Category: Economics

Are corporate profits a sinkhole for purchasing power?

That seems to be Krugman’s argument here, and here, excerpt:

So corporations are taking a much bigger slice of total income — and are showing little inclination either to redistribute that slice back to investors or to invest it in new equipment, software, etc.. Instead, they’re accumulating piles of cash.

I am confused by this argument. I would understand it (though not quite accept it) if corporations were stashing currency in the cupboard. Instead, it seems that large corporations invest the money as quickly as possible. It can be put in the bank and then lent out. It can purchase commercial paper, which boosts investment.

Maybe you are less impressed if say Apple buys T-Bills, but still the funds are recirculated quickly to other investors. This may not end in a dazzling burst of growth, but there is no unique problem associated with the first round of where the funds come from. If there is a problem, it is because no one sees especially attractive investment opportunities in great quantity. (To the extent there is a real desire to invest, the Coase theorem will get the money there.) That’s a problem at varying levels of corporate profits and some call it The Great Stagnation.

The same response holds if Apple puts the money into banks which earn IOR at the Fed and the money “simply sits there.” The corporations are not withholding this money from the loanable funds market but rather, to the extent there is a problem, the loanable funds market does not know how to invest it at a sufficiently high ROR.

If anything, large corporations are more likely to diversify out of the U.S. dollar, which could boost our exports a bit, a plus for a Keynesian or liquidity trap story.

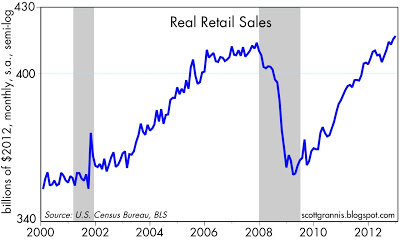

When one looks at the components of aggregate demand, retail sales, after a large and obvious hit, seem to be recovering. They are up 4.7% from Dec. 2011 to Dec. 2012 (pdf). If that is what a sinkhole looks like, as I said I am puzzled:

Here is the story of business investment minus corporate profits and that series doesn’t impress me (Krugman seems to think it is doing OK). The trickier variable of net investment you will find here and that looks worse.

By the way, Fritz Machlup considered related arguments in his 1940 book.

My real fear about the UK productivity puzzle

…Britain’s economists are also puzzling over why the economy remains moribund even though more and more people are in work. There are still about half a million fewer people working as full-time employees than there were before the 2008 crash, but the number of people in some sort of employment has surpassed the previous peak. Economists think the rise in insecure temporary, self-employed and part-time work, while a testament to the British labour market’s flexibility, helps to explain why economic growth remains elusive.

That is from Sarah O’Connor’s excellent FT piece about working for Amazon in their warehouses.

How much does graduate school matter for being an economics professor?

There is a new paper, by Zhengye Chen, an enterprising undergraduate from the University of Chicago:

Of the 138 Ph.D. economics programs in the United States, the top fifteen Ph.D. programs in economics produce a substantial share of successful economics research scholars. These fifteen Ph.D. programs in turn get 59% of their faculty from only the top six schools with 39% coming from only two schools, Harvard and MIT. Those two schools are also the PhD origins for half of John Bates Clark Medal recipients. Details for assistant professors, young stars today, American Economics Association Distinguished Fellows, Nobel Laureates, and top overseas economics departments are also discussed.

There is much more here, and for the pointer I thank Lee Benham. I’ll add three points:

1. It has been evident for a while that the former “top six” is in some ways collapsing into a “top two,” namely Harvard and MIT.

2. I was surprised that NYU beats out Stanford for the #6 slot.

3. Two Nobel Laureates, John Hicks and James Meade, did not have a Ph.d at all.

Health care cost control in Massachusetts, continuing the bad news string for ACA

Representatives from the state’s nonprofit health plans as well as national for-profit insurers doing business in Massachusetts estimated the “medical cost trend,” a key industry measure, will climb between 6 and 12 percent this year — higher than last year’s cost bump and more than double the 3.6 percent increase set as a target in a state law passed last year.

