My Law and Literature reading list, Spring 2010

The semester is underway!

The New English Bible, Oxford Study Edition.

In the Belly of the Beast, by Jack Henry Abbott.

Borges and the Eternal Orangutans, by Fernando Verrissimo.

Glaspell’s Trifles, available on-line.

Sherlock Holmes, The Complete Novels and Stories, Sir Arthur Conan Doyle, volume 1.

I, Robot, by Isaac Asimov.

Moby Dick, by Hermann Melville, excerpts, chapters 89 and 90, available on-line.

Year’s Best SF 9, edited by David G. Hartwell and Kathryn Cramer.

Oscar Wilde, De Profundis.

Kathryn Davis, The Walking Tour.

Nadezhda Mandelstam, Hope Against Hope: A Memoir.

Haruki Murakami, Underground: The Tokyo Gas Attack and the Japanese Psyche.

Timothy J. Gilfoyle, A Pickpocket’s Tale.

Henning Mankell, Sidetracked.

Edgar Allen Poe, The Gold-Bug, available on-line.

Walker Percy, The Thanatos Syndrome.

We also will view a small number of movies.

Peter Leeson update

He is now the North American editor of Public Choice, replacing Michael Munger and of course we all congratulate him. I have a modest proposal for how he should referee submitted papers, let's see if he uses it.

More on the economics of credit cards

Joshua Gans directs my attention toward this symposium, led by Geoffrey Manne. Here is an excerpt from Manne's summary statement:

…theory and empirical evidence suggest that lowering interchange fees does nothing to help consumers, and in fact harms them by raising annual fees and thus again by limiting competition among cards at the point of sale. Perhaps there is some policy reason why we would want to help merchants at the expense of consumers, but the issue, often framed as merchants and consumers against banks and card networks, really seems to be merchants against consumers. At best, we have no idea what the full social implications of capping interchange fees would be–but there is still a conflict between merchant and consumer interests, and we should be wary.

Here is Joshua Gans's post on the importance of the "no surcharge rule":

The better rule to subvert would be the ‘no surcharge rule’ that prevents merchants from offering different prices to consumers based on payment instrument. That rule was abandoned in Australia and we see many instances where it bites. In that situation, the strong theoretical prediction is that what fees Visa uses to extract payments from merchants do not matter for overall efficiency; even if they do matter for prices. This is one of those cases where there are relatively simple regulatory interventions to try that could have a big effect.

I am not endorsing all of these materials but simply offering them up for evidence that a moral condemnation of Visa is an overly hasty response.

Assorted links

2. New story on high-frequency trading.

3. 2010 book preview; oddly not one of them excites me except maybe the Per Petterson.

4. The music industry of the future?

5. "Superstar teachers had four other tendencies in common: they avidly recruited students and their families into the process; they maintained focus, ensuring that everything they did contributed to student learning; they planned exhaustively and purposefully–for the next day or the year ahead–by working backward from the desired outcome; and they worked relentlessly, refusing to surrender to the combined menaces of poverty, bureaucracy, and budgetary shortfalls." More here.

6. Why the Eurozone has a tough decade to come.

7. Ezra Klein is on Colbert tonight, early part of the show. Today his WP blog is broken so he can't announce it.

The Visa fees article

Everyone is blogging about it, here is the link. Kevin Drum has one good summary, or here is Yves Smith or Felix Salmon, both of whom are upset. The upshot is that the supermarket pays Visa a fee if you use a "sign for it" card rather than entering a PIN number for a debit card, though it's a little more complicated than that.

My practice does not match the setting of the article exactly, but here's how it goes. As Natasha forced me to internalize years ago, when I use my Visa credit card, and sign for payment, I receive frequent flyer miles. When I use my Visa BB&T debit card (yes, my two main payment cards are both Visa), I don't get anything back. By using the credit card, resources are redistributed away from the store and to both Visa and me. On net that's a better deal for me and that's why I end up signing so often. This could be efficient too, in a constrained second best sense. For one thing, it indicates the supermarket was earning ex ante monopoly profit; is it so tragic for some of that profit to be split by Visa and me? One way to understand Visa is that it is supplying countervailing power by "organizing" consumers against the retail monopoly and distributing the gains from the new bilateral monopoly arrangement.

