Some blurbs for *Talent*, with Daniel Gross

“Talent” is what happens when two brilliant and profoundly iconoclastic minds apply their imagination to one of the hardest of all business problems: the search for good people. I loved it.”

–Malcolm Gladwell

“Talent is everything―whether in investing and building startups, or in other creative endeavors. Between product, market, and people, I’ve always bet on the last one as the biggest predictor of success. But while talent may be everywhere, it’s unevenly distributed, and hard to ‘find.’ So how do we better discover, filter, and match the best talent with the best opportunities? This book shares how, based on both scientific research and the authors’ own experiences. The future depends on this know-how.”

―Marc Andreessen, co-founder of Netscape and Andreessen Horowitz

“The most important job of any leader is to find individuals with a ‘creative spark,’ and the potential to discover, invent and build the future. If you want to learn the art and science of spotting and empowering exceptional people, Talent is brimming with fresh insights and actionable advice.”

―Eric Schmidt, co-founder of Schmidt Futures and former CEO of Google

“I do not know of any skills more worth developing than the ability to find exceptional undeveloped talent. I have spent many years trying to get good at that, and I was still astonished by how much I learned reading this book.”

Sam Altman, CEO of OpenAI, formerly of YCombinator

“Two of the premier talent spotters working today, Cowen and Gross have written the definitive history of identifying talent. Anyone who is interested in innovation, entrepreneurship, or the roots of America’s start-up economy must read this book.”Christina Cacioppo is CEO and co-founder of Vanta

You can order here on Amazon or here on Barnes & Noble.

Recommended!

Saudi fact of the day

Saudi Aramco has overtaken Apple as the world’s most valuable company after higher oil prices pushed shares of the world’s biggest crude exporter to record levels while a broader tech stock sell-off weighed on the iPhone maker.

The Saudi Arabian oil company’s market capitalisation on Wednesday was $2.426tn, exceeding Apple’s $2.415tn by just over $10bn. It is the first time that Saudi Aramco has regained the top spot since 2020 and follows a broader sell-off in technology stocks since the start of the year.

Apple became the first company to hit a $3tn market cap in early January, although its shares have suffered in recent months as investors reassess lofty valuations in the tech sector in light of a reversal in monetary policy and worries that inflation will weaken consumers’ spending habits.

Here is more from the FT. It will be interesting to see what a world with higher real interest rates looks like…

The most underrated talent in AI?

Who are the most underrated talents in AI and machine learning?

Think technical, and think builders. More Midjourney, Gwern, and 15.ai.

Comments are open, thanks in advance!

Wednesday assorted links

1. “The telltale sign of a successful intellectual life is weirdness – weird in the best possible way.” Short essay on my approach to things, a good piece I thought.

2. How much did slavery and cotton accelerate U.S. economic growth?

3. Will China build a dam with an army of robots and 3-D printers? (Would not take entirely at face value this one.)

The new Derek Thompson project on progress

Today's piece is also an announcement!

I’m launching a new project with @TheAtlantic called “Progress," which pulls together my newsletter, monthly calls with readers on progress and the abundance agenda, and some larger forthcoming projects and events. https://t.co/q1xpHsUNR8

— Derek Thompson (@DKThomp) May 11, 2022

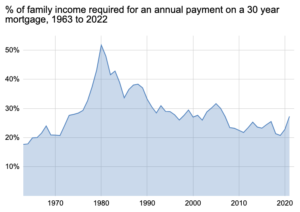

When were U.S. home prices at their worst?

That of course is only one metric, and it focuses on flows rather than homes as an asset. It nonetheless puts a number of matters in perspective. Here it is in words:

1981 was the most unaffordable year for those who need a mortgage, with annual payments consuming a whopping 52% of their income. For comparison, in 2022 mortgage payments require 27% and the absolute lowest point is back in 1963 when only 18% was required. In 2006 (at the peak of the housing bubble), families would need 30% of their income. Thus we can confidently say that 2022 is so far not the worst year in history for those who can’t afford to buy a house without a loan.

Canada and New Zealand seem to be the truly scary places. Here is the full essay by Nikita Sokolsky.

How big a deal would a nuclear explosion be?

