Category: Economics

On the public choice of Abenomics

Sober Look reports:

Price increases have been driven by weaker yen rather than pricing power improvements of domestic producers. Japan is generating the “wrong” kind of inflation…The combination of declining or stagnant nominal wages and rising prices is creating serious hardships for the nation’s citizens.

Electricity and fuel prices are way up, for instance, as you will see in his graphs. Contra Sober Look, I suspect this is the way Abenomics is “supposed” to work, and it hearkens back to a long tradition of Japanese policy toward “forced savings,” dating at least as far back as the 1930s. Still, this decline in real consumption opportunities is exactly why I think there will be practical limits to Abenomics as a sustained strategy for economic growth. It is rewriting real wage contracts for most workers, and most of them will never get that consumption back or bargain back to the old real wage. Many exporters will be better off.

And by the way, if you exclude the cost of energy, there is still deflation in Japan.

From the comments

This is from Ted Craig:

Another way to look at the effect of mechanization is to look at how it affected the other living employees of farmers. The U.S. horse population peaked at 26.5 million in 1915. It declined rapidly after that, hitting a low of just over 3 million in 1960. While it is about 9 million now, that’s because of increased ownership as pets.

I’m not saying humans will be destroyed like horses, but it raises some questions about the ease of transition.

Eliezer Yudkowsky asks about automation

From the MR comments:

http://lesswrong.com/lw/hh4/the_robots_ai_and_unemployment_antifaq/

(Tyler, have you read that?)

I don’t actually get Brynjolfsson and McAfee. I read the original book and it seemed very unoriginal and not to address at all the basic question of “Why did Ricardian reemployment work fine when agricultural jobs went from 95% to 3%, work fine when automobiles put the whole horse-and-buggy industry out of existence, work fine when women entered the workforce during WWII, and then suddenly stop working?”

The Ricardian comparison is the technology-relevant one here, and I would challenge the notion that it went fine. Think of the machines of the industrial revolution as getting underway sometime in the 1770s or 1780s. The big wage gains for British workers don’t really come until the 1840s. Depending on your exact starting point, that is over fifty years of labor market problems from automation, and yes it is correct to also blame various bad laws, mobility restrictions, wars and taxes, and the like. Even Ricardo, very much a free market economist, worried about the machinery question in his day and rightly so. The industrial revolution was a wonderful development with huge ongoing gains, but still it did bring some very real adjustment issues.

A second point is that now we have a much more extensive network of government benefits and also regulations which increase the fixed cost of hiring labor. Insofar as automation creates short-run adjustment problems, those problems are more likely to show up in the form of decreased labor force participation than they did in previous eras. We are living in a time where the long-run trend is for labor force participation to fall in any case, and that was not in general the case during those earlier episodes.

You also might try to run with a “back then machines substituted for brawn, now they are substituting for brains” argument. Maybe so, but you don’t even need to make that work to have a substantial (non-Luddite) worry.

Immigration and wages

Matt Yglesias has a good post covering new research on immigration and wages:

… [a] new study of immigration to Denmak by Mette Foget and Giovanni Peri is one of the most detailed examinations of the issue that we’ve seen and it finds that Danish workers benefit from an inflow of complementary immigrants:

Using a database that includes the universe of individuals and establishments in Denmark over the period 1991-2008 we analyze the effect of a large inflow of non-European (EU) immigrants on Danish workers. We first identify a sharp and sustained supply-driven increase in the inflow of non-EU immigrants in Denmark, beginning in 1995 and driven by a sequence of international events such as the Bosnian, Somalian and Iraqi crises. We then look at the response of occupational complexity, job upgrading and downgrading, wage and employment of natives in the short and long run. We find that the increased supply of non-EU low skilled immigrants pushed native workers to pursue more complex occupations. This reallocation happened mainly through movement across firms. Immigration increased mobility of natives across firms and across municipalities but it did not increase their probability of unemployment. We also observe a significant shift in the native labor force towards complex service industries in locations receiving more immigrants. Those mechanisms protected individual wages from immigrants competition and enhanced their wage outcomes. While the highly educated experienced wage gains already in the short-run, the gains of the less educated built up over time as they moved towards jobs that were complementary to those held by the non-EU immigrants.

