Category: Economics

Alas, Bob Lucas has passed away

RIP, he was one of the great economists of our time…

Sentences of the Day

The Washington Post on the plan to refurbish Union Station in DC:

The federal environmental review of the project, which began in 2015, is at least three years behind schedule. Once the federal approval process is complete, a design phase is likely to take several years, project officials said, possibly followed by 13 years of construction.

A good example of the Ezra Klein point about the costs of everything bagel liberalism. By the way, the push to eliminate more than a thousand parking spots at the station seems counter-productive. I’m not a fan of parking minimums but in typical liberal fashion that has been turned into an anti-parking, anti-car crusade regardless of context. In fact, a railroad station is precisely where you do want parking to avoid the last mile(s) problem and encourage rail use.

The price of leisure and the demand to work

Fun is cheaper and that matters!:

Recreation prices and hours worked have both fallen over the last century. We construct a macroeconomic model with general preferences that allows for trending recreation prices, wages, and work hours along a balanced-growth path. Estimating the model using aggregate data from OECD countries, we find that the fall in recreation prices can explain a large fraction of the decline in hours. We also use our model to show that the diverging prices of the recreation bundles consumed by different demographic groups can account for much of the increase in leisure inequality observed in the United States over the last decades.

That is from a newly published paper by Alexandr Kopytov, Nikolai Roussanov, and Mathieu Taschereau-Dumouchel. It is in the premiere issue of a new journal Journal of Political Economy Macroeconomics.

More persistence and propagation than you might think?

Macroeconomic cycles are much more self-reinforcing and correspondingly resistant to shocks and hence longer-lasting than what is commonly thought…

The key idea is that economic developments feature strong endogenous propagation mechanisms which yield endogenous cyclical behavior ala limit cycles.

And:

What is at heart of this behavior? There are three factors that the authors point towards. First is strategic complementarity between economic agents’ behavior, such as the fact that firms want to invest when other firms are investing. Second, you need inertia in individual behavior, so that rapid changes in behavior are costly. And finally, you need dependence on some stock variable such as aggregate amount of capital or durable goods. All of these requirements seem very realistic assumption about the real world.

What are the implications of such model? Among other things this means that in certain periods of time the economy is very robust to negative shocks, because these shocks do not have the power to overturn the forces (resulting from the strategic complementarity between agents) that are pushing economic activity higher. They might push us slightly lower for some period of time, but they don’t turn things completely around. And once their effect fades the economy continues in its previous trajectory. In a sense, this view suggests that economic cycles are more like a titanic.

It also means that there is certain dichotomy in terms of shocks. Shocks ranging in size from “small” to “large-but-not-gigantic” proportions do not change the underlying trajectory of the economy, unless we are already close to turning point in the limit cycle. Meanwhile, truly gigantic shocks, like the global financial crisis, are not just deviation from the medium-term trend defined by the limit cycle, but a change in the medium-term trend.

And in conclusion:

To summarize, the limit cycle view suggests that a powerful enough shock, such as the rebound when economies re-opened after the pandemic recession, can put us on a upward spiral, and that such spiral features such a strong self-reinforcing mechanisms that even large negative shocks cannot derail us. This in contrast to standard DSGE models that feature only relatively weak propagation of shocks, and, crucially, do not feature any medium-term cyclical behavior.

Here is much more from Kamil Kovar, a good and important post.

Kevin Bryan on LLMs and GPTs for economic research

Here is the talk. I am waiting for someone to do some background “anthropological” research and field work, and create a fully simulated economy of say a village of five hundred people. (It is not difficult to have LLMs simulate human responses in economic games.) After that, the social sciences will never be the same again.

Substitutes Are Everywhere: The Great German Gas Debate in Retrospect

In March of 2022 a group of top economists released a paper analyzing the economic effects on Germany of a stop in energy imports from Russia (Bachmann et al. 2022). Using a large multi-sector mathematical model the authors concluded that if prices were allowed to adjust, even a substantial shock would have relatively low costs. In contrast, the German chancellor warned that if the Russians stopped selling oil to Germany “entire branches of industry would have to shut down” and when asked about the economic models he argued that:

[the economists] get it wrong! And it’s honestly irresponsible to calculate around with some mathematical models that then don’t really work. I don’t know absolutely anyone in business who doesn’t know for sure that these would be the consequences.

The Chancellor was not alone in predicting big economic losses; some studies estimated reductions in output of 6-12% and millions of unemployed workers. The key distinction between the economists and the others was in their understanding of elasticities of substitution. When the Chancellor and the average person think about a 40% reduction in natural gas supplies, they implicitly assume that each natural gas-dependent industry must cut its usage by 40%. They then consider the resulting decline in output and the cascading effects on downstream industries. It’s easy to get very worried using this framework.

