Month: May 2013

American Austerity (and Growth)

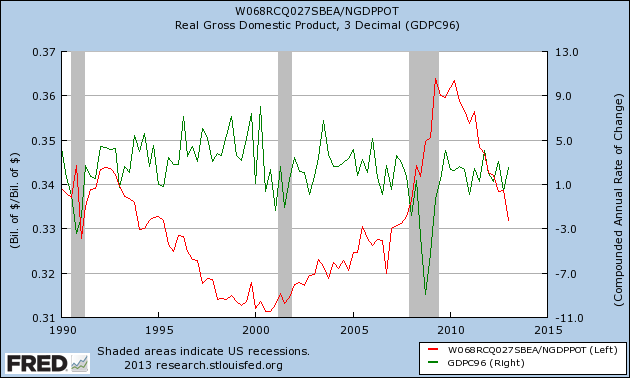

The red line in the chart above is Paul Krugman’s preferred measure of austerity, the ratio of overall government expenditure to potential GDP. The idea of potential GDP has plenty of problems and biases but I want to be more than fair. In his post on American Austerity Krugman warns:

the truth is that federal stimulus is years behind us, while state and local governments have cut back, so the overall story is one of fiscal contraction that’s smaller than in Europe, but not by that much.

…Spending is down to what it was before the recession, and also significantly lower than it was under Reagan. Bear in mind that in the years since the recession began we’ve seen a significant number of boomers reach retirement age, which would ordinarily have led to rising spending, not to mention the effects of rising health care costs. Bear in mind also that the private sector is still deleveraging, which means that government should be spending more to help sustain the economy. So this is actually a picture of very bad policy. (emphasis added)

I assume that by very bad policy what Krugman means is a policy that is likely to have very bad effects. Hence, I have added to Krugman’s graph the growth rate of real gdp (annual rate). I don’t see the very bad effects. In the 1990s growth was strong even while “austerity” was increasing (falling red line) [as this sentence appears to be driving people mad do note that it is a factual description of the data from which I do not draw a conclusion]. More recently, we have seen a big increase in austerity according to Krugman and his measure but although there has been no boom, growth has remained modest. As Justin Wolfers tweeted this morning with the strong jobs report, “the recovery has been remarkably persistent, and resilient,” albeit not rapid. Scott Sumner argues that this is bye, bye Keynesian multiplier as monetary policy stands triumphant (also here) which is one possible interpretation.

Labor markets in everything

A New York City real estate company made the offer and dozens of employees are getting inked.

As CBS 2′s Emily Smith reported Tuesday, a tattoo can be a way to show off your personality. For Rapid Realty employees, it is the fast track to a 15 percent pay raise if you get inked with the company logo.

There are no size or location restrictions. Brooke Koropatnick got hers behind the ear.

The story is here, and for the pointer I thank Mark Thorson. By the way, there is this too:

The credit doesn’t go to Rapid Realty owner Anthony Lolli. He said he got the idea from a loyal employee who wasn’t doing it for money.

“He calls me up, he says ‘Hey Anthony, I’m getting the logo on me.’ I show up at the shop and I’m like ‘this is cool, how can I repay you?’” Lolli said.

A few remarks on the Oregon Medicaid study

There is a simple quotation from Josh Barro, who by the way has supported ACA. Josh wrote:

Despite efforts to spin it to the contrary, this is bad news for advocates of the Medicaid expansion. While Medicaid is clearly good for some things, it was supposed to be good for all of the measures tracked.

Or here is Ray Fisman:

Now that the clinical results have started to come in, it’s time for liberal media types like myself to eat some humble pie. Today’s New England Journal article presents a set of findings showing that Medicaid had no effect on a set of conditions where you would expect proper health management to make a difference. There are effective treatment protocols for hypertension, cholesterol, and diabetes, yet insurance status had no effect on blood pressure, cholesterol levels, or glycated hemoglobin (a measure of diabetic blood sugar control).

Do read the rest of those posts for a more complete picture of the results, but many commentators are overlooking these rather simple upshots.

