The Rising Cost of Child and Pet Day Care

Everyone talks about the soaring cost of child care (e.g. here, here and here), but have you looked at the soaring cost of pet care? On a recent trip, it cost me about $82 per day to board my dog (a bit less with multi-day discounts). And no, that is not high for northern VA and that price does not include any fancy options or treats! Doggie boarding costs about about the same as staying in a Motel 6.

Many explanations have been offered for rising child care costs. The Institute for Family Studies, for example, shows that prices rise with regulations like “group sizes, child-to-staff ratios, required annual training hours, and minimum educational requirements for teachers and center directors.” I don’t deny that regulation raises prices—places with more regulation have higher costs—but I don’t think that explains the slow, steady price increase over time. As with health care and education, the better explanation is the Baumol effect, as I argued in my book (with Helland) Why Are the Prices So Damn High?

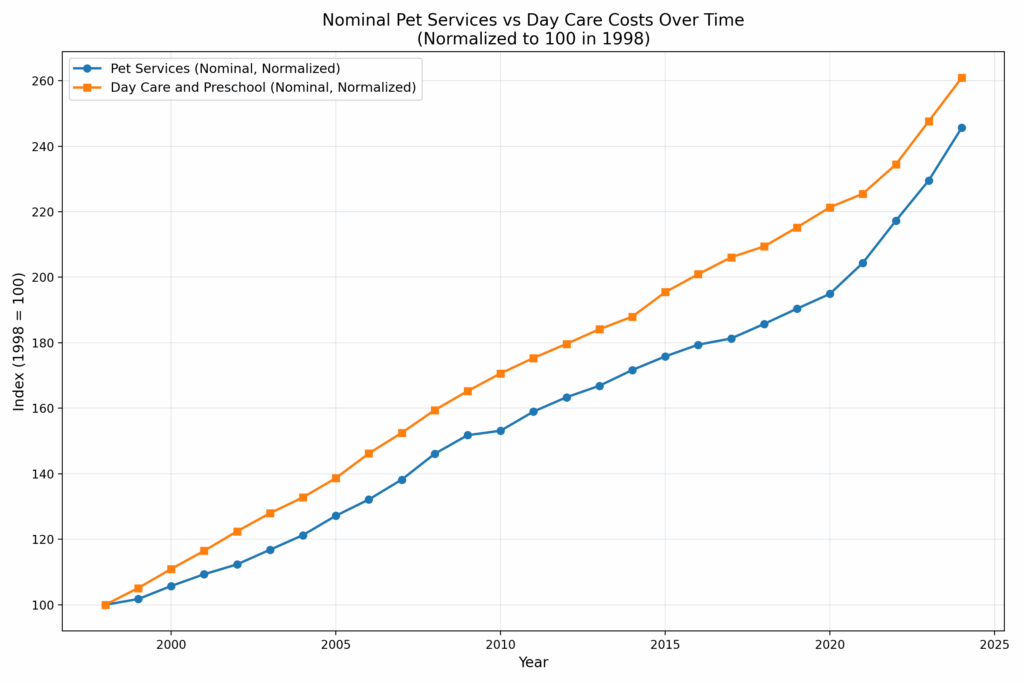

Pet care is less regulated than child care, but it too is subject to the Baumol effect. So how do price trends compare? Are they radically different or surprisingly similar? Here are the two raw price trends for pet services (CUUR0000SS62053) and for (child) Day care and preschool (CUUR0000SEEB03). Pet services covers boarding, daycare, pet sitting, walking, obedience training, grooming but veterinary care is excluded from this series so it is comparable to that for child care.