When the economists replied that there were opportunities for substitution they were typically met with disbelief and misunderstanding. The disbelief stemmed from a lack of appreciation of the many opportunities for substitution that permeate an economy. In our textbook, Modern Principles, Tyler and I explain how the OPEC oil shock in the 1970s led to an increase in brick driveways (replacing asphalt) and the expansion of sugar cane plantations in Brazil (for ethanol production). Amazingly, the oil shock also prompted flower growers to move production overseas, as the reduction in heating oil costs from growing in sunnier climates outweighed the increase in transportation fuel expenses. While these examples highlight long-term changes, short-term substitutions are also possible, though their precise details are usually hidden from central planners and economists.

The misunderstanding came from thinking that we need every user of fuel to find substitutes. Not at all! In reality, as fuel prices rise, those with the lowest substitution costs will switch first, freeing up fuel for users who have more difficulty finding alternatives. Just one industry with favorable substitution possibilities, combined with a few moderately adaptable industries, can produce a significant overall effect. Moreover, there are nearly always some industries with viable substitution options. To see why reverse the usual story and ask, if fuel prices fell by 50% could your industry use more fuel? And if fuel prices fell by 50% are their industries that could switch into the now cheaper fuel?

The misunderstanding came from thinking that we need every user of fuel to find substitutes. Not at all! In reality, as fuel prices rise, those with the lowest substitution costs will switch first, freeing up fuel for users who have more difficulty finding alternatives. Just one industry with favorable substitution possibilities, combined with a few moderately adaptable industries, can produce a significant overall effect. Moreover, there are nearly always some industries with viable substitution options. To see why reverse the usual story and ask, if fuel prices fell by 50% could your industry use more fuel? And if fuel prices fell by 50% are their industries that could switch into the now cheaper fuel?

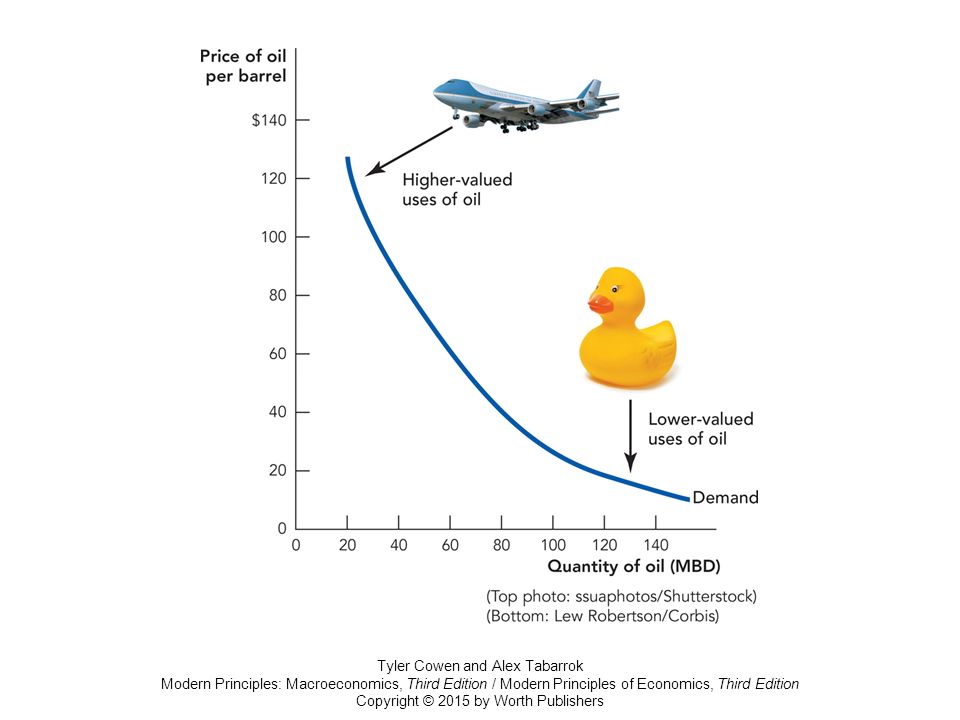

People often find it easier to imagine new uses rather than ways to reduce existing consumption. However, it is typically the new uses that are scaled back first. Tyler and I illustrate this with our jet and rubber ducky graph. Although jet aircraft won’t shift away from oil even at high prices, rubber (actually plastic) duckies, which are made from oil, can find substitutes–wood, for example–when oil prices rise. And if plastic ducky manufacturers cannot find substitutes, they go out of business, freeing up more oil for other uses. In this way, the market identifies the least valuable goods to cease production, another kind of substitution.

