Category: Economics

The distributional incidence of QE and lower interest rates

A new McKinsey study has crossed my desk, “QE and ultra-low interest rates: Distributional effects and risks.” It offers a few estimates:

1. As a result of QE, governments in the US, UK, and Eurozone have benefited by about $1.6 trillion in lower debt service costs and profits remitted from central banks.

2. Households in those same countries have lost about $630 billion in reduced interest income.

3. Non-financial corporations have gained about $710 billion through lower debt service costs.

I would urge extreme caution in interpreting these or indeed any such results, as the nature of the no-QE-weaker-AD alternative scenario is hard to spell out and in any case would impose losses of its own. “Never reason from a pecuniary externality change” a wag once told me. Still, you can use those numbers as one example of a very rough “apply ceteris paribus assumptions to a macro problem” estimate.

One interesting takeaway from this report is that European life insurance companies may be in persistent financial trouble. Many life insurance policies are written for 40 or 50 years but the companies cannot find assets to match those durations. As the bonds they hold mature, they cannot easily reinvest in safe assets with yields comparable to what they are guaranteeing their policyholders. For instance some German life insurers are guaranteeing a return of 1.75 percent, but German ten year Bunds were yielding only about 1.54 percent (the report is from November). The insurance companies will either steadily lose money or be forced to seek out riskier investments, which is also to some extent prohibited by law and regulation. Here is one relevant Moody’s report, which explains why German life insurance companies are especially vulnerable. There are related readings here.

*F.A. Hayek and the Modern Economy*

That is a new volume edited by Sandra J. Peart and David M. Levy.

More than just the usual blah blah blah about Hayek, this book is full of original material. The book’s home page, with table of contents, is here.

And here is our recent MRUniversity class on Friedrich A. Hayek, and his Individualism and Economic Order.

Interview with John Cochrane

There are many interesting bits from the interview, sometimes polemic bits too, here is one excerpt:

EF: What do you think are the biggest barriers to our own economic recovery?

Cochrane: I think we’ve left the point that we can blame generic “demand” deficiencies, after all these years of stagnation. The idea that everything is fundamentally fine with the U.S. economy, except that negative 2 percent real interest rates on short-term Treasuries are choking the supply of credit, seems pretty farfetched to me. This is starting to look like “supply”: a permanent reduction in output and, more troubling, in our long-run growth rate.

This part reminds me of some ideas in my own Risk and Business Cycles:

There is a good macroeconomic story. In a business cycle peak, when your job and business are doing well, you’re willing to take on more risk. You know the returns aren’t going to be great, but where else are you going to invest? And in the bottom of a recession, people recognize that it’s a great buying opportunity, but they can’t afford to take risk.

Another view is that time-varying risk premiums come instead from frictions in the financial system. Many assets are held indirectly. You might like your pension fund to buy more stocks, but they’re worried about their own internal things, or leverage, so they don’t invest more.

A third story is the behavioral idea that people misperceive risk and become over- and under-optimistic. So those are the broad range of stories used to explain the huge time-varying risk premium, but they’re not worked out as solid and well-tested theories yet.

The implications are big. For macroeconomics, the fact of time-varying risk premiums has to change how we think about the fundamental nature of recessions. Time-varying risk premiums say business cycles are about changes in people’s ability and willingness to bear risk. Yet all of macroeconomics still talks about the level of interest rates, not credit spreads, and about the willingness to substitute consumption over time as opposed to the willingness to bear risk. I don’t mean to criticize macro models. Time-varying risk premiums are just technically hard to model. People didn’t really see the need until the financial crisis slapped them in the face.

I’ve long believed the risk premium is the underexplored variable in macroeconomics and finally this is being rectified.

