Month: December 2014

Assorted links

1. Nouriel Roubini on the new machine age.

2. Do high heels influence how men behave?

3. Amazon introduces Dutch-style auctions.

4. Steve Albini defends today’s world of music.

5. An app for valet parking service.

6. Jonathan Gruber’s opening statement (pdf).

7. Russia’s richest man bought Watson’s Nobel medal and now will return it to him.

Don’t overestimate spending on elections

Binyamin Appelbaum has a new and excellent piece on this topic:

Even the 2012 presidential election, which recorded $2.6 billion in campaign spending, underperformed many forecasts. And spending has declined in each of the last two congressional elections. Candidates and other interested parties spent $3.7 billion on this year’s midterms, down from an inflation-adjusted total of $3.8 billion in 2012, which was less than the $4 billion spent in2010, according to the nonprofit Center for Responsive Politics. (These figures do not include a few hundred million dollars in unreported spending on issue ads.) In fact, spending has dropped as the economy has grown and despite a series of contests in which at least one house of Congress was plausibly at stake. “Dire warnings rang out that the decision would herald a new era in politics,” wrote Adam Bonica, a Stanford University political scientist, in a 2013 paper about the effects of Citizens United. “Three years on, there is little evidence that these predictions have come to pass.” Over the past year, Americans spent more on almonds than on selecting their representatives in Congress.

The article is here, interesting throughout. Campaign finance, of course, is one of the areas where “the Left” is most likely to take an anti-science stance.

Stock market losers of the year

A snap presidential election — and the chances of Syriza coming into power if the government fails to win enough support to push its candidate through — are all it took to push the ASE [Greek stock index] down over 10 per cent on Tuesday.

Which makes it a 27 per cent drop for the Athens bourse this year. Only the Portuguese, Nigerian, Russian (in US dollars), and Ukrainian stock markets have done worse in 2014.

From David Keohane and Joseph Cotterill in the FT, here is more. Here is one negative scenario for those of you into Greek pessimism. Here is a more sober look at what is going on in Greece, from Open Europe blog.

Which are the most undervalued economies?

The question refers to which economies are underrated or undervalued, not which economies are the strongest. (Along these lines, LBJ is probably the most overrated player in the NBA today, but he is still also probably the best.)

Last time I picked Pakistan and the Philippines, the latter was a good choice for sure, although now its reputation has caught up to the reality of ongoing rapid growth. I would say Pakistan remains up for grabs, but still the growth rate has been running about five percent, which you would hardly guess from a random episode of Homeland season four. The fiscal deficit is down from eight percent to 5.5 percent, a big step for Pakistan. The stock market has been doing quite well. I don’t wish to claim vindication there, but at the very least it does seem they were underrated a year ago or two and still today.

This year I am going to pick Sri Lanka as well, which has a growth rate of about eight percent, one of the highest in the world. The country receives a lot of bad press because of its vicious, decades-long civil war. Sri Lanka also practices censorship and has iffy democratic credentials and a potentially chaotic election coming up. That’s what helps make it underrated, but of course the war is over now.

The educational system is reasonably good relative to per capita income, English literacy is much higher than in India, and the Chinese are building a lot of infrastructure there. Its tourism potential will expand considerably (I loved the trip there I did with Yana). The poverty rate is down. Here is one overview of recent developments. Here are a variety of country reports, lots of positive features.

Still, you don’t hear so much positive about Sri Lanka these days. On economic terms, I don’t find this one such a tough call, it’s simply a sticky reputation because of the bad politics and previous history.

So my picks for most underrated, this year, are Sri Lanka and Pakistan.

Here are some of my quasi-predictions from 2012.