Substitution is a more nuanced concept than many people imagine. Here’s another example. Imagine that an economy has an energy-intensive goods producing sector and that there are few substitutes for the fuel used in this sector. Disaster? Not at all. We don’t need a fuel substitute, if we can substitute imports of the energy-intensive goods for domestically produced versions. Storage is also a substitute and notice that the more you substitute away from a fuel in final uses the greater the effective storage. If you use 1 gallon a day a 10 gallon tank lasts 10 days. If you use a quarter gallon a day it lasts 40 days. Everything is connected.

All of these myriad changes happen under the guidance of the invisible hand, i.e. the price system. Remember, a price is a signal wrapped up in an incentive. Thus Bachmann et al. wisely recommended letting energy prices rise to convey the signal and not insuring energy users so the incentive effects were fully felt on the margin.

So what happened? Gas from Russia was indeed cut very substantially but the German economy did not collapse and instead proved as robust as predicted, perhaps even more so. (The Chancellor’s predictions were off the mark but, to be fair, the government also did do a good job in sourcing new supplies and building reserves.) Moll, Schularick, and Zachmann have revisited the analysis and conclude:

The economic outcomes confirm the core theoretical argument that macro elasticities are larger than micro elasticities and that “cascading effects” along the supply chain would be muted as opposed to destroying the economy’s entire industrial sector. As foreseen, producers partly switched to other fuels or fuel suppliers, imported products with high energy content, while households adjusted their consumption patterns….Market economies have a tremendous ability to adapt that was widely underestimated. In addition, the German economics ministry (BMWK) was very successful in quickly sourcing gas supplies from third countries and building LNG capacity. Finally, it probably helped that German policymakers refrained from imposing a price cap on natural gas (like in many other European countries) and instead opted for lumpsum transfers based on households’ and firms’ historical gas consumption.

Hat tip: Alex Wollman.

Stanley Engerman, RIP

Here is one remembrance. I thank several MR readers for the pointer.

Free Insurance for Everyone!

President Biden says “We’re planning to make it mandatory for airlines to compensate travelers with meals, hotels, taxis, and cash, miles, or travel vouchers when your flight is delayed or cancelled because of their mistake.”

A classic example of the Happy Meal Fallacy:

Some restaurants offer burgers without fries and a drink. These restaurants cater to low-income people who enjoy fries and drinks but can’t always afford them. To rectify this sad situation a presidential candidate proposes The Happy Meal Act. Under the Act, burgers must be sold with fries and a drink. “Burgers by themselves are not a complete, nutritious meal,” the politician argues, concluding with the uplifting campaign slogan, “Everyone deserves a Happy Meal!”

But will the Happy Meal Act make people happy? If burgers must come with fries and a drink, restaurants will increase the price of a “burger.” Even though everyone likes fries and a drink they may not like the added benefits by as much as the increase in the price of the meal. Indeed, this must be the case since consumers could have bought the meal before the Act but chose not to. Requiring firms to sell benefits that customers value less than their cost makes both firms and customers worse off.

Almost everyone understands this when it comes to burgers and fries but make it burgers, fries and air miles and some people will think this is a good idea. To recap, requiring firms to sell benefits that customers value less than their cost makes both firms and customers worse off. And if customers value the benefits at more than the cost then that’s a profit opportunity and there is no need for a mandate.

New blog on science and economic growth

By economist Jack Leach, here is the blog. Here is a post on the Greek origins of modern science.

Lessons from the COVID War

In preparation for a National Covid Commission a group of scholars directed by Philip Zelikow (director of the 9/11 Commission) began interviewing people and organizing task forces (I was an interviewee). The Covid Commission didn’t happen, a fact that illustrates part of the problem:

The policy agenda of both major American political parties appear mostly undisturbed by this pandemic. There is no momentum to fix the system….The Covid war revealed a collective national incompetence in governance….One common denominator stands out to us that spans the political spectrum. Leaders have drifted into treating this pandemic as if it were an unavoidable national catastrophe.

The results of this early investigation, however, are summarized in Lessons from the COVID WAR. Overall, a good book, not as pointed or data driven as I might have liked (see my talk for a more pointed overview), but I am in large agreement with the conclusions and it does contain some clarifying tidbits such as this one on the Obama playbook.

Innumerable speeches, books, and articles have stated that the Obama administration gave the incoming Trump administration a “playbook” on how to confront a pandemic and that this playbook was ignored. The Obama administration did indeed prepare and leave behind the “Playbook for Early Response to High-Consequence Emerging Infectious Disease Threats and Biological Incidents.”

But this playbook did not actually diagram any plays. There was no “how.” It did not explain what to do…when it came to the job of how to contain a pandemic that was headed for the United States in January 2020, the playbook was a blank page.