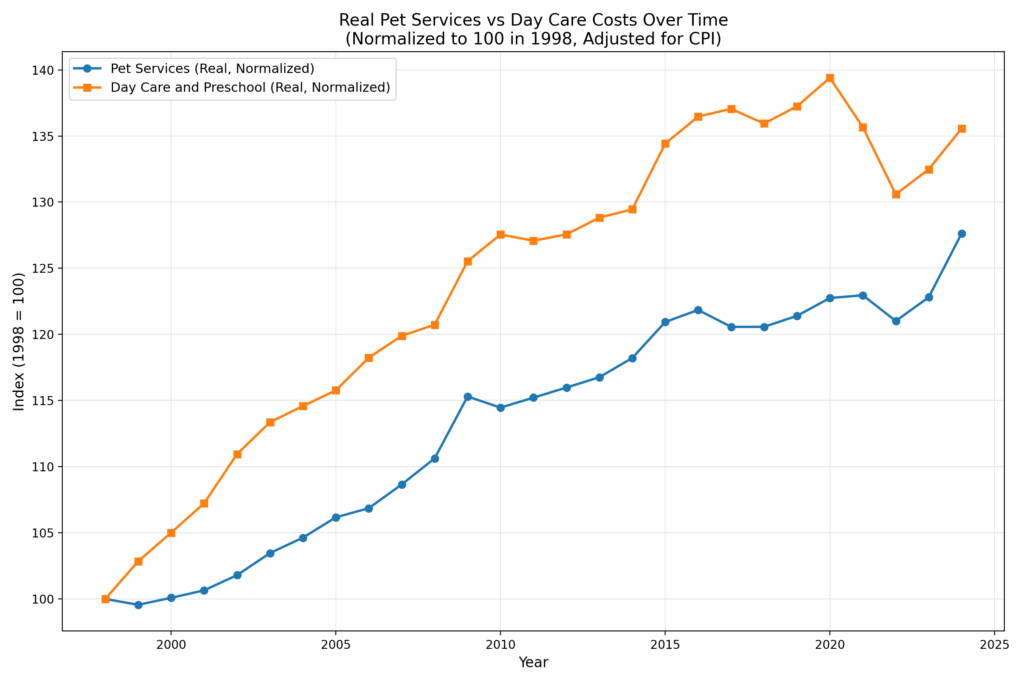

As you can see, the trends are nearly identical, with child care rising only slightly faster than pet care over the past 26 years. Of course, both trends include general inflation, which visually narrows the gap. When we normalize to the overall CPI, we get the following:

Over 26 years, the real (relative) price of Day Care and Preschool has increased 36%, while Pet Services have risen 28%. If regulation doesn’t explain the rise in pet care costs–and it probably doesn’t–then regulation probably doesn’t explain the rise in child care costs either. After all, child and pet care are very similar goods!

The similar rise in the price of child day care and pet day care/boarding is consistent with Is American Pet Health Care (Also) Uniquely Inefficient? by Einav, Finkelstein and Gupta, who find that spending on veterinary care is rising at about the same rate as spending on human health care. Since the regulatory systems of pet and human health care are very different this suggests that the fundamental reason for rising health care isn’t regulation but rising relative prices and increasing incomes (fyi this is also an important reason why Americans spend more on health care than Europeans).

Thus, my explanation for rising prices in child care and pet care is that productivity is increasing in other industries more than in the care industries which means that over time we must give up more of other goods to get child and pet care. In short, if productivity in other sectors rises while child/pet care productivity stays flat, relative prices must rise. Another way to put this is that to retain workers, wages in stagnant-productivity sectors must rise to match those in (equally labor-skilled) high-productivity sectors. That means paying more for the same level of care, simply to keep the labor force from leaving

But rising productivity in other sectors is good! Thus, I always refer to the Baumol effect rather than the “cost disease” because higher prices are not bad when they reflect changes in relative prices. As with education and health care the rising price of child and pet care isn’t a problem for society as whole. We are richer and can afford more of all goods. It can be a problem, however, for people who consume more than the average quantities of the service-sector goods and people who have lower than average wage gains. So what can we do? Redistribution is one possibility.

If we focus on the prices, the core problem is that care work is labor-intensive and labor has a high opportunity cost. One solution is to lower the opportunity cost of that labor. Low-skill immigration helps: when lower-wage workers take on support roles, higher-wage workers can focus on higher-value tasks. As I’ve put it, “The immigrant who mows the lawn of the nuclear physicist indirectly helps to unlock the secrets of the universe.” Same for the immigrant who provides boarding for the pets of the nuclear physicist.

Another solution is capital substitution—automation, AI, better tools. But care jobs resist mechanization; that’s part of why productivity growth is so slow in these sectors. Still, the basic truth remains: if we want more affordable day care—for kids or pets—we need to use less of what’s expensive: skilled labor. That means either importing more people to do the work, or investing harder in ways to do it with fewer hands.

Horseshoe Theory: Trump and the Progressive Left

Many of Trump’s signature policies overlap with those of the American progressive left—e.g. tariffs, economic nationalism, immigration restrictions, deep distrust of elite institutions, and an eagerness to use the power of the state. Trump governs less like Reagan, more like Perón. As Ryan Bourne notes, this ideological convergence has led many on the progressive left to remain silent or even tacitly support Trump policies, particularly on trade.

“[P]rogressive Democrats like Senator Elizabeth Warren have chosen to shift blame for Trump’s tariff-driven price hikes onto large businesses. Last week, they dusted off—and expanded—their pandemic-era Price Gouging Prevention Act. While bemoaning Trump’s ‘chaotic’ on-off tariffs, their real ire remains reserved for ‘greedy corporations,’ supposedly exploiting trade policy disruption to pad prices beyond what’s needed to ‘cover any cost increases.’

…The Democrats’ 2025 gouging bill is broader than ever, creating a standing prohibition against ‘grossly excessive’ price hikes—loosely suggested at anything 20 percent above the previous six-month average—but allowing the FTC to pick its price caps ‘using any metric it deems appropriate.’

…Instead of owning the pricing fallout from his trade wars, President Trump can now point to Democratic cries of ‘corporate greed’ and claim their proposed FTC crackdown proves that it’s businesses—not his tariffs—to blame for higher prices.

If these progressives have their way, the public debate flips from ‘tariffs raise prices’ to ‘the FTC must crack down on corporate greed exploiting trade policy reform,’ with Trump slipping off the hook.”

