Shout It From the Rooftops: Parking is a Scarce Resource!

Donald Shoup, whose work on parking has been featured on MR on several occasions, is retiring. Patrick Siegman, “the first Shoupista”, has written an appreciation which includes this excellent quote from Shoup’s classic study, Cashing Out Employer-Paid Parking:

Minimum parking requirements in the planning profession are closely analogous to bloodletting in the medical profession. For over two thousand years doctors prescribed bloodletting to cure most diseases, and medical textbooks contained elaborate parking-requirement-like tables telling exactly how much blood should be let from exactly which part of the body, and when, for every disease…

One strong similarity between bloodletting and minimum parking requirements is the general public acquiescence to both practices without any scientific research on their effects…

Another similarity between bloodletting and minimum parking requirements is the harm caused by both practices. In the case of bloodletting, the problem was magnified because physicians didn’t clean their instruments before proceeding to the next patient. In the case of parking requirements, the problem is magnified when planners require far more parking than is demanded even when all parking is free. Recall here that Willson (1992) found that the number of parking spaces required by zoning ordinances was double the peak accumulation of cars parked at suburban office sites in Southern California.

A final similarity between bloodletting and minimum parking requirements is that the practice of bloodletting gradually fell out of use, and minimum parking requirements in zoning ordinances are gradually being replaced by parking caps.

For much of his career, Shoup was a lonely voice shouting in the wilderness but he shouted reason and fact and his work has had increasing influence in recent years.

Addendum: Here is Tyler’s NYT column on Shoup’s work, Free Parking Comes at a Price.

Adjudicating the Krugman-Bernanke debate on secular stagnation

Here is Krugman’s long and complex post, do read it carefully. Here are a few points:

1. Bernanke said that non-secular stagnation in other countries might cause capital outflows and thus exchange rate depreciations in the potentially ss (secular stagnation) countries, thereby boosting their exports and demand.

2. Krugman argues in return that those real interest rate differentials will be offset by expected exchange rate appreciation, so the capital outflows won’t be so profitable. Why switch funds from a stagnating Europe to a non-stagnating India, if expected euro appreciation will wipe out potential profits in India from the point of view of an investor in Europe?

3. I think that is the wrong comparison of interest rates and the wrong metric of expected currency appreciation.

4. Rather than looking at real interest rate differentials, take the market’s implied prediction for the euro to be the forward-futures exchange rates. These futures rates match the differences in nominal rates on each currency across the relevant time horizons. Those equilibrium relationships hold true with or without secular stagnation, whether in one country or in “n” countries, and from those relationships you cannot derive the claim that expected currency movements offset cross-border differences in real rates of return.

4b. (It is the nominal rate here because, from the point of view of a European investor, your final real return in terms of your own unit of account depends on a combination of the nominal rate abroad, combined with expected future currency conversion rates. Got that?)

5. In that setting, rates of return in non-ss countries still will drive capital flows toward those countries (and an exchange rate depreciation, and thus higher exports, for the origin country, in this case the eurozone.)

6. The best way to speak of the non-ss countries, for international economics, is that their corporate sectors offer nominal expected rates of return which are relatively high, compared to their nominal government bond rates. Once you see this as the correct terminology, it is obvious that capital still will flow outwards to the non-ss countries, even with expected exchange rate movements. The excess profits are there, capital flows out, the euro weakens or appreciates less strongly, and eurozone exports are stimulated, as Bernanke had analyzed.

7. Theory aside, some of the empirics suggest exchange rates often are close to a random walk (pdf), as opposed to being predicted by nominal interest rate differentials. This still supports the Bernanke hypothesis.

8. Yes, I am familiar with the Frankel (1979) strand of the literature on how real interest differentials can forecast currency changes, but it is actually a theoretical puzzle that domestically measured real interest rates (sometimes) have had this explanatory power. And most importantly in this literature high real rates of return tend to predict currency appreciation, not depreciation, so funds should flow all the more to the higher return venues. It is not a rigorous relationship in any case. And on top of that Mishkin (1984), among others, has shown such an equalization on the real interest rate, across borders, is rejected by the data.