The key question here is how we should marginally revise our beliefs, or perhaps should have revised them all along (the results of this study are not actually so surprising, given other work on the efficacy of health insurance). For instance should we revise health care policy toward greater emphasis on catastrophic care, or how about toward public health measures, or maybe cash transfers? (I would say all three.) One might even use this study to revise our views on what should be included in the ACA mandate, yet I haven’t heard a peep on that topic. I am instead seeing a lot of efforts to distract our attention toward other questions.

I am sometimes reluctant to speculate about motives, but I believe there is currently a fear of stating the actual truth, given that ACA and the Medicaid expansion are coming under increasing political fire, very often involving mistruths from the Republicans I might add.

You are seeing obfuscations of reality when you encounter two particular responses to the new Medicaid results, which I have been seeing with disturbing frequency. The first is something like “But you still buy health insurance, don’t you?” The second is when the debate is steered into showing that Medicaid does indeed benefit poor people (which is obviously true, and was so before and after this study).

Those are both examples of running away from the idea of thinking at the margin. A better response would run more along the lines of “The Medicaid expansion had been oversold, we now should think more along some other lines for improving our health care system. Let’s admit that we have more of a mess on our hands than we had realized or let on.” You don’t have to deny that Medicaid might help with long-term care problems, for instance, or advocate the abolition of Medicaid. The real results from the new study are most likely about health insurance and health care, not so much about Medicaid per se; see Ezra’s on-target remarks.

Compare what you have seen over the last two days with the writings on the earlier phases of the Oregon study, when it seemed to be yielding a more positive picture of Medicaid. Those earlier writings often were preparing for a coronation of this study (please do read that link) but now we are seeing hand-wringing and all sorts of talk about the study’s limitations.

For varying and useful perspectives, here are Carroll and Frakt and Megan McArdle.

Coming on the heels of the debate over Reinhart and Rogoff, I find this all sad. If there is any cheery lesson it is that, in relative terms, macroeconomics is in better shape than we had thought!

Izabella Kaminska’s counterintuitive model of the modern world

1) Because of the safe asset problem there is a diminishing return — or even negative return — to QE at some point. In fact, rather than being inflationary, it becomes deflationary.

2) Interest on reserve policy is actually designed to counteract this deflationary — and negative rate inducing — effect. In fact, IOER, or the ability to hold reserves at the central bank for no negative interest cost, shows that central banks are effectively supporting short-term rates rather than depressing them. If not for the ability to hold reserves at the central bank, then rates could very well be negative.

3) The crisis is in many ways a deposit crisis not a debt crisis. There are simply too many deposits seeking principal protection and not enough safe assets to protect against capital destruction by negative rates.

4) Negative rates are a function of global abundance (brought on by technological advances), and a trend that cannot be stopped even by the strongest central bank — unless society regresses backwards (like many goldbugs would seemingly desire). For rates to stay positive we have to hoard almost everything in the world form the people that need it, if it is to have value. The artificial scarcity tactics that have been used through the ages to achieve this, are getting harder to execute because of technological liberation — which is enabling the emergence of collaborative economy which bypasses rates of return.

5) Central banks taking charge of digital money and issuing it directly to consumers is one way to ensure deposits can always be protected from negativity.

6) Value in the capital system, and our definition of growth, is very likely being transformed as a result.

7) Greater efficiency and abundance may also eventually lead to the end of arbitrage.

Here is more. You will find that differs from the perspectives usually expressed here (most of all #4), but it is always good to pass along contrasting points of view.

Assorted links

1. A new database on educational quality.

2. On the unreliability of early New Zealand gdp figures.

3. Claims about the economics of Game of Thrones.

4. Status competition among religions, as designed by the homeless.

5. There is now a journal for porn studies.

6. China gives Algeria an opera house.

7. Edward Hugh: what kind of test case will Japan prove to be?

We are not as wealthy as we thought we were, and its consequences

Erzo G.J. Luttmer has an interesting new paper and model (pdf):

When consumers realize they are not as wealthy as they thought they were, they reduce consumption and save more. This lowers the real interest rate, making the development of new projects more profitable. The price of new projects rises relative to the price of consumption. The Stolper-Samuelson theorem therefore implies an increase in managerial wages, and a decline in worker wages. If the economy operates in a region where the supply of worker labor is sufficiently elastic, this can lead to a significant reduction in the employment of workers, while managers are reallocated towards developing new projects.