Trump’s political coalition isn’t policy-driven. It’s built on anger, grievance, and zero-sum thinking. With minor tweaks, there is no reason why such a coalition could not become even more leftist. Consider the grotesque canonization of Luigi Mangione, the (alleged) murderer of UnitedHealthcare CEO Brian Thompson. We already have a proposed CA ballot initiative named the Luigi Mangione Access to Health Care Act, a Luigi Mangione musical and comparisons of Mangione to Jesus. The anger is very Trumpian.

A substantial share of voters on the left and the right increasingly believe that markets are rigged, globalism is suspect, and corporations are the real enemy. Trump adds nationalist flavor; progressives bring the regulatory hammer. The convergence of left and right in attacking classical liberalism– open markets, limited government, pluralism and the basic rules of democratic compromise–is what worries me the most about contemporary politics.

Gross(ery) Confusion

Zephyr Teachout’s NYTs op-ed on grocery store prices is poorly argued.

The food system in the United States is rigged in favor of big retailers and suppliers in several ways. Big retailers often flex their muscles to demand special deals; to make up the difference, suppliers then charge the smaller stores more.

Let’s be clear about what is actually going on. Costco offers its suppliers lower prices in return for bigger orders. There is nothing anti-competitive about volume discounting. Moreover, are firms dismayed or are they eager to sell to big, bad Costco? Google AI gives a good answer:

…firms are eager to sell to Costco because of the immense potential for sales and brand exposure, but they must be prepared to meet stringent requirements, negotiate competitive pricing, and be able to handle high volume and demanding logistics.

Would Americans be better off without Costco? Doubtful given that more than one-quarter of all Americans pay for a Costco membership (either individually or as a family).

Teachout’s idea that suppliers “make up the difference” by charging smaller stores more is also economically incoherent. Profit-maximizing firms already charge what the market will bear. If Costco’s volume justifies a discount, that doesn’t mean suppliers can or should charge higher prices to other buyers. Yes, there are models where costs change with volume but costs could go down with volume and, in any case, those models don’t rely on the folk theory of “making up the difference.”

That’s one of the subtler mistakes. Here’s a more glaring one:

Consider eggs. At the independent supermarket near my apartment, the price for a dozen white eggs last week was $5.99. At a major national retailer a few blocks away, it was $3.99. (For an identical box of cereal, the price difference was $3.) Any number of factors may contribute to a given price, but market power is a particularly consequential one.

Read that again: the firm allegedly abusing market power is the one charging less.

It gets stranger:

New York City has a strong price gouging law on the books, which forbids anyone — suppliers and retailers — from jacking up prices during a state of emergency unless the seller’s own costs have gone up accordingly. The city couldn’t have stopped the bird flu that devastated flocks, but maybe it can stop suppliers from cynically exploiting a crisis to justify exorbitant prices.

This makes two errors. First, she acknowledges it’s not gouging if costs rise—then cites egg prices rising due to the bird flu devastating flocks. That’s literally a textbook case of a supply shock. Maybe some firms exploited the crisis—but eggs rising in price after millions of chickens are killed is the best example you’ve got???

Second, within the span of a few paragraphs, the op-ed veers from claiming large retailers charge prices that are unfairly low to blaming them for charging prices that are too high. I’m surprised she didn’t go for the trifecta and accuse them of colluding to charge the same price.

AIs and Spontaneous Order

Tupy and Boettke in the WSJ on AI and the economy:

The belief that AI can achieve comparable results to free markets, let alone surpass them, reflects a misplaced confidence in computation and a misunderstanding of the price system. The problem for the would-be AI planners is that prices don’t exist like facts about the physical world for a computer to collect and process. They arise from competitive bidding over scarce resources and are inseparable from real market exchanges. Moreover, prices aren’t fixed inputs to be assumed in advance. They are continually being discovered and formed by entrepreneurs testing ideas about future consumer wants and resource constraints.

Economic models that treat prices as given overlook the entrepreneurial actions that create them in the first place. Ludwig von Mises made this point in 1920: Without real market exchange, central planners lack meaningful prices for capital goods. Consequently, they can’t calculate whether directing steel to railways rather than hospitals adds or destroys value.

I would another point. We are not going to have one AI to rule us all. Instead, there are going to be millions of agents who themselves will be participants in the market process. The buying and selling of the AI agents will contribute to the formation of prices but for all the Hayekian reasons that process will not be capable of being predicted.

As I said 7 years ago on Quora:

AIs will themselves be part of the economy. Firms and individuals use AIs to make decisions. Thus, any AI has to take into account the decisions of other AIs. But no AI is going to be so far advanced beyond other AIs that this will be possible. In other words, as AIs increase in power so does the complexity of the economy.

The problem of perfectly organizing an economy does not become easier with greater computing power precisely because greater computing power also makes the economy more complex.

This isn’t to say AI won’t help improve economic policy—it might, if we listen. But the future economy won’t look like a centrally planned machine. It will look like an economy of von Neumanns—autonomous agents buying, selling, and strategizing in complex interaction.

