Results for “dylan” 143 found

How to save the world — earn more and give it away

Dylan Matthews reports:

Jason Trigg went into finance because he is after money — as much as he can earn.

The 25-year-old certainly had other career options. An MIT computer science graduate, he could be writing software for the next tech giant. Or he might have gone into academia in computing or applied math or even biology. He could literally be working to cure cancer.

Instead, he goes to work each morning for a high-frequency trading firm. It’s a hedge fund on steroids. He writes software that turns a lot of money into even more money. For his labors, he reaps an uptown salary — and over time his earning potential is unbounded. It’s all part of the plan.

Why this compulsion? It’s not for fast cars or fancy houses. Trigg makes money just to give it away. His logic is simple: The more he makes, the more good he can do.

He’s figured out just how to take measure of his contribution. His outlet of choice is the Against Malaria Foundation, considered one of the world’s most effective charities. It estimates that a $2,500 donation can save one life. A quantitative analyst at Trigg’s hedge fund can earn well more than $100,000 a year. By giving away half of a high finance salary, Trigg says, he can save many more lives than he could on an academic’s salary.

…In many ways, his life still resembles that of a graduate student. He lives with three roommates. He walks to work. And he doesn’t feel in any way deprived. “I wouldn’t know how to spend a large amount of money,” he says.

The full story is here. Here is commentary from Salam and Sanchez. And I have just received the new book by Michael M. Weinstein and Ralph M. Bradburd, The Robin Hood Rules for Smart Giving, an analytical treatment written by two economists.

Why is there no Milton Friedman today?

You will find this question discussed in a symposium at Econ Journal Watch, co-sponsored by the Mercatus Center. Contributors include Richard Epstein, David R. Henderson, Richard Posner, Daniel Houser, James K. Galbraith, Sam Peltzman, and Robert Solow, among other notables. My own contribution you will find here, I start with these points:

If I approach this question from a more general angle of cultural history, I find the diminution of superstars in particular areas not very surprising. As early as the 18th century, David Hume (1742, 135-137) and other writers in the Scottish tradition suggested that, in a given field, the presence of superstars eventually would diminish (Cowen 1998, 75-76). New creators would do tweaks at the margin, but once the fundamental contributions have been made superstars decline in their relative luster.

In the world of popular music I find that no creators in the last twenty-five years have attained the iconic status of the Beatles, the Rolling Stones, Bob Dylan, or Michael Jackson. At the same time, it is quite plausible to believe there are as many or more good songs on the radio today as back then. American artists seem to have peaked in enduring iconic value with Andy Warhol and Jasper Johns and Roy Lichtenstein, mostly dating from the 1960s. In technical economics, I see a peak with Paul Samuelson and Kenneth Arrow and some of the core developments in game theory. Since then there are fewer iconic figures being generated in this area of research, even though there are plenty of accomplished papers being published.

The claim is not that progress stops, but rather its most visible and most iconic manifestations in particular individuals seem to have peak periods followed by declines in any such manifestation.

A short history of economics at U. Mass Amherst

From Dylan Matthews. Here is an excerpt:

The tipping point, Wolff says, was the denial of tenure for Michael Best, a popular, left-leaning junior professor. “He had a lot of student support, and because it was the 1960s students were given to protest,” Wolff recalls. That, and unrelated personality tensions with the administration, inspired the mainstreamers to start leaving.

That created openings, which, in 1973, the administration started to fill in an extremely unorthodox way. They decided to hire a “radical package” of five professors: Wolff (then at the City College of New York), his frequent co-author and City College colleague Stephen Resnick, Harvard professor Samuel Bowles (who’d just been denied tenure at Harvard), Bowles’s Harvard colleague and frequent co-author Herbert Gintis, and Richard Edwards, a collaborator of Bowles and Gintis’s at Harvard and a newly minted PhD. All but Edwards got tenure on the spot.

