Charles Duhigg’s The Power of Habit

The skills necessary to ride a bike are multifaceted, complex and not at all obvious or even easily explicable to the conscious mind. Once you learn, however, you never forget–that is the power of habit. Without the power of habit, we would be lost. Once a routine is programmed into system one (to use Kahneman’s terminology) we can accomplish great skills with astonishing ease. Our conscious mind, our system two, is not nearly fast enough or accurate enough to handle even what seems like a relatively simple task such as hitting a golf ball–which is why sports stars must learn to turn off system two, to practice “the art of not thinking,” in order to succeed.

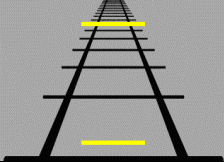

Habits, however, can easily lead one into error. In the picture at right, which yellow line is longer? System one tells us that the l ine at the top is longer even though we all know that the lines are the same size. Measure once, measure twice, measure again and again and still the one at top looks longer at first glance. Now consider that this task is simple and system two knows with great certainty and conviction that the lines are the same and yet even so, it takes effort to overcome system one. Is it any wonder that we have much greater difficulty overcoming system one when the task is more complicated and system two less certain?

ine at the top is longer even though we all know that the lines are the same size. Measure once, measure twice, measure again and again and still the one at top looks longer at first glance. Now consider that this task is simple and system two knows with great certainty and conviction that the lines are the same and yet even so, it takes effort to overcome system one. Is it any wonder that we have much greater difficulty overcoming system one when the task is more complicated and system two less certain?

You never forget how to ride a bike. You also never forget how to eat, drink, or gamble–that is, you never forget the cues and rewards that boot up your behavioral routine, the habit loop. The habit loop is great when we need to reverse out of the driveway in the morning; cue the routine and let the zombie-within take over–we don’t even have to think about it–and we are out of the driveway in a flash. It’s not so  great when we don’t want to eat the cookie on the counter–the cookie is seen, the routine is cued and the zombie-within gobbles it up–we don’t even have to think about it–oh sure, sometimes system two protests but heh what’s one cookie? And who is to say, maybe the line at the top is longer, it sure looks that way. Yum.

great when we don’t want to eat the cookie on the counter–the cookie is seen, the routine is cued and the zombie-within gobbles it up–we don’t even have to think about it–oh sure, sometimes system two protests but heh what’s one cookie? And who is to say, maybe the line at the top is longer, it sure looks that way. Yum.

System two is at a distinct disadvantage and never more so when system one is backed by billions of dollars in advertising and research designed to encourage system one and armor it against the competition, skeptical system two. Yes, a company can make money selling rope to system two, but system one is the big spender.

{kind=link}

Habits can never truly be broken but if one can recognize the cues and substitute different rewards to produce new routines, bad habits can be replaced with other, hopefully better habits. It’s habits all the way down but we have some choice about which habits bear the ego.

Charles Duhigg’s The Power of Habit, about which I am riffing off here, is all about habits and how they play out in the lives of people, organizations and cultures. I most enjoyed the opening and closing sections on the psychology of habits which can be read as a kind of user’s manual for managing your system one. The Power of Habit, following the Gladwellian style, also includes sections on the habits of corporations and groups (hello lucrative speaking gigs) some of these lost the main theme for me but the stories about Alcoa, Starbucks and the Civil Rights movement were still very good.

Duhigg is an excellent writer (he is the co-author of the recent investigative article on Apple, manufacturing and China that received so much attention) It will also not have escaped the reader’s attention that if a book about habits isn’t a great read then the author doesn’t know his material. Duhigg knows his material. The Power of Habit was hard to put down.

Austerity as a substitute for trust

Here is a common view, not incorrect as far as it goes:

Struggling euro-zone economies like Greece, Portugal, Spain and Italy cannot cut their way back to growth. Demanding rigid austerity from them as the price of European support has lengthened and deepened their recessions. It has made their debts harder, not easier, to pay off.

And here is a useful Paul Krugman post on austerity, perhaps the best single (brief) statement of his views on European austerity. Three observations:

1. I have yet to see a numerical analysis of European fiscal austerity which adjusts for a) falling ngdp, b) the collapse of their banking systems, c) and the collapse of M3 and money markets in some of these regions, noting that in Italy there are partial (very recent) signs of a money market turnaround. The blame gets pinned on the fiscal austerity.

2. I have yet to see a numerical analysis of European fiscal austerity which considers the prospect of later catch-up growth. This can make the costs of austerity much smaller, though of course from discount rates and habit formation there is still a cost.