Shorting Your Rivals: A Radical Antitrust Remedy

Conventional antitrust enforcement tries to prevent harmful mergers by blocking them but empirical evidence shows that rival stock prices often rise when a merger is blocked—suggesting that many blocked mergers would have increased competition. In other words, we may be stopping the wrong mergers.

In a clever proposal, Ayres, Hemphill, and Wickelgren (2024) argue that requiring merging firms to short the stock of a close competitor would powerfully realign incentives.

Suppose firms A and B want to merge. Regulators allow the merger on one condition: A-B must take a sizable short position in firm C, a direct competitor. If the merger is anti-competitive and leads to higher industry prices, C’s profits and stock price rise, and A-B takes a financial hit. But if the merger is pro-competitive and drives prices down, C’s stock falls and A-B profits.

A short creates two desirable effects:

- Selection Effect: Only those mergers that are expected to lower prices (and hurt rivals) are financially attractive to the merging parties.

- Incentive Effect: Post-merger, A-B has less incentive to raise prices because doing so boosts C’s stock price, triggering losses on the short.

The short isn’t perfect. Markets might be too shallow, or the rival’s stock could rise for unrelated reasons which imposes extra risk. The authors suggest fixes: instead of a short, require the firm to write Margrabe-style call option. These options have strike prices which float relative to another asset, for example a market or industry price. In this case, A-B would be penalized not if the market as a whole rose but only if the rival outperforms the market.

But the cleanest solution doesn’t require financial instruments at all. Just tie executive pay to relative performance—make the A-B CEO’s bonus depend on beating C’s performance. This is good for shareholders, aligns incentives even in private markets, and doesn’t require making big public bets.

Shorting your rivals sounds strange. But it’s a clever way to force firms to reveal whether their merger helps consumers—or just themselves. Or as I like to say, a bet is a tax on bullshit.

Hat tip: Kevin Lewis.

Addendum: See also this earlier paper, Incentive Contracts as Merger Remedies by Werden, Froeb and Tschantz.

The Sputnik vs. Deep Seek Moment: The Answers

In The Sputnik vs. DeepSeek Moment I pointed out that the US response to Sputnik was fierce competition. Following Sputnik, we increased funding for education, especially math, science and foreign languages, organizations like ARPA were spun up, federal funding for R&D was increased, immigration rules were loosened, foreign talent was attracted and tariff barriers continued to fall. In contrast, the response to what I called the “DeepSeek” moment has been nearly the opposite. Why did Sputnik spark investment while DeepSeek sparks retrenchment? I examine four explanations from the comments and argue that the rise of zero-sum thinking best fits the data.

Several comments fixated on DeepSeek itself, dismissing it as neither impressive nor threatening. Perhaps but DeepSeek was merely a symbol for China’s broader rise: the world’s largest exporter, manufacturer, electricity producer, and military by headcount. These critiques missed the point.

Some commenters argued that Sputnik provoked a strong response because it was seen as an existential threat, while DeepSeek—and by extension China—is not. I certainly hope China’s rise isn’t existential, and I’m encouraged that China lacks the Soviet Union’s revolutionary zeal. As I’ve said, a richer China offers benefits to the United States.

But many influential voices do view China as a very serious, even existential, threat—and unlike the USSR, China is economically formidable.

More to the point, perceived existential stakes don’t answer my question. If the threat were greater, would we suddenly liberalize immigration, expand trade, and fund universities? Unlikely. A more plausible scenario is that if the threat were greater, we would restrict harder—more tariffs, less immigration, more internal conflict.

Several commenters, including my colleague Garett Jones, pointed to demographics—especially voter demographics. The median age has risen from 30 in 1950 to 39 in recent years; today’s older, wealthier, more diverse electorate may be more risk-averse and inward-looking. There’s something to this, but it’s not sufficient. Changes in the X variables haven’t been enough to explain the change in response given constant Betas so demography doesn’t push that far but does it even push in the right direction?

Age might correlate with risk-aversion, for example, but the Trump coalition isn’t risk-averse—it’s angry and disruptive, pushing through bold and often rash policy changes.

A related explanation is that the U.S. state has far less fiscal and political slack today than it did in 1957. As I argued in Launching, we’ve become a warfare–welfare state—possibly at the expense of being an innovation state. Fiscal constraints are real, but the deeper issue is changing preferences. It’s not that we want to return to the moon and can’t—it’s that we’ve stopped wanting to go.

In my view, the best explanation for the starkly different responses to the Sputnik and DeepSeek moments is the rise of zero-sum thinking—the belief that one group’s gain must come at another’s expense. Chinoy, Nunn, Sequiera and Stantcheva show that the zero sum mindset has grown markedly in the U.S. and maps directly onto key policy attitudes.

Zero sum thinking fuels support for trade protection: if other countries gain, we must be losing. It drives opposition to immigration: if immigrants benefit, natives must suffer. And it even helps explain hostility toward universities and the desire to cut science funding. For the zero-sum thinker, there’s no such thing as a public good or even a shared national interest—only “us” versus “them.” In this framework, funding top universities isn’t investing in cancer research; it’s enriching elites at everyone else’s expense. Any claim to broader benefit is seen as a smokescreen for redistributing status, power, and money to “them.”