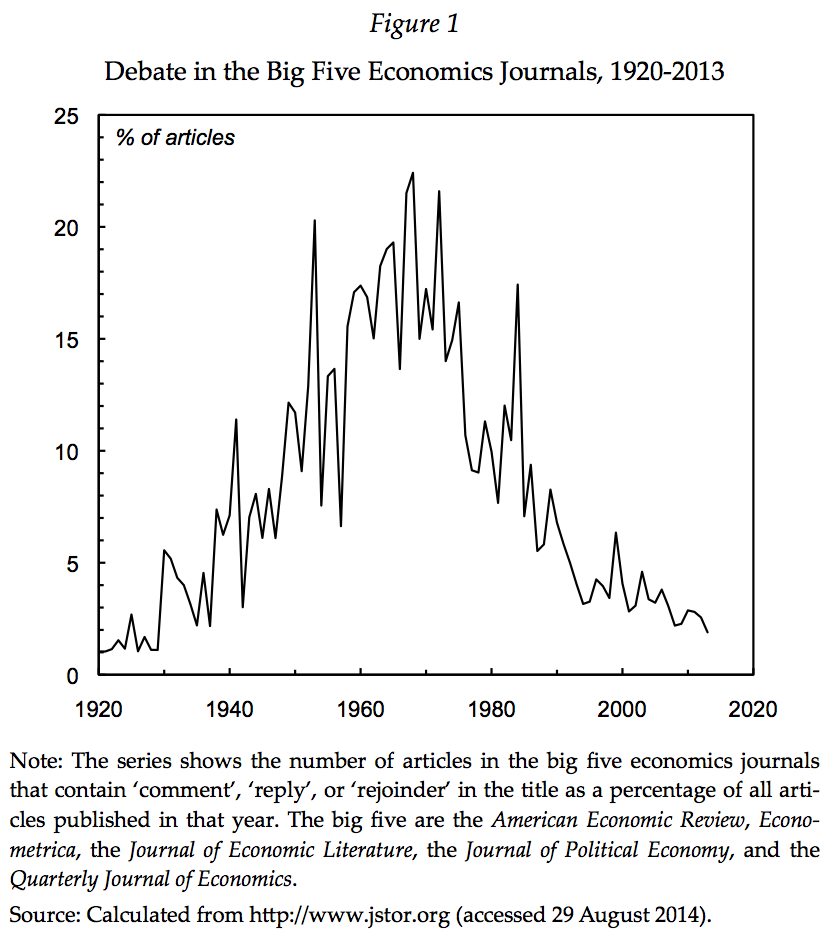

The rise and fall of debate in the leading economics journals

The full article is here, by Joe Francis, cited on Twitter by Justin Wolfers.

The Jean Tirole Nobel lecture

Assorted links

1. A good music aggregator for “popular smart-indie” 2014 recordings.

2. Corey Robin on the real problem with TNR.

3. Improving the power of the mouse brain with human cells.

4. Australian writers pick their favorite books of the year.

5. Amy Alkon podcast with my GMU colleague Todd Kashdan on his new book on the dark side of the emotions (warning: clicking on the link does bring some noise).

6. Markets in everything, three-year-old fruit cake edition.

The partisan nature of economists

There is a new 538 article on this, by Zubin Jelveh, Bruce Kogut and Suresh Naidu, here is one excerpt:

We first found that an economist’s research area is correlated with his or her political leanings. For example, macroeconomists and financial economists are more right-leaning on average while labor economists tend to be left-leaning. Economists at business schools, no matter their specialty, lean conservative. Apparently, there is “political sorting” in the academic labor market.

A word analysis indicates the most left-leaning phrase is “post Keynesian,” followed by “credit union.” The most right-leaning phrase is “free banking,” and then “bank note” and “hedge fund.” Here is some good news:

There’s no evidence that publication decisions are determined by editor ideology.

And yet:

…a left-leaning economist is more likely to report numerical results aligned with liberal ideology (and the same is true for right-leaning economists and conservative ideology)

This won’t be a popular paragraph with everyone:

Policymakers may need to “re-center” economists’ findings by adjusting for ideology. Take the area of tax rates for high earners. The average optimal tax rate reported by economists in our data is 41 percent. Using our model, we can also estimate that these economists as a group are slightly left of center. We can then figure out what optimal top tax rate a hypothetical centrist economist would report: 33 percent.

Here is the authors’ lengthy research paper on all of this (pdf).

For the pointer I thank Bruce Bartlett.

Why do people in Manhattan wait in line so much?

Restaurants, movies, you name it, it seems you so often see people in The Big Apple waiting in line. In the spacious northern Virginia, in contrast, things are built larger and sellouts are uncommon. You stroll right in and let them take your money.

It is not a priori that the net effect should work this way. Manhattan has higher rents, but also a higher value of human capital, and thus possibly the losses from waiting time are higher. But Manhattan also has higher inequality, which means those waiting are often the young rather than the wealthy. The rich can queue-jump in separate spheres of activity, whether it be holding MOMA membership, being a regular at Le Bernardin, or getting a special invitation to the movie premiere on opening night and walking down a red carpet.

(If you are wondering “why don’t they just raise the price?”, raising the price changes the composition and quality mix of buyers, not always in desired ways for long-run profit maximization. In the implicit model here, allowing queuing and building more capacity are two alternative substitutes for raising the price.)

Lately I have noticed a small but perhaps not insignificant increase in “waiting culture” in Washington, D.C. What are ostensibly the town’s two best restaurants — Little Serow and Rose’s Luxury — now both involve significant waits, as the places do not take reservations.

Income inequality is rising, and in select parts of this country, land rents are rising more rapidly than are returns to human capital for the marginal buyer/waiter.

Does that mean we can expect a culture of waiting to spread further throughout the bicoastal United States?

Zuckerberg on Facebook v. Apple

Tim Cook, echoing others, recently said “When an online service is free, you’re not the customer. You’re the product.” Facebook’s Mark Zuckerberg took umbrage in an interview with Time:

“A frustration I have is that a lot of people increasingly seem to equate an advertising business model with somehow being out of alignment with your customers,” Zuckerberg says. “I think it’s the most ridiculous concept. What, you think because you’re paying Apple that you’re somehow in alignment with them? If you were in alignment with them, then they’d make their products a lot cheaper!”