3. Ideally it really would be better to say “Italy, I trust you to cut spending later, after your economy has recovered.” This cross-national trust is not present, least of all with Greece but also elsewhere. What is the best available policy in the absence of this trust, knowing that the periphery nations have to send some kind of credible signal to the wealthier nations of the North, in return for ongoing aid?

You can think of those three points as the “frontier reasons” why not all economists agree on European austerity. There are indeed some “dY/dG denialists,” but there are too many attacks on them and not enough explorations of the real issues.

Ironically, postponing austerity is most likely to succeed when there is lots of trust in a country (and in fact whether or not that trust is deserved). You can imagine the Swedes agreeing to themselves “we’ll cut spending three years from now” but the Greeks not, not without external constraint. Thus, writers who unmask the depravity of the American polity, and who polarize opinion, are oddly enough doing harm to the anti-austerity point of view.

You will find an alternative perspective on intellectual strategy here.

Assorted links

Books in my pile, real or virtual

1. The Economists’ Voice: Top Economists Take On Today’s Problems, edited by Stiglitz, Edlin, and DeLong, useful excerpts from the journal.

2. Noam Scheiber, The Escape Artists: How Obama’s Team Fumbled the Recovery. I enjoyed reading this book very much, though I am not the one to judge its account of “inside baseball.” There is plenty on Geithner and Summers. Here is Warsh on Scheiber on Summers.

3. Matthew D. Adler, Well-Being and Fair Distribution: Beyond Cost-Benefit Analysis. A detailed examination and defense of social welfare functions, which I have not read.

4. Tyler Cowen, Crie sua Própria Economia, in Brazilian, reviews and the like are here.

5. Alan Beattie, illustrious FT correspondent, Who’s in Charge Here?: How Governments are Failing the World Economy, eBook only, due out in March.

Why is there a shortage of talent in IT sectors and the like?

There have been some good posts on this lately, for instance asking why the wage simply doesn’t clear the market, why don’t firms train more workers, and so on (my apologies as I have lost track of those posts, so no links). The excellent Isaac Sorkin emails me with a link to this paper, Superstars and Mediocrities: Market Failures in the Discovery of Talent (pdf), by Marko Terviö, here is the abstract:

A basic problem facing most labor markets is that workers can neither commit to long-term wage contracts nor can they self fi nance the costs of production. I study the effects of these imperfections when talent is industry-specifi c, it can only be revealed on the job, and once learned becomes public information. I show that fi rms bid excessively for the pool of incumbent workers at the expense of trying out new talent. The workforce is then plagued with an unfavorable selection of individuals: there are too many mediocre workers, whose talent is not high enough to justify them crowding out novice workers with lower expected talent but with more upside potential. The result is an inefficiently low level of output coupled with higher wages for known high talents. This problem is most severe where information about talent is initially very imprecise and the complementary costs of production are high. I argue that high incomes in professions such as entertainment, management, and entrepreneurship, may be explained by the nature of the talent revelation process, rather than by an underlying scarcity of talent.

This result relates also to J.C.’s query about talent sorting, the signaling model of education, CEO pay, and many other results under recent discussion. If it matters to you, this paper was published in the Review of Economic Studies. I’m not sure that a theorist would consider this a “theory paper” but to me it is, and it is one of the most interesting theory papers I have seen in years.

Why doesn’t the right-wing favor looser monetary policy?

Reading Scott’s post induced me to write down these few points. I have noticed that right-wing public intellectuals are skeptical of more expansionary monetary policy for a few reasons:

1. There is a widespread belief that inflation helped cause the initial mess (not to mention centuries of other macroeconomic problems, plus the problems from the 1970s, plus the collapse of Zimbabwe), and that therefore inflation cannot be part of a preferred solution. It feels like a move in the wrong direction, and like an affiliation with ideas that are dangerous. I recall being fourteen years of age, being lectured about Andrew Dickson White’s work on assignats in Revolutionary France, and being bored because I already had heard the story.

2. There is a widespread belief that we have beat a lot of problems by “getting tough” with them. Reagan got tough with the Soviet Union, soon enough we need to get tough with government spending, and perhaps therefore we also need to be “tough on inflation.” The “turning on the spigot” metaphor feels like a move in the wrong direction. Tough guys turn off spigots.

