Fauci Didn’t Test

I am not a Fauci hater but I think this criticism of Facui from epidemiologist and oncologist Vinay Prasad hits the mark:

Lockdown was specifically advocated for by Anthony Fauci (‘15 days to stop the spread’/ ‘hunker down’/ ‘shelter in place’), and Fauci would go on to make hundreds of other specific policy recommendations. Although he initially rejected it, by April 2020, he recommended community cloth masking to slow the coronavirus (an intervention for which we now have randomized data showing it doesn’t work).

Fauci opposed Ron DeSantis in numerous TV interviews in spring 2020 when DeSantis reopened schools. He called school reopening reckless— though it was widely embraced in western Europe at the time, and now clearly the correct policy choice.

Fauci supported vaccine mandates and border closure. He repeated the false statement that 6ft of social distancing had an empirical basis. Many in the media and medicine think criticizing him is unfair— he did the best he could with what he knew at the time—but it is fair to criticize a scientist who presented his views as facts when they were at best speculation. And, moreover, there is one criticism that no one can deny:

Although he was director of the NIAID, and although he controlled a 5 billion dollar infectious disease research budget, he chose to launch, fund and conduct precisely ZERO randomized trials of non-pharmacologic interventions.

Hat tip: MD.

The Marginal Revolution Theory of Innovation

A FDA panel voted against approving MDMA (ecstasy) for post-traumatic stress disorder. Putting aside the specifics of the case, I was vexed by this statement on innovation from one of the experts voting no:

“I absolutely agree that we need new and better treatments for PTSD,” said Paul Holtzheimer, deputy director for research at the National Center for PTSD, a panelist who voted no on the question of whether the benefits of MDMA-therapy outweighed the risks.

“However, I also note that premature introduction of a treatment can actually stifle development, stifle implementation and lead to premature adoption of treatments that are either not completely known to be safe, not fully effective or not being used at their optimal efficacy,” he added.

A textbook example of making the perfect the enemy of the good. But the problem is even worse. Holtzheimer seems to think that treatments spring from the lab perfectly formed like Athena springing from the brow of Zeus. Indeed, Holtzheimer suggests that treatments should be kept in the lab until they are perfect. News flash: there are no perfect treatments–no drug or device in use today is completely known to be safe, fully effective, and used at its optimal efficacy. Not one. If we follow Holtzheimer’s counsel, we will never approve a new drug.

Innovation is a dynamic process; success rarely comes on the first attempt. The key to innovation is continuous refinement and improvement. A firm with sales gains greater resources to invest in further research and development. Additionally, they benefit from customer feedback, which provides valuable insights for enhancing their products and processes. Learning by doing requires doing. But if imperfect treatments are never approved, scientists often don’t return to the lab to refine and improve them. Instead, the project dies. Thus, when considering innovation today, it’s essential to think about not only the current state of technology but also about the entire trajectory of development. A treatment that’s marginally better today may be much better tomorrow.

Small steps toward a much better world.

