Results for “age of em” 17238 found

Might Greece see some version of hyperinflation?

Keep in mind that things can go badly under either a yes or no vote today. (I am not even sure the referendum result will make such a difference, since it is all in the subsequent deal, or lack thereof, and the terms would be different anyway.) Yet I do not think a hyperinflation is the likely result.

As things stand, Greece could run out of euros in well under a week. That is a deflationary pressure. To be sure, Greek companies are already starting to print up various kinds of scrip. But those will be media of exchange priced in terms of euros, not new media of account. The script will to some extent stabilize against deflationary pressures, by preventing a total economic collapse, but they won’t themselves cause hyperinflation. If one company prints up too much scrip, the value of that brand will fall in terms of euros. In contrast, a “domestic” medium of account is usually firmly entrenched in a classic hyperinflation.

Greece may eventually move away from the euro as a medium of account, but that likely would happen only once an alternative payment medium — perhaps the new drachma — is relatively stable in value. Again, there is no expected hyperinflation. Deposit confiscation will be required long before hyperinflation is an option, do note that is not exactly a reassuring thought. In fact hyperinflation is too slow and inefficient a way to steal from the citizenry in this setting.

An interesting set of issues revolves around bill prepayment. If you didn’t know, electronic transfers within the country are still allowed, so everyone is trying to prepay bills rather than receive a haircut on their deposits (see the link above). Various events could speed up or slow down these pressures, for instance greater stability combined with outside aid could limit deposit confiscation risk and thus lower bank deposit velocity. Alternatively, greater risk could cut either way. It could lead to more prepayment and higher velocity, but it also could induce suppliers to take actions to make prepayment harder. There are some complex options here, though still I don’t see them giving rise to a hyperinflation. Again, the key point is that even under Grexit scenarios the euro remains a medium of account for a while still, and deflationary deposit confiscation will be needed before hyperinflation could extract enough seigniorage.

As Frances Coppola points out, Grexit is a process not an event and many of the early and indeed intermediate steps already are underway.

An Abandoned Space Ship

China facts of the day

Greece is small, China is large:

The Shanghai Composite has now fallen 12.1 per cent since Monday, its third consecutive week of double-digit losses since hitting a seven-year high on June 12.

The Shanghai index is firmly in bear market territory, down 28.6 per cent since the June peak, while the tech-heavy Shenzhen Composite has fallen 33.2 per cent.

There were also signs on Friday that the stock market turmoil is beginning to reverberate beyond China. The Australian dollar, often traded as a proxy for China growth, is down 1.2 per cent to a six-year low of US$0.7539.

The 21st Century Business Herald, a Chinese daily newspaper, on Friday quoted multiple futures traders as saying they had received phone calls from the China Financial Futures Exchange instructing them not to short the market.

That is from Gabriel Wildau at the FT. China’s brokerages have pledged over $19 billion to help “stabilize” the market, not usually a good sign.

That said, flights into Greece for July-September seem to be down by up to fifty percent.