There's nothing to stop the store from offering me frequent flyer miles, or other forms of discount, if I use a means of payment which they prefer. I've yet to see a deal good enough to make me switch. (When Sears pushes this on me, I just say no because Visa offers me a better deal.) And I find it easy enough to believe that the petty monopoly of the local grocer is more significant than the market power in the potentially more contestable cards and payment market.

Again, I don't know how much of the entire market works on the basis that I experience. But it's one simple example of how "higher fees" can be good rather than bad.

Not long ago Ronald Coase turned 99 years old and I am delighted to see he is still alive. His ideas are still alive too.

Addendum: When issues of this sort arise, there is a common pattern in blogospheric discussion: Blogger A criticizes a market practice with tones of absolute condemnation. Blogger C (in this case, me!) responds with a plausible scenario, and a microeconomics-consistent first-order explanation, that things aren't so bad after all. Blogger D tries to defend Blogger A by shifting the burden of proof to Blogger C to demonstrate that markets are efficient in such a case and by leveling charges of market fundamentalism and by citing some second or third best arguments that the market can fail after all. Don't be fooled by that polemic slide in emphasis; the burden of proof is on the critics here — those asserting the existence of an evil and asking us to move beyond a loose agnosticism – not on me.

French sales start today, by law

Trading laws stipulate that there are two periods for sales in France. Winter sales from January to February and summer sales from June to July. In each case, the sales last for five weeks. All goods on sale must have been in the shop for a minimum of thirty days prior to the sale date – nu buying in cheap stock and selling it as a sale item. Reuctions must ne visibly displayed in percentage terms. labels must also show the old pre sale price and the new sale price. Retaiers are allowed to reduce their prices three times in the sales – after the first fortnight, and again in the final week.

Outside the official sale periods, retailers are allowed two weeks in the year, to use at their discretion, for extra sales such as pre-christmas sales or spring sales.

…Tomorrow morning [today] many shops (with permission from their local trading authorities) will be opening at 7am. Needless to say that the starting date is a national one decreed by the government.

Here is more information and I thank Bill Hawshaw for the pointer.

Ben Casnocha on advice

He enumerates fourteen interesting points, here is one of them:

2. We overvalue advice on difficult decisions and undervalue advice on easy ones. So say some studies. During the college admissions process, kids get a million opinions on an admittedly important and difficult situation, but in the end receive so many contradictory thoughts that they end up confused. On the other hand, when faced with where to go for lunch, people would do better to ask around a bit for a recommendation.

Ben also tweets:

Lists of numbered points where the total number is too pat (5, 10, 15, 20, etc) usually have more fluff than a list of points w/ an odd #.

Assorted links

Words of Wisdom from Robert Shiller

Strategic default on mortgages will grow substantially over the next

year, among prime borrowers, and become identified as a serious

problem. The sense that ‘everyone is doing it’ is already growing, and

will continue to grow, to the detriment of mortgage holders. It will

grow because of a building backlash against the financial sector,

growing populist rhetoric and a declining sense of community with the

business world. Some people will take another look at their mortgage

contract, and note that nowhere did they swear on the bible that they

would repay.

From the WSJ's Real Time Economics.

The economics of advice

At times I believe the following propositions, in appropriately qualified fashion:

1. You don't know what a person really thinks until you hear his or her advice. Along these lines, if you really want to know what a person thinks, ask for advice and he or she will open up.

2. In philanthropy there is a saying: "Ask for money and you will get advice. Ask for advice and you will get money."

3. There are many exacting scholars who should be locked in a room, asked for advice of various kinds, and forced to speak into a tape recorder with no edits allowed. The advice-giving mode mobilizes insights which otherwise remain dormant, perhaps for fear of falsification or ridicule or of actually influencing people. All of the transcripts should be put on The Advice Website, with an open comments section, to limit the actual influence of the advice. Some famous people would be revealed as foolish in critical regards. The contents would be most interesting as non-advice and the site would carry a government warning that the advice is not to be taken seriously.

4. Often we do not trust people until we hear their advice. We suspect in any case that they wish to control us, and until we know what they have in mind, we remain wary. Sometimes it is necessary to give advice — even pointless advice — to establish trust.

These remarks are not intended to apply to medical or clinical advice.