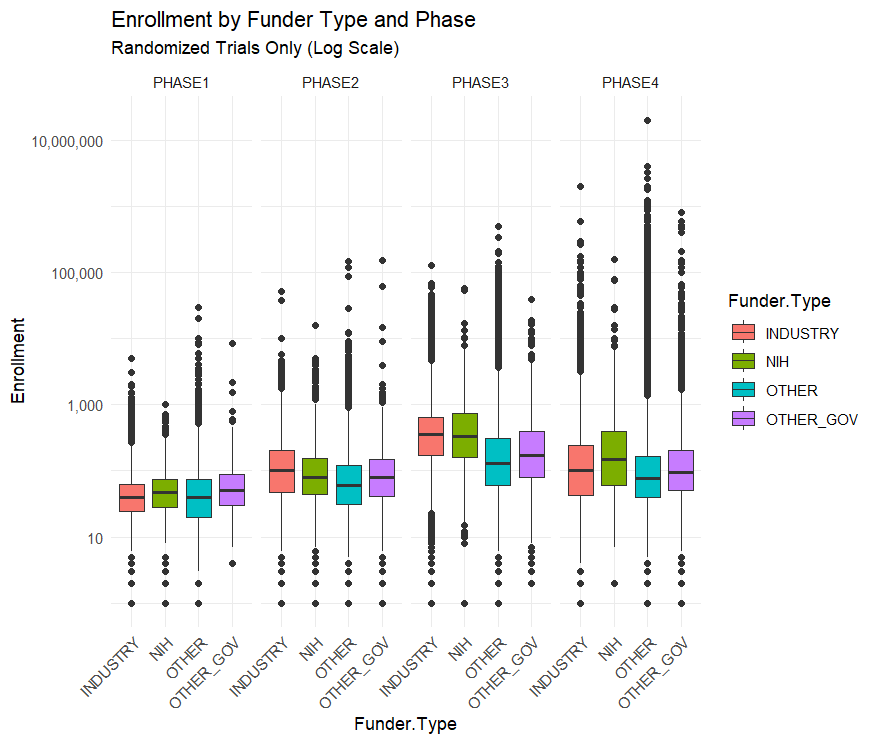

The NIH Doesn’t Fund Small Crappy Trials

A nice catch by Max at Maximum Progress:

[A common critique] is that the NIH funds too many “small crappy trials.” That quote is from a FDA higher up, but the story has been repeated by many others…I downloaded all of the clinical trial data from ClinicalTrials.gov to find out….The median NIH funded trial has 48 participants while the median industry funded trial has 67. The average NIH funded trial has 288 participants while the average industry trial has 335 and the average “Other” funded trial (mostly universities and the associated hospitals) has 923 participants.

By median or by average NIH trials are the smallest out of all the funders. This seems to confirm the “small crappy trials” narrative

…This narrative is reversed, however, when you split up the trials by phase.

Across all trials NIH funded ones are the smallest, but within each phase NIH trials are the largest or second largest. Their overall small enrollment average is just due to the fact that they fund more Phase I trials than Phase III. But NIH Phase I trials have a bigger sample size than industry funded trials on average.

This is an example of Simpson’s Paradox in the wild!

Arguing that the NIH should stop funding unusually small trials is easy but arguing that they should shift from funding the Phase I trials closest to basic research towards later stage trials is less clear.

The NIH’s clinical trial strategy is certainly not perfect and improving it is valuable. But a systematic bias towards “small crappy trials” doesn’t really seem like it’s an important problem facing the NIH.

The Danish Mortgage System Avoids Lock-In

Tyler and I have been promoting the Danish mortgage system for years. Recall that in the Danish system each mortgage is backed by a matching bond. As a consequence, mortgage holders have two ways to pay a mortgage: 1) hold the mortgage and pay the monthly payments or 2) buy the matching bond and, in effect, extinguish the mortgage. The latter option is valuable because when interest rates rise, the price of mortgages fall. As I wrote earlier:

Thus, if a Danish borrower takes out a 500k mortgage at 3% interest and then rates rise to 6%, the value of that mortgage falls to $358k and the borrower could go to the market, buy their own mortgage, deliver it to the bank, and, in this way, extinguish the loan. Since the value of homes also falls as interest rates rise this is also a neat bit of insurance. Remarkable!

James Rodriguez writing at Business Insider points out another advantage of the Danish system, it avoids lock in:

When mortgage rates shoot up, as they did over the past two years, many would-be sellers decide they don’t want to move after all. Sure, a new home could be nice, but trading up would mean parting ways with a cheap mortgage rate. What may have been a welcome change suddenly sounds like a painful, expensive divorce. So they sit tight. A gummed-up housing market is good for nobody: First-time buyers can’t find enough homes for sale, and wannabe sellers remain trapped in places that are either too big or too small. This is called the lock-in effect — and it could linger for decades.

… One estimate (here, AT) suggests the lock-in effect prevented more than 1 million people from selling their homes in the span of just a year and a half, a steep toll considering about 5 million homes exchange hands in a typical year. I used to think of these golden handcuffs as an inevitable side effect of the magical 30-year fixed mortgage. But it doesn’t have to be this way. The answer to our problems may lie thousands of miles away … in Denmark.