Tada! A lot of people have twisted themselves into a position where this kind of result strikes them as contrarian or counterintuitive. But if you think about population dynamics in a non-immigration context you’ll see that this is the conventional wisdom. If a deadly virus killed five percent of the population of Chicago, incomes would fall not rise. Chicago isn’t populated by subsistence farmers imperiled by land scarcity. Its residents participate in a 21st century service economy where they benefit from complex complementarities and an elaborate division of labor. That’s why big cities are engines of opportunity.

Ygelsias’s analogy to cities is a good one. Bryan Caplan has another way of explaining the point, “In a society of Einsteins, Einsteins take out the garbage, scrub floors, and wash dishes.” Thus, low-skilled immigration can increase wages by allocating talent to higher productivity jobs.

Marketing the asylum

Gentrification and rising real estate prices will lead to many kinds of capital conversion. Here is Mind Hacks:

Regular readers will know of my ongoing fascination with the fate of the old psychiatric asylums and how they’re often turned into luxury apartments with not a whisper of their previous life.

It turns out, a 2003 article in The Psychiatrist looked at exactly this in 71 former asylum care hospitals.

It’s cheekily called ‘The Executives Have Taken Over the Asylum’ and notes how almost all have been turned into luxury developments. Have a look at Table 1 for a summary.

The authors also had a look at the marketing material for these new developments and wrote a cutting commentary on how the glossy brochures deal with the institutions mixed legacies.

The estate agents want to play on the often genuinely beautiful architecture and, more oddly, the security of the sites, while papering over the fact the buildings had anything to do with mental illness.

Here is the article, here is the original 2003 piece (pdf). Here is one summary from Chaplin and Peters:

The only reminders of the former inhabitants found by the authors at any of the 32 redeveloped sites were a memorial garden dedicated to the patients of Cell Barnes and Hill End Hospitals, St Albans, a plaque at Littlemore Hospital, Oxford, and photographs of the former Bethlem Hospital at the Imperial War Museum.

Former mental hospital buildings appear to be undergoing a metamorphosis from containing the most disadvantaged and least-valued members of society to providing homes with character at a high market price. Paradoxically, asylum can now be bought in an ideal self-contained community, with security to keep society out.

*Scarcity: Why Having Too Little Means so Much*

That is the new book by Sendhil Mullainathan and Eldar Shafir, and as you might expect it is one of the most significant economics books of the year. Here is their bottom line:

The poor are not just short on cash. They are also short on bandwidth.

For an example, imagine giving both rich and poor an intelligence test with this question:

Imagine that your car has some trouble, which requires a $300 service. Your auto insurance will cover half the cost. You need to decide whether to go ahead and get the car fixed, or take a chance and hope that it lasts for a while longer. How would you go about making such a decision? Financially, would it be an easy or a difficult decision for you to make?

In their answers to that question, we are told, rich and poor look equally smart. Now run the same question with different groups, but change the first sentence to this:

Imagine that your car has some trouble, which requires an expensive $3000 service.

All of a sudden the poorer individuals did much worse in response to this question and the authors claim this result has been replicated repeatedly. Control studies suggest it is not about the number being larger per se, but rather that the poor individuals see this as a more stressful decision, which lowers their measured fluid intelligence.

Overall I find this all very intriguing, but would like to have a better sense of how this fits in with other results about the relative rigidity of IQ. I also worry about tests where there is an exogenous increase in stressfulness, to which test participants must submit. There are various ways that an examiner could stress me out, but part of one’s smarts, whether at high income levels or low, is exercising some control over matching your talents to the environment.

Here is a good review of the book by Oliver Burkeman. By the way, Alex Tabarrok and MR make a cameo appearance on p.103.

Addendum: Here is Alex on their work.