3. There is a widespread belief that central bank discretion always will be abused (by no means is this view totally implausible). “Expansionary” monetary policy feels “more discretionary” than does “tight” monetary policy. Run those two words through your mind: “expansionary,” and “tight.” Which one sounds and feels more like “discretion”? To ask such a question is to answer it.

Within these frameworks of beliefs, expansionary monetary policy just doesn’t feel right. Yet I still agree with the arguments of Scott (and others) that it would have been the right thing to do.

What are the costs of signaling at a macro level?

There is a new paper from Ricardo Perez Truglia, from Harvard, on this topic. It strikes me as quite speculative, but nonetheless a step forward in addressing a very difficult question and adding some structure to the analysis of a very difficult problem. Here are his conclusions:

The goal of the paper is to provide a quantitative idea of the practical importance of conspicuous consumption. We estimated a signaling model using nationally representative data on consumption in the US, which we then use to estimate welfare implications and perform counterfactual analysis. We found that the market value of NMGs [TC: non market goods, as result from the signal] is non-negligible: for each dollar spent in clothing and cars the average household gets around 35 cents of net bene ts from NMGs. However, the large value of NMGs does not imply that the losses from the positional externality are also large. The results suggest that richer household would still consume relatively more of the NMG even in absence of NMGs, so the cost of the signal that they send is not very high. As a result, the signaling equilibrium attains almost 90% of the full potential bene ts from the NMGs, which is very e fficient. The unattained benefi ts, $32 per household per month, can serve as an intuitive upper bound to the bene fits that can be gained through economic policy, such as a tax on observable goods aimed at correcting the positional externality.

A related point is that if utility functions evolve so that people enjoy the very act of sending the signal, that too will lower the associated deadweight loss from signaling.

Here is the author’s home page.

Assorted links

2. Markets in everything, honey trap edition, or should they call it something else?

3. Do hedge fund returns have lower volatility?

4. The still-underrated Dylan Matthews covers MMT, graphic here.

5. Remarkable Swedish rescue, but of what?

Test-tube hamburger is on its way

The world’s first test-tube hamburger, created in a Dutch laboratory by growing muscle fibres from bovine stem cells, will be ready to grill in October.

“I am planning to ask Heston Blumenthal [the celebrity chef] to cook it,” Mark Post, leader of the artificial meat project at Maastricht University, said at the American Association for the Advancement of Science annual meeting in Vancouver.

The story is here. Both Alex and I have blogged about comparable (but less successful) projects in the past. Here is a longer article on the same development.

The most interesting man in the world?

At 9, he settled a dispute with a pistol. At 13, he lit out for the Amazon jungle.

At 20, he attempted suicide-by-jaguar. Afterward he was apprenticed to a pirate. To please his mother, who did not take kindly to his being a pirate, he briefly managed a mink farm, one of the few truly dull entries on his otherwise crackling résumé, which lately included a career as a professional gambler.

From the NYTimes obit of John Fairfax and oh did I mention he rowed across the Atlantic…and the Pacific.

Congress gets two right

In a rare display of function, Congress extended the payroll tax cut and in the same deal they arranged to sell more spectrum, both good ideas and ones that I have argued for extensively. Frankly, I am pleased but surprised. Any inside knowledge on how this was accomplished?

J.C. Bradbury emails me on the allocation of talent

I hope you are doing well. I have a Micro III question that I thought might interest you. I often have such Tyler questions, but keep them to myself, yet this morning I decided to share with you.

What does Jeremy Lin tell us about talent evaluation mechanisms? This article ( http://www.wired.com/wiredscience/2012/02/what-jeremy-lin-teaches-us-about-talent/?utm_source=dlvr.it&utm_medium=twitter ) argues that the standard benchmarks for evaluating basketball and football players at the draft level are flawed. The argument is that Jeremy Lin couldn’t get the opportunity to succeed because his skill wasn’t being picked up by the standard sorting procedure. This got me thinking. Baseball sorts players in a different way than basketball. In professional basketball (and football), college sports serve as minor leagues, where teams face a high variance in competition (the difference between the best and worst teams in a top conference is normally quite large), with very little room for promotion. There is some transferring as players succeed and fail at lower and higher levels, but for the most part you sink or swim at your initial college. This is compounded by the fact that the initial allocation of players to college teams is governed by a non-pecuniary rewards structure with a stringent wage ceiling, which likely hinders the allocation of talent. At the end of your college career, NBA teams make virtually all-or-nothing calls on a few players to fill vacancies at the major-league level. In baseball it’s different. Players play their way up the ladder, and even players who are undrafted can play their way onto teams at low levels of the minor league. At such low levels, the high variance in talent is high like it is in college sports; however, promotions from short-season leagues through Triple-A, allow incremental testing of talent along the way without much risk. I have looked at metrics for predicting major-league success from minor-league performance and found that it is not until you reach the High-A level (that is three steps below the majors) can performance tell you anything. Players in High-A who are on-track for the majors are about-the age of college seniors. Performance statistics from Low-A and below have no predictive power. Baseball is also much less of a team game than basketball, so this should make evaluation easier in baseball but it is still quite difficult by the time most players would be finishing college careers. Also, a baseball scout acquaintance, who is very well versed in statistics, tells me that standard baseball performance metrics in college games are virtually useless predictors of performance (this is contrary to an argument made in Moneyball). Even successful college baseball players almost always have to play their way onto the team.