…Danish sellers are able to earn a profit when they trade in their low mortgage rates for more-expensive ones, making it easier to move even when rates rise.

TaskRabbit for AI Hires

Many people are interested in knowing, which AI is the closest to achieving AGI? That’s an important question for philosophers and computer scientists but more and more I am seeing firms arise to answer a different question, Which AI should I hire?

EquiStamp, for example, rates dozens of AIs based on multiple evaluations, including custom evaluations tailored to specific business tasks. For instance, one firm may want to hire an AI to handle customer queries, another to sort packages, another to summarize internal technical documents. The best AI for each task might differ from the AI that scores highest on general reasoning power. In addition, businesses care not just about performance but also about speed and cost. No reason to hire AI-Einstein to sort the mail. AIs are also continually being re-trained so their performance can fluctuate. Businesses, therefore, may want to continually test their AIs and quickly hire and fire AIs as needed.

In short, a spot-market for hiring AIs is developing.

Kal Mansur

My first commissioned art work. A piece by artist Kal Mansur who I met in high school. It’s not a painting but an embedded 3D sculpture so the work changes in different lights and angles. You will perhaps note a homage to Frank Lloyd Wright.

Caplan and Cowen

A hilarious but also informative rapid-style debate between Bryan Caplan and Tyler on YIMBY and NIMBY.

