Questions that are rarely asked

But they are asked by Roland Stephen:

What signals are food trucks sending by pricing only in round numbers ($6, $8 etc.) unlike brick and mortar competitors (whose prices are often very similar, but expressed with lots of .95s )?

My best guess is this. You buy something from a food truck and then you eat it. You don’t keep running up a tab. (The same is true for food stalls by the way, though you may run up a tab in the hawker centre as a whole.) In a sit-down restaurant, there is a sequence of salad, main course, drinks, dessert, and so on. People might estimate their total running bill using first digits, and thus there is reason to “trick” them into thinking they have spent somewhat less than they have. The food truck doesn’t have that same incentive.

Addendum: Many of you say “to economize on change,” and maybe so. But why is this motive especially strong at food trucks? The truck clearly has the room to carry the change, and the typically urban clientele is the same group of people who are paying $6.99 plus tax somewhere else. In this context maybe speed matters more, or the percentage of cash transactions is higher to the extent many trucks do not take credit cards or wish to discourage the use of such cards.

What kind of doctor should I become?

Hi Professor Cowen,

I am a loyal MR reader and I wondered if you could comment on the following situation:

I am a 3rd year medical student, and for the purposes of this question, let’s assume I have equal interest and ability in the various medical specialties. In order to create the greatest good for the greatest number of people through my work in medicine (i.e., the highest return to society), what specialty should I pursue? I should add that, although I intend to practice in the U.S., I am open to devoting as much of my free time/vacation as possible to pro bono medical activities, and further, that I wish to do the interventions myself (instead, for example, or just making lots of money and then donating the proceeds to some other charitable activity). In attempting to answer this question, I’ve been looking at DALYs and QALYs associated with various medical interventions (e.g., cataract surgery). Am I going about answering this question the right way? Any thoughts?

An interesting corollary would be asking what job, in any field, has the highest return to society. Is there any literature on this?

The fundamental institutional failure to overcome is that many lives “out there” are pretty happy, and very much worth living, but those individuals do not have enough money to afford reasonable doctors. If you are seeking to maximize social welfare, look to step into some of these gaps.

But which gap in particular?

The second binding constraint, in my view, is that most people won’t in fact go through with their plan to do a lot of social good. That means you too. So you wish to seek out a form of do-gooding which is incentive-compatible over the long run, or in other words which is fun for you or rewarding in some other way. This second consideration is likely to prove decisive.

For instance you might decide the fight against dengue (just an example to make a point, not an actual net assessment) is the way to go, based on a narrow cost-benefit analysis. But it is hard as a field worker to really, fully protect yourself against dengue. And getting dengue can be very bad indeed. As you age, the pressures not to go into the field will mount. You might do more good by pledging your efforts to fight a malady which you can help fix without so much direct risk or exposure to yourself, let’s say infant mortality.

You will note a difference here between pledges of individual effort and pledges of money. A money pledger, thinking in game-theoretic Nash terms, will realize that effort pledgers will resist the fight against dengue. That is all the more reason why throwing money at the fight against dengue may bring high returns, namely that at the margin not enough is being done from the side of volunteer and quasi-volunteer labor. (In general this distinction creates a problem with talking up one kind of cause over another, namely that labor and money face differing incentives and should hear different messages of encouragement.)

You will note also that in a second best optimum, field workers will appear to be “consuming too many perks.” At the same time, donated funds should be trying to push field workers out of their comfort zones, at least on the margin.

I would add two final points. First, if you have a reasonable chance of being a research superstar, that may be the path to follow.

Second, if you are not already attached, spent time cultivating social circles (aid work, World Bank, vegetarians, etc.) where you are likely to meet a partner or spouse who will support a similar vision to help the world.

Addendum: David Henderson adds comment.

The costs of measuring value too precisely (model this)

…the editors at The Verge have a policy that seems a little bit odd and anachronistic: They don’t let writers see how much traffic their stories generate. Ever.

As the American Journalism Review reported, in a piece called “No Analytics for You: Why The Verge Declines To Share Detailed Metrics With Reporters,” the editors at The Verge simply don’t want their writers thinking about traffic.

What’s more, The Verge is not alone in this practice. Re/code, a tech site run by Kara Swisher and Walt Mossberg, the longtime Wall Street Journal tech columnist, also won’t share traffic stats with writers. MIT Technology Review holds numbers back too.

