Category: Data Source

Has international travel to the U.S. really collapsed?

But despite some ominous signs, a close look at the data shows that travel to the United States is largely holding up — at least so far.

Nearly as many foreign travelers have arrived at American airports this year than during the same period last year, according to an analysis by The New York Times of entry data collected from every international airport in the country.

International arrivals did drop more than 10 percent in March compared with last year, but this was largely because Easter fell unusually late this year, pushing back a popular travel window for European tourists. More recent figures from April show that travel over the holiday looked similar to previous years.

Here is more from the NYT. The main major difference is for Canadians, who are indeed more skittish, and their ticket sales are down 21 percent.

Buffett’s Alpha

Berkshire Hathaway has realized a Sharpe ratio of 0.76, higher than any other stock or mutual fund with a history of more than 30 years, and Berkshire has a significant alpha to traditional risk factors. However, we find that the alpha becomes insignificant when controlling for exposures to Betting-Against-Beta and Quality-Minus-Junk factors. Further, we estimate that Buffett’s leverage is about 1.6-to-1 on average. Buffett’s returns appear to be neither luck nor magic, but, rather, reward for the use of leverage combined with a focus on cheap, safe, quality stocks. Decomposing Berkshires’ portfolio into ownership in publicly traded stocks versus wholly-owned private companies, we find that the former performs the best, suggesting that Buffett’s returns are more due to stock selection than to his effect on management. These results have broad implications for market efficiency and the implementability of academic factors.

Here is the paper by Andrea Frazzini, David Kabiller, and Lasse Heje Pedersen. Quite the run, now over. Via J.

Large Language Models, Small Labor Market Effects

That is a new paper from Denmark, by Anders Humlum and Emilie Vestergaard, here is the abstract:

We examine the labor market effects of AI chatbots using two large-scale adoption surveys (late 2023 and 2024) covering 11 exposed occupations (25,000 workers, 7,000 workplaces), linked to matched employer-employee data in Denmark. AI chatbots are now widespread—most employers encourage their use, many deploy in-house models, and training initiatives are common. These firm-led investments boost adoption, narrow demographic gaps in take-up, enhance workplace utility, and create new job tasks. Yet, despite substantial investments, economic impacts remain minimal. Using difference-in-differences and employer policies as quasi-experimental variation, we estimate precise zeros: AI chatbots have had no significant impact on earnings or recorded hours in any occupation, with confidence intervals ruling out effects larger than 1%. Modest productivity gains (average time savings of 2.8%), combined with weak wage pass-through, help explain these limited labor market effects. Our findings challenge narratives of imminent labor market transformation due to Generative AI.

Not a surprise to me of course. Arjun Ramani offers some interpretations. And elsewhere (FT): “Google’s core search and advertising business grew almost 10 per cent to $50.7bn in the quarter, surpassing estimates for between 8 per cent and 9 per cent.”

Slow takeoff, people, slow takeoff. I hope you are convinced by now.

Is this a lot or a little?

“The Effect of Deactivating Facebook and Instagram on Users’ Emotional State” — by Hunt Alcott, et.al.

We estimate the effect of social media deactivation on users’ emotional state in two large randomized experiments before the 2020 U.S. election. People who deactivated Facebook for the six weeks before the election reported a 0.060 standard deviation improvement in an index of happiness, depression, and anxiety, relative to controls who deactivated for just the first of those six weeks. People who deactivated Instagram for those six weeks reported a 0.041 standard deviation improvement relative to controls. Exploratory analysis suggests the Facebook effect is driven by people over 35, while the Instagram effect is driven by women under 25.

What is wrong with the simple model that Facebook and Instagram allow you to achieve some very practical objectives, such as staying in touch with friends or expressing your opinions, at the cost of only a very modest annoyance (which to be clear existed in earlier modes of communication as well)?

Here is also a new paper on phone app usage in the classroom, by Billur Aksoy, Lester R. Lusher, and Scott E. Carrell:

Phone usage in the classroom has been linked to worsened academic outcomes. We present findings from a field experiment conducted at a large public university in partnership with an app marketed as a soft commitment device that provides incentives to reduce phone use in the classroom. We find that app usage led to improvements in classroom focus, attendance, and overall academic satisfaction. Analysis of time spent outside the classroom suggests a potential substitution effect: students using the app allocated less time to study, particularly on campus. Overall, though statistically insignificant, we find improvements in transcript grades associated with app usage.

Again NBER. I just do not see the compelling case for the apocalyptic interpretations here.