You should not believe in this to the exclusion of traditional aggregate demand channels, but still it is an interesting way to visualize some supplemental effects. Note that workers who are quite good at building new projects will earn premia, while others, in the declining sectors, are losing their jobs. That is not so different from the world we live in.

For the pointer I thank Paddy Carter.

“Investigating America’s elite”

That is a new paper by Jonathan Wai, from the latest issue of Intelligence, with the subtitle “Cognitive ability, education, and sex differences,” and here is the abstract:

Are the American elite drawn from the cognitive elite? To address this, five groups of America’s elite (total N = 2254) were examined: Fortune 500 CEOs, federal judges, billionaires, Senators, and members of the House of Representatives. Within each of these groups, nearly all had attended college with the majority having attended either a highly selective undergraduate institution or graduate school of some kind. High average test scores required for admission to these institutions indicated those who rise to or are selected for these positions are highly filtered for ability. Ability and education level differences were found across various sectors in which the billionaires earned their wealth (e.g., technology vs. fashion and retail); even within billionaires and CEOs wealth was found to be connected to ability and education. Within the Senate and House, Democrats had a higher level of ability and education than Republicans. Females were underrepresented among all groups, but to a lesser degree among federal judges and Democrats and to a larger degree among Republicans and CEOs. America’s elite are largely drawn from the intellectually gifted, with many in the top 1% of ability.

I don’t yet see this paper on-line, but here is some summary coverage.

The MRUniversity course on Mexico

With President Obama visiting Mexico today, I thought I would remind you all that the excellent Robin Grier is teaching this course over at MRUniversity.com. It is called Mexico’s Economy: Current Prospects and History.

Interpreting Statistical Evidence

Betsey Stevenson & Justin Wolfers offer six principles to separate lies from statistics:

1. Focus on how robust a finding is, meaning that different ways of looking at the evidence point to the same conclusion.

In Why Most Published Research Findings are False I offered a slightly different version of the same idea

Evaluate literatures not individual papers.

SWs second principle:

2. Data mavens often make a big deal of their results being statistically significant, which is a statement that it’s unlikely their findings simply reflect chance. Don’t confuse this with something actually mattering. With huge data sets, almost everything is statistically significant. On the flip side, tests of statistical significance sometimes tell us that the evidence is weak, rather than that an effect is nonexistent.

That’s correct but there is another point worth making. Tests of statistical significance are all conditional on the estimated model being the correct model. Results that should happen only 5% of the time by chance can happen much more often once we take into account model uncertainty not just parameter uncertainty.

3. Be wary of scholars using high-powered statistical techniques as a bludgeon to silence critics who are not specialists. If the author can’t explain what they’re doing in terms you can understand, then you shouldn’t be convinced.

I am mostly in agreement but SW and I are partial to natural experiments and similar methods which generally can be explained to the lay public while other econometricians (say of the Heckman school) do work that is much more difficult to follow without significant background and while being wary I also wouldn’t reject that kind of work out of hand.

4. Don’t fall into the trap of thinking about an empirical finding as “right” or “wrong.” At best, data provide an imperfect guide. Evidence should always shift your thinking on an issue; the question is how far.

Yes, be Bayesian. See Bryan Caplan’s post on the Card-Krueger minimum wage study for a nice example.

5. Don’t mistake correlation for causation.

Does anyone still do this? I know the answer is yes. I often find, however, that the opposite problem is more common among relatively sophisticated readers–they know that correlation isn’t causation but they don’t always appreciate that economists know this and have developed sophisticated approaches to disentangling the two. Most of the effort in a typical empirical paper in economics is spent on this issue.

6. Always ask “so what?” …The “so what” question is about moving beyond the internal validity of a finding to asking about its external usefulness.

Good advice although I also run across the opposite problem frequently, thinking that a study done in 2001 doesn’t tell us anything about 2013, for example.