9. So I agree with Bernanke. We should not think of real interest rate differentials as being washed out by expected currency movements. And then the flow of investment abroad can break the secular stagnation chain of reasoning.

10. Bernanke is not arguing that “currency movements and export boosts will set everything right.” I take him to be suggesting “if the problem were so fully one of the demand-side, currency movement and export boosts could set everything right.” But since it seems they can’t set everything right, we should infer it is not a problem of the demand side only. That is a subtle but important difference in argumentation.

11. Personally, I favor supply-side over demand-side analysis for the long run.

Capital average is over

Peter Orszag reports:

During roughly the same period, the return on invested capital — that is, how much profit is generated for each dollar of investment — also grew more unequal between companies. While the typical return was roughly constant, at about 10 percent, returns became more dispersed over time.

In particular, from 1965 to 1967, only 1 percent of non-financial firms earned returns of 50 percent or more, but from 2005 to 2007, 14 percent did. In other words, 50 years ago, one out of 100 firms earned 50 percent returns. More recently, one out of seven did.

These data suggest three things: First, the typical return to capital hasn’t changed much, which is what you would expect, given that the capital-output ratio excluding land and housing has been stable.

Second, from company to company, that return has become much more unequal, as has productivity. Some of this inequality between companies in returns and productivity tends to spill over into wages. And this is precisely what we’ve seen. It explains more of the rise in overall earnings inequality than does the increased gaps between the pay of higher earners and rank-and-file workers within a given company.

The full article is here.

MOOC sentences to ponder, and the law of demand still holds

“What jumped out for me was the survey that revealed that in some cases as many as 39 percent of our learners are teachers,”

There are two ways to view this. One is that educators are simply talking to each other. The alternative — more likely in my view — is that on-line and face-to-face education are in fact complements, but also that our educators know much less than they sometimes let on. They need MOOCs to learn the material, or more optimistically to improve their presentations of it.

And how is this for the law of demand?:

Across 12 courses, participants who paid for “ID-verified” certificates (with costs ranging from $50 to $250) earned certifications at a higher rate than other participants: 59 percent, on average, compared with 5 percent. Students opting for the ID-verified track appear to have stronger intentions to complete courses, and the monetary stake may add an extra form of motivation.

I’ve long thought the standard meme “Only [small number goes here] percent of starters complete free MOOCS” was a weak argument. This shows you why.

The piece discusses other interesting results as well.