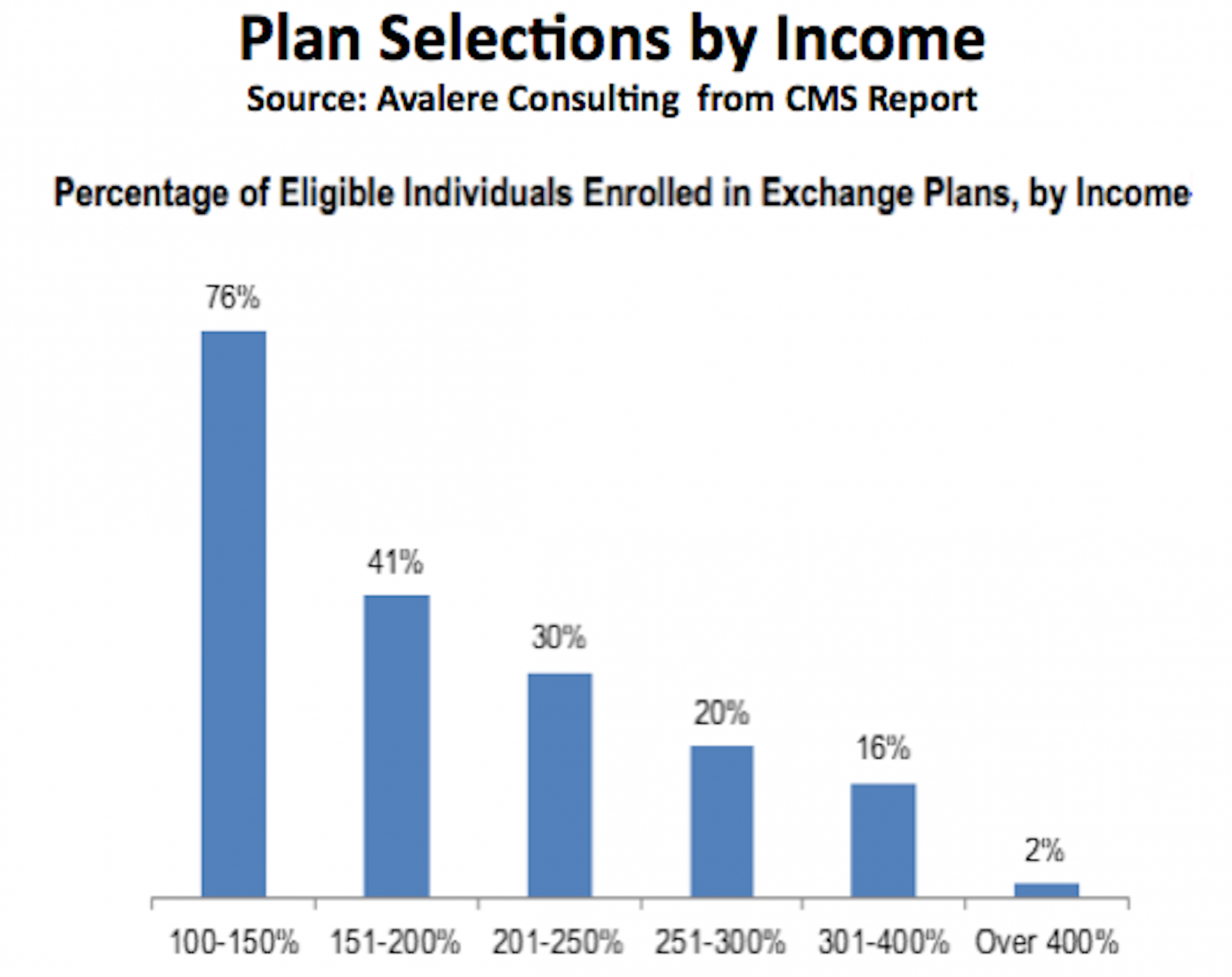

Why is Obamacare still unpopular?

After all of this and two complete open enrollments, only 40% of those who are eligible for Obamacare have signed up—far below the proportion of the market insurers have historically needed to assure a sustainable risk pool.

If this were a private enterprise enjoying these kinds of benefits [ namely legal coercion], and only sold its product to 40% of the market, its CEO would be fired.

Looking at this picture, only 20% of those eligible for Obamacare, who make between 251% and 300% of the poverty level, bought Obamacare. Why?

The Obama administration will in fact be increasing the subsidies it will pay to insurance companies.

Babbler birds babble non-babble

A study of the chestnut-crowned babbler bird from Australia revealed a method of communicating that has never before been observed in animals.

The bird combines sounds in different combinations to convey meaning.

The findings could help in the understanding of how language evolved in humans, researchers report in the online journal PLOS Biology.

Co-researcher Dr Andy Russell from the University of Exeter said: “It is the first evidence outside of a human that an animal can use the same meaningless sounds in different arrangements to generate new meaning.

“It’s a very basic form of word generation – I’d be amazed if other animals can’t do this too.”

A better player for a bad team?