Here is more, and for the pointer I thank Jeffrey Flier.

Sentences about coal

Europe’s use of the fossil fuel spiked last year after a long decline, powered by a surge of cheap U.S. coal on global markets and by the unintended consequences of ambitious climate policies that capped emissions and reduced reliance on nuclear energy.

…In Germany, which by some measures is pursuing the most wide-ranging green goals of any major industrialized country, a 2011 decision to shutter nuclear power plants means that domestically produced lignite, also known as brown coal, is filling the gap . Power plants that burn the sticky, sulfurous, high-emissions fuel are running at full throttle, with many tallying 2012 as their highest-demand year since the early 1990s. Several new coal power plants have been unveiled in recent months — even though solar panel installations more than doubled last year.

Here is more.

And first they came for the law professors…

Last week, it was reported that law school applications were on pace to hit a 30-year low, a dramatic turn of events that could leave campuses with about 24 percent fewer students than in 2010. Young adults, it seems, have fully absorbed the wretched state of the legal job market.

Beware most measures of government consumption

Garett Jones reports:

Here’s one big area where I think we should change what we call one type of government spending: Medicare and Medicaid. Currently, these types of spending are counted as transfer payments (BEA PDF here) and so when we measure GDP they show up in C, consumer purchases. I think they should show up in G, government purchases. These medical purchases are so tightly controlled by the government that doctors–oops, “medical service providers”–have become and should be considered government contractors just like defense contractors or construction firms.

Sometimes you hear or read talk of “government consumption plunging,” but sometimes what is happening is that health care expenditures are crowding out other programs, which is not exactly the same thing as fiscal consolidation.

Good sentences about fashion and copying

The mass copying of a style is what creates a trend, and trends sell clothes today. This is why many in the industry furiously protect their right to ripping each other off. Two law professors, Kal Raustiala and Chris Sprigman, have argued against the design piracy act on the grounds that the American apparel industry “may actually benefit” from copying, as it speeds up the creation and exhaustion of trends.

Note the clever assignment of the externality. Rapid copying is needed for customers to develop the expectation that trends come and go rapidly, and thus to get customers to visit the store and buy today. Yet no single business will invest enough on its own in creating these broader expectations, because the industry as a whole reaps the benefit. The “copying game” induces the sellers to, in essence, act collusively to help establish these “hurry up and buy now” expectations.

The quotation is from Elizabeth L. Cline’s Overdressed: The Shockingly High Cost of Cheap Fashion, which I quite enjoyed reading, despite some glaring weaknesses when it comes to FDI, wages, and foreign development. I now understand the affordable yet fashionable clothing stores in Tysons Corner Mall, and how they have changed over the last fifteen years, and I can thank this book for that.

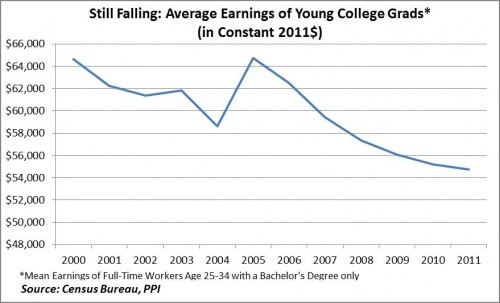

Average earnings of young college graduates are still falling

Alas, take a look:

Diana G. Carew, who works with Michael Mandel, reports:

The latest Census figures show real earnings for young college grads fell again in 2011. This makes the sixth straight year of declining real earnings for young college grads, defined as full-time workers aged 25-34 with a bachelor’s only. All told, real average earnings for young grads have fallen by over 15% since 2000, or by about $10,000 in constant 2011 dollars.

That picture is the single biggest reason why higher education in this country is in economic trouble as a sector. And yes, I do understand that the “education premium” is robust, but that means wages for non-college workers have been hurting as well. At some margin, when it comes to determining how much you will pay for college, the absolute return matters too. The full article is here.

Will health insurance premia rise for young males?