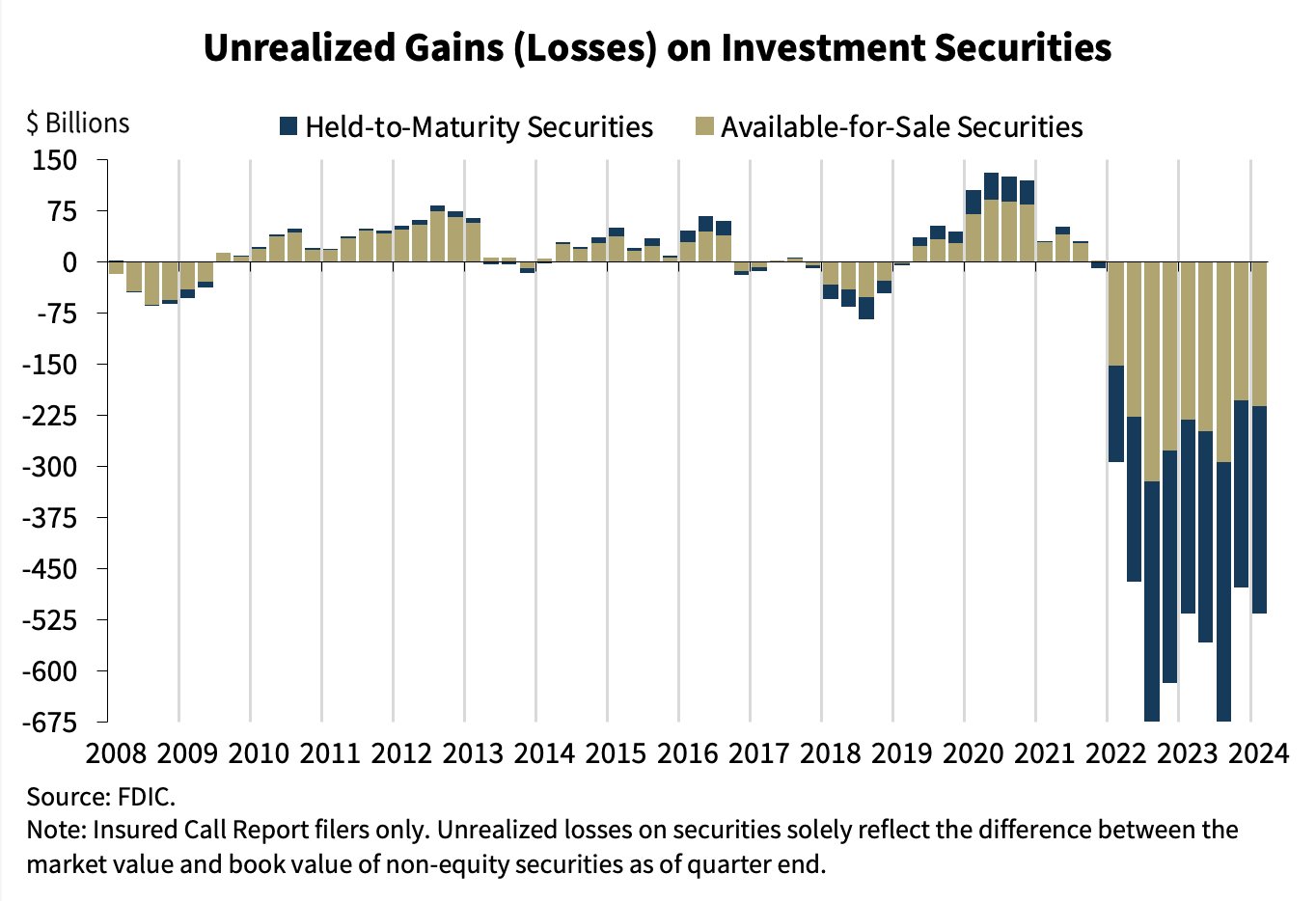

Bailouts Forever

When interest rates rise, the price of long-term assets falls. Consequently, when the Fed began raising interest rates in 2022, the value of bonds and mortgages dropped, causing significant accounting losses for banks heavily invested in these assets. Silicon Valley Bank went bust, for example, because depositors fled upon realizing it was holding lots of Treasury bonds.

Interest rates remain high and many banks have large unrealized losses on their books. According to the latest FDIC data (see below) unrealized losses currently total $516.5 billion, far exceeding levels seen during the 2008-2009 financial crisis. Price risk is not the same as default risk and if the banks can hold onto their assets until maturity then they will be solvent. The real danger, as with SVB, is if unrealized losses are combined with a deposit run. So far that doesn’t seem to be happening but it’s well within the realm of possibility.

In other news, Hypertext has an issue devoted to Anat Admati and Martin Hellwig’s The Banker’s New Clothes. Admati and Hellwig write:

The 2010 Dodd-Frank Act in the United States promised the end of bank bailouts and “too-big-to-fail” institutions. The European Union’s 2014 legislation for dealing with banks likely to fail was claimed to provide “a framework” to “deal with banks that experience financial difficulties without either using taxpayer money or endangering financial stability.” In November 2014, Mark Carney, at the time the governor of the Bank of England and chair of the Financial Stability Board (FSB), a body of financial regulators from around the world, announced triumphantly that an agreement about new rules for the thirty largest and most complex, “globally systemic” financial institutions would prevent bailouts in the future. Many people in politics and the media believed these claims.

Two From the Tabarrok Brothers

Maxwell Tabarrok offers an excellent review of an important paper.

Taxation and Innovation in the 20th Century is a 2018 paper by Ufuk Akcigit, John Grigsby, Tom Nicholas, and Stefanie Stantcheva that provides some answers. They collect and clean new datasets on patenting, corporate and individual incomes, and state-level tax rates that extend back to the early 20th century. The headline result: taxes are a huge drag on innovation. A one percent increase in the marginal tax rate for 90th percentile income earners decreases the number of patents and inventors by 2%. The corporate tax rate is even more important, with a one percent increase causing 2.8% fewer patents and 2.3% fewer inventors.

Especially useful is Max’s back of the envelope calculation putting this result in the context of other methods to increases innovation.

Read the whole thing.

For something completely different, Connor Tabarrok offers an update on Charlotte the Stingray:

A “miracle pregnancy” picked up by national news brought huge business to a small-town aquarium, but months after the famous stingray was due, there are still no pups. Are we being scammed by a fish?

I particularly liked this line:

Taking all of this into account, my stance is that even if they got it on, it’s unlikely that this shark will have to dish out any child support to Charlotte’s pups.

Read the whole thing.

Are MR readers more interested in tax policy or virgin birth stingrays? We shall see.