I am no longer so sure, as I outlined in my recent Bloomberg column:

Until recently, my view was that any actual use of a nuclear weapon, no matter the scale, would dramatically change everything. Nuclear use would no longer be considered taboo, and the world would enter a state of collective shock and trauma. Other countries around the world would start frantically preparing for war, or the possibility of war.

But recent events have nudged me away from that viewpoint. For instance, I have seen a pandemic that arguably has caused about 15 million deaths worldwide, yet many countries, including the U.S. haven’t made major changes in their pandemic preparation policies. That tells me we are more able to respond to a major catastrophe with collective numbness than I would have thought possible.

Of course I am referring to a smaller tactical nuclear weapon, as might be used against Ukraine. India by the way lost five or so million people during the pandemic and they didn’t even fire their health minister. And:

I also have seen Trumpian politics operate through the social media cycle. Former President Donald Trump did and said outrageous things on a regular basis (even if you agree with some of them, the relevant point is that his opponents sincerely found them outrageous). Yet the rapidity of the social media news cycle meant that most of those actions failed to stick as major failings. Each outrage would be followed by another that would blot out the memory of the preceding one. The notion of “Trump as villain” became increasingly salient, but the details of Trumpian provocations mattered less and less.

Might the detonation of a tactical nuclear weapon follow a similar pattern? Everyone would opine on it on Twitter for a few weeks before moving on to the next terrible event. “Putin as villain” would become all the more entrenched, but dropping a tactical nuclear weapon probably wouldn’t be the last bad thing he would do.

To cite the terminology of venture capitalist Marc Andreessen, the tactical nuclear weapon might stay “the Current Thing” for a relatively short period of time.

Let’s hope we don’t find out.

Fourth Nobel conversation at MRU

On machine learning:

Here are the first three conversations.

Tuesday assorted links

GDPR and the Lost Generation of Innovative Apps

Using data on 4.1 million apps at the Google Play Store from 2016 to 2019, we document that GDPR induced the exit of about a third of available apps; and in the quarters following implementation, entry of new apps fell by half. We estimate a structural model of demand and entry in the app market. Comparing long-run equilibria with and without GDPR, we find that GDPR reduces consumer surplus and aggregate app usage by about a third. Whatever the privacy benefits of GDPR, they come at substantial costs in foregone innovation.

That is from a new NBER working paper by Rebecca Janßen, Reinhold Kesler, Michael E. Kummer & Joel Waldfogel.

“If economists are so smart, why aren’t they rich?”

Peter Coy (NYT) considers a few hypotheses. My take here is pretty simple. Here are three of the main ways to beat market returns:

1. Build a new product and sell it successfully.

2. Assemble and maintain an especially talented team of quants. (It is a separate but still relevant question at what scale you can do this and thus how rich you can become.)

3. “See” something about the market, at least for a limited period of time, that other people do not and invest accordingly. That might be falling interest rates, the rise of consumer tech, or the persistence of low inflation (all until recently!). Note that #3 requires you to have some money in the first place, and for your run to be long enough that you truly become rich.

Putting aside generic demographic factors, there is no particular reason to expect #1 or #2 to be much correlated with expertise in economics.

You might think that #3 is somewhat correlated with expertise in economics, but I don’t think it is very much. You can pile up a bunch of ancillary reasons why economists might not be practically oriented enough to succeed at #3. But even putting all that aside, economic theories of “regime change” just aren’t very good! (It is comparative statics that we excel at, but that knowledge can be replicated and sold cheaply to the rest of the investment community, if it turns out to be valuable.) So knowing economics won’t correlate much with success at strategy #3. And some of those non-economists who succeed at #3 are just lucky anyway.

And that is why, dear reader, most economists are not very rich. You are correct in downgrading their intelligence for these reasons, though there are still some regards in which they are quite smart, such as having ability at hypothesis testing, or perhaps having the ability to ask very good and penetrating questions about economic issues.

Monday assorted links

1. What makes for a good YouTube video?

2. The ten-year anniversary of The Start-Up of You, by Reid Hoffman and Ben Casnocha.

4. Citation practices and the Chicago School of Economics. Interesting results, but too much bad terminology in the abstract! Do the researchers actually not realize this?