…Under those five’s guidance, the department came to specialize in both Marxist economics and post-Keynesian economics, the latter of which presents itself as a truer successor to Keynes’s actual writings than mainstream Keynesians like Paul Samuelson. “When I got there, the department basically had three poles,” said Gerald Epstein, who arrived as a professor in 1987. “There was the postmodern Marxian group, which was Steve Resnick and Richard Wolff, and then there was a general radical economics group of Sam Bowles and Herb Gintis, and then a Keynesian/Marxian group. Jim Crotty was the leader of that group.” Suffice it to say, most mainstream departments have zero Marxists, period, let alone Keynesian/Marxist hybrids or postmodern Marxists.

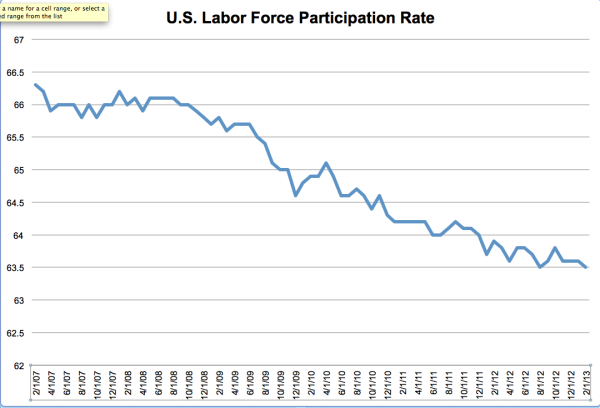

And yet the labor force participation rate is still falling

From Peter Coy, source here. (And broken down by age here, I never find that disaggregation reassuring however, since the elderly are working more and the young less.) Here are related comments and charts from Dylan Matthews. Yet perhaps Felix Salmon has the clincher:

{kind=link}

The number of multiple jobholders rose by 340,000 this month, to 7.26 million — a rise larger than the headline rise in payrolls. Which means that one way of looking at this report is to say that all of the new jobs created were second or third jobs, going to people who were already employed elsewhere. Meanwhile, the number of people unemployed for six months or longer went up by 89,000 people this month, to 4.8 million, and the average duration of unemployment also rose, to 36.9 weeks from 35.3 weeks.

Catherine Rampell discusses the rise of part-time work, very important stuff. Here are relevant remarks by Pethoukis. Here is more on the long-term unemployed.

By the way, my point is not to deny the “good news” aspects of the report, as summarized by Matthews and discussed elsewhere. I would instead put it this way: we are recovering OK from the AD crisis, but the structural problems in the labor market are getting worse. It’s becoming increasingly clear those structural problems were there all along and also that they are a big part of the real story. On the AD side, mean-reversion really is taking hold, as it should and as is predicted by most of the best neo-Keynesian models.

The 20 Greatest Songs About Work?

The list is here. Number one is Tennessee Ernie Ford’s “Sixteen Tons,” followed by Dylan’s “Maggie’s Farm.” “Atlantic City” would not have been my Springsteen pick but overall the list is better than expected. There is, however, an odd under-representation of folk music, see for instance this list.

Why are the service sectors underrepresented on such lists? There is “Dr. Robert,” “Lawyers, Guns, and Money,” “Police and Thieves,” and many others from the more stagnant sectors of the economy, although arguably police productivity has risen quite a bit.

For the pointer I thank the estimable Chug.

Surnames and the laws of social mobility

Here is some new work by Gregory Clark (pdf):

What is the true rate of social mobility? Modern one-generation studies suggest considerable regression to the mean for all measures of status – wealth, income, occupation and education across a variety of societies. The β that links status across generations is in the order of 0.2-0.5. In that case inherited surnames will quickly lose any information about social status. Using surnames this paper looks at social mobility rates across many generations in England 1086-2011, Sweden, 1700-2011, the USA 1650-2011, India, 1870-2011, Japan, 1870-2011, and China and Taiwan 1700-2011. The underlying β for long-run social mobility is around 0.75, and is remarkably similar across societies and epochs. This implies that compete regression to the mean for elites takes 15 or more generations.