Money for Blood and Short Term Jobs

The excellent Tim Taylor on a new paper on plasma donation:

John M Dooley and Emily A Gallagher take a different approach in “Blood Money: Selling Plasma to Avoid High-Interest Loans” (Review of Economic Studies, forthcoming, published online May2, 2024; SSRN working paper version here). They are investigating how the opening of a blood plasma center in an area affects the finances of low-income individuals. As background, they write:

“Plasma, a component of blood, is a key ingredient in medications that treat millions of people for immune disorders and other illnesses. At over $26 billion in annual value in 2021, plasma represents the largest market for human materials. The U.S. provides 70% of the global plasma supply, putting blood products consistently in the country’s top ten export categories. The U.S. produces this level of plasma because, unlike most other countries, the U.S. allows pharmaceutical corporations to compensate donors – typically about $50 per donation for new donors, with rates reaching $200 per donation during severe shortages. The U.S. also permits comparatively high donation frequencies: up to twice per week (or 104 times per year)…”

Not too surprisingly, plasma donors tend to be young and poor and they use plasma donation to substitute away from non-bank credit like payday loans.

I am struck by Tim’s thoughts on how this connects with labor markets and regulation:

…I find myself thinking about the financial stresses that many Americans face. Being paid a few hundred dollars for a series of plasma donations isn’t an ideal answer. Neither is taking out a high-interest short-term loan; indeed, taking out a loan at all may be a poor idea if you aren’t expecting to have the income to pay it back. In the modern US economy, hiring someone for even a short-term job involves human resources departments, paperwork, personal identification, bookkeeping, and tax records. These rules have their reasons, but the result is that finding a short-term job that pays for a few days work isn’t simple, even if though most urban areas have a semi-underground network of such jobs.

Roger Miller’s classic 1964 song, “King of the Road,” tells us that “two hours of pushin’ broom/ Buys an eight by twelve four-bit room.” Even after allowing for a certain romancing of the life of a hobo in that song, the notion that a low-income person can walk out the door and find an two-hour job that pays enough to solve immediate cash-flow problems–other than donating plasma–seems nearly impossible in the modern economy.

Monaco on the Marin Headlands

The Dalmation Coast in Croatia, the Amalfi Coast in Italy and Monaco’s coast on the Mediterranean Sea are often found on lists of the most beautiful coastlines in the world. Here are some pictures. Hard not to agree. The fourth picture is of the Marin coastline near San Francisco. It’s also beautiful but is it obviously more beautiful than the other coastlines? Personally, I don’t think so. But one thing is different. Far fewer people are enjoying the Marin coast. Why? Because fewer people live there. Can something be beautiful if there is no one to see it?

There is something to be said for protecting natural wilderness but must we do so on some of the most valuable land in the world?

I agree with Market Urbanism, “Quite simply, we must build Monaco on the Marin Headlands.”

Hat tip to Bryan Caplan who makes the point about beauty in his excellent, Build, Baby, Build.

Croatia

Amalfi

Monaco

Marin:

Deadly Precaution

MSNBC asked me to put together my thoughts on the FDA and sunscreen. I think the piece came out very well. Here are some key grafs:

…In the European Union, sunscreens are regulated as cosmetics, which means greater flexibility in approving active ingredients. In the U.S., sunscreens are regulated as drugs, which means getting new ingredients approved is an expensive and time-consuming process. Because they’re treated as cosmetics, European-made sunscreens can draw on a wider variety of ingredients that protect better and are also less oily, less chalky and last longer. Does the FDA’s lengthier and more demanding approval process mean U.S. sunscreens are safer than their European counterparts? Not at all. In fact, American sunscreens may be less safe.

Sunscreens protect by blocking ultraviolet rays from penetrating the skin. Ultraviolet B (UVB) rays, with their shorter wavelength, primarily affect the outer skin layer and are the main cause of sunburn. In contrast, ultraviolet A (UVA) rays have a longer wavelength, penetrate more deeply into the skin and contribute to wrinkling, aging and the development of melanoma, the deadliest form of skin cancer. In many ways, UVA rays are more dangerous than UVB rays because they are more insidious. UVB rays hit when the sun is bright, and because they burn they come with a natural warning. UVA rays, though, can pass through clouds and cause skin cancer without generating obvious skin damage.