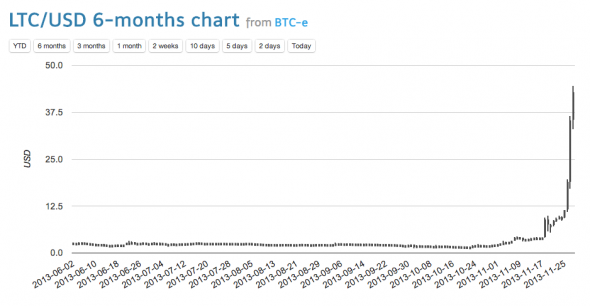

A short disquisition on the value of Litecoin

That is from Izabella Kaminska. Here is Wikipedia on Litecoin.

Uber-Economist

Uber is hiring economists. Looks like an interesting job:

Urban transportation has looked the same for a long time – a really long time – thanks in large part to regulatory regimes that don’t encourage innovation. We think it’s time for change. We’re a tech company sure, and we’re working in the transportation space, but at the end of the day we’re disrupting very old business models. Our Public Policy team prefers winning by being right over some of the darker lobbying arts, and so we’re looking for a Policy Economist to tease smart answers to hard questions out of big data. How do the old transportation business models impact driver income? What effect if any is Uber having on the housing market or drunk driving or public transit? To what extent are the different policy regimes in New York City and Taipei responsible for different transportation outcomes? Just a few of the questions we want you to dig on.

On-line education at the AEA meetings in Philadelphia

I can recommend to you all the session Economics Education in the Digital Age, scheduled for Saturday, January 4, at 10:15 a.m.

Nancy Rose is chairing the proceedings and presented papers will be by Caroline Hoxby, Banerjee and Duflo, and Acemoglu, Laibson, and List, as well as by Alex and myself. They are all very interesting papers, as you would expect from these economists.

How and why Bitcoin will plummet in price

My post from yesterday was perhaps not specific enough, so let me outline one possible scenario in which the value of Bitcoin (and other cryptocurrencies) would fall apart. For purposes of argument, let’s say that a year from now Bitcoin is priced at $500. Then you want some Bitcoin, let’s say to buy some drugs. And you find someone willing to sell you Bitcoin for about $500.

But then the QuitCoin company comes along, with its algorithm, offering to sell you QuitCoin for $400. Will you ever accept such an offer? Well, QuitCoin is “cheaper,” but of course it may buy you less on the other side of the transaction as well. The QuitCoin merchants realize this, and so they have built deflationary pressures into the algorithm, so you expect QuitCoin to rise in value over time, enough to make you want to hold it. So you buy some newly minted QuitCoin for $400, and its price springs up pretty quickly, at which point you buy the drugs with it. (Note that the cryptocurrency creators will, for reasons of profit maximization, exempt themselves from upfront mining costs and thus reap initial seigniorage, which will be some fraction of the total new value they create, and make a market by sharing some of that seigniorage with early adopters.)

Let’s say it costs the QuitCoin company $50 in per unit marketing costs for each arbitrage of this nature. (Alternatively you can think of that sum as representing the natural monopoly reserve currency advantage of Bitcoin.) In that case both the company and the buyers of QuitCoin are better off at the initial transfer price of $400 and people will prefer that new medium. Over time the price of Bitcoin will have to fall to about $450 in response to competition.

But of course the story doesn’t end there. Along comes SpitCoin, offering to sell you some payment media for $300. Rat-FacedGitCoin offers you a deal for $200. ZitCoin is cheaper yet. And so on.

Once the market becomes contestable, it seems the price of the dominant cryptocurrency is set at about $50, or the marketing costs faced by its potential competitors. And so are the available rents on the supply-side exhausted.

There is thus a new theorem: the value of WitCoin should, in equilibrium, be equal to the marketing costs of its potential competitors.

This theorem will hold even if you are very optimistic about market demand and think that grannies will get in on it. In fact the larger the network of demanders, the lower the marginal marketing cost may be — a bit like cellphones — and that means even lower valuations for the dominant cryptocurrency.