Here is NPR coverage:

“If I just know that you share a rare surname with someone who was wealthy in 1800, I can predict now that you’re nine times more likely to attend Oxford or Cambridge. You’re going to live two years longer than an average person in England. You’re going to have more wealth. You’re more likely to be a doctor. You’re more likely to be an attorney,” Clark says.

Dylan Matthews offers some charts. For the pointer I thank Fred Rossoff.

The new Nobel Prize in literature odds

The Japanese novelist Haruki Murakami has emerged as the early favourite to win this year’s Nobel prize for literature.

The acclaimed author of titles including Norwegian Wood, The Wind-Up Bird Chronicle and, most recently, IQ84, Murakami has been given odds of 10/1 to win the Nobel by Ladbrokes.

Last year the eventual winner of the award, the Swedish poet Tomas Tranströmer, was the betting firm’s second favourite to take the prize, given initial odds of 9/2 behind the Syrian poet Adonis, at 4/1. This year Adonis has slipped down the list, given odds of 14/1 alongside the Korean poet Ko Un and the Albanian writer Ismail Kadare.

New names in Ladbrokes list this year include the Chinese author Mo Yan and the Dutch writer Cees Nooteboom, both coming in with strong odds of 12/1 to win the Nobel prize.

And:

Britain’s strongest contender for the Nobel this year, which goes to “the most outstanding work in an ideal direction”, is – according to Ladbrokes – Ian McEwan, who comes in at 50/1, behind the singer-songwriter Bob Dylan, at 33/1. American novelist Philip Roth is at 16/1, alongside his compatriot Cormac McCarthy, the Israeli author Amos Oz and the highest-placed female writer, the Italian Dacia Maraini.

The article is here.

“Getting a good meal in D.C. requires some ruthless economics”

This piece is by me, in The Washington Post. Here is one bit:

The key is to hit these restaurants in the “sweet spot” of their cycle of rise and fall. At any point in time Washington probably has five to 10 excellent restaurants; they just don’t last very long at their highest levels of quality.

Here’s how it works. A new chef opens a place or a well-known chef comes to town and starts up a branch. Good reviews are essential to get the place off the ground, and so they pull out all stops to make the opening three months, or six months, special. And it works. In today’s world of food blogs, Twitter and texting, the word gets out quickly.

…Through information technology, we have speeded up the cycle of the rise and fall of a restaurant. Once these places become popular, their obsession with quality slacks off. They become socializing scenes, the bars fill up with beautiful women (which attracts male diners uncritically), and they become established as business and power broker spots. Their audiences become automatic. The transients of Washington hear about where their friends are going, but they are less likely to know about the hidden gem patronized by the guy who has been hanging around for 23 years, and that in turn means those gems are less likely to exist in the first place.

In economic terms, think of this as a quest for the thick market externalities. Search and monitoring are most intense in the early stages of a restaurant’s life, and so that is the best time to go. There is an analogy in music: Bob Dylan and Chuck Berry do not always give the very best concerts, because they do not have to. You may or may not like up-and-coming bands, but at least they will be trying very hard.

The full article is here.

Assorted links

2. Markets in everything, honey trap edition, or should they call it something else?

3. Do hedge fund returns have lower volatility?

4. The still-underrated Dylan Matthews covers MMT, graphic here.

5. Remarkable Swedish rescue, but of what?

Harvard fact of the day

In 2010, 31 percent of the graduating (undergraduate) class reported taking a job in financial services, source here, pointer from Dylan Matthews.