Here is Bryan Caplan, offering direct advice to his colleagues (an excellent post). Brett Arends questions whether you should take advice from people who write for a living.

Daron Acemoglu on the U.S.-Mexican border

Via Arnold Kling, Acemoglu writes:

On one side of the border fence, in Santa Cruz County, Arizona, the median household income is $30,000. A few feet away, it's $10,000….The key difference is that those on the north side of the border enjoy law and order and dependable government services — they can go about their daily activities and jobs without fear for their life or safety or property rights. On the other side, the inhabitants have institutions that perpetuate crime, graft, and insecurity.

With apologies to Douglass North, I am rarely happy with this kind of explanation. First, are the bad institutions cause or effect? Most likely we need a framework which allows them to be both.

Second, I want the theory to also explain the (quite large) difference between the truly poor Chiapas and the relatively wealthy northern Mexico. By many metrics northern Mexico is more corrupt than Chiapas (there is more to be corrupt over, for one thing, plus drug routes play a role) and it very likely has higher rates of violent crime. In general I prefer theories which explain three data points to theories which explain two. Chiapas, of course, isn't some weird outlier which I pulled out of a hat; it's in the same country as northern Mexico and many people from that region have populated both northern Mexico and Arizona for that matter. I could have picked many other parts of Mexico as well.

One factor is positive selection into northern Mexico, on grounds of ambition and desire for higher wages. Another factor is that northern Mexican norms are (partially) geared to support American multinationals and these norms have spread more generally, including to Mexican enterprises in the region.

On another point, as I get older, I tend to view "family structure which encourages an obsession with education" as an increasingly important variable for explaining levels in per capita income, if not always growth rates in the immediate moment. It's not a truly independent variable — when it comes to growth what is? — but it's one good place to start. It helps explain why the Soviet Union, after decades of state fascism/communism, slid into a living standard higher than that of much of Latin America. It explains quite a bit of Arizona vs. Mexico but less of northern Mexico vs. Chiapas. Acemoglu mentions education in his article, but he seems to view it as resulting from instiutions rather than causing them.

I don't buy into the genetic explanations but still I view "family structure which encourages an obsession with education" as very hard to replicate through policy. Emmanuel Todd's The Causes of Progress has many problems, but it is an under-mined book when it comes to the causes of both liberty and economic growth.

Assorted links

1. Ask Felix Salmon anything, via Chris F. Masse.

2. Brad DeLong on studying heterogeneous capital.

3. Where does Chinese inflation go?

4. Via Felix Salmon, very good Sana'a image.

Markets in everything, South Korean faux funeral edition

Jung, a slight 39-year-old with an undertaker's blue suit and a

preacher's demeanor, is a resolute counselor on the ever-after who

welcomes clients with the invitation, "OK, today let's get close to

death."Jung runs a seminar called the Coffin Academy, where,

for $25 each, South Koreans can get a glimpse into the abyss. Over four

hours, groups of a dozen or more tearfully write their letters of

goodbye and tombstone epitaphs. Finally, they attend their own funerals

and try the coffin on for size.In a candle-lighted chapel, each

climbs into one of the austere wooden caskets laid side by side on the

floor. Lying face up, their arms crossed over their chests, they close

their eyes. And there they rest, for 10 excruciating minutes."It's

a way to let go of certain things," says Jung, a former insurance

company lecturer. "Afterward, you feel refreshed. You're ready to start

your life all over again, this time with a clean slate."Across

South Korea, a few entrepreneurs are conducting controversial forums

designed to teach clients how to better appreciate life by simulating

death. Equal parts Vincent Price and Dale Carnegie, they use mortality

as a personal motivator for a variety of behaviors, from a healthier

attitude toward work to getting along with family members.Many

firms here see the sessions as an inventive way to stimulate

productivity. The Kyobo insurance company, for example, has required

all 4,000 of its employees to attend fake funerals like those offered

by Jung.

The full article is here and I thank Kaylin Wainwright and Daniel Lippman for the pointers. Here is an earlier MR post on how contemplating mortality changes your behavior.

The charity tax

The estimated social pressure cost of saying no to a solicitor is $3.5 for an in-state charity and $1.4 for an out-of-state charity. Our welfare calculations suggest that our door-to-door fund-raising campaigns on average lower utility of the potential donors.