(It is an interesting question what fixed, marginal, and average cost look like here. Arguably market participants will not accept any cryptocurrency which is not ultimately and credibly fixed in supply, so for a given cryptocurrency the marginal cost of marketing more at some point becomes infinite. Marginal cost of supply for the market as a whole is perhaps the (mostly) fixed cost of setting up a new cryptocurrency-generating firm, which issues blocks of cryptocurrency, and that we can think of as roughly constant as the total supply of cryptocurrency expands through further entry. In any case this issue deserves further consideration.)

Note that the more “optimistic” you are about Bitcoin, presumably you should also be more optimistic about its future competitors too. Which means the theorem will kick in and you should be a bear on Bitcoin price. Arguably it’s the bears on the general workability of cryptocurrencies who should be bullish on Bitcoin price because a) we know Bitcoin already exists, and b) we would have to consider that existence an unexpected and unreplicable outlier of some sort. Yet the usual demon of mood affiliation denies us such a consistency of reasoning, and the cryptocurrency bulls are often also bulls on Bitcoin price, as too many of us prefer a consistency of mood!

In theory

Now, theoretically, you might believe that the current price of Bitcoin already reflects exactly those marketing costs of potential competitors and thus the current equilibrium is stable or semi-stable. Maybe so, but I doubt that. The current value of outstanding Bitcoin is about $20 billion or so, and it doesn’t seem it cost nearly that much to launch the idea. And now that we know cryptocurrencies can in some way “work,” it seems marketing a competitor might be easier yet. (You will note that by its nature, there are some Bitcoin imperfections permanently built into the system, imperfections which a competitor could improve upon. Furthermore the longer Bitcoin stays in the public eye, the more likely that an established institution will label its new and improved product LegitCoin and give it a big boost.)

You can think of that $20 billion — or perhaps just some chunk of that? — as a very rough measure of the prize to be won if you can come up with a successful Bitcoin competitor. Even a fraction of that sum will spur some real effort.

In short, we are still in a situation where supply-side arbitrage has not worked its way through the value of Bitcoin. And that is one reason — among others — why I expect the value of Bitcoin to fall — a lot.

I thank Brad DeLong for an email query and analysis which sparked this blog post.

Addendum: Maybe I’ll write another post on the possible expected deflationary bias in any cryptocurrency, given that expected price changes usually get compressed into the present and that an overall expected rate of return equality must hold. And the question of how much an initial issuer can exempt itself from mining costs as a form of reaping upfront seigniorage. and the profit-maximizing way of sharing these gains with early adopters. Those are two hanging issues with respect to the analysis here, in addition to the matter of cost structure discussed in the parentheses above. And now go reread Kareken and Wallace (1981). “=/∞” I think one has to say here.

On the future of Dogecoin, BitCoin, and other cryptocurrencies of the non-realm

An email query from Brad DeLong reminds me of this old Bart Taub paper, “Private Fiat Money with Many Suppliers” (jstor):

A dynamic rational expectations model of money is used to investigate whether a Nash equilibrium of many firms, each supplying its own brand-name currency, will optimally deflate their currencies in Friedman’s (1969) sense. The optimal deflation does arise under an open loop dynamic structure, but the equilibrium breaks down under a more realistic feedback control structure.

There is also Marimon, Nicolini, and Teles (pdf) and the work of Berentsen., all building on Ben Klein’s piece from 1974. This literature has been read a few different ways, but I take the upshot to be that a) a monopolized private fiat money might be stable in supply, to protect the stream of future quasi-rents, and b) private competing fiat monies will not be stable in overall supply, for reasons of time consistency and also the competitive erosion of available rents. In other words, when it comes to the proliferation of cryptocurrencies, the more the merrier but not for those holding them.

I don’t agree with the modeling strategy of this 1981 Kareken and Wallace paper on the indeterminacy of equilibrium exchange rates, but still it is another useful starting point.

Addendum: Krugman adds a bit more on Bitcoin, from a friend of his, John R. Levine. Here is the final bit from Levine:

My current guess is that the Bitcoin bubble will collapse when there is some bad news, e.g., a regulator demands registration of Bitcoin wallets, people try and cash out, and find that that while it’s easy to buy bitcoins, it’s much harder to find people willing to buy back nontrivial amounts, very hard to collect the sales proceeds, and completely impossible without revealing exactly who you are.