I suspect the analysis cited in this article is an exaggeration, but it is even more than I thought the exaggeration would be:

The survey, fielded by the conservative American Action Forum and made available to POLITICO, found that if the law’s insurance rules were in force, the premium for a relatively bare-bones policy for a 27-year-old male nonsmoker on the individual market would be nearly 190 percent higher.

…Insurers have been reluctant to share their premium projections for a variety of reasons, but Holtz-Eakin, through a lawyer intermediary, was able to get aggregated, anonymous data under a nondisclosure agreement. On average, premiums for individual policies for young and healthy people and small businesses that employ them would jump 169 percent, the survey found.

Note that subsidies would cushion such price shocks for lower-income individuals and that the premia for older and less healthy people would fall, by twenty-two percent according to a comparable estimate (do not forget that a smaller percentage figure is being applied to a larger absolute number). From a distance, it is difficult to judge how realistic these projections are.

Still, I would think that the chance of younger individuals refusing to adhere to the mandate is higher than Massachusetts-linked projections have been indicating.

I would say that in recent times there has been a string of bad news about ACA and few new reported items of good news.

Addendum, from the comments, from Carl the Econ Guy:

The whole survey is here:

http://americanactionforum.org/sites/default/files/AAF_Premiums_and_ACA_Survey.pdf

Look at Table 1– where it says that the average premium for young healthy males will go from $2,000 to a little over $5,000. Yikes.

A simple macro model of collateral

Regulators are pushing for non-centrally cleared trades to be backed by high levels of collateral, such as cash or government bonds. This is where the $10tn figure comes in. It is the amount of extra collateral that could be required according to estimates by the International Swaps and Derivatives Association.

Here is the full FT article. It stresses that figure of ten trillion may be too high an estimate, but a separate lower estimate still runs at $2 to $4 trillion.

Let’s play out the scenario. In some future world, what if most savings is done by corporations and also by traders at the clearinghouse, in the form of collateral. Collateral, however, is not “smoothed” across assets but rather is an either/or decision. They won’t take your sheepdog as collateral, nor will they take shares in small tech companies. Most of the saving is done in the form of approved safe assets and the rest of the economy is somewhat starved for investment.

I call it the return of financial repression. Let’s see how far it is allowed to go.

The Cyprus bailout

No one wants to bail out Cyprus because it is “Greece with dodgy banks,” one third Russian depositors, a tax haven, corrupt, and the banking system is measured at eight times the size of the real economy. Even a pro-bailout politician may not wish to soil the name of bailouts by handling this case. The Germans are balking.

But if depositors take losses in Cyprus, what kind of precedent does this set?

One risky scenario is that it sets off a run on some of the weaker eurozone banks.

A better case scenario is that the market distinguishes Cyprus from the other cases (all of them? some of them?) in the eurozone and European Union. But that too involves a trick. Let’s say the market can distinguish Cyprus from Spain. Can the market also distinguish Greece from Spain? Is it good to break the expectation of “we’re all in this together,” even when doing so is justified?

A systemically costless fail of credit obligations in Cyprus is itself risky. It leads people to start wondering what else might be a systemically costless fail and testing that boundary. (“If we let Greece go, maybe they’ll know we are still committed to Spain…”) Which means a Cyprus fail might be systemically costly in the first place.

Developing…

Acemoglu and Robinson on the great stagnation

Two things are absent in this debate, however.

First, much evidence shows that what determines technological innovations isn’t some sort of “exogenous innovation capacity,” but incentives…

Schmookler illustrated these ideas vividly with the example of the horseshoe. He documented that there was a very high rate of innovation leading to improvements in the horseshoe throughout the late 19th and early 20th centuries because the increased demand for transport meant increased demand for better and cheaper horseshoes. It didn’t look like there was any sort of limit to the improvements or any evidence of an “exogenous innovation capacity” in this ancient technology, which had been around since 2nd century BC. Then suddenly, innovations came to an end, but this had nothing to do with running out of low hanging fruit. Instead, as Schmookler put it (p. 93), it was because the incentives to innovate in this technology disappeared because “the steam traction engine and, later, internal combustion engine began to displace the horse… “

Their full post is here.

