Category: Economics

Who will win the economics Nobel Prize this year?

Diane Coyle mentions some possible picks:

Environmental economics: Partha Dasgupta, William Nordhaus

Update: Twitter folks strongly recommend adding Martin Weitzman in this category.

Growth: Paul Romer, Robert Barro

Inequality: Anthony Atkinson, Angus Deaton

Innovation (and much else): Will Baumol (now 93!)

Econometrics: David Hendry

All good guesses. I’ll add Diamond and Dybvig for banking, and possibly an early grant to Banerjee, Duflo, and Kremer for development and RCTs. That would make economics look scientific, for a year at least. I expect Bernanke, Woodford, and Svensson to get a prize as well for monetary economics, although probably not right now. It is too close to Bernanke’s memoir and Svensson’s tenure at the Swedish central bank.

Here is a WSJ list. What do you think? Since I’ve never once been right about a particular year, trying to pick someone would only curse them. The award will come this Monday of course.

*Chicagonomics: The Evolution of Chicago Free Market Economics*

That is the new book from Lanny Ebenstein, I found it well-written and useful. You can read about Henry Simons, the Cowles Commission, Hayek, Jacob Marschak, of course Milton Friedman, and much mmore. Friedman, by the way, originally had intended to become an actuary.

Here is Friedman on Hayek from an Ebenstein interview from 1995:

Q: How would you describe Hayek personally?

A: In terms of his personal characteristics, Hayek was a very complicated personality. He was by no means a simple person. He was very outgoing in one sense but at the same time very private. He did not like criticism, but he never showed that he didn’t like criticism. His attitude under criticism, as I found, was to say: “Well, that’s a very interesting thing. At the moment, I am busy, but I’ll write to you about it more later.” And then he never would!

Friedman is extremely frank about Hayek in this interview, and repeatedly mentions that he objected to how Hayek treated his first wife. I have never seen Friedman be so negative, or for that matter so emotionally involved, and when it comes to The Fatal Conceit he simply avers: “It’s not up to Hayek at his best.”

You can then turn to two pages of Paul Samuelson, in a letter to Ebenstein, criticizing Milton Friedman. Ebenstein, by the way, argues that Friedman is essentially a left-wing, utilitarian thinker.

Why is Daniel Hamermesh leaving campus at UT Austin?

Economics professor emeritus Daniel Hamermesh will withdraw from his position next fall, citing concerns with campus carry legislation.

The law will allow the concealed carry of guns in campus buildings beginning Aug. 1, 2016. Hamermesh said he is not comfortable with the risk of having a student shoot at him in class. He teaches a course with 475 students enrolled, according to a letter Hamermesh wrote Sunday to UT President Gregory Fenves…

Hamermesh, who said he is under contract to teach his course in fall 2016 and fall 2017, said he will complete the semester at UT and will teach at the University of Sydney next fall.

Hamermesh said he thinks the legislation will impact the University’s ability to draw new faculty and staff to work at UT.

There is more at the link, via Catherine Rampell.

The problems of Harvard economics?

Here is an article in The Crimson, with many interesting bits, including about Raj Chetty. In turns out space is also a problem, even back in the mid-1980s I thought Littauer was not impressive. It has not improved:

Economics faculty also say that the kind laboratory work common in modern economics—and exemplified by Chetty’s work on government policy—require physical space that is lacking in Littauer and scattered around campus.

“You need infrastructure to run the types of projects he is running,” Antràs said.

Bernheim said Stanford was working “on much closer collaboration and integration” between its economics research buildings to provide adequate space because of Chetty’s arrival and other new hires. He would not comment on the specifics of Chetty’s hiring package, including any lab space he may receive.

And of course, Littauer is old. It hasn’t undergone a major renovation in decades and lacks a functioning air conditioning system.

Whether there are plans to renovate Littauer is uncertain. FAS Dean Michael D. Smith would not comment on any plans to add space to the building, though he noted that conversations about department space across FAS are ongoing.

Even more, the Fine Arts Library, which moved temporarily to Littauer in 2007 during the renovation of the Fogg Museum, compounds the problem of tight space in the building.

University professor Jerry R. Green said the move “pained” him and that now many books used by the Economics department are housed in the Harvard Depository.

Here are the current Harvard faculty, all via Matthew Kahn. And here Matt comments. And Niall Ferguson is leaving Harvard for Hoover.

Meeting of the minds?

Bernanke: “If you get to choose between being rich or famous, I would vote for rich.”

On Twitter, Paul Romer responded:

Nah. Rich is over-rated. It’s too hard to turn money into satisfaction.

The links are here. What should we infer from this dialogue? Model this, so says I…

Addendum: Romer adds comment on Twitter…and more…and more.