Assorted links

1. Soda taxes don’t seem to work.

2. Can a health care company actually satisfy the customer?

3. How hard is it to become really good at table tennis? And the common law origins of the infield fly rule.

4. Summers responds to Bernanke. And Robert Moses responds to Robert Caro. And Bernanke on the global savings glut.

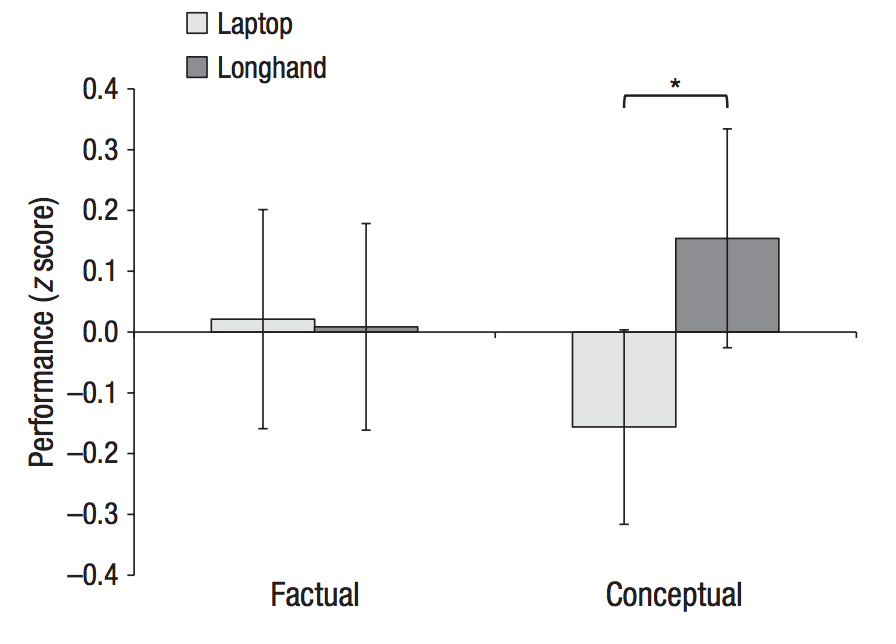

Why you should take notes by hand — not on a laptop

Vox reports on a study comparing taking notes by hand versus using a laptop

For the first study, the students watched a 15-minute TED talk and took notes on it, then took a test on it half an hour afterward. Some of the test questions were straightforward, asking for a particular figure or fact, while others were conceptual, and asked students to compare or analyze ideas.

The two groups of students — laptop users and hand-writers — did pretty similarly on the factual questions. But the laptop users did significantly worse on the conceptual ones:

The problem appears to be that the laptop turns students into stenographers, people who write down everything they hear as quickly as they can. Students who take handwritten notes, however, try to process the material as they are writing it down so that they only have to write down the key ideas. Forcing the brain to extract the most vital information is actually when the learning happens.

The laptops resulted in worse learning even under the study conditions when they were actually used to take notes. In the real world, the laptops are a tempting distraction. I am reminded of the day my son came to my class. He sat in the back and afterwards he said “Dad, I can see why you are so interested in online education. Half of your students are online during your class already.”

Why the world is getting weirder (and will get weirder yet)

It used to be that airliners broke up in the sky because of small cracks in the window frames. So we fixed that. It used to be that aircraft crashed because of outward opening doors. So we fixed that. Aircraft used to fall out of the sky from urine corrosion, so we fixed that with encapsulated plastic lavatories. The list goes on and on. And we fixed them all.

So what are we left with?

Sadly, we all know the answer to that question.

…And so, with more rules we have solved most of the problems in the world. That just leaves the weird events left like disappearing 777’s, freak storms and ISIS. It used to be that even minor storms would be a problem but we have building codes now (rules). Free of rules, we’d probably have dealt with ISIS by now too.

Ultimately, this is why the world is getting weirder, and will continue to do so. Now with global media you get to hear about it all.

That is from a very interesting mini-essay by Steve Coast, hat tip goes to The Browser.

How universal are rates of social mobility across time and societies?

Gary Solon, in a new survey paper, takes issue with the earlier results of Greg Clark, which had suggested social mobility was roughly constant across a wide spectrum of cases. Solon writes:

…the results reported by Clark do not reflect a universal law of social mobility. Quite to the contrary, other studies based on group-average data, even surnames data, frequently produce intergenerational coefficient estimates much smaller than Clark’s.

A second testable prediction of Clark’s hypothesis…is that instrumental variables (IV) estimation of the regression of son’s log earnings on father’s log earnings should yield a coefficient estimate in the 0.7-0.8 range if father’s long earnings are instrumented with grandfather’s log earnings. When Lindahl et al, estimated that regression with their data from Malmo, Sweden, the IV coefficient estimate was 0.15, considerably higher than their ordinary least squares (OLS) estimate of 0.303. They obtained a remarkably similar comparison of IV and OLS estimates when they used years of education instead of log earnings as the status measure. The pattern of IV estimates exceeding OLS estimates is consistent with Clark’s general story about measurement error in particular indicators as proxies for social status. It is equally consistent with all the alternative stories listed in section II for why grandparental status may not be “excludable” from a multigenerational regression. What the results are not consistent with is a universal law of social mobility in which the intergenerational coefficient is always 0.7 or more…

A third testable prediction…is that using an omnibus index that combines multiple indicators of social status should make the intergenerational coefficient estimate “much closer to that of the underlying latent variable.” [But]…The resulting estimate was not “much closer” to the 0.7-0.8 range.

In sum, when Clark’s hypothesis is subjected to empirical tests, it does not fare so well.

Here is an ungated version.