Back to Lin. He played in the Ivy League and his stats weren’t all that bad or impressive in an environment that is far below the NBA. If Lin is a legitimate NBA player, he didn’t have many opportunities to play his way up like a baseball player does. In the NBA, he experienced drastic team switches, and even when making a team he received limited opportunities to play. MLB teams often keep superior talent in the minors so that they can get practice and be evaluated through in-game competition. An important sorting mechanism for labor market sorting is real-time work. Regardless of your school pedigree, most prestige professions (lawyers, financial managers, professors, etc.) have up-or-out rules after a period of probationary employment where skill is evaluated in real world action. Yes, there is a D-League and European basketball, but the D-league is not as developed as baseball’s minor-league system, and European basketball has high entry cost and may suffer from the same evaluation problems faced by the NBA. Thus, I wonder if the de facto college minor-league systems of basketball and football hinder the sorting of talent so that the Jeremy Lins and Kurt Warners of the world often don’t survive. Thus, another downside of these college sports monopsonies is an inferior allocation of talent at the next level.

J.C.’s points of course apply (with modifications) to economics, to economies, and to our understanding of meritocracy, not to mention to how books, movies, and music fare in the marketplace. Overall I would prefer to see economics devote much more attention to the topic of the allocation of talent.

Here is J.C. on Twitter, here are his books.

Political markets in everything

Forgive the music at the link, from Lucknow:

Your vote would not only change the fate of Uttar Pradesh, but it could also fetch extra marks for your child. In a unique first, many schools in the city have decided to award extra marks to students whose parents will cast vote in the assembly election.

And there is this:

The incentive would not be limited to exams alone, it would also find a mention in the character certificate of a student. Mishra suggested that a column for marking whether or not the child successfully convinced his/her parents to vote and hence displayed a sense of civic consciousness will be added in the report card. In case of a student is of 18 years then the relevant entry will be a mark on his/her own performance on the election day.

For the pointer I thank Sharath Rao.

What good are hedge funds?

How can they beat the market consistently, especially if we take EMH seriously at all? And if they don’t beat the market, how is 2-20 to be justified? Here is a snippet from an interesting Amazon review:

…this kind of comparison misses the entire point of most hedge funds. A market-neutral fund is not designed as a stand-alone investment, but as a diversifier for an equity portfolio. It can have half the return of equities with the same volatility, and still be valuable. The question isn’t whether putting 100% of your money in hedge funds did better than putting 100% in stocks, it’s what portion of assets an investor should allocate to hedge funds. Using the author’s own numbers, an investor would have done best to have 30% of assets in hedge funds, rebalancing annually, from 1998 to 2010. That produced 4.2% annual alpha (return in excess of what you could have gotten investing in stock index funds and t-bills with the same volatility). That number is certainly overstated, hedge fund investors typically do worse than the index suggests, but it demonstrates that you can’t consider only stand-alone returns. This point is borne out by the finding that endowments and pension funds that make use of hedge funds have consistently better risk-adjusted performance than those that do not.

The review, by Aaron C. Brown, offers other points of interest. I’ve ordered the underlying asset itself (the book) and I will report back on it. It was reviewed in today’s FT, still no permalink.

Assorted links

1. Measuring the output gap, an excellent post looking at capacity utilitzation and changes in inflation rates to back out an answer to this question. The bottom line is that the output gap probably isn’t nearly as large as is often claimed. And Karl Smith comments, I would note the connection between the ppf and trust.

2. Obama’s hardline turn against medical marijuana.

3. Markets between everything and everyone, and Literary Saloon reviews Allan Meltzer.

4. Testing Milton Friedman, new TV show with Caplan, Yglesias, Dalmia, Williams, others.