Here, from my earlier post, are my rules for evaluating statistical studies:

1) In evaluating any study try to take into account the amount of background noise. That is, remember that the more hypotheses which are tested and the less selection which goes into choosing hypotheses the more likely it is that you are looking at noise.

2) Bigger samples are better. (But note that even big samples won’t help to solve the problems of observational studies which is a whole other problem).

3) Small effects are to be distrusted.

4) Multiple sources and types of evidence are desirable.

5) Evaluate literatures not individual papers.

6) Trust empirical papers which test other people’s theories more than empirical papers which test the author’s theory.

7) As an editor or referee, don’t reject papers that fail to reject the null.

Immigration, production, and the Rybczynski theorem

Two of the assumptions of some of the pro-immigration arguments, when combined together, strike me as a bit odd. It is commonly claimed for instance that migration to the United States does not lower American wages much if any (I agree by the way, as do most economists). It also is claimed that migration will help us boost our production of capital-intensive goods, such as tech products. Therein lies the tension.

Enter the Rybczynski theorem. The sequence here is as follows. An influx of labor does not lower wages, but it does cause both labor and capital to flow out of the capital-intensive sector and into the labor-intensive sector. Labor-intensive production will rise but capital-intensive production will fall. (If you are wondering about the intuition, consider that prices and wages are remaining fixed. All of the adjustment must take place in terms of quantities, and equalizing marginal product and wage, following the influx of new labor, requires more capital in the labor-intensive sector, thus draining some production from the capital-intensive sector.)

In other words, the core model for constant or near-constant wages, following immigration, also implies that capital-intensive production should fall, following an exogenous influx of labor.

You will note that immigration remains welfare-improving in this model. Still, it is not exactly the deal which has been promised. You also can imagine someone taking a more dynamic perspective and fearing the long-term growth consequences of losing output in the capital-intensive sector. You also now have liberty to wonder if a negative wage effect might mean a stronger rather than weaker case for immigration, given that the capital-intensive sector in the U.S. arguably produces global public goods.

Here is one empirical study of the matter, by Slaughter and Hanson. It supports the predictions of the Rybczynski theorem. Ethan Lewis (pdf) considers the famous Cuban boat lift example, when the influx of immigrants did not lower wages, but he also finds it may have hurt capital goods production in the Miami area. Those results are hardly dispositive, but they don’t exactly throw out the Rybczynski framework either.

To be sure, the Rybczynski theorem is far from self-evidently correct. Prices and wages need not be fixed, especially for a country as large on the global stage as the United States. 2 x 2 x 2 models do not adequately capture the heterogeneity of labor. Even defining “labor-intensive” and “capital-intensive” is fraught with ambiguity when countries do not share all of the same technologies, as illustrated by the debates over the Heckscher-Ohlin theorem (to measure labor-intensity, are we adding up the number of bodies or instead measuring their “effectiveness”?, in which case labor and capital blur together because capital makes labor more effective).

Still, models are useful in organizing our thoughts, and this is a model which I do not see getting much attention. I typically have applied comparative advantage to this question (if more immigrants come, high-skilled citizens are freed up to produce more capital goods), but perhaps the Rybczynski model is also relevant.

I also note that I do not view the primary purpose of this blog as hammering home specific policy conclusions, I would rather put doubts and thought processes on the table. Anyway, maybe this model provides some structure for a better understanding of the trade-offs involved with immigration policy.

I look forward to reading your comments on this issue.

How anti-gun is Hollywood and the entertainment industry?

Here is from today’s news:

The sweeping gun control measure signed by Gov. Andrew M. Cuomo and hailed by Democratic leaders has a surprising critic: Hollywood.

Officials in the movie and television industry say the new laws could prevent them from using the lifelike assault weapons and high-capacity magazines that they have employed in shows like “Law & Order: Special Victims Unit” and films like “The Dark Knight Rises.”

Twenty-seven pilots, television and feature projects, including programs like “Blue Bloods” and “Person of Interest,” are now in production in New York State using assault weapons and high-capacity magazines, according to the Motion Picture Association of America. Industry workers say that they need to use real weapons for verisimilitude, that it would be impractical to try to manufacture fake weapons that could fire blanks, and that the entertainment industry should not be penalized accidentally by a law intended as a response to mass shootings.