“Growth is getting harder to find, not ideas”

Here is the thread, here is the paper:

Relatively flat US output growth versus rising numbers of US researchers is often interpreted as evidence that “ideas are getting harder to find.” We build a new 46-year panel tracking the universe of U.S. firms’ patenting to investigate the micro underpinnings of this claim, separately examining the relationships between research inputs and ideas (patents) versus ideas and growth. Over our sample period, we find that researchers’ patenting productivity is increasing, there is little evidence of any secular decline in high-quality patenting common to all firms, and the link between patents and growth is present, differs by type of idea, and is fairly stable. On the other hand, we find strong evidence of secular decreases in output unrelated to patenting, suggesting an important role for other factors. Together, these results invite renewed empirical and theoretical attention to the impact of ideas on growth. To that end, our patent-firm bridge, which will be available to researchers with approved access, is used to produce new, public-use statistics on the Business Dynamics of Patenting Firms (BDS-PF).

By Teresa C. Fort, Nathan Goldschlag, Jack Liang, Peter K. Schott, and Nikolas Zolas. Via Basil Halperin.

Book ban sentences to ponder

Using a staggered difference-in-differences design, we find that the circulations of banned books increased by 12%, on average, compared with comparable nonbanned titles after the ban. We also find that banning a book in a state leads to increased circulation in states without bans. We show that the increase in consumption is driven by books from lesser-known authors, suggesting that new and unknown authors stand to gain from the increasing consumer support. Additionally, our results demonstrate that books with higher visibility on social media following the ban see an increase in consumption, suggesting a pivotal role played by social media. Using patron-level data from the Seattle Public Library that include the borrower’s age, we provide suggestive evidence that the increase in readership in the aggregate data is driven, in part, by children reading a book more once it is banned. Using data on campaign emails sent to potential donors subscribed to politicians’ mailing lists, we show a significant increase in mentions of book ban-related topics in fundraising emails sent by Republican candidates.

That is from a new paper by Uttara M. Ananthakrishnan, et.al., via Kris Gulati.

The Russian paradox

So much education, so little human capital:

According to the UNESCO Institute for Statistics (UIS) statistical database, Russians age 25 and older averaged 12.4 years of schooling circa 2019—almost the same as for Organisation for Economic Co-operation and Development (OECD) Europe, which averaged 12.6 years. While some Western European countries—Germany, Iceland, Switzerland, and the UK—reported mean years of schooling (MYS) well above Russia’s, others reported lower levels than Russia: among them, Austria, Belgium, Greece, Ireland, Italy, Portugal, and Spain…

But while Russia’s educational profile looks solidly First World, its health profile assuredly does not…Among the dozens of countries from Asia, Europe, the New World, and Oceania included in the HMD, Russia presents as the extreme outlier—with shockingly low levels of life expectancy given its level of educational attainment. According to Barro-Lee, MYS at age 15 in Australia and Russia in 2010 were basically indistinguishable, yet in that same year, combined male and female life expectancy at age 15 was almost 14 years lower for Russia. The last time life expectancy at age 15 in Australia was at Russia’s 2010 level, according to HMD, was in 1929—well before the penicillin era…

As of 2019, Russian male life expectancy at age 15 looks to be solidly in the middle of the range for UN’s official roster of least developed countries (LDCs)—the immiserated and fragile states designated as “the most disadvantaged and vulnerable members of the UN family.” If WHO calculations were correct, life expectancy for a young man in Russia was all but identical to that of his Haitian counterpart at that time—and practically half of the world’s LDCs in Figure 3 had higher life expectancies than Russia!

That is from a longer piece by Nicholas Eberstadt, via Mike Doherty.

AI on Tariffs

There is some evidence that the White House used AI to come up with a quick and dirty (and incorrect) formula to correlate tariff rates with trade deficits. I have no problem with using AI, I think they just didn’t go far enough. The White House should have asked the AI a question like this:

Suppose the US imposed tariffs on other countries in an effort to reduce bilateral trade deficits to zero using the formula for the tariff of (exports-imports)/imports. What do you estimate would be the consequences of such a policy?

Answer (O1 Pro):

A tariff schedule keyed to bilateral deficits—imposing a rate equal to (US exports − US imports) / US imports—would be extremely disruptive and unlikely to achieve its goal. Key points:

Immediate Impact on Prices and Supply Chains

If the US imports more than it exports from a given country, (exports − imports) is negative, making the tariff percentage negative unless the formula is modified (e.g., by absolute value). In practice, one would presumably set a positive tariff aimed at closing the bilateral gap.