The problem is that American sunscreens work better against UVB rays than against the more dangerous UVA rays. That is, they’re better at preventing sunburn than skin cancer. In fact, many U.S. sunscreens would fail European standards for UVA protection. Precisely because European sunscreens can draw on more ingredients, they can protect better against UVA rays. Thus, instead of being safer, U.S. sunscreens may be riskier.

Most op-eds on the sunscreen issue stop there but I like to put sunscreen delay into a larger context:

Dangerous precaution should be a familiar story. During the Covid pandemic, Europe approved rapid-antigen tests much more quickly than the U.S. did. As a result, the U.S. floundered for months while infected people unknowingly spread disease. By one careful estimate, over 100,000 lives could have been saved had rapid tests been available in the U.S. sooner.

I also discuss cough medicine in the op-ed and, of course, I propose a solution:

If a medical drug or device has been approved by another developed country, a country that the World Health Organization recognizes as a stringent regulatory authority, then it ought to be fast-tracked for approval in the U.S…Americans traveling in Europe do not hesitate to use European sunscreens, rapid tests or cough medicine, because they know the European Medicines Agency is a careful regulator, at least on par with the FDA. But if Americans in Europe don’t hesitate to use European-approved pharmaceuticals, then why are these same pharmaceuticals banned for Americans in America?

Peer approval is working in other regulatory fields. A German driver’s license, for example, is recognized as legitimate — i.e., there’s no need to take another driving test — in most U.S. states and vice versa. And the FDA does recognize some peers. When it comes to food regulation, for example, the FDA recognizes the Canadian Food Inspection Agency as a peer. Peer approval means that food imports from and exports to Canada can be sped through regulatory paperwork, bringing benefits to both Canadians and Americans.

In short, the FDA’s overly cautious approach on sunscreens is a lesson in how precaution can be dangerous. By adopting a peer-approval system, we can prevent deadly delays and provide Americans with better sunscreens, effective rapid tests and superior cold medicines. This approach, supported by both sides of the political aisle, can modernize our regulations and ensure that Americans have timely access to the best health products. It’s time to move forward and turn caution into action for the sake of public health and for less risky time in the sun.

Hedging Star Wars and Close Encounters

An old story but new to me. Lucas and Spielberg swapped 2.5% net points on Star Wars and Close Encounters. Pretty smart bet for both of them.

Spielberg tells the story:

George came back from Star Wars a nervous wreck. He didn’t feel Star Wars came up to the vision he initially had. He felt he had just made this little kids’ movie. He came to Mobile, Alabama where I was shooting Close Encounters on this humongous set and hung out with me for a couple of days.

He said, ‘Oh my God, your movie is going to be so much more successful than Star Wars. This is gonna be the biggest hit of all time.’ He said, ‘You want to trade some points? I’ll tell you what, I’ll give you two and a half per cent of Star Wars if you give me two and a half per cent of Close Encounters.’

I said, Sure, I’ll gamble with that, great. And I think I came out on top of that bet. I did a lot better than George!

Both movies were wildly profitable. Close Encounters made so much money and rescued Columbia from bankruptcy. It was the most money I ever made on a movie before, but Close Encounters was a meagre success story. Star Wars was a phenomenon and I was the happy beneficiary of a couple of net points from that movie which I am still seeing money on today!

The Sea Change on Crypto-Regulation

In the last few weeks there has been a sea change in crypto regulation:

1. Bitcoin spot ETFs were approved–reluctantly, after a 3-judge Federal Appeals court ruled unanimously that the SEC had acted arbitrarily and capriciously–but nevertheless opening Bitcoin holdings to institutional investors. Case in point, The State of Wisconsin bought Bitcoin ETFs for its pension fund.

2. In a very unusual move, SAB 121, was overturned by the House and then, even more surprisingly, overturned by the Senate including the votes of many Democrats. < href=”https://www.sec.gov/oca/staff-accounting-bulletin-121″>SAB 121 is an SEC staff accounting bulletin (not law but guidance) that said to banks if you hold crypto for your customers, i.e. a custody service, you must account for it on your balance sheet. This guidance does not apply to custody of any other asset. Essentially, SAB 121 made it prohibitive for banks to offer custody services for crypto because that service would then impact all kinds of risk and asset regulations on the bank. Aside from singling out crypto, the SEC is not a regulator of banks so this seemed like a regulatory overreach.