One source added:

“Weapons are part of our history as a culture as humans,” said Ryder Washburn, vice president of the Specialists, a leading supplier of firearms for productions that is based in Manhattan. “To tell stories, you need them.”

The follow-up study on Medicaid coverage in Oregon

Here is some overview coverage from Annie Lowrey, an important issue of course with some striking results. Here is coverage from Sarah Kliff. Here is commentary from Justin Wolfers, and here. After the R&R saga, I say it’s time for someone to stand up and admit “We have some egg on our face with this one.”

Addendum: Reading more carefully through the quotations from Finkelstein and Holahan in the Lowrey piece, I find it amazing, and I suppose even embarrassing, what those commentators are claiming as a positive result. Of course it is worth comparing the program to simply giving people the cash.

Why the housing market imploded

In a recent paper, Christopher L. Foote, Kristopher S. Gerardi, and Paul S. Willen report (pdf):

This paper presents 12 facts about the mortgage market. The authors argue that the facts refute the popular story that the crisis resulted from financial industry insiders deceiving uninformed mortgage borrowers and investors. Instead, they argue that borrowers and investors made decisions that were rational and logical given their ex post overly optimistic beliefs about house prices. The authors then show that neither institutional features of the mortgage market nor financial innovations are any more likely to explain those distorted beliefs than they are to explain the Dutch tulip bubble 400 years ago. Economists should acknowledge the limits of our understanding of asset price bubbles and design policies accordingly.

Scott Sumner summarizes the twelve points here:

Fact 1: Resets of adjustable rate mortgages did not cause the foreclosure crisis.

Fact 2: No mortgage was “designed to fail.”

Fact 3: There was little innovation in mortgage markets in the 2000s.

Fact 4: Government policy toward the mortgage market did not change much from 1990 to 2005.

Fact 5: The originate-to-distribute model was not new.

Fact 6: MBSs, CDOs, and other “complex financial products” had been widely used for decades.

Fact 7: Mortgage investors had lots of information.

Fact 8: Investors understood the risks.

Fact 9: Investors were optimistic about home prices.

Fact 10: Mortgage market insiders were the biggest losers.

Fact 11: Mortgage market outsiders were the biggest winners.

Fact 12: Top-rated bonds backed by mortgages did not turn out to be “toxic.” Top-rated bonds in collateralized debt obligations (CDOs) did.

Addendum: There was earlier Boston Globe coverage here.

Assorted links

1. Another look at the STEM job market.

2. What’s it like to live in the middle of nowhere?

3. In China the license plates can cost more than the car.

4. Markets in everything (or does this defeat the whole purpose of cross-dressing?)

What is the most perfectly average place in the United States and why?

That is a question from Annie Lowrey, who recognizes its (supposed) “extreme folly.”

I’ve thought about this for years, and always Knoxville, Tennessee comes to mind. Knoxville is big enough to be something, but not a truly large metropolis, being only the third largest city in Tennessee. It is educated enough to avoid some of the more stereotypical features of the South and indeed it was recently named the #2 “reading city” in America. It has elements of the South and of Appalachia, two major regions of the country. Eleven percent of Knox County adults are “binge drinkers.” It is not one of “12 American boomtowns.”

What else in America might be typical?

Here are nominations of Muncie, Indiana and Kansas City, MO.

Ethnically speaking, Wichita Falls is close to the national norm.

According to this article, high poverty and unemployment are wrecking the averageness of Peoria, Illinois.

Louisville is not a bad pick.

Obviously we must rule out NY, CA, TX, and probably any coastal state as well. I can see the virtues of selecting a Kansas City suburb, which picks up elements of both the South and the Midwest, but I fear that is in a way too typical. The most average place in the United States is in fact just a bit off and has some flavor of its own and choosing Knoxville picks up that too.

Addendum: Matt Yglesias selects Jacksonville, Florida. Kevin Drum cites marketers in favor of Albany, NY.