That's from Stefano DellaVigna, John List, and Ulrike Malmendier. You'll find an ungated copy here.

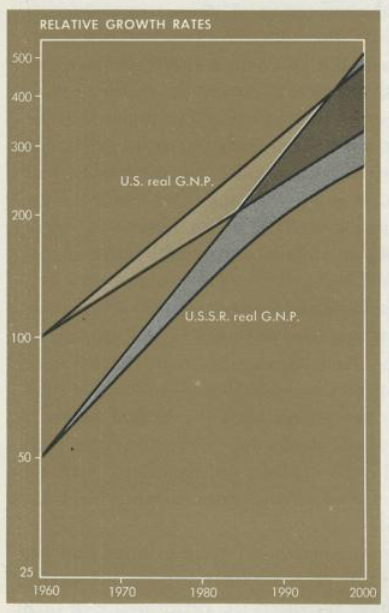

Soviet Growth & American Textbooks

In the 1961 edition of his famous textbook of economic principles, Paul Samuelson wrote that GNP in the Soviet Union was about half that in the United States but the Soviet Union was growing faster. As a result, one could comfortably forecast that Soviet GNP would exceed that of the United States by as early as 1984 or perhaps by as late as 1997 and in any event Soviet GNP would greatly catch-up to U.S. GNP. A poor forecast–but it gets worse because in subsequent editions Samuelson presented the same analysis again and again except the overtaking time was always pushed further into the future so by 1980 the dates were 2002 to 2012. In subsequent editions, Samuelson provided no acknowledgment of his past failure to predict and little commentary beyond remarks about “bad weather” in the Soviet Union (see Levy and Peart for more details).

Among libertarians, this story has long been the subject of much informal amusement. But more recently my colleague David Levy and co-author Sandra Peart have discovered that the story is much more interesting and important than many people, including myself, had ever realized.

Among libertarians, this story has long been the subject of much informal amusement. But more recently my colleague David Levy and co-author Sandra Peart have discovered that the story is much more interesting and important than many people, including myself, had ever realized.

First, an even more off-course analysis can also be found in another mega-selling textbook, McConnell’s Economics (still a huge seller today). Like Samuelson, McConnell estimated Soviet GNP as half that of the United States in 1963 but he showed that the Soviets were investing a much larger share of GNP and thus growing at rates “two to three times” higher than the U.S. Indeed, through at least ten (!) editions, the Soviets continued to grow faster than the U.S. and yet in McConnell’s 1990 edition Soviet GNP was still half that of the United States!

A second case of being blinded by “liberal” ideology? If so, Levy and Peart throw another curve-ball because the very liberal even “leftist” texts of the time, notably those by Lorie Tarshis and Robert Heilbroner did not make the Samuelson-McConnell mistake.

Tarshis and Heilbroner were more liberal than Samuelson and McConnell but offered a more nuanced, descriptive and tentative account of the Soviet economy. Why? Levy and Peart argue that they were saved from error not by skepticism about the Soviet Union per se but rather by skepticism about the power of simple economic theories to fully describe the world in the absence of rich institutional detail.

To make their predictions, Samuelson and McConnell relied heavily on the production possibilities frontier (PPF), the idea that the fundamental tradeoff for any society was between “guns and butter.” Thus, in the 1948 edition Samuelson wrote:

The Russians having no unemployment before the war, were already on their Production-possibilities curve. They had no choice but to substitute war goods for civilian production-with consequent privation.

Note that Samuelson assumes all countries and economic systems are efficient (the Russians are “on” the curve) only the choice of guns versus butter differs. When the war ended, the fundamental tradeoff became one between investment and consumption and since the Soviets invested a greater share of GNP they would naturally consume less but grow faster. Moreover, since the Soviet’s had solved the unemployment problem they were, if anything, more efficient than the U.S. (here we see the Keynesian influence).

Levy and Peart conclude that although ideology may have played a role what arguably made a bigger difference was the blindness imposed by chosen tools. As they write:

We are all constrained by means of models: we gain insight in one dimension by blinding ourselves to events in other dimensions. Competition among models may be necessary to insure that the benefits of the models exceeds their cost.

(Applications to the financial crisis are apposite.)

Addendum: Bryan Caplan also comments. As Bryan notes, a very good economist can use PPFs and still get the story right.