Ben Bernanke on the secular stagnation hypothesis

Here is his second real blog post. Excerpt:

My greatest concern about Larry’s formulation, however, is the lack of attention to the international dimension. He focuses on factors affecting domestic capital investment and household spending. All else equal, however, the availability of profitable capital investments anywhere in the world should help defeat secular stagnation at home. The foreign exchange value of the dollar is one channel through which this could work: If US households and firms invest abroad, the resulting outflows of financial capital would be expected to weaken the dollar, which in turn would promote US exports. (For intuition about the link between foreign investment and exports, think of the simple case in which the foreign investment takes the form of exporting, piece by piece, a domestically produced factory for assembly abroad. In that simple case, the foreign investment and the exports are equal and simultaneous.) Increased exports would raise production and employment at home, helping the economy reach full employment. In short, in an open economy, secular stagnation requires that the returns to capital investment be permanently low everywhere, not just in the home economy. Of course, all else is not equal; financial capital does not flow as freely across borders as within countries, for example. But this line of thought opens up interesting alternatives to the secular stagnation hypothesis, as I’ll elaborate in my next post.

Keep ’em coming Ben, but you’re not a real blogger until you’ve covered the infield fly rule…

China fact of the day

New brokerage accounts have surged since China’s bull market got running mid-2014. The number of new trading accounts hit a five-year high in early March. But as you can see in the chart above, a lot of those new investors probably aren’t the savviest.

Some 67.6% of households that opened new accounts in the past quarter haven’t graduated from high school, according Orlik’s chart, which comes from a large-scale quarterly national survey of household assets and income conducted by Gan Li of the Southwestern University of Finance and Economics. Only 12% have a college education. Among existing investors surveyed, only 25.5% lack a high school diploma; 40.3% have finished college.

From Gwynn Guilford, there is more here.

*Genealogy of American Finance*

By Robert E. Wright and Richard Sylla, Columbia Business School Publishing, this is both a beautiful picture book, coffee table style, and also a history of America’s “Big 50” financial institutions. It appears to be a very impressive creation, full of useful information.

File under “Arrived in my Pile”! You can order it on Amazon here.

Tuesday assorted links

Are more egalitarian societies more likely to adopt school vouchers?

Timothy Hicks has a new and recently published paper:

It is argued in this article that the marketisation of schools policy has a tendency to produce twin effects: an increase in educational inequality, and an increase in general satisfaction with the schooling system. However, the effect on educational inequality is very much stronger where prevailing societal inequality is higher. The result is that cross-party political agreement on the desirability of such reforms is much more likely where societal inequality is lower (as the inequality effects are also lower). Counterintuitively, then, countries that are more egalitarian – and so typically thought of as being more left-wing – will have a higher likelihood of adopting marketisation than more unequal countries. Evidence is drawn from a paired comparison of English and Swedish schools policies from the 1980s to the present. Both the policy history and elite interviews lend considerable support for the theory in terms of both outcomes and mechanisms.

There are less gated versions here, and for the pointer I thank the excellent Kevin Lewis.

The Aztec diet was more nutritious than it may seem at first

Colin M. MacLachlan, in his splendid Imperialism and the Origins of Mexican Culture, reports:

1. Corn gruel and tamales were reinforced with fish, seeds of various kinds, fruit, and honey.

2. Beans were supplemented with meat from iguanas, armadillos, and rabbits.

3. The calcium content of corn was (and still is) increased by alkaline cooking with lime (“nixtamalization,” duh).

4. “Pulque” has “substantial food value,” “whether fermented or fresh.”

5. Dried red maguey worms have 71 percent protein.

6. Axayacatl (a species of aquatic insect sometimes called “water boatmen“) have 68.7% protein.

7. Mesquite pods and seeds have high caloric value.

8.”Tecuitlatl (spirulina), the green scum collected from lakes with high saltwater content, was sold in the market to be eaten with chilies and tomatoes and has been shown to be a modern wonder food.”

As you can see, the world of food really could have evolved along very different lines.

I also enjoyed this line from the book:

The fundamental belief that the gods sacrificed themselves to create the Earth and continued to do so to sustain it locked the gods and humans into a circular dependency — a relationship characterized by fearful respect coupled with regulated violence.

Definitely recommended, and oh yes that reminds me, here is the livestream for my chat later today with Peter Thiel.

Headlines to ponder

Bank of Bird-in-Hand is the only new bank to open in the U.S. since 2010, when the Dodd-Frank law was passed

The WSJ story is here, via Binyamin Appelbaum.