Such high tariffs would sharply raise import prices for both consumers and firms reliant on foreign inputs. It would encourage attempts to switch suppliers but at the cost of disrupting supply chains and increasing production expenses.

Retaliation and Trade War Dynamics

Targeted countries would almost certainly retaliate with their own tariffs. Retaliation would damage US export sectors—especially agriculture and high-value manufacturing—and risk a broader trade war.

Countries with a US trade surplus would apply punitive measures that shift US business to alternative suppliers, undermining the very exports the policy is meant to foster.

Misalignment with Macroeconomic Fundamentals

Bilateral imbalances reflect global production patterns, comparative advantage, and macro factors like savings–investment imbalances and currency flows. A country that persistently imports more overall does so because it’s running a capital account surplus. Tariffs don’t fundamentally alter that global saving–investment arithmetic.

If the US still runs an overall current account deficit, restricting imports from some countries will simply shift deficits to others. Global supply chains will rearrange, but the total US deficit will be largely unchanged.

Violation of Trade Agreements

Such a policy almost certainly violates WTO rules, since it imposes discriminatory tariffs based on bilateral imbalances. The resulting litigation and sanctions would add more uncertainty.

Net Effect: Reduced Efficiency, Higher Costs

Economically, the net effect is negative. Costs rise for US consumers and US manufacturers reliant on imported inputs. Retaliatory measures reduce export opportunities. Overall trade volume shrinks. Growth slows, and no fundamental improvement in the US external balance occurs.

In summary, a bilateral “deficit-equalizing” tariff policy would create severe distortions, invite retaliation, and do little to fix the structural causes of US trade deficits. Empirical evidence and standard trade theory both suggest it would reduce economic efficiency and likely harm US producers and consumers alike.

Good answer.

Hat tip: SB.

Britain’s productivity problem

A big chunk of it is coming from the health care sector. Information and communications are not growing in productivity as rapidly as before, and Britain has done less well boosting productivity with tech and also in oil and gas extraction. Here is the thread, here is the underlying study from the Resolution Foundation. This is important work.