I have changed my mind on this issue quite a bit over the last four to five years. Yes incentives matter, but outside of extreme environments are changes in incentives explaining the changes in what we observe? I now think it is of critical importance where a sector or economy is on “the innovation curve.” It was easier to innovate in game theory in the 1980s than it is today, even though the salaries of top economists have risen significantly. The pharmaceuticals market is larger than ever before, and yet the pipeline is largely dry. We are simply at a point where further breakthroughs are hard (and it is not obvious that FDA innovation taxes are getting worse over this period of change.) Weren’t so many inventors of the 19th century largely “yahoos,” with no fancy degrees, relatively low pay, little or no peer review, not at the peak of the Flynn effect, and so on, and yet they were on a fruitful part of the innovation curve and performed wonders.

I think in terms of general purpose technologies and platform-like breakthroughs. Once you get them, innovation runs wild, otherwise it is tough sledding, with incentives still accounting for some of the variation within a particular place on the innovation curve.

Good shop name

That is from the web site of Nancy Hanrahan, who teaches sociology and critical theory and music at George Mason. Just recently I was talking to a Polish man whom I met standing in front of The Village Vanguard, and who claims to own 20,000 jazz LPs, and he told me that Nancy is married to Kip Hanrahan, the esteemed yet still underrated jazz musician, start with Desire Develops an Edge.

Mark Thoma’s spending cuts

Here is a Mark Thoma comment on my recent column, here is the introduction:

I’m all for more cuts to defense too, but it’s only fair to note that some cuts have been made there already.

Also, why are only spending cuts mentioned when the discussion is the budget? Please don’t tell me that if it’s not spending cuts, i.e. if it’s a tax increase, it doesn’t count for budget discussions (and Keynesian economics, which is part of his discussion, does not make this distinction). Thus, note also that the American Taxpayer Relief Act (ATRA) added another half trillion in deficit reduction. Together, the $1.5 trillion in appropriations cuts, plus the $.5 trillion in tax increases in the ATRA, plus the $300 billion in interest savings amount to around a bit over $2.3 trillion in deficit reduction…

Not once in Mark’s post does the word “baseline” appear. In fact I covered the defense “appropriations cuts” in my piece, noting that relative to baseline, even with the sequester (much less without) defense spending is roughly constant in real terms. Mark simply doesn’t recognize I made that point but instead portrays me as oblivious to the issue. (Additional comments from Angus here). I don’t see that as much evidence for our fiscal rectitude.

Or let’s look at the bigger picture of the back and forth. Take Mark’s sentence: “Also, why are only spending cuts mentioned when the discussion is the budget?”, after which he refers to tax increases. My very last column I called for tax increases, a bit now and more later. Mark covered that column. What was Mark’s reaction then? He complained that I didn’t also call for rectification of the content of government spending decisions and income shares, in both cases toward greater egalitarianism.

I see Mark as falling into a bad habit here, namely he encounters a specific argument which makes him uncomfortable and then looks around for reasons to reject or downgrade the source of that argument, rather than focusing on the argument itself.

Mark also accuses me of being ideological. That’s in the eye of the beholder. In this week’s column I called for cuts in farm subsidies (or abolition), Medicare, and defense, and switching out of any possible cuts in infrastructure or support for basic research. That’s pretty close to the consensus of economists. Elsewhere I’ve called (repeatedly) for significant increases in science funding and the fixing of LaGuardia airport, among other infrastructure projects. In the column I argue that there are both demand-side and supply-side reasons for drawing the distinctions I do between which parts of spending should be boosted and which should be cut. I argue that Keynesian economics is valid if applied correctly. Ryan Avent, not a member of the Tea Party, says he has “some sympathy” for my views on the sequester. I don’t doubt that I am to the libertarian side of Mark, but if he finds that all too ideological, and worthy of a calling out, I think he is skating at a margin where he will find it very difficult to learn from the people who disagree with him.