Richard Clarida, FOMC nominee

Here is his Wikipedia page. Here is some bio. Here is his 1999 survey on monetary policy. Here is Google Scholar. He is a very wise and very accomplished economist. Here is his piece on what we’ve learned about monetary policy in the last decade, with special reference to the liquidity trap and zero bound. Excerpt:

According to monetary theory, central banks have at least two powerful – and complementary – tools to reflate a depressed economy: printing money and supporting the nominal price of public and private debt. As Bernanke (2002) himself argues, a determined central bank can deploy both tools for as long as it wants regardless of 1) how credible its commitment is and 2) how expectations are formed or 3) how term or default premia are determined. There are two fundamental questions. First, can these tools, aggressively deployed, eventually generate sufficient expectations of inflation so that they lower real interest rates? Forward looking models generally predict that the answer is yes. However, the interplay between monetary policy and the yield curve can become complex when central banks are at the zero lower bound (Bhansali et. al. 2009) and central banks seek to provide a “deflation put.”

Also, as discussed above, given the prominent role that inflation expectations play in inflation dynamics, inflation inertia is the enemy of reflation once deflation sets in. A second question relates to the monetary transmission mechanism itself. In a neoclassical world that abstracts from financial frictions, a sufficiently low, potentially negative real interest rate can trigger a large enough inter-temporal shift in consumption and investment to close even a large output gap. But in a world where financial intermediation is essential, an impairment in intermediation – a credit crunch – can dilute or even negate the impact of real interest rates on aggregate demand. In the limiting case of a true liquidity trap, no level of the real interest rate is sufficient in and of itself to close the output gap and reflate the economy. Credit markets in the U.S. appear at this writing to be bifurcated.

There is more to say about Clarida but I have to run to dinner and the theater!

Basically I see it as that Obama and Bernanke have chosen two academics — two guys who think monetary policy really works, or at least can really work. Odds are, they are Ben’s guys, and in my view that is good news. By the way, Clarida I believe is a Republican.

Addendum: Dylan Matthews has good remarks.

Assorted links

1. Bob Dylan’s satellite radio theme hour to return.

2. New uses for old soda bottles. And looming peak dirt?

3. Really fast urban evolution of animals.

4. Nudging the poor to consume more medical services: is time more important than money?

{kind=link}

Assorted links

*Listen to This*

She [Mitsuko Uchida] tells of how she once tried to get [Radu] Lupu to visit Marlboro. "I got every excited, describing how people do nothing but play music all day long. But he said no. His explanation was very funny. "Mitsuko," he said, "I don't like music as much as you."

That's from the new book on music by Alex Ross. It's not a comprehensive tour de force like The Rest is Noise was, but it is smart and well-written on every page and if you liked the first book you should buy and read the second. The portraits cover, among others, Radiohead, Bjork, John Luther Adams, Marian Anderson, Lorraine Hunt Lieberson, and Uchida. The chapter on Bob Dylan is especially good and it eclipses Sean Wilentz's entire recent book on Dylan.

Serial hyperspecializers, and how they think

The highly-regarded-but-still undervalued Elijah Millgram has a paper on this topic, and he seems to be preparing a book. Here is one good short bit:

So one reasonable strategy for a hyperspecializer will be to divide its energies between activities that don't share standards and methods of assessment, and let's abbreviate that to the fuzzier, problematic, but more familiar word, "values." It will be a normal side effect of pursuing the parallel hyperspecialization strategy that its values are incommensurable. The hedonic signals that guide reallocation of resources between niches do not require that niche-bound desires or goals or standards be comparable across niches. If you are a serial (and so, often a parallel) hyperspecializer, incommensurability in your values turns out not to be a mark of practical irrationality, or even an obstacle to full practical rationality, but rather, the way your evaluative world will look to you, when you are doing your practical deliberation normally and successfully. Evaluative incommensurability is a threat to the sort of rationality suitable for Piltdown Man. Serial hyperspecializers gravitate towards and come equipped for incommensurability.

Here is a good review of Millgram's latest book, which argues, among other things, that truth is messy in nature.

Adam Phillips serves up a Bob Dylan quotation: "I have always admired people who have left behind them an incomprehensible mess."