5. Jordan Peterson to be Chancellor of Ralston College. Here is the Facebook page for Ralston.

That was then, this is now, cryptocurrency edition

Nouriel Roubini, a blockchain basher who famously called Bitcoin “the mother of all bubbles,” is working to develop a suite of financial products including a tokenized asset intended to act as a “more resilient dollar” in the face of higher inflation, climate change and civil unrest.

Roubini, nicknamed “Dr. Doom” for his bearish views, sees room for an asset-backed digital coin that could help protect against higher prices and benefit from soaring demand for land and commodities, as well as a loss of confidence in fiat currencies. He’s working with Dubai-based Atlas Capital Team LP, which he joined two years ago as co-founder and chief economist, to create the new products.

In doing so, Roubini is tapping into growing concerns over the pace of inflation as well as speculation about the longer-term outlook for the dollar, with prominent financial voices including Bridgewater Associates LP’s Ray Dalio and Credit Suisse AG strategist Zoltan Pozsar having argued the U.S. currency risks gradually losing its reserve status.

The greenback’s lofty position could be in jeopardy as the U.S. “prints too much money and adversaries start de-dollarizing,” Roubini said in an interview. “We recognized that America’s dollar reserve currency could be at risk and are working to create a new instrument that’s effectively a more resilient dollar.”

Unlike many cryptocurrencies, Roubini stresses that the coin would be backed by real assets — a mix of short-term U.S. Treasuries, gold and U.S. property (in the form of Real Estate Investment Trusts, or Reits) that’s expected to be less affected by climate change.

Here is more from Bloomberg. Here are earlier writings of relevance. I’m all for new business ventures, but perhaps he has the inflation timing wrong on this one? In any case, welcome Nouriel to the Austrian School of Economics!

China’s Bizarre Authoritarian-Libertarian COVID Strategy

It’s difficult to understand China’s COVID strategy. On the one hand, China has confined millions of people to their homes, even to the extent of outlawing walking outside or having food delivered. Many thousands of other people have been taken from their homes and put into quarantine centers. On the other hand, vaccination is not mandatory! I can understand authoritarianism. I can understand libertarianism. I have difficulty understanding how jailing people, potentially without food, is ok but requiring vaccinations is not. (Here’s a legal analysis of China’s vaccine policy.) Moreover, put aside making vaccines mandatory because as far as I can tell, China has only recently started to get serious about non-coercive measures to vaccinate the elderly. The Washington Post notes:

The vaccination drive has been mild compared to some of the other pandemic-control measures and did not prioritize the elderly. Some younger people have been required to get vaccinated for their jobs, but vaccination of retirees remains optional. Incentives like eggs, grains and other foodstuffs — a staple of China’s vaccination drive since last year — are now being bolstered by home checkups, mobile clinics and the widespread mobilization of public servantsto ensure the elderly get shots.

China is shutting down factories costing its economy trillions of dollars and the best they come up with to get elderly people vaccinated is egg incentives???!

It’s difficult to understand what the Chinese leadership is thinking. It’s conceivable that the Chinese vaccines are much less effective than we have been led to believe but that seems unlikely. As far as we can tell the Chinese vaccines are not quite as good as the mRNA vaccines but good enough to prevent severe disease and pass FDA approval in the United States. My best guess is that President Xi Jinping is so powerful and insulated from reality and alternative viewpoints that he is just soldiering on either oblivious to the pain and foolishness of his policies or indifferent, much like Mao before him during the great famine.

The Essential Women of Liberty

Here’s another excellent book in the Essential Scholars series. You can download the book for free, find additional resources, introductory videos and more at the Women of Liberty web page.

This series of essays, written by leading scholars in the United States, Canada and Europe, explores the lives and ideas of some of the most influential women over the past few centuries whose work contributed enormously to the democratic, prosperous and free societies that many people enjoy today. They are a remarkably diverse group of women. Their lives span the eighteenth to twenty-first centuries and their contributions are significant despite the barriers each faced. Some were educated at prestigious universities while others only had informal schooling. Some were academics, others writers and journalists, and still others activists. What they had in common was an understanding of the power of freedom and liberty, and their influential advocacy of such during their lives. These essays are a celebration and recognition of their lives and contributions.