I also appreciated that Lessons has some some unheralded success stories from the state and local level. You may recall Tyler and I blogging repeatedly in 2020 about the advantages of pooled tests. Eventually pooled testing was approved but I haven’t seen data on how widely pooling was adopted or the effective increase in testing capacity that was produced. Lessons, however, offers an anecdote:

In San Antonio, a local charitable foundation paired with a blood bank to create a central Covid PCR testing lab (antigen tests were not yet readily available) that could combine samples (pooling) for efficiency and cost reduction, but also determine which individual in a pool was positive. Importantly, results were available within about twelve hours. That meant results were available before the start of school the new day.

The program helped San Antonio get kids back into the schools.

More generally, it’s striking that US schools were closed for far longer than French, German or Italian schools. See data at right on the number of weeks that “schools were closed, or party closed, to in-person instruction because of the pandemic (from Feb. 2020-March 2022)”. (South Korea, it should be noted, had some of the most advanced online education systems in the world.)

One general point made in Lessons that I wholeheartedly agree with this is that the school closures and many of the other controversial aspects of the pandemic response such as the lockdowns and mask mandates “were really symptoms of the deep problem. Without a more surgical toolkit, only blunt instruments were left.” With better testing, biomedical surveillance of the virus and honest communication we could have done better with much less intrusive and costly policies.

Addendum: See my previous reviews of Gottlieb’s Uncontrolled Spread, Michael Lewis’s The Premonition, Slavitt’s Preventable and Abutaleb and Paletta’s Nightmare Scenario.

Addendum 2: A typo in Lessons had France closing schools for 2 weeks instead of 12 weeks. Corrected.

Generative AI and firm values

What are the effects of recent advances in Generative AI on the value of firms? Our study offers a quantitative answer to this question for U.S. publicly traded companies based on the exposures of their workforce to Generative AI. Our novel firm-level measure of workforce exposure to Generative AI is validated by data from earnings calls, and has intuitive relationships with firm and industry-level characteristics. Using Artificial Minus Human portfolios that are long firms with higher exposures and short firms with lower exposures, we show that higher-exposure firms earned excess returns that are 0.4% higher on a daily basis than returns of firms with lower exposures following the release of ChatGPT. Although this release was generally received by investors as good news for more exposed firms, there is wide variation across and within industries, consistent with the substantive disruptive potential of Generative AI technologies.

A significant effect, here is the new NBER working paper from Andrea L. Eisfeldt, Gregor Schubert, and Miao Ben Zhang.

The Public Choice Outreach Conference

There are just a few spots left! Tell your students. Apply now!

![]()

The rising tide of housing quality

This study analyzes patterns of housing consumption and expenditures among social safety net recipients since 1985. For safety net recipients, including Supplemental Security Income (SSI), Supplemental Nutrition Assistance Program (SNAP) and cash welfare (AFDC/TANF), monthly housing expenditures have risen from $692 to $1,341. However, these increased expenditures partially reflect housing quantity improvements, including more square footage, more rooms, and larger lot sizes. The data also show a marked improvement in housing quality, such as fewer sagging roofs, broken appliances, rodents, and peeling paint. The housing quality for social safety net recipients improved across 35 indicators. These quality improvements equate to a 35 to 44 percent increase in housing consumption and suggest that a typical safety net recipient in 2021 experiences housing consumption equivalent to the average national household in 1985. Though relative housing consumption has remained similar for safety net recipients, this “rising tide” of housing quality may have additional benefits for the health and well being of families and children living in better housing.

That is from a new paper by Erik Hembre, J. Michael Collins, and Samuel Wylde. Via the excellent Kevin Lewis.

How much does short-run economic “DNA” persist across interruptions?

One of the current macro puzzles is that we keep on receiving good labor market reports during a time of monetary and credit tightening. Which is the missing “dark matter” variable that helps to explain this?

One general observation, stressed by Conor Sen, is simply that we don’t have real macro data or macro models for pandemics or post-pandemic recoveries. I agree, but what exactly might be the missing key variable(s)?

If we rewind to say February 2020, might there have been favorable conditions for further economic growth, conditions that implied some degree of momentum but no tendency toward a destructive Minsky moment? And were those favorable conditions somehow “frozen in amber” during the pandemic, to be thawed, taken out, and reconstituted during the recovery and subsequent growth period?

How exactly does one freeze and then thaw out initial macro conditions during a pandemic? What exactly would it be that is happening, as might be expressed in a simple model? Is there some kind of “macro accelerator” that is carried over across time? Is it a “previously processed working out of excess” that remains in place during the pandemic recovery? (One tweet by Conor, which I don’t at the moment find, seemed to raise this as one possibility.)

What else?

Polish Vending Machine for Contact Lenses

Here’s one in Lithuania. See my post The Optometry Racket for more on the context.

Hat tip: Tadeusz Giczan.