Zero-sum thinking doesn’t just explain the response to China; it’s also amplified by the China threat. (hence in direct opposition to some of the above theories, the people who most push the idea that the China threat is existential are the ones who are most pushing the zero sum response). Davidai and Tepper summarize:

People often exhibit zero-sum beliefs when they feel threatened, such as when they think that their (or their group’s) resources are at risk…Similarly, working under assertive leaders (versus approachable and likeable leaders) causally increases domain-specific zero-sum beliefs about success….. General zero-sum beliefs are more prevalent among people who see social interactions as a competition and among people who possess personality traits associated with high threat susceptibility, such as low agreeableness and high psychopathy, narcissism and Machiavellianism.

Zero-sum thinking can also explain the anger we see in the United States:

At the intrapersonal level, greater endorsement of general zero-sum beliefs is associated with more negative (and less positive) affect, more greed and lower life satisfaction. In addition, people with general zero-sum beliefs tend to be overly cynical, see society as unjust, distrust their fellow citizens and societal institutions, espouse more populist attitudes, and disengage from potentially beneficial interactions.

…Together, these findings suggest a clear association between both types of zero-sum belief and well-being.

Focusing on zero-sum thinking gives us a different perspective on some of the demographic issues. In the United States, for example, the young are more zero-sum thinkers than the old and immigrants tend to be less zero-sum thinkers than natives. The likeliest reason: those who’ve experienced growth understand that everyone can get a larger slice from a growing pie while those who have experienced stagnation conclude that it’s us or them.

The looming danger is thus the zero-sum trap: the more people believe that wealth, status, and well-being are zero-sum, the more they back policies that make the world zero-sum. Restricting trade, blocking immigration, and slashing science funding don’t grow the pie. Zero-sum thinking leads to zero-sum policies, which produce zero-sum outcomes—making the zero sum worldview a self-fulfilling prophecy.

Tariff Shenanigans

In our textbook, Tyler and I give an amusing example of how entrepreneurs circumvented U.S. tariffs and quotas on sugar. Sugar could be cheaply imported into Canada and iced tea faced low tariffs when imported from Canada into the U.S., so firms created a high-sugar iced “tea” that was then imported into the US and filtered for its sugar!

Bloomberg reports a similar modern workaround. Delta needs new airplanes but now faces steep tariffs on imported European aircraft. As a result, Delta has been stripping European planes of their engines, importing the engines at low tariff rates, and installing them on older aircraft.

Blame Canada! Measles Edition

Polimath has a good post on measles. The recent spike in U.S. cases has drawn alarm. As the New York Times reports:

There have now been more measles cases in 2025 than in any other year since the contagious virus was declared eliminated in the United States in 2000, according to new data released Wednesday by the Centers for Disease Control and Prevention.

The grim milestone represents an alarming setback for the country’s public health and heightens concerns that if childhood vaccination rates do not improve, deadly outbreaks of measles — once considered a disease of the past — will become the new normal.

But as Polimath notes, U.S. vaccination rates remain above 90% nationally. The problem isn’t broad domestic anti-vax sentiment but rather concentrated gaps in coverage, often within insular religious communities. These local shortfalls do explain how outbreaks spread once they begin—but how do they begin in the first place, given these communities are islands within a largely vaccinated country? Polimath says blame Canada! (and Mexico!)

The greater concern in my mind is not the problem of low measles vaccination coverage in the United States, but among our immediate neighbors. In Ontario, the MMR vaccination rate among 7-year-olds is under 70%. As in the examples above, this rate seems to be particularly low “in specific communities”, whatever that is supposed to mean. This has resulted in the ongoing spread of measles such that Ontario’s measles infection rate is 40 times higher than the United States. Canada officially “eliminated” measles in 1998. But with vaccine rates as low as they are, it seems like Canada is at risk for losing that “elimination” status and becoming an international source for measles.

Similarly, Mexico is having a measles outbreak that is substantially worse than the US outbreak. Importantly, the Mexican outbreak has been the worst in the Chihuahua province (over 3,000 cases), which borders Texas and New Mexico.

I’m less interested in blame than in the useful reminder that not all politics is American politics. Vaccination rates have dipped worldwide and not in response to U.S. politics or RFK Jr. In fact, despite RFK Jr. the U.S. is doing better than some of its North American and European peers. Outbreaks here may be triggered by cross-border exposure, not failures in U.S. public health alone. Not all politics is American—and not all American outcomes are made in America.

Hat tip: the excellent Stephen Landry.

Technology Transfer and Development Economics

The Sputnik vs. DeepSeek Moment: Why the Difference?

In 1957, the Soviet Union launched Sputnik triggering a national reckoning in the United States. Americans questioned the strength of their education system, scientific capabilities, industrial base—even their national character. The country’s self-image as a global leader was shaken, creating the Sputnik moment.