“We used to show the writers and editors traffic, and told them to grow it; but it had the wrong effect. So we stopped,“ says Jason Pontin, CEO, editor in chief and publisher of MIT Technology Review. ”The unintended consequence of showing them traffic, and encouraging them to work to grow total audience, is that they became traffic whores. Whereas I really wanted them to focus on insight, storytelling, and scoops: quality.”

That phrase – “traffic whore” – tells you everything you need to know about why some journalists have an aversion to chasing traffic. They fear it creates an incentive to do the wrong things.

Of course these policies hold only at some margins I believe…nor are they used at Gawker.

The full article, by Dan Lyons, is here.

Assorted links

1. How crowdsourcing helps robots.

2. Do zebras have stripes to confuse flies?

3. The top 30 thinkers under 30? (includes three in economics).

4. Why did the greatest living juggler open a construction business?

5. The new demand for terminal masters in economics. And Japanese yakuza marketing.

High-frequency trading and the retail investor

Matthew Philips explains it clearly:

The idea that retail investors are losing out to sophisticated speed traders is an old claim in the debate over HFT, and it’s pretty much been discredited. Speed traders aren’t competing against the ETrade guy, they’re competing with each other to fill the ETrade guy’s order. While Lewis does an admirable job in the book of burrowing into the ridiculously complicated system of how orders get routed, he misses badly by making this assumption.

The majority of retail orders never see the light of a public exchange. Instead, they’re mostly filled internally by large wholesalers; among the biggest are UBS (UBS), Citadel, KCG (KCG) (formerly Knight Capital Group), and Citigroup (C). These firms’ algorithms compete with each other to capture those orders and match them internally. That way, they don’t have to pay fees for sending them to one of the public exchanges, which in turn saves money for the retail investor.

There is also this:

…according to estimates from Rosenblatt Securities, the entire speed-trading industry made about $1 billion, down from its peak of around $5 billion in 2009. That’s nothing to sneeze at, but it isn’t impressive once you put it into context: JPMorgan Chase (JPM) made more than $5 billion in profit in just the last quarter.

If that doesn’t convince you, just listen to all those Keynesians who are proudly calling this a form of useful economic stimulus, akin to pyramid-building, or an invasion from outer space…oh wait…

Facts about hotel mini-bars (model this)

What’s surprisingly affordable in hotel rooms across the globe is, however, vodka. It’s much cheaper than peanuts and, in some cases, even water.

That is the case for instance in Zurich, Helsinki, and Oslo. (Where is the profitable cross-subsidy? Or is this price discrimination? Is vodka less likely to be claimed for reimbursement from third-party payment?) In Toronto hotel minibars, a can of nuts costs on average $18.23, at least among the hotels sampled.

That is all from Annalisa Merelli, via David Wessel.

Does classroom time matter?

Maybe not so much. There is a new NBER working paper by Theodore J. Joyce, Sean Crockett, David A. Jaeger, Onur Altindag, and Stephen D. O’Connell, the abstract is here:

We test whether students in a hybrid format of introductory microeconomics, which met once per week, performed as well as students in a traditional lecture format of the same class, which met twice per week. We randomized 725 students at a large, urban public university into the two formats, and unlike past studies, had a very high participation rate of 96 percent. Two experienced professors taught one section of each format, and students in both formats had access to the same online materials. We find that students in the traditional format scored 2.3 percentage points more on a 100-point scale on the combined midterm and final. There were no differences between formats in non-cognitive effort (attendance, time spent with online materials) nor in withdrawal from the class. Comparing our experimental estimates of the effect of attendance with non-experimental estimates using only students in the traditional format, we find that the non-experimental were 2.5 times larger, suggesting that the large effects of attending lectures found in the previous literature are likely due to selection bias. Overall our results suggest that hybrid classes may offer a cost effective alternative to traditional lectures while having a small impact on student performance.

I do not see an ungated copy, do any of you find one?

The falling market share of General Motors

The General Motors market share in the US fell from 62.6% to 19.8% between 1980 and 2009, noticed Susan Helper and Rebecca Henderson. Helper is now the chief economist at the US commerce department, and Henderson is a management professor at Harvard.

The article is by Heidi Moore. The market here is working, but oh so slowly. I would like to see behavioral economics papers on why so many people continued to buy General Motors (and here I mean the standard cars) for as long as they did.

Here is a timeline of GM recalls.