Zuckerberg is only partially correct. Apple and Facebook both want to maximize profits but for Apple a key element in profit is increasing price above cost. Zuckerberg’s point is that one way of doing that is to take advantage of market power and raise price against the interests of customers. But Apple’s market power isn’t a given, it’s a function of the quality of Apple’s products relative to its competitors. Thus, Apple has a significant incentive to increase quality and because it can’t charge each of its customers a different price a large fraction of the quality surplus ends up going to customers and Apple customers love Apple products.

Facebook doesn’t charge its customers so relative to Apple it has a greater interest in increasing the number of customers even if that means degrading the quality. As a result, Facebook has more users than Apple but no one loves Facebook. Facebook is broadcast television and Apple is HBO. See my post Why Has TV Replaced Movies as Elite Entertainment for the diagram.

Chile is backsliding on its reforms

In principle, almost everyone agrees that investing more in education makes sense as it could help build human capital and see Chile advance out of “middle income status” and into the ranks of the developed world.

However, banning students from using vouchers to attend for-profit schools and prohibiting schools that receive public subsidies from receiving top-up payments from parents, also goes against the market-based system. That has startled Chile’s close-knit and conservative business class, which fears the return of statist policies once endorsed by socialist president Salvador Allende in the 1970s.

…Compounding the uncertainty is that the reform drive coincides with the end of a commodity boom that has seen the price of copper, which makes up half of Chilean exports, shrink 12 per cent this year. In the third quarter, economic growth collapsed to 0.8 per cent, from almost 5 per cent a year ago, while investment contracted 10 per cent.

Amid the abrupt slowdown, critics joke that Ms Bachelet’s unwieldy coalition, “The New Majority”, is much like Christine Lagarde’s “New Mediocre”, as the head of the International Monetary Fund recently described the world economy. Certainly, business confidence has fallen in the gloomy atmosphere, while Ms Bachelet’s popularity has plummeted to 42 per cent from 58 per cent in June.

The FT article has other points of interest. Perhaps Chile soon will no longer be so overrated.

A variety of media stocks may fall even further

…Google announced that 56.1% of ads served on the internet are never even “in view”—defined as being on screen for one second or more. That’s a huge number of “impressions” that cost money for advertisers, but are as pointless as a television playing to an empty room.

This is not a big revelation. The web metrics company ComScore reported last year that 46% of online ads are never seen. Spider.io, an ad fraud company acquired by Google in February, has pointed out that a large portion of ads are “viewed” only by robots, revealing that one botnet of 120,000 virus-infected computers viewed ads billions of times, running up the tab for advertisers without offering them the human eyeballs they sought.

There is more here, by Zach Wener-Fleiner, and for the pointer I thank a loyal MR reader.

Assorted links

1. Stephen L. Carter picks best books of the year.

2. $80 million Bitcoin transaction.

3. Profile of me, in Dutch. I took the guy to the local Yemeni restaurant.

4. In this problem of tax incidence theory, which is the more elastic factor of production?

5. Aubade, read by Philip Larkin.

That was then, this is now

Some of the White House economists were dubious and privately called Mrs. Clinton’s health care team “the Bolsheviks.” In return, according to Ms. Rivlin, the economists were “sometimes treated like the enemy.” Their suggested changes were ignored. “We could have beaten Ira alone,” said Mr. Blinder. “But we couldn’t beat Hillary.”

There is more here from the NYT, mostly about Hillary, not about that episode.

How Technology Might Someday Fight Income Inequality

That is the theme of my latest column for The Upshot. In Average is Over I offered a few sentences toward the end about how in the longer run technology might restore greater income equality. or at least greater consumption equality. I thought I should turn that point into a column, here is one excerpt:

Another set of future gains, especially for lesser-skilled workers, may come as computers become easier to handle for people with rudimentary skill. Not everyone can work fruitfully with computers now. There is a generation gap when it comes to manipulating electronic devices, and many relevant tasks require knowledge of programming or, more ambitiously, the entrepreneurial skill of creating a start-up. That, in a nutshell, is how our dynamic sector has concentrated its gains among a relatively small number of employees, thus leading to more income inequality.

This particular type of inequality may very well change. As the previous generation retires from the work force, many more people will have grown up with intimate knowledge of computers. And over time, it may become easier to work with computers just by talking to them. As computer-human interfaces become simpler and easier to manage, that may raise the relative return to less-skilled labor.

Here is more:

A final set of forces to reverse growing inequality stem from the emerging economies, most of all China. Perhaps we are living in a temporary intermediate period when America and many other developed nations bear a lot of the costs of Chinese economic development without yet getting many of the potential benefits. For instance, China and other emerging nations are already rich enough to bid up commodity prices and large enough to drive down the wages of a lot of American middle-class workers, especially in manufacturing. Yet while these emerging economies are keeping down the costs of manufactured goods for American consumers, they are not yet innovative enough to send us many fantastic new products, the way that the United States sends a stream of new products to British or French consumers, to their benefit.

That state of affairs will probably end. Over the next few decades, we can expect China, India and other emerging nations to supply more innovations to the global economy, including to the United States.

Do read the whole thing.