The response was swift and ambitious. NSF funding tripled in a year and increased by a factor of more than ten by the end of the decade. The National Defense Education Act overhauled universities and created new student loan programs for foreign language students and engineers. High schools redesigned curricula around the “new math.” Homework doubled. NASA and ARPA (later DARPA) were created in 1958. NASA’s budget rocketed upwards to nearly 5% of all federal spending and R&D spending overall increased to well over 10% of federal spending. Immigration rules were liberalized (perhaps not in direct response to Sputnik but as part of the ethos of the time). Foreign talent was attracted. Tariff barriers continued to fall and the US engaged with international organizations and promoted globalization..

{kind=link}

The U.S. answered Sputnik with bold competition not an aggrieved whine that America had been ripped off and abused.

America’s response to rising scientific competition from China—symbolized by DeepSeek’s R1 matching OpenAI’s o1—has been very different. The DeepSeek Moment has been met not with resolve and competition but with anxiety and retreat.

Trump has proposed slashing the NIH budget by nearly 40% and NSF by 56%. The universities have been attacked, creating chaos for scientific funding. International collaboration is being strangled by red tape. Foreign scientists are leaving or staying away. Tariffs have hit highs not seen since the Great Depression and the US has moved away from the international order.

Some of this is new and some of it is an acceleration of already existing trends. In Launching the Innovation Renaissance, for example, I said that by the Federal budget numbers, America is a warfare-welfare state not an innovation state. However, to be fair, there are some bright spots. Market‑driven research might partially offset public cuts. Big‑tech R&D now exceeds $200 billion annually—more than the entire federal government spending on R&D. Not everything we did post-Sputnik was wise nor is everything we are doing today foolish.

Nevertheless, the contrast is stark: Sputnik spurred investment and ambition. America doubled down. DeepSeek has sparked defensiveness and retreat. We appear to be folding.

Question of the hour. Why has America responded so differently to similar challenges? Can understanding that pivot help to reverse it? Show your work.

GAVI’s Ill-Advised Venture Into African Industrial Policy

GAVI, the Vaccine Alliance has saved millions of lives by delivering vaccines to the world’s poorest children at remarkably low cost. It’s frankly grotesque that RFK Jr. cites “safety” as a reason to cut funding—when the result of such cuts will be more children dying from preventable diseases. Own it.

You can find plenty of RFK Jr. criticism elsewhere, however, and GAVI is not above criticism. Thus, precisely because GAVI’s mission is important, I want to focus on a GAVI project that I think is ill-motivated and ill-advised, GAVI’s African Vaccine Manufacturing Accelerator (AVMA).

The motivation behind the AVMA is to “accelerate the expansion of commercially viable vaccine manufacturing in Africa” to overcome “vaccine inequity” as illustrated during the COVID crisis. The problem with this motivation is that most of Africa’s delay in receiving COVID vaccines was driven by funding issues and demand rather than supply. Working with Michael Kremer and others, I spent a lot of time encouraging countries to order vaccines and order early not just to save lives but to save GDP. We were advisors to the World Bank and encouraged them to offer loans but even after the World Bank offered billions in loans there was reluctance to spend big sums. There were supply shortages in 2021 in Africa, as there were elsewhere, but these quickly gave way to demand issues. Doshi et al. (2024) offer an accurate summary:

Several reasons likely account for low coverage with COVID-19 vaccines, including limited political commitment, logistical challenges, low perceived risk of COVID-19 illness, and variation in vaccine confidence and demand (3). Country immunization program capacity varies widely across the African Region. Challenges include weak public health infrastructure, limited number of trained personnel, and lack of sustainable funding to implement vaccination programs, exacerbated by competing priorities, including other disease outbreaks and endemic diseases as well as economic and political instability.

Thus, lack of domestic vaccine production wasn’t the real problem—remember, most developed countries had little or no domestic production either but they did get vaccines relatively quickly. The second flaw in the rationale for the AVMA is its pan-African framing. Africa is a continent, not a country. Why would manufacturing capacity in Senegal serve Kenya better than production in India or Belgium? There’s a peculiar assumption of pan-African solidarity, as if African countries operate with shared interests that go beyond those observed in other countries that share a continent.

Both problems with the rationale for AVMA are illustrated by South Africa’s Aspen pharmaceuticals. Aspen made a deal to manufacture the J&J vaccine in South Africa but then exported doses to Europe. After outrage ensued it was agreed that 90% of the doses would be kept in Africa but Aspen didn’t receive a single order from an African government. Not one.

Now to the more difficult issue of capacity. Africa produces less than .1% of the world’s vaccines today. The African Union has what it acknowledges is an “ambitious goal” to produce over 60 percent of the vaccines needed for Africa’s population locally by 2040. To evaluate the plausibility of this goal do note that this would require multiple Serum‑of‑India‑sized plants.