Carl-Henri Prophète on Haitian economic growth

He writes to me:

…just to let you know that Haiti’s economy grew by 4.3% in 2013. This is the highest growth rate since the 1970s excluding post embargo and post earthquake years (1995 and 2011). Nothing spectacular, but worth noticing I think. Some people may question these numbers in a country where the National Statistics Institute regularly looses its best staff to NGOs where they can earn 3 times their previous salary. But there is a general feel that economic activity was definitely higher than usual in 2013.

This is partly due to luck: There were no hurricanes or major drought period during the year, so agriculture which accounts for around a 1/4 of the economy grew by 4.6%. The construction sector did also well (+9%) thanks to major infrastructure investment by the government funded by generous Venezuelan aid and some major private investments (in the hotel sector for instance). Exports also increased in real terms by 5%. By the way, there are two firms assembling low cost Android tablets in the country now, which may lead to a greater diversification in exports away from garments in the future. (see here http://bit.ly/1lnVVxjand here http://bit.ly/Jkit6v)

However, inequality is still very high and even more spatially visible as the relatively wealthy suburb of Petion Ville is booming and has became the de-facto capital since the earthquake. Also, there are questions about how long this Venezuelan aid will last and its impact on the country’s debt, corruption and government accountability. Furthermore, there should be elections for many parliament seats in 2014 which may fuel political instability.

*The Second Machine Age*

The authors are Erik Brynjolfsson and Andrew McAfee, and the subtitle is Work, Progress, and Prosperity in a Time of Brilliant Technologies.

I have written enough on related issues that a review seems pointless, but after having read it through I will say a) it will be one of the most important books of the coming year, and b) everyone should read it. It will be out January 20, 2014.

Here is Pethokoukis on the book, with a handy summary. Here is a new Tim Harford column citing the book.

Why does Singapore have such a low birth rate?

In the comments, Collin asked:

How is it the most productive, functional country Singapore has one of the lowest birth rate in the world? Is this robot future in which only the better off have children? Why is it richer the world is the less people can afford children?

Right now the total fertility rate in Singapore is at about 1.2 and at times it has slipped down as far as 1.16. (Though it just went up to 1.29, perhaps because of “dragon babies,” noting that intertemporal substitution may snatch some of this back.) Why?

1. Singapore does education very well, and education lowers birth rates.

2. Singapore land and housing prices are especially high, which makes it very costly to have a family with three kids. Long working hours are expected too.

3. Singapore is a lot more fun than it used to be, and in this regard it has improved more than say France has. Children are a bit more fun, because modern life is safer, but “the fun of children” is subject to Baumol’s cost disease.

4. Women are doing very well in Singapore and arguably they are not so willing to marry down in terms of income and educational status. I was struck, when I gave a talk to the economists at the Civil Service College in Singapore this summer, that well over half the audience was female. Sadly for some, rates of female “singlehood” for women in their twenties are still rising (pdf, very useful). Controlling for education, however, female singlehood is not going up, which indicates the decline in fertility is related to the rise in education. And in that same piece you will find direct evidence for a “marriage squeeze” for well educated women and less educated men. That same squeeze doesn’t seem as strong in the other wealthy East Asian countries.

5. This 209 pp. cross-national comparative study (pdf, also very useful) suggests that Singapore’s generous childbearing subsidies do not work because women are still expected to shoulder so many responsibilities of child rearing. The traditional family model there is stronger than in say France. At the same time, France is a culture of leisure, long vacations, and limited work hours in a way which is quite far from practices in Singapore.

6. Modern fairytales do not work. Rap music also does not work (try this video, if you need help), nor do government-sponsored cruises and speed dating services.

7. It is suggested that population density lowers birth rates.

8. Child care and subsidized child care have been less common in Singapore than in France (see about p.119 of this pdf, the comparative study cited above), though Singapore has been changing in this regard.