A Test of Dominant Assurance Contracts

The free rider problem is a challenge to the market provision of public goods. In my paper on dominant assurance contracts I use game theory to show how some public goods can be produced by markets using a special contract. In an assurance contract people pledge to fund a public good if and only if enough others pledge to fund the public good. Assurance contracts were not well known when I began to write on this topic but have now become common due to organizations like Groupon and Kickstarter which work on this principle (indeed, I have been credited with the ideas behind Groupon although sadly for my bank account I don’t think that claim would stand in a court of law). Since no money is paid unless the total pledges are high enough to fund the public good, assurance contracts remove the fear that your contribution will be wasted if other people fail to contribute. However, if you don’t believe that others will pledge there is no reason for you to pledge and if you don’t pledge others have no reason to pledge either so your beliefs will turn out to be accurate. With even low transaction costs the no pledge equilibrium seems quite likely.

What a dominant assurance contract adds is that the entrepreneur agreeing to produce the public good if k or more pledge also agrees that if fewer than k pledge he will pay a prize to those who did pledge. Pledging is now a no-lose proposition–if enough people pledge you get the public good and if not enough pledge you get the prize. A contract like this makes it a dominant strategy to pledge and so the public good is funded. (See the paper for details).

Recently Jameson Quinn tried the idea out with a campaign on Quora. The public good was to contribute to The Center for Election Science. Each pledger agreed to give $60 to the Center if 20 or more similarly pledged and Jameson agreed that if fewer than 20 pledged he would give each person who did pledge $5 and they would have to pay nothing. (This is the essence, Jameson actually modified the dominant assurance contract to offer slightly different terms at 19 and over 20. He has some interesting ideas on this score, see the post for details). So what happened?

Success! It was a nail-biter as the final 3 pledges came in only in the last half hour. Remarkably, the lure of $5 for nothing helped to produce a public good which the pledgers all wanted but might not have produced had the incentive to free ride not been counteracted.

Kickstarter has made assurance contracts familiar, perhaps the next evolution of funding mechanisms will do the same for dominant assurance contracts.

In equilibrium, they pay him to listen to their ads, or how to strike back at The Man

The bottom line is this:

Because he works from home, Mr Beaumont has been able to increase his revenue by keeping cold callers talking – asking for more details about their services.

And it works this way:

A man targeted by marketing companies is making money from cold calls with his own premium-rate phone number.

In November 2011 Lee Beaumont paid £10 plus VAT to set up his personal 0871 line – so to call him now costs 10p, from which he receives 7p.

The Leeds businessman told BBC Radio 4’s You and Yours programme that the premium line had so far made £300.

…Once he had set up the 0871 line, every time a bank, gas or electricity supplier asked him for his details online, he submitted it as his contact number.

He added he was “very honest” and the companies did ask why he had a premium number.

He told the programme he replied: “Because I’m getting annoyed with PPI phone calls when I’m trying to watch Coronation Street so I’d rather make 10p a minute.”

He said almost all of the companies he dealt with were happy to use it and if they refused he asked them to email.

The full story is here, and for the pointer I thank Michael Rosenwald.

*The Second Machine Age*

The authors are Erik Brynjolfsson and Andrew McAfee, and the subtitle is Work, Progress and Prosperity in a Time of Brilliant Technologies.

It is due out January 2014, self-recommending, and it is likely to be the best and most important economics book of the forthcoming year.

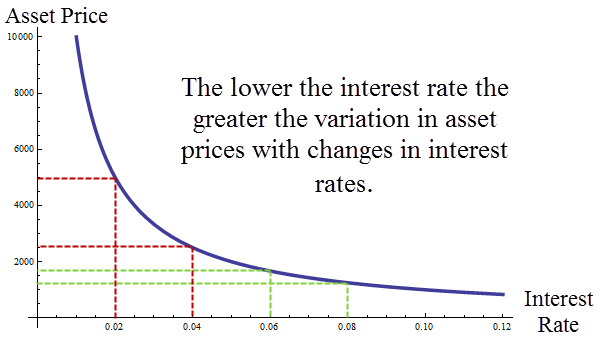

Asset Prices and Interest Rates

There has been a lot of discussion recently of Fed policy, tapering, and asset price “bubbles.” One point to bear in mind is that when interest rates are low even rationally determined asset prices may fluctuate wildly. Consider, the simplest Gordon model of asset prices in which future dividends are expected to be $100 forever, then the asset price is $100/r where r is the interest rate. If r is .1, for example, then the stock will be worth $1000. At an interest rate of 10% the price of an asset that pays $100 forever is just $1000 because the future is heavily discounted. If the interest rate were to fall to 9%, the asset price would rise to 1111.11 ($100/.09). The asset is worth more at a lower interest rate because the future counts for more but not that much more since the far future is still discounted to near zero. On the other hand, if the interest rate were .02 the asset would be worth $5000, much more since the future is discounted less heavily. Most importantly, notice that if the interest rate were to fall the same amount as before to .01 then the asset price doubles to $10,000. Thus, when interest rates are low we can expect very wide swings in asset prices. The figure illustrates:

The Gordon model is simple, of course, but adding other factors such as possible variations in dividend growth rates tends to reinforce the conclusion. At low interest rates, for example, even small variations in dividend growth rates will also generate large swings in asset prices.

The lesson is that QE doesn’t have to generate bubbles to generate wide swings in asset prices it just has to lower interest rates.

Indian food price inflation

Vegetable prices in India spiked 46.59% in July year over year, another ugly bullet point in the country’s persistent struggle with massive food inflation.

The longer story is here.

Last week an Indian truck was hijacked for its forty tons of onions. Here are Brendan Greeley and Kartik Goyal on India’s onion price crisis.

By the way, the falling rupee is not helping India’s export performance. The rupee is also creating planning horizon problems for Indian corporations.

What is the right way to think about China’s foreign reserves?

They are not just a big treasure chest for the absorption of bad debts. Paul J. Davies writes:

To buy the dollars that China does not want sloshing around the economy, the central bank creates Renminbi. However, in order to avoid a big money-printing exercise it also issues treasury notes into the market to soak up – or sterilise – the local currency created to buy the foreign currency.

The vast majority of the foreign exchange reserve assets at the People’s Bank are matched by Renminbi liabilities in China’s banks and other financial institutions. If it tries to spend dollars without repaying these liabilities it undoes its earlier sterlisation and prints money. If China wants to print money to soak up its bad debts – and take the risks that come with this policy – its foreign reserves are really irrelevant to that decision.

The other problem with “spending” these reserves lies in the misconception that they are an asset of the country – something like its retained profits from its trade with the outside world.

China has run a current account surplus of increasing size since the late 1990s. A good chunk of this is money paid for goods and services sold – but another good chunk is foreign direct investment. This is not money handed over by outsiders never to be seen again. (Okay, so maybe it often seems like it is, but losing to money to fraud and bad investments is not the point here…)

The point is that the stock of net foreign direct investment represents a liability of the country to outsiders – it is plant, equipment, streams of future profits and so on that are owned by foreigners not by Chinese.

This is interesting too:

Betweeen 2008 and 2012, the total accumulated by China, India, Korea, Taiwan, Hong Kong, Singapore, Indonesia, Malaysia, Thailand and The Philippines almost exactly matches the growth in the US federal Reserve’s balance sheet due to quantitative easing. As he says, the correlation appears very high.

What this suggests – and what is backed up by data from Hong Kong banks in particular – is that along with FDI, China has recently drawn in a lot of cheap credit from overseas. This also amounts to an external liability against the forex assets.

Here is more.

Chinese insurance markets in everything

People in 41 cities in China can insure their enjoyment of the full moon during the Mid-Autumn Festival from Monday.

An internet-based insurance product was launched by Taobao Insurance under the Alibaba Group, China’s largest online shopping platform, together with Allianz China General Insurance Company.

Internet users can insure themselves against inconveniences during their moon gazing at the Mid-Autumn Festival, and will be paid off if they cannot see the moon because of poor weather on the day.

Residents of cities of Shanghai, Guangzhou and Shenzhen can pay a premium of 20 yuan (US$3.24) and receive 50 yuan (US$8) from the insurer if they cannot see the moon.

People living in 41 cities of China, including the three cities above and the country’s capital of Beijing, can pay a premium of 99 yuan (US$16) and receive 188 yuan (US$31) if they fail to see the moon through poor weather. Everyone who purchases the insurance will get a box of mooncakes as well.

Here is more, and for the pointer I thank Jonathan Zhou.

The economics of the war in Syria

The Dubai market just crashed seven percent, image here. Here is a longer story. The Saudi market is falling too; in theory that market is soon opening up to foreign investors. There are rumors that the Saudis are offering the Russians goodies to back away from supporting Assad.