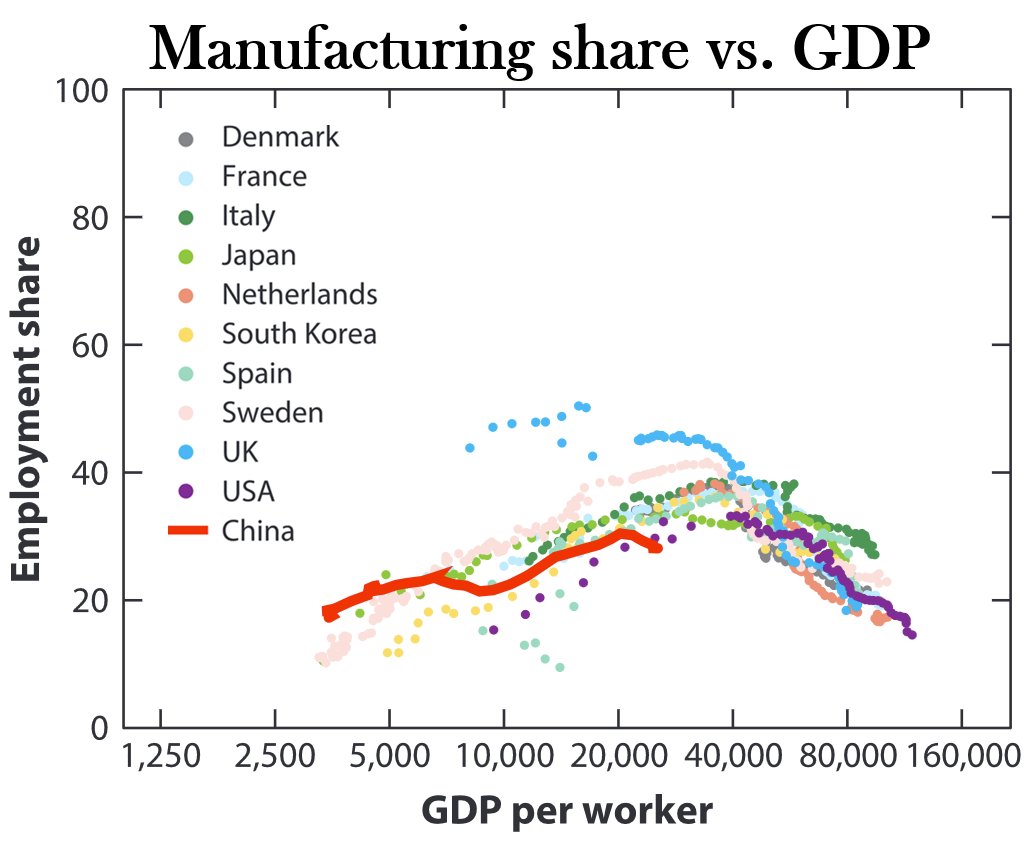

Manufacturing share vs. GDP

Via Basil Halperin. This is not a question of confusing causation and correlation, if anything it is the protectionists who have such an error in their mind’s eye. These days the average U.S. service sector job pays more than a manufacturing job.

Tariff sentences to ponder

We find that only 15.1 percent of the decline in goods-sector employment from 1992 to 2012 stems from U.S. trade deficits; most of the decline is due to differential productivity growth.

Here is the full paper by Kehoe, Ruhl, and Steinberg, via Zack Mazlish. I believe we have covered this issue before.

Using machine learning to measure CEO depression

We introduce a novel measure of CEO depression by applying machine learning models that analyze vocal acoustic features from CEOs’ conference call recordings. Our research was preregistered via the Journal of Accounting Research‘s registration-based editorial process. In this study, we validate this measure and examine associated factors. We find that greater firm risk is positively associated with CEO depression, whereas higher job demands are negatively associated with CEO depression. Female and older CEOs show a lower likelihood of depression. Using this novel measure, we then explore the relationship between CEO depression and career outcomes. Although we do not find any evidence that CEO depression is associated with CEO turnover, we find some evidence that turnover-performance sensitivity is higher among depressed CEOs. We also find limited evidence of higher compensation and higher pay-performance sensitivity for depressed CEOs. This study provides new insights into the relationship between CEO mental health and career outcomes.

Here is the full article, by Sung-Yuan (Mark) Cheng and Nargess M. Golshan. Via the excellent Kevin Lewis.

How strong is the best case for industrial policy?

The textbook case for industrial policy is well understood: sectors with relatively large external economies of scale should be subsidized at the expense of other sectors. Little is known, however, about the magnitude of the welfare gains from such interventions. We develop an empirical strategy that leverages commonly available trade data to estimate sector-level economies of scale and, in turn, to quantify the gains from optimal industrial policy in a general equilibrium environment. Our results point toward significant economies of scale across manufacturing sectors but gains from industrial policy that are hardly transformative, even among the most open economies.

…recall that South Korea — a country often presented as an industrial policy success story — experienced gains in real GDP per capita of 6.82% a year from 1960 to 1989, as documented in Rodrik (1995). A 4.06% long-run welfare increase in nothing to spit at, but a miracle it is not.

That is from a new JPE piece by Dominick Bartelme, Arnaud Costinot, Dave Donaldson, and Andres Rodriguez-Clare. Here are less gated copies of the piece.

How Good is AI at Twisting Arms? Experiments in Debt Collection

How good is AI at persuading humans to perform costly actions? We study calls made to get delinquent consumer borrowers to repay. Regression discontinuity and a randomized experiment reveal that AI is substantially less effective than human callers. Replacing AI with humans six days into delinquency closes much of the gap. But borrowers initially contacted by AI have repaid 1% less of the initial late payment one year later and are more likely to miss subsequent payments than borrowers who were always called by humans. AI’s lesser ability to extract promises that feel binding may contribute to the performance gap.

That is from a new paper by James J. Choi, Dong Huang, Zhishu Yang, and Qi Zhang. No AI asked me to run this blog post!

The Research Behavior of Individual Investors

Browser data from an approximately representative sample of individual investors offers a detailed account of their search for information, including how much time they spend on stock research, which stocks they research, what categories of information they seek, and when they gather information relative to events and trades. The median individual investor spends approximately six minutes on research per trade on traded tickers, mostly just before the trade; the mean spends around half an hour. Individual investors spend the most time reviewing price charts, followed by analyst opinions, and exhibit little interest in traditional risk statistics. Aggregate research interest is highly correlated with stock size, and salient news and earnings announcements draw more attention. Individual investors have different research styles, and those that focus on short-term information are more likely to trade more speculative stocks.

That is from a new NBER working paper by Toomas Laarits and Jeffrey Wurgler.