Kevin Love, in his infinite wisdom, decided to test the free agent market. At least for a while, it seemed to raise the possibility that he wouldn’t return to the Cleveland Cavaliers with LeBron James.

Courtside critics of Love frequently cite the Coase theorem, especially when criticizing his play this last year for Cleveland. Arguably Love is a better player on a bad team than he is on a good team. He scores a lot, but only if he is the primary option on offense; you can see this by comparing his numbers on Minnesota, a poor team where he was a big star, with his numbers for Cleveland, where he was the number three scoring option. He needs a lot of touches to hone his shooting, which is a kind of scale effect. He also pulls in a lot of rebounds by neglecting his duties on team defense. For a poor team, maybe that is OK, because the team defense had serious holes anyway. For a good team it can wreck the entire plan.

This situation differs from the traditional O-Ring model (clever link there), in which the lesser talented workers hold the more talented worker back. Here the lesser talented workers allow a flawed, attention-demanding competitor to flourish.

It may sound negative to say a player is more valuable on a bad team, but that is a skill too. These individuals are perhaps no less virtuous or hard-working than those who are better on a good team. Michael Adams was better on bad teams (and he played on lots of them), but was hard-working and non-selfish and also widely admired, even though he was too short and weak to hold the line in a good defensive set-up.

There are analogues in business. Some managers may have special talents in bringing out the best in less talented workers. Or they may make better decisions when they get to be the real boss of just about everything. They may need a lot of unfettered experience to refine their skills, and perhaps they’re not so good at collaboration anyway.

Some politicians may be better at running chaotic countries; Nelson Mandela would have been wasted as Prime Minister of Iceland.

Some economists may be of more value in weak departments than in strong departments. Their generalist skills fill in a greater number of gaps, and perhaps they can bring out the best in weaker students, when better students would find their lack of specialization a bigger drawback.

What are other examples of this phenomenon?

Given that Kevin Love is indeed re-signing with Cleveland, does this mean the knock on him is wrong? Or is the equilibrium that the Cavaliers will become a worse team? Or maybe virtually all players are good bargains the year before the salary cap will go up a lot? Maybe Cleveland re-signed him…because they can? The rumored deal is for $110 million, tell Coase about that.

Wednesday assorted links

1. The mystery of the multiple job holder. And tomorrow morning, Bobby Bonilla will be $1.2 million richer.

2. Were the Xian terracotta warriors inspired by Greek art?

3. Claims about what moves the stock market.

4. Economic models of the Neolithic.

5. Defaulting on the IMF makes Grexit much harder to pull off.

6. County by county, red voter areas actually have slightly more stable families.

China and the high cost of hiring labor

…[recent developments] may well mark the beginning of an important longer-term shift in China’s labor market and policies: the State Council lowered employers’ required contributions to two social insurance programs, injury and maternity insurance, a move it said would save firms 27 billion renminbi a year (see the China Labour Bulletin for an English-language summary). Yes, I know this sounds boring and technical, so why is it important? Because it starts to address one of the biggest but least-known issues in China’s job market: the very high costs employers face to hire workers.

It is not a very well-known fact that China has some of the toughest labor regulations in the world, and some of the highest required contribution rates to social insurance programs. As a result, the “labor wedge”–the percentage of the total cost of an employee that comes from things other than wages–in China is around 45%, as high as in a number of European countries (this is according to an estimate by John Giles in a World Bank paper;…

This fact does not square with the widespread perception of China as a nation of sweatshops employing hordes of migrant workers, and indeed is a relatively recent development stemming from the 2008 Labor Contract Law. But China’s problem with these generous worker protections is ultimately the same one that many other developing countries have encountered: strong legal protections and generous insurance programs are so expensive that in practice they only become available to part of the workforce. Effectively China has two labor markets: one for urban white-collar jobs with all the legal protections, and one for blue-collar jobs held by rural migrant workers that generally lack the full set of benefits.