Here is a typical Singaporean answer to the question:

What is stopping you from having more than 1-2 children?

“Very stressful, because when they misbehave, you have to scold them.”Why do you think some Singaporeans are not having children nowadays?

“It is very stressful for Singaporeans as the cost of living has gone up and they do not have time for their children. More women are now busy working too.”

If you are interested in the comparison, ethnic Chinese in Malaysia have a total fertility rate of about 1.8. Malays in Singapore have a TFR of about 1.6, whereas the ethnic Chinese and ethnic Indians in Singapore are just barely above 1.0. To me that suggests that both culturally-specific-to-Chinese-high-earner factors and cost-of-living-in-Singapore factors are playing a significant role. Malay population growth, in terms of Malay babies born in Malaysia, is robust. Perhaps Singaporean men need more confidence. In Shanghai, by the way, the rate is barely above 1.0.

If I had to put it all in a sentence, I might try this: in Singapore, work and educational norms have shifted far faster than have family norms, relative to other birth-subsidizing countries such as France.

Note, most of all, that the low birth rate in Singapore is not the fault of Lee Kuan Yew.

Walter Oi has passed away

Here is an appreciation from David Henderson. Here is an appreciation from Steve Landsburg. Oi played a key role in helping to end the military draft, he was a mainstay of the Rochester economics program, he wrote an essential piece on the economics of two-part tariffs, he analyzed the implications of labor as a fixed factor for employment over the course of the business cycle, and also he was known for having overcome blindness to pursue a very successful career. Here is Oi on scholar.google.com.

John Cochrane on portable health insurance

The entire Op-Ed is interesting and noteworthy, but the part on health insurance is perhaps the cutting edge of the piece analytically:

Health insurance should be individual, portable across jobs, states and providers; lifelong and guaranteed-renewable, meaning you have the right to continue with no unexpected increase in premiums if you get sick. Insurance should protect wealth against large, unforeseen, necessary expenses, rather than be a wildly inefficient payment plan for routine expenses.

People want to buy this insurance, and companies want to sell it. It would be far cheaper, and would solve the pre-existing conditions problem. We do not have such health insurance only because it was regulated out of existence. Businesses cannot establish or contribute to portable individual policies, or employees would have to pay taxes. So businesses only offer group plans. Knowing they will abandon individual insurance when they get a job, and without cross-state portability, there is little reason for young people to invest in lifelong, portable health insurance. Mandated coverage, pressure against full risk rating, and a dysfunctional cash market did the rest.

Rather than a mandate for employer-based groups, we should transition to fully individual-based health insurance. Allow national individual insurance offered and sold to anyone, anywhere, without the tangled mess of state mandates and regulations. Allow employers to contribute to individual insurance at least on an even basis with group plans. Current group plans can convert to individual plans, at once or as people leave. Since all members in a group convert, there is no adverse selection of sicker people.

I suppose my worry is this. As individuals age, they will become greater health risks and that will hold even if Cochrane keeps Medicare going. That means a higher price for their individual portable insurance. It is not clear to me under what conditions premia can be raised legally (what does “unexpected increase” mean?), but it seems the result is much higher premia for sick people, or legally-mandated low premia, but then providers will restrict access and lower the quality of care, as another means of raising the price of course. Contractually speaking, price is verifiable but quality of care is not. The overall problem is not one of “adverse selection” but rather simply that the good information of the suppliers means that insurance is hard to sell at all for many conditions.

I do understand the option of letting the premia rise, and selling insurance against that event too, and maybe that could work. Still, it is surprising how many insurance markets don’t really blossom even if it seems they would make economic sense. Just ask Robert Shiller or look at the earlier history of failed CPI futures. I’d like to experiment with Cochrane’s idea, which I think has real promise, but on a trial basis first. The question is what such a trial might actually mean, and who would be willing to give up their current arrangements to make such an experiment possible. If the recent Obamacare reactions show anything, it is that status quo bias is getting stronger all the time in matters of health care.