Matt Levine and Felix Salmon on Michael Lewis and HFT

In my alternative Michael Lewis story, the smart young whippersnappers build high-frequency trading firms that undercut big banks’ gut-instinct-driven market making with tighter spreads and cheaper trading costs. Big HFTs like Knight/Getco and Virtu trade vast volumes of stock while still taking in much less money than the traditional market makers: $688 million and $623 million in 2013 market-making revenue, respectively, for Knight and Virtu, versus $2.6 billion in equities revenue for Goldman Sachs and $4.8 billion forJ.P. Morgan. Even RBC made 594 million Canadian dollars trading equities last year. The high-frequency traders make money more consistently than the old-school traders, but they also make less of it.

There is more here. Here is Felix Salmon on the book:

Similarly, Lewis goes to great lengths to elide the distinction between small investors and big investors. As a rule, small investors are helped by HFT: they get filled immediately, at NBBO. (NBBO is National Best Bid/Offer: basically, the very best price in the market.) It’s big investors who get hurt by HFT: because they need more stock than is immediately available, the algobots can try to front-run their trades. But Lewis plays the “all investors are small investors” card: if a hedge fund is running money on behalf of a pension fund, and the pension fund is looking after the money of middle-class individuals, then, mutatis mutandis, the hedge fund is basically just the little guy. Which is how David Einhorn ended up appearing on 60 Minutes playing the part of the put-upon small investor. Ha!

Lewis is also cavalier in his declaration that intermediation has never been as profitable as it is today, in the hands of HFT shops. He does say that the entire history of Wall Street is one of scandals, “linked together trunk to tail like circus elephants”, and nearly always involving front-running of some description. And he also mentions that while you used to be able to drive a truck through the bid-offer prices on stocks, pre-decimalization, nowadays prices are much, much tighter — with the result that trading is much, much less expensive than it used to be. Given all that, it stands to reason that even if the HFT shops are making good money, they’re still making less than the big broker-dealers used to make back in the day. But that’s not a calculation Lewis seems to have any interest in.

Assorted links

1. The Monty Python culture that is Norway.

2. Tim Harford on the limits of Big Data.

3. Can gratitude reduce costly impatience?

4. Education, in-state vs. out-of-state tuition arbitrage. File under markets in everything.

5. Why has the price of limes quadrupled?

6. Proof by watercolor painting: “The Lamington, Australia’s famed dessert, was actually invented in New Zealand and originally named a “Wellington”, according to new research published by the University of Auckland.”

7. The extreme hazards of microbial sex (speculative).

*Particle Fever*

That is the new science documentary about the Hadron Collider and the search for the Higgs particle, reviewed here. I enjoyed it very much, and it makes being a scientist seem glamorous, in the good sense of that concept. The visuals of what goes on at CERN are striking, all the more so for being juxtaposed against mooing Swiss cows. And reheating a super-cooled magnet, and removing some helium contamination, is not easy to do.

The scientists in this movie seem to think their success will be measured in binary up/down fashion, and yet so far the results are mixed and inconclusive, as if they had been doing macroeconomics.

During one early part of the movie, at a public meeting, a self-proclaimed economist stands up from the audience and asks what is the economic rationale for the project, in front of a group of people drawn mostly from the scientific community. The man presenting the project responds proudly that such a question does not really need to be answered, and his audience of scientists cheers. The film audience in Greenwich Village was emboldened by this retort and there was audible positive murmuring, and some apparent scorn for the economist.

I wonder how the same scene would play out if the question concerned high-frequency trading?

A good sentence

I still want to see an economist reconcile a belief in secular stagnation with a belief in Piketty’s claim that the return on capital is going to exceed the growth rate of the economy on a secular basis.

That is from Arnold Kling.

Jürgen Osterhammel on the Crimean War

The Crimean War, which it lost, and resistance to its great-power pretensions at the Congress of Berlin in 1878, drove the Tsarist Empire to look farther eastward. Siberia acquired a new luster in official propaganda and the national imagination, and a major scientific effort was made to “appropriate” it. Great tasks seemed to lie ahead for this redeployment of national forces. The conviction that Russia was expanding into Asia as a representative of Western civilization — an idea that had originated in the first half of the century — was now turned in an anti-Western direction by currents inside the country. Theorists of Pan-Slavism or Eurasianism sought to create a new national of imperial identity and to convert Russia’s geographical position as a bridge between Europe and Asia into a spiritual advantage. The Pan-Slavists, unlike the milder, Romantically introverted Slavophiles of the previous generation, did not shrink from a more aggressive foreign policy and the associated risks of tension with Western European powers. That was one tendency. But after the 1860s, after the Crimean War, also witnessed the strengthening of the “Westernizers,” who made some gains in their efforts to make Russia a “normal” and, by the standards of the day, successful European country. Reforms introduced by Alexander II seemed to restore this link with “the civilized world.” But the ambiguity between the “search for Europe” and the “flight from Europe” was never dissolved.