The price of oil is going up.

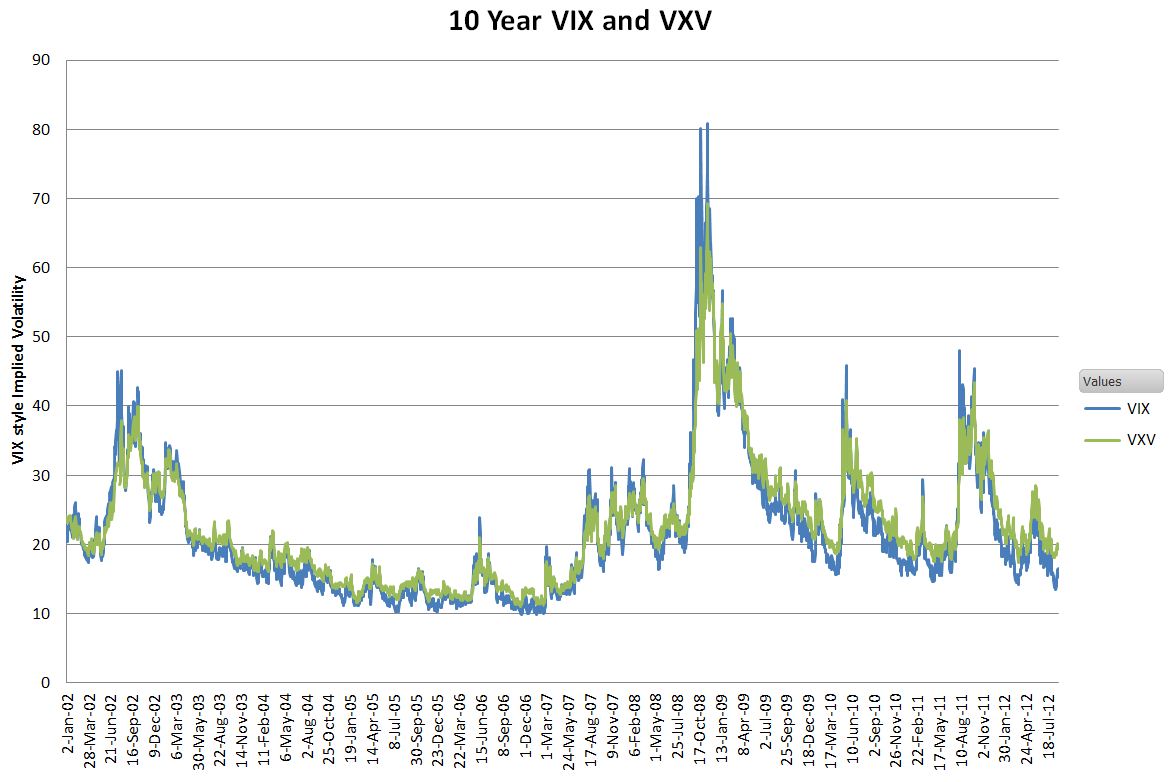

Measuring risk with VIX and VXV

Discussing Robert Hall’s latest (pdf), Paul Krugman asks for a measure which shows the evolution of the risk premium for the U.S. economy. Here is one possible candidate:

Here is one discussion of that graph, and the difference between VIX and VSV. Here is a systematic look at VIX. It is “…a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. Since its introduction in 1993, VIX has been considered by many to be the world’s premier barometer of investor sentiment and market volatility.”

You can see that as of late 2011 measured risk is still fairly high. A wag might also wonder about the risk of measured risk and that seems to show a few noticeable bounce backs since the worst of the crisis period, suggesting that the U.S. economy has not really been in the clear.

Another relevant measure of risk is that people were for years willing to lend the Treasury money at negative two percent real rates of return, and at a time when equity returns turned out to be strongly positive and growth was moderately positive. That is to me the single strongest piece of information about risk. Someday (already?) we’ll look back and marvel at those prices.

This report from the Cleveland Fed shows how much small business lending has dried up, and much of this turns up in quantities rather than prices.

So in my view the evidence for higher risk premia is quite strong.