and the United States find that their home-grown talent isn’t good enough that tells you that the demand for talent is immense. My favorite example of this from the business world is Sergio Marchionne. Marchionne is the CEO of Italy’s Fiat and the Chairman and CEO of Chrysler, among several other positions. He commutes between Italy and the United States, lives in Switzerland, and has dual Italian and Canadian (!) citizenship. Appointments and potential appointments like those of Carney and Fischer illustrate that the demand for talent and the winner-take-all phenomena of a globalized world are not limited to the business world.

Small differences in quality at the top have a greater impact the larger the firm, the market, or the economy. How many truly great decisions did Bill Gates make at Microsoft (compared to another plausible CEO)? I would guess that fewer than 10 decisions made billions of dollars of difference. And if Yellen-Fischer make just a few better calls than their next best counterparts, well that could easily be worth hundreds of billions.

It’s also notable that the Federal Reserve is trying to create the highest-quality team. O-ring production tells us that you maximize the value of production by matching high-quality workers with other high quality workers. In the private sector, O-ring production magnifies inequalities of talent into even larger inequalities of income. In the public-sector, O-ring production magnifies inequality of talent into even larger inequalities of power.

The bottom line is this, a common set of factors is driving inequality: equality of opportunity, assortative mating, O-ring production, increases in the demand for talent driven by the leveraging of talent through technology. The forces are similar and so are the results, the money elite, the monetary elite, the power elite.

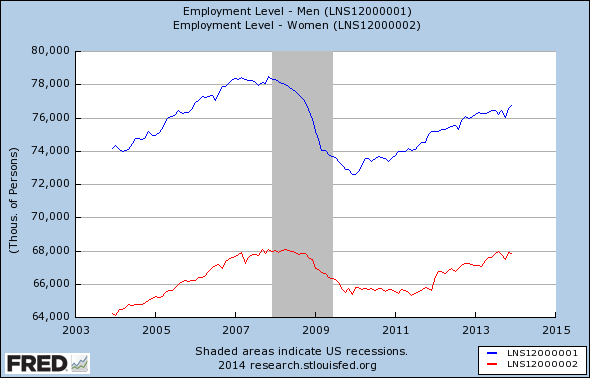

Women have regained pre-crash employment, men have not

There is more here from Matt Yglesias.

Measure for Measure (affective computing as a means of social control)

Cognitive psychologist Mary Czerwinski and her boyfriend were having a vigorous argument as they drove to Vancouver, B.C., from Seattle, where she works at Microsoft Research. She can’t remember the subject, but she does recall that suddenly, his phone went off, and he read out the text message: “Your friend Mary isn’t feeling well. You might want to give her a call.”

At the time, Czerwinski was wearing on her wrist a wireless device intended to monitor her emotional ups and downs. Similar to the technology used in lie detector tests, it interprets signals such as heart rate and electrical changes in the skin. The argument may have been trivial, but Czerwinski’s internal response was not. That prompted the device to send a distress message to her cellphone, which broadcast it to a network of her friends. Including the one with whom she was arguing, right beside her.

There is more here.

How well do minimum wage increases target poverty?

David Henderson writes:

Economists Joseph J. Sabia and Richard V. Burkhauser examined the effects of state minimum wage increases between 2003 and 2007 and reported that they found no evidence the increases lowered state poverty rates.

Further, they calculated the effects of a proposed increase in the federal minimum wage to $9.50 on workers then earning $5.70 (or 15 cents less than the minimum in March 2008) to $9.49. They found that if the federal minimum wage were increased to $9.50 per hour:

. Only 11.3 percent of workers who would gain from the increase live in households officially defined as poor.

. A whopping 63.2 percent of workers who would gain were second or even third earners living in households with incomes equal to twice the poverty line or more.

. Some 42.3 percent of workers who would gain were second or even third earners who live in households that have incomes equal to three times the poverty line or more.

There is more from David here.