That is from the just-published The Transformation of the World: A Global History of the Nineteenth Century. Here is my previous post on the book.

Here is Bryan Caplan “You Don’t Know the Best Way to Deal with Russia.” Here is a short piece on how much sympathy some Germans have for the Russians.

Assorted links

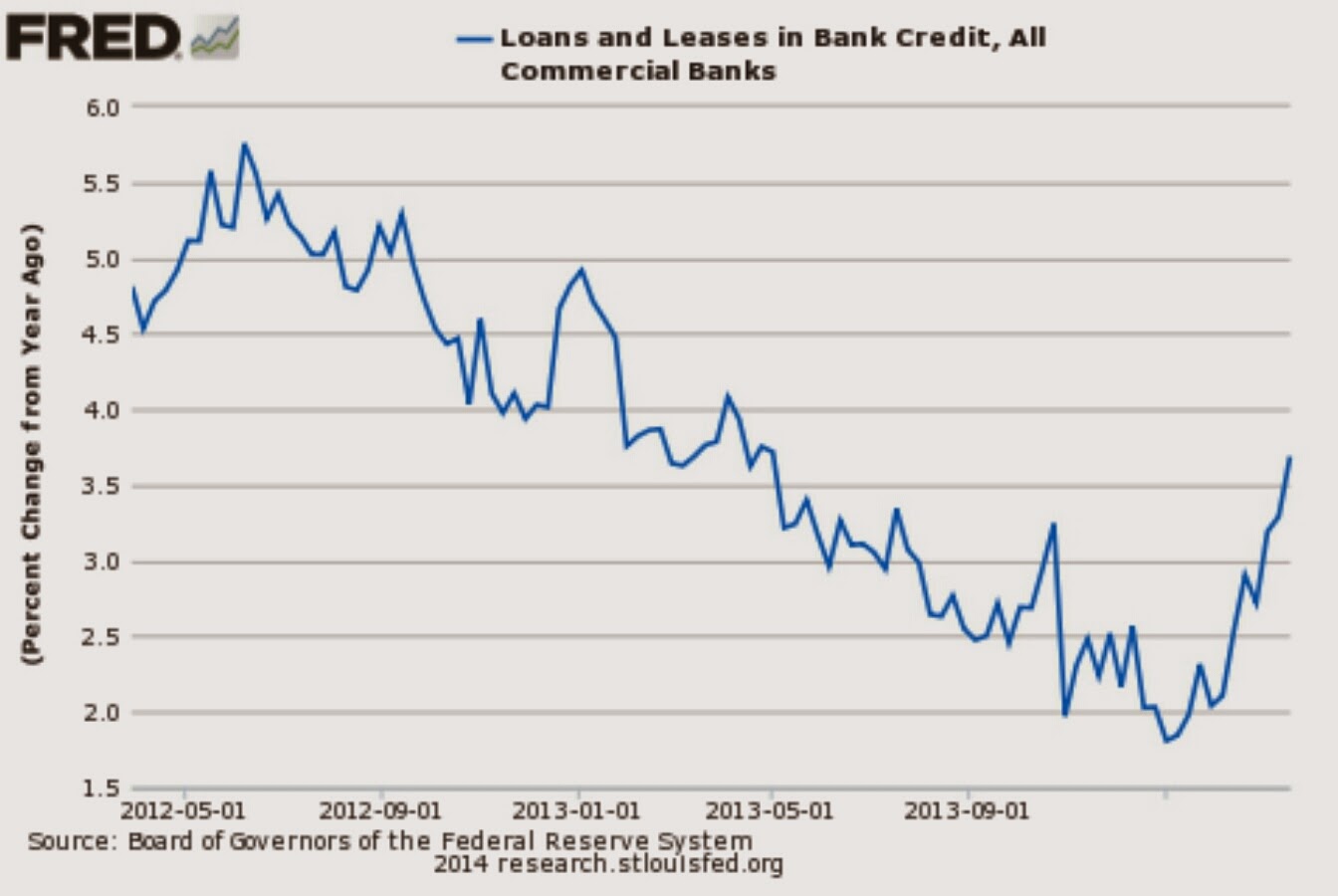

Loan growth and the taper

From Sober Look, there is further discussion and pictures here.