President Biden said he will veto but that is no longer certain. It wasn’t just crypto lobbying against SAB 121 but traditional banks. The banks point to the approval of Bitcoin ETFs saying, quite logically, why can’t we custody these ETFs the way we do every other ETF? Senate Majority leader Chuck Schumer, D-N.Y., sometimes called Wall Street’s man in Washington, voted in favor of nullifying SAB 121. Schumer can read the room.

3. The House voted to ban the Fed from establishing a Central Bank Digital Currency (CBDC).

4. The House approved a wide-ranging bill to (finally!) establish regulations for digital assets markets. The vote was 279-136 in favor with many Democrats crossing party lines to support it.

5. After saying nothing for months, usually a bad sign, the SEC approved Ethereum spot ETFs. On the surface, this might have seemed logically inevitable given the approval of Bitcoin spot ETFs but many people thought the SEC would do everything it could to find daylight between Bitcoin and ETH. Instead, it tacitly acknowledged that ETH is a commodity and not a security.

Why is this happening? I see three main factors at play. First, crypto is becoming integrated with traditional finance. As the big banks get involved, the politics around crypto are shifting. Second, crypto is becoming normalized. Ironically, the prosecution of Sam Bankman-Fried, Changpeng Zhao and manipulators like Avraham Eisenberg may have convinced some U.S. regulators that crypto doesn’t have to be destroyed, it can be tamed. Nakamoto might not be pleased but realistically this was the only option to move forward. Eventually, everyone wants to pay their mortgage. Third, Trump’s strong endorsement of crypto has alarmed the Biden administration. Most political issues are firmly divided along party lines, but crypto remains an open issue. With millions of crypto owners in the United States, a significant number are highly motivated to vote their wallets. Biden doesn’t want to give the crypto issue to Trump.

None of this means we are entering crypto Nirvana but as far as regulation is concerned a lot has changed in just a matter of weeks.

Full Disclosure: I am an advisor to several firms in the crypto space including MultiversX, Bluechip and 0L.

The Left on FDA Peer Approval

Robert Kuttner discovered an excellent treatment for colds while vacationing in France and is rightly outraged that it’s not available in the United States:

Toward the end of our stay, my wife and I both got bad coughs (happily, not COVID). We went to our wonderful local pharmacist in search of something like Mucinex or Robitussin, which are not great but better than nothing.

“We have something much better,” said he. And he did. It’s called ambroxol. It works on an entirely different chemical principle, to thin sputum, facilitate productive coughing, and also operates as a pain reliever and gentle decongestant with no rebound effect.

We experienced it as a kind of miracle drug for coughs and colds. A box cost eight euros.

Ambroxol is available nearly everywhere in the world as a generic. It has been in wide use since 1979.

But not in the U.S.

…You can’t get ambroxol in the U.S. because of the failure of the Food and Drug Administration to grant reciprocal recognition to generic medications approved by its European counterpart, the European Medicines Agency, when they have long been proven safe and effective. To get FDA approval for the sale of ambroxol in the U.S., a drug company would need to sponsor extensive and costly clinical trials. Since it is a generic, as cheap as aspirin, no drug company would bother.

…I’ve petitioned the FDA, asking them to create a fast-track procedure, whereby generic drugs approved in Europe, and well established as safe and effective, could get reciprocal approval in the U.S.

This would produce approval of ambroxol as over-the-counter medication for coughs and colds without unnecessary new clinical trials. And should ambroxol turn out to have real benefits for Parkinson’s as well, it would already be well established in the U.S. as an inexpensive generic.

Influenced by my work on FDA reciprocity aka peer approval, Ted Cruz introduced a bill, the Result Act to fast-track approval in the United States for drugs and devices already approved in other developed countries. Similarly, AOC has noted that the FDA is far behind the world in approving advanced sunscreens. Perhaps there is an opportunity here for bipartisan support.

Hat tip: the excellent Scott Lincicome.