*Foolproof: Why Safety Can Be Dangerous and How Danger Makes Us Safe*

That is the new and excellent book by Greg Ip, no fluff here substance all around. From the book’s home page:

How the very things we create to protect ourselves, like money market funds or anti-lock brakes, end up being the biggest threats to our safety and wellbeing.

Here is one excerpt:

The experiment found that people with no impairment to the brain’s emotional center were much more conservative. After losing money on one coin toss, only 40 percent of them agreed to invest on the next — but 85 percent of the brain-damaged patients did. By the end of the game, the brain-damaged patients had earned an average of $25.70 while the healthy players averaged $22.60.

And another:

By Spellberg’s reckoning, the odds of an adverse reaction to an antibiotic, such as an allergic reaction, are about 1 in 10, whereas the odds that someone will suffer because antibiotics were wrongly withheld are about 1 in 10,000. Nonetheless, most physicians do not want to run the risk of letting a patient suffer when an antibiotic could help…His research in Nepal produced the depressing finding that antibiotic resistance was highest in communities with the most doctors.

Spellberg thinks trying to persuade doctors not to prescribe antibiotics is a doomed strategy. Better, he says, to develop tests that rapidly identify what bug a patient has and thus whether an antibiotic is needed.

Strongly recommended, devoured my copy in a single sitting right away, due out this coming Tuesday. By the way here is the FT review by Andrew Hill.

A new AEA website pursues relevance

The AEA is profiling research from all seven of our journals covering the wide range of topics that economists study. Follow us on Twitter for the latest updates.

For the pointer I thank Aaron Sojourner.

Another risk-based model of business cycles

I say if you don’t understand risk-based models, it is difficult to grasp why recovery has been so slow, or why the cycle was so tough to begin with. Here is Mete Kilic, Jessica A. Wachter:

What is the driving force behind the cyclical behavior of unemployment and vacancies? What is the relation between job creation incentives of firms and stock market valuations? This paper proposes an explanation of labor market volatility based on time-varying risk, modeled as a small and variable probability of an economic disaster. A high probability of a disaster implies greater risk and lower future growth, which lowers the incentives of firms to invest in hiring. During periods of high disaster risk, stock market valuations are low and unemployment rises. The risk of a disaster generates a realistic equity premium, while time- variation in the disaster probability generates the correct magnitude for volatility in vacancies and unemployment. The model can thus explain the comovement of unemployment and stock market valuations present in the data.

That is a new NBER working paper.

Ben Bernanke’s memoir *The Courage to Act*

1. When it comes to South Carolina, he is a cornball, but a likable one.

2. He played Strato-O-Matic baseball as a kid. No mention of Jim Bunning in that context.

3. After two years at Harvard, he had taken only Econ 101. Later Dale Jorgensen became his mentor.

4. He is a fan of Borges, with the influence coming from his wife, who has taught Spanish literature.

5. He regrets his earlier tough rhetoric on the Japanese central bank.

6. Greenspan’s marriage proposal to Andrea Mitchell was riddled with his trademark ambiguity. Bernanke, in contrast, proposed after two months of courtship.

7. Bernanke underestimated the extent of the housing bubble. Various negative consequences were to ensue from the collapse of housing prices.

8. “I had never gone overboard on libertarianism…”

9. Ben got really, really mad at the AIG chief executives, in fact he “seethed.”

10. The Fed did not have a good, legal way to bail out Lehman. It needed a buyer, and no buyer was to be found. A short-term infusion of cash would not have sufficed. And Ben was afraid at the time that if he confessed the Fed’s impotence in this regard, the market reaction would have been negative.

11. The idea of a mortgage cram down made good sense but was never politically feasible.

12. “So, by setting the interest rate we paid on reserves high enough, we could prevent the federal funds rate from falling too low.”

13. I found the discussions of Wachovia and WaMu came the closest to offering new perspective and information. Perhaps he was able to say more because these actions did not skirt the possibility of the Fed exceeding its mandate.

14. He had a favorable impression of the frankness of John McCain.

15. He thought QE should been done through the purchase of corporate bonds, but the Fed didn’t have the right kind of authority at that time.

16. He argues that the idea of ngdp targeting is too complicated and could not easily be made credible, given that the Fed has built up its reputation as an inflation fighter. It also raises the risk that a non-credible ngdp target wouldn’t boost output, but would deliver price inflation, thereby resurrecting stagflation as a potential problem. (By the way, here is Scott’s response.)

17. He is still upset at the coverage he received from Paul Krugman.

18. In Nunavut he passed on raw seal meat and a dogsled ride.

The bottom lines: This book has way, way more economics than I expected and probably more than the publisher wanted. It really is Ben’s attempt to defend his place in history, and yes the book does deliver a huge dose of Bernanke. This is not ghostwritten fluff. It does not however dish much “dirt” or shed much new light on the key episodes of the financial crisis. Both in public and in the book Ben has been extremely gentlemanly. Still, as I kept on reading I could not escape the feeling that he is deeply, deeply annoyed by many of his critics, and very much determined to tell the story from his point of view. That is what you get from this book.