More generally, vaccines are complex products requiring big up-front investments and long lead times:

Vaccine manufacturing is one of the most demanding in industry. First, it requires setting up production facilities, and acquiring equipment, raw materials, and intellectual property rights. Then, the manufacturer will implement robust manufacturing processes and manage products portfolio during the life cycle. Therefore, manufacturers should dispose of an experienced workforce. Manufacturing a vaccine is costly and takes seven years on average. For instance, it took about 5–10 years to India, China, and Brazil to establish a fully integrated vaccine facility. A longer establishment time can be expected for African countries lacking dedicated expertise and finance. Manufacturing a vaccine can costs several dozens to hundreds of million USD in capital invested depending on the vaccine type and disease indication.

All countries in Africa rank low on the economic complexity index, a measure of whether a country can produce sophisticated and complex products (based on the diversity and complexity of their export basket). But let us suppose that domestic production is stood up. We must still ask, at what price? If domestic manufacturing ends up being more expensive than buying abroad (as GAVI acknowledges is a possibility even with GAVI’s subsidies), will African countries buy “locally” and pay more or will solidarity go out the window?

Finally, even if complex vaccines are produced at a competitive price, we still haven’t solved the demand problem. GAVI again has a rather strange acknowledgment of this issue:

Secondly, adequate country demand is another critical enabler. For AVMA to be successful, African countries will need to buy the vaccines once they appear on the Gavi menu. The Secretariat is committed to ongoing work with the AU and Member States on demand solidarity under Pillar 3 of Gavi’s Manufacturing Strategy.

So to address vaccine inequity, GAVI is investing in local production….but the need to manufacture “demand solidarity” among African governments reveals both the flaw in the premise and the weakness of the plan.

Keep in mind that the WHO only recognizes South Africa and Egypt as capable of regulating the domestic production of vaccines (and Nigeria as capable of regulating vaccine imports). In other words, most African governments do not have regulatory systems capable of evaluating vaccine imports let alone domestic production.

GAVI wants to sell the AVMA as if were an AMC (Advance Market Commitment) but it isn’t. It’s industrial policy. An AMC would offer volume‑and‑price guarantees open to any manufacturer in the world. An AMC with local production constraints is a weighted down AMC, less likely to succeed.

None of this is to imply that GAVI has no role to play. In addition to a true AMC, GAVI could arrange contracts to pay existing global suppliers to maintain idle capacity that can pivot to African‑priority antigens within 100 days. GAVI could possibly also help with regulatory convergence. There is an African Medicines Agency which aims to operate like the EMA but it has only just begun. If the AMA can be geared up, it might speed up vaccine approval through mutual recognition pacts.

The bottom line is that the $1.2 billion committed to AVMA would likely better more lives if it was directed toward GAVI’s traditional strengths in pooled procurement and distribution, mechanisms that have proven successful over the past two decades. Instead, AVMA drags GAVI into African industrial policy. A poor gamble.

The Paradox of India

Tyler often talks about cracking cultural codes. India is the hardest—and therefore the most fascinating—cultural code I’ve encountered. The superb post The Paradox of India by Samir Varma helps to unlock some of these codes. Varma is good at describing:

In 2004, something extraordinary happened that perfectly captured India’s unique nature: A Roman Catholic woman (Sonia Gandhi) voluntarily gave up the Prime Ministership to a Sikh (Manmohan Singh) in a ceremony presided over by a Muslim President (A.P.J. Abdul Kalam) in a Hindu-majority country.

And nobody commented on it.

Think about that. In how many countries could this happen without it being THE story? In India, the headlines focused on economic policy and coalition politics. The religious identities of the key players were barely mentioned because, well, what would be the point? This is how India works.

This wasn’t tolerance—it was something deeper. It was the lived experience of a civilization where your accountant might be Jain, your doctor Parsi, your mechanic Muslim, your teacher Christian, and your vegetable vendor Hindu. Where festival holidays meant everyone got days off for Diwali, Eid, Christmas, Guru Nanak Jayanti, and Good Friday. Where secularism isn’t the absence of religion but the presence of all religions.

But goes beyond that:

You might be thinking: “This is fascinating, but I’m not Indian. I can’t draw on 5,000 years of civilizational memory. How does any of this help me navigate my increasingly polarized world?”

Here’s what I’ve learned from watching India work its magic: The mental moves that make pluralism possible aren’t mystical—they’re learnable. Think of them as cognitive tools:

The And/And Instead of Either/Or: When faced with contradictions, resist the Western urge to resolve them. Can something be both sacred and commercial? Both ancient and modern? Both yours and mine? Indians instinctively answer yes.

Contextual Truth Over Universal Law: What’s right for a Jain isn’t right for a Bengali, and that’s okay. Truth can be plural without being relative. Multiple valid perspectives can coexist without canceling each other out.

Strategic Ambiguity as Wisdom: Not everything needs to be defined, categorized, and resolved. Sometimes the wisest response is a head waggle that means yes, no, and maybe all at once.

Code-Switching as a Life Skill: Indians don’t just switch languages—they switch entire worldviews depending on context. At work, modern. At home, traditional. With friends, fusion. This isn’t hypocrisy; it’s sophisticated social navigation.

The lesson isn’t “be more tolerant.” It’s “develop comfort with unresolved multiplicity.” In a world demanding you pick sides, the Indian model suggests a radical alternative: Don’t.