Is the United States saving rate too low?

Evan Soltas reports:

The conventional story is that the U.S. has undersaved and overconsumed for decades…

Why is that story wrong? It ignores the fact that households and institutions make up only about a third of U.S. gross saving.

Domestic businesses, which do the other two thirds of U.S. saving and are not reflected in that personal savings rate, have been saving far more than they have in the past. That has offset the decline in personal saving. We can see that in a graph of gross private saving over gross domestic income below.

The U.S. saves about one fifth of gross domestic income — it saved a little more than that in the 1970s and over the last few years, a little less than that in the 1950s and the 1990s. The apocalyptic trend towards zero savings is simply not there. What appears to be a long-term decline in the savings rate is in fact a hand-off between households and businesses in who does the saving.

There are useful graphs at the link and basically it means you should have bought those extra Christmas presents. I would add the cautionary note — for Americans but not for the world — that business savings may be more mobile internationally than are household savings. You also can view these numbers as a harbinger of greater wealth inequality in our future.

From the comments, on seasonal business cycles

ohwilleke reports:

While “Christmas” is new, the notion of a consumption splurge after the fall harvest, followed by a lean late winter-early spring season (Lent/Ramadan) before the spring harvest is deeply rooted in pre-modern agricultural reality. When you have an abundance of perishable goods it makes sense to consume them before they go bad, and then to string out the more limited supply of durable foodstuffs when fresh foodstuffs are scarce. In the same way, summer vacation is rooted in the need to free up children for agricultural labor at times of peak demand. As noted above, spring weddings supply a consumption boost after the Spring Harvest and also are timed to minimize the likelihood of critical parts of a first pregnancy taking place during the lean late winter-early spring (although these days it has more to do with the end of the school year).

Only with cheap and fast trans-hemispheric shipping (together with a lack of significant piracy for most of that trade), and advances in food preservation and refrigeration in the last half century or so, have those agricultural considerations become irrelevant (although, of course, excess and lean times should fall at different parts of the year in the Southern hemisphere and in places like Southern India, the Sahel, and the tropics of Asia, African and South America that have different seasons).

Japan and China use end of year bonuses (often as 6-12% of annual compensation) as a significant part of annual compensation as a way to share rather than leveraging macroeconomic risk for firms and the economy as a whole. In good years, when there is more supply, lots of people get big bonuses; in bad years, scarcity is widespread. The main virtue of this approach is that it makes firms more robust and puts them under less pressure to engage in cyclic layoffs but making labor costs look more like equity and less like debt. This too was well suited to an agricultural tradition rooted in sharecropping or the equivalent that was once widespread in all feudal economies as well as in neo-feudal economies in places like the American South. This isn’t a strategy limited to the orient. It is also the quintessential Wall Street economy model utilized by major financial firms like investment banks and the large law firms that serve them.

The pressure from the “real economy” – both the goods and services supply side and the labor demand side – to have punctuated consumption is much weaker now than it once was, particularly in economies or sectors of economies without the strong annual bonus tradition. The largest sectors of the modern economy that are both strongly cyclic in terms of business cycles and very seasonal within each year, are construction and real estate – and these cycles also drive a fair amount of durable goods consumption. Both construction and real estate are weakest in the winter. Agriculture’s share of the economy is now much more stable from a consumer’s perspective and much smaller as a percentage of the total economy. Real estate handles cyclic shifts by being largely commission based. Construction relies on highly fragmented project specific team building through networks of general contractors and subcontractors rather than integrated firms (a pattern also common in the film industry and theater industry).

Bottom line: The finance oriented macroeconomic models obsessed with interest rates, inflation, GDP growth rates, unemployment rates and size of the public finance sector are ill suited to analyzing optimal seasonal business cycle patterns. A more fruitful analysis looks at the roots of current seasonal patterns in economic history and at the way that the “real economy” has changed with technology to see if those patterns still make sense, perhaps for new reasons.

You will find ohwilleke’s blog here.