That is yet another neglected China story…

The view from Vilnius, part II

When Greece’s finance minister, Yanis Varoufakis, in an early round of negotiations in Brussels, complained that Greek pensions could not be cut any further, he was reminded bluntly by his colleague from Lithuania that pensioners there have survived on far less. Lithuania, according to the most recent figures issued by Eurostat, the European statistics agency, spends 472 euros, about $598, per capita on pensions, less than a third of the 1,625 euros spent by Greece. Bulgaria spends just 257 euros. This data refers to 2012 and Greek pensions have since been cut, but they still remain higher than those in Bulgaria, Lithuania, Latvia, Croatia and nearly all other states in eastern, central and southeastern Europe.

There is more from Andrew Higgins in the NYT here.

Tuesday assorted links

1. Has 3-D printing stagnated?

2. Claims about Russia. A speculative but important piece by Max Fisher. And Russian village prints its own currency.

4. Rare earths were never such a big problem to begin with.

The Anne Krueger report on Puerto Rico

You’ll find it here (PDF), co-authored with Ranjit Teja and Andrew Wolfe. Here is a bit of the introductory summary:

Structural reforms

Restoring growth requires restoring competitiveness. Key here is local and federal action to lower labor costs gradually and encourage employment (minimum wage, labor laws, and welfare reform), and to cut the very high cost of electricity and transportation (Jones Act). Local laws that raise input costs should be liberalized and obstacles to the ease of doing business removed. Public enterprise reform is also crucial.

Fiscal reform and public debt.

Probably the most startling finding in this report will be that the true fiscal deficit is much larger than assumed. Even a major fiscal effort leaves residual financing gaps in coming years, which can be bridged by debt restructuring (a voluntary exchange of existing bonds for new ones with a longer/lower debt service profile). Public enterprises too face financial challenges and are in discussions with their creditors. Despite legal complexities, all discussions with creditors should be coordinated.

Institutional credibility.

The legacy of weak budget execution and opaque data – our fiscal analysis entailed many iterations – must be overcome. Priorities include legislative approval of a multi-year fiscal adjustment plan, legislative rules on deficits, a fiscal oversight board, and more reliable and timely data.

If I were a Puerto Rican considering statehood…I know how I would vote.

For the pointer I thank Felix Salmon.

Is there economic hope for men?

Allison Schrager has a new piece on that topic in Playboy, and with a new (old) idea, here is one part:

Harvard economist Lawrence Katz thinks that when the economy shifts, those who lose out experience “retroactive unemployment” in pursuit of jobs that no longer exist; however, he anticipates a bright future for men in the new economy. As an expert in the ways technology affects the middle class, Katz predicts the rise of the “new artisan” as a substantial trend in middle-class employment.

His theory holds that technology will commoditize and cheapen products in all industries but that artisanal workers will offer a superior interpersonal experience coupled with unique goods and services, commanding premium prices in turn. Men, he notes, are especially well suited to such roles. “These kinds of jobs go back to colonial times,” Katz says. “Individuals brought their own ingenuity and creativity to provide small-scale, high-quality products. In the 19th century they were displaced by mass production, but technology is already bringing a resurgence of this type of work.”

…If Katz’s prediction about new artisans comes to pass, the ways men and women fit into the economy will come to complement each other. Their roles will change, in some ways becoming more traditional and in others less: Women may be likelier to spend their careers in nine-to-five corporate positions, enjoying the regular hours, benefits and predictable pay those jobs entail. Forty-nine percent of women already work in firms with more than 500 employees, compared with 43 percent of men, and their share of the corporate pie is growing. That certainty will empower men to take on less predictable but possibly higher-paying work in self-employment.

A world in which men strive to learn new skills and take on riskier, entrepreneurial household roles may even prove more fulfilling than office work—but this requires changing our definition of a “good job.” Expecting men to be better-educated, office-work-oriented breadwinners is an outmoded idea. The artisan of the future will still be skilled and possess just as much potential to provide for his family. The technological revolution is yet another turn in the cycle of economic progress, and workers of both genders must learn to adapt. The end of men is not nigh; the end of our dated notion of work, however, is.