In our age of rising nationalism and cultural purism, when countries are building walls and communities are retreating into echo chambers, India stands as a glorious, maddening, inspiring mess—proof that diversity isn’t just manageable but might be the secret to civilizational immortality.

After all, it’s hard to kill something that contains multitudes. When one part struggles, another thrives. When one tradition calcifies, another innovates. When one community turns inward, another builds bridges.

It’s not a bug. It’s a feature.

And maybe, just maybe, it’s exactly what the world needs to remember right now.

Read the whole thing. Part 1 of 3.

Trump Accounts are a Big Deal

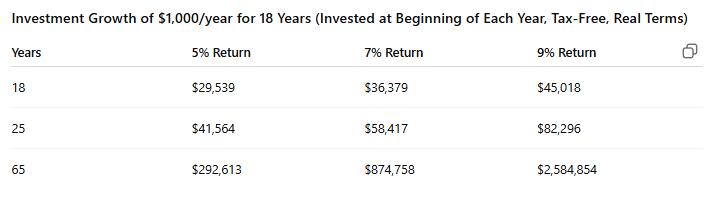

Trump’s One Big Beautiful Bill Act was signed into law on July 4, 2025. It’s so big that many significant features have been little discussed. Trump Accounts are one such feature under which every newborn citizen gets $1000 invested in the stock market. These accounts could radically change social welfare in the United States and be one important step on the way to a UBI or UBWealth. Here are some details:

- Government Contribution: A one-time $1,000 contribution per eligible child, invested in a low-cost, diversified U.S. stock index fund.

- Eligibility: U.S. citizen children born between January 1, 2025, and December 31, 2028 (with a valid Social Security number and at least one parent with a valid Social Security number).

- Employer Contributions: Employers can contribute up to $2,500 annually per employee’s child, and these contributions are excluded from the employee’s gross income for tax purposes. These are subject to the overall $5,000 annual contribution limit (indexed for inflation) per child (which includes parental contributions).

The employer contribution strikes me as important. Suppose that in addition to the initial $1000 government payment that on average $1000 is added per year for 18 years (by a combination of parent and parent employer contributions). Note that this is below the maximum allowed annual contribution of $5000. At a historically reasonable 7% real rate of return these accounts will be worth ~36k at age 18 (when the money can be fully withdrawn), $58k at age 25 and $875k at age 65 subject to uncertainty of course as indicated below.

The $1000 initial payment is available only for newborns but, as I read the text, the parent and employer donations can be made for any child under the age of 18 so this is basically an IRA for children. It’s slightly complicated because if the child or parents put after-tax money into the account that is not taxed at withdrawal (you get your basis back) but everything else is taxed on withdrawal as ordinary income like an IRA. There are approximately 3.5 million citizen births a year so the program will have direct costs of $3.5 billion plus indirect costs from reduced taxes due to the tax-free yearly contribution allowance, which as noted could be quite large as it can go to any child. Thus the program could be quite expensive. On the other hand, it’s clear that the accounts could reduce reliance on social security if held for long periods of time. The $1000 initial contribution is limited to four years but once 14 million kids get them, the demand will be to make them permanent.

Genetic Counseling is Under Hyped

In an excellent interview (YouTube; Apple Podcasts, Spotify) Dwarkesh asked legendary bio-researcher George Church for the most under-hyped bio-technologies. His answer was both surprising and compelling:

What I would say is genetic counseling is underhyped.

What Church means is that gene editing is sexy but for rare diseases carrier screening is cheaper and more effective. In other words, collect data on the genes of two people and let them know if their progeny would have a high chance of having a genetic disease. Depending on when the information is made known, the prospective parents can either date someone else or take extra precautions. Genetic testing now costs on the order of a hundred dollars or less so the technology is cheap. Moreover, it’s proven.

Since the early 1980s the Jewish program Dor Yeshorim and similar efforts have screened prospective partners for Tay-Sachs and other mutations. Before screening, Tay-Sachs struck roughly 1 in 3,600 Jewish births; today births with Tay-Sachs have fallen by about 90 percent in countries that adopted screening programs. As more tests are developed they can be easily integrated into the process. In addition to Tay-Sachs, Dor Yeshorim, for example, currently tests for cystic fibrosis, Bloom syndrome, and spinal muscular atrophy among other diseases. A program in Israel reduced spinal muscular atrophy by 57%. A study for the United States found that a 176 panel test was cost-effective compared to a minimal 5 panel test as did a similar study on a 569 panel test for Australia.

A national program could offer testing for everyone at birth. The results would then be part of one’s medical record and could be optionally uploaded to dating websites. In a world where Match.com filters on hobbies and eye color, why not add genetic compatibility?

Do it for the kids.

Addendum: See also my paper on genetic insurance (blog post here).

Amazon’s Robotic Revolution

Amazon now employs almost as many robots as humans leading to huge productivity improvements. From the second graph, “end-to-end” packages handled by Amazon rose from 175 in 2015 to nearly 4000 in 2025. Incredible. Excellent piece in the WSJ.

Hat tip: Edward Conard.