France fact of the day

…mergers aside, the youngest firm in the CAC 40, the main stock index, was founded in 1967.

That is from The Economist., via James Pethokoukis.

The rise of the private coach at university

I have been predicting this, Emma Jacobs covers it in the FT:

This new breed of tutors catering to undergraduates is growing (admittedly from a low base). Once the guilty secret of schoolchildren seeking to get into selective schools or gain top marks in exams, private tutors are now helping British undergraduates and even postgraduates at universities. As many teenagers and twenty-somethings start their new university terms, some will be seeking the help of tutors, like Ms Kasson. Some even assist graduates applying for jobs in banks and professional services firms.

Edd Stockwell, co-founder of Tutorfair, a non-profit organisation that also provides tutoring to children whose parents cannot afford the fees, has seen the number of requests for degree-level tutorials double in the past year. Luke Shelley, director of Tavistock Tutors, says its services for undergraduates have grown “rapidly” in the past six years.

There will be very large classes, such as MOOCs and based on the kind of resources you find on MRUniversity.com. And there will be very small classes, perhaps of one or two. It’s the in-between class size, of say two hundred students, that doesn’t always make sense.

Do however note this:

In Ms Mali’s experience it is the parents that are driving the undergraduate tuition business. “Sometimes you do wonder if [the child would be more successful] if they allowed them to fail.”

This is an under-discussed point in today’s ideological environment.

The incompetence of thieves

I investigate self-reported theft data in the NLSY 1997 Cohort for the years 1997–2011. Several striking patterns emerge. First, individuals appear to be active thieves for extremely short periods – in most cases in only one year, and fewer than 5% of thieves for more than three years out of the 15 years of data. Second, self-reported earnings from theft are generally very low and there is little evidence of “successful” criminals or consistent earnings from theft. Third, measures that proxy impatience (smoking, for example) are highly correlated with theft. Fourthly, thieves and non-thieves have similar earnings during the years of peak theft activity, but thieves have lower earnings in their late 20s (after most have long since stopped committing theft). Attrition of survey respondents, underreporting and incapacitation effects do not appear to explain this. There may be “professional thieves” too rare to show up in even large samples such as the NLSY. Theft in the United States thus appears to be substantially a phenomenon of individuals entering a temporary period of intensified risk-taking in adolescence.

That is from a new Geoffrey Fain Williams paper in JEBO, via the excellent Kevin Lewis. Kevin also links to new evidence that concealed carry laws are orthogonal to crime rates.

Dare I suggest that eighty percent of the world is run on this basis?

Despite the cloud cast by the Volkswagen scandal, automakers are proposing that they be allowed a 70 percent increase in the nitrogen oxides their cars emit, unreleased documents show, as part of new European pollution tests.

Under the new plan, cars in Europe would for the first time be tested on the road, using portable monitoring equipment, in addition to laboratory testing.

The automakers, which include Volkswagen, General Motors, Daimler, BMW, Toyota, Renault, PSA Peugeot Citroën, Ford and Hyundai, are essentially conceding what outside groups have said for some time — that the industry cannot meet pollution regulations when cars are taken out of testing laboratories.

Here is the Danny Hakim NYT story.

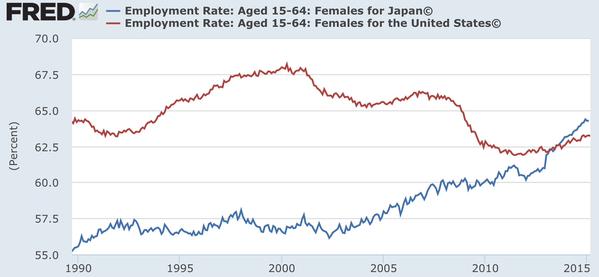

Japan (America) fact of the day

Japanese females quietly overtake American females in terms of #labor force participation.

Noah writes: Note the big jump and trend break when Abe took office.

Credit scores and committed relationships

This paper presents novel evidence on the role of credit scores in the dynamics of committed relationships. We document substantial positive assortative matching with respect to credit scores, even when controlling for other socioeconomic and demographic characteristics. As a result, individual-level differences in access to credit are largely preserved at the household level. Moreover, we find that the couples’ average level of and the match quality in credit scores, measured at the time of relationship formation, are highly predictive of subsequent separations. This result arises, in part, because initial credit scores and match quality predict subsequent credit usage and financial distress, which in turn are correlated with relationship dissolution. Credit scores and match quality appear predictive of subsequent separations even beyond these credit channels, suggesting that credit scores reveal an individual’s relationship skill and level of commitment. We present ancillary evidence supporting the interpretation of this skill as trustworthiness.

That is a new Fed working paper (pdf) by Jane Dokko, Geng Li, and Jessica Hayes.