I believe the link would count as “safe for work,” but do note you may get a Playboy pop-up as I did, and there are sidebar ads, no full nudity but still this is Playboy beware if need be.

Not in Greece, but news nonetheless

The Chinese stock market is tanking again, down more than seven percent today, seventeen percent or so over the last three days. Read David Keohane.

Puerto Rico isn’t going to pay up, and they announced this through the NYT.

Utrecht is going to experiment with a basic income scheme.

Central Russian officials crack down on yoga to limit the spread of occultism.

Would there (will there?) be contagion from Grexit?

If you put Greek total debt in perspective, it’s smaller than that of many other EU nations, including Portugal. And that is as a percentage of gdp. Furthermore most of the remaining Greek debt is held by public sector institutions.

The difference of course is that Greece is being run by The Not Very Serious People. Portugal is often described as the next weakest link in the eurozone, but Portuguese politics are not nearly so…vivid. The amount of fiscal consolidation they have done is more or less accepted by the public. That makes Portugal more likely to survive, and it also makes the EU more willing to bail out Portugal, and extend any bailout if needed.

The performance of Syriza won’t encourage European voters to take chances on other less tested, left-wing parties, and that also militates against contagion.

(In the meantime, I don’t understand why Anglo-American left-wing intellectuals have been egging on the Syriza performance. Even if you think the current mess is mostly Germany’s fault in normative terms, the marginal product of the Syriza government still has been catastrophically negative. It wasn’t long ago that Greek banks were raising fresh equity and were said to have recovered. Here is Krugman’s defense, I find Anders Aslund more persuasive, furthermore Grexit would mean more austerity not less.)

For contagion, here are a few possible problems:

1. If Greece does reasonably well after Grexit, many others will ask why should they not follow suit and that could turn into a self-fulfilling prophecy. I’ll bet against that, but it’s worth mentioning. It also would take a while to develop.

2. As Greece exists, the ECB has to express a strength of commitment to the other debt-ridden nations. Delivering the right message is tricky here, because for legal and public opinion reasons the ECB cannot make the kind of unconditional commitments the Fed can. So markets might become unhappy with the decline in creative ambiguity at the ECB. I believe the ECB can finesse this one — in essence the message “we’ll help any EU government which is more responsible than Syriza” is fairly credible and in fact is already being signaled by the Eurogroup. So I’ll bet against this problem too, but still it could happen.

3. If only for geopolitical and also humanitarian reasons, the EU cannot wash its hands of Greece, even if Greece leaves the EU. But deciding how to deal with Greece might bring considerable disagreements among the remaining eurozone nations, as might the attempt to spell out exit procedures. Festering, emotional issues are not good for dysfunctional political unions, and a lot of the “hold the line” solidarity might melt away with Grexit.

4. There might be a very slow form of contagion as the reversibility of the currency union becomes better and better known and people start seeing it as little more than a currency board arrangement. As with #3, that could become an ongoing problem, still it doesn’t quite seem dramatic enough to produce rapid contagion.

Here is my previous post on the topic. Robin Wigglesworth surveys a variety of differing views on contagion and other short-run effects. I wrote this post last night, so if I am wrong it might already be evident by now.

Scandinavian Unexceptionalism

That is the new IEA book from Nima Sanandaji, freely available here (pdf), introduction by Tom G. Palmer. Here is one short bit:

The descendants of Scandinavian migrants in the US combine the high living standards of the US with the high levels of equality of Scandinavian countries. Median incomes of Scandinavian descendants are 20 per cent higher than average US incomes. It is true that poverty rates in Scandinavian countries are lower than in the US. However, the poverty rate among descendants of Nordic immigrants in the US today is half the average poverty rate of Americans – this has been a consistent finding for decades. In fact, Scandinavian Americans have lower poverty rates than Scandinavian citizens who have not emigrated. This suggests that pre-existing cultural norms are responsible for the low levels of poverty among Scandinavians rather than Nordic welfare states.

The book has many other points of interest.