Category: Economics

Are real rates of return negative? Is the “natural” real rate of return negative?

Here is a long and very interesting post by Paul Krugman, also referencing a recent talk by Larry Summers. There is also this older Krugman post, and here is Gavyn Davies, and also Ryan Avent. And Scott Sumner. Do read and listen to these, there is much in there to ponder. I do very much agree with the claim that lower rates of return make recovery more difficult and for the longer haul as well. And I am happy to welcome these thinkers, or in the case of Krugman re-welcome, to stagnationist ideas.

I cannot, however, agree with the central arguments about negative real interest rates, and the necessity for negative natural rates of interest (there are a variety of interlocking claims here, so do read them for yourself. I am not sure any brief summary can quite reproduce the arguments, which are also not fully clear).

As I frame the data, we have had negative real rates on government securities, but positive rates on many other investments in the U.S. The difference reflects a very high real risk premium, which of course we would like to lower, and the differences also reflect some degree of investment segmentation. The positive rates on these other investments are evidenced by recent broad stock market gains, observed rates of productivity growth (low but clearly positive), high internal corporate hurdle rates, and so on. The “average vs. marginal” distinction is an important one, but still I don’t see how it can be used to push us away from seeing relevant real rates of return as positive. Nor do I think monopoly is widespread enough for that assumption to be a game-changer. Even Apple competes with Samsung and others in its major product lines.

Given the multiplicity of real rates in the American economy, I get nervous when I read about the real rate or the natural rate. (Don’t forget Sraffa [1932] and also Arnold Kling discusses the different issue of varying rates across people. Interfluidity questions whether the idea of a natural rate makes sense at all.) I also get nervous when I do not see serious talk about the embedded risk premium in the observed structure of market rates. I grow more nervous yet when the average vs. marginal question is not spelled out more explicitly.

In my view very negative real rates of return would not be a “natural rate” giving rise to full employment through a better equilibration of planned savings and investment. Given a pretty flat employment to population ratio, very negative real rates of return across the economy as a whole would have to mean negative economic growth and other attendant difficulties.

And no, I don’t think that output shrinkage associated with the persistently negative real interest rate would be expansionary through liquidity trap mechanisms; for one thing the negative wealth effect and the higher risk premium likely would offset the positive velocity effect on currency balances. The velocity effect on currency balances, from inflation, just isn’t that strong. At persistent negative rates of return we are much more likely to see an interdependence of AS and AD and some kind of cascading collapse of both. Or maybe it is simply better to say the framework has broken down than to try to squeeze one’s own predictions out of that set up.

Furthermore if you think destruction will help you ought then think that capital obsolescence will pull us out of Hansen’s long-term stagnation within five to ten years. On top of all that, I worry about the apparent “out of equilibrium” assumptions embedded in a model that has both a) negative real rates of return on investment and b) those investments being made in the first place, given that storage costs don’t seem to be enormously high.

I don’t mean this in a rude or polemic way, but the arguments we have been reading do not yet make sense.

Here is a claim I do find possible, although it is not one I am pushing. That would be a neo-Wicksellian argument that rates of return on capital are positive but low, and investors need low and indeed very negative borrowing rates to reflate the economy, given how high the risk premium is. I don’t read Krugman as promoting that view (note his citation of Samuelson’s OLG model for instance), although I think that is what the argument will have to boil down to. Otherwise it ends up being a call for output destruction, which, while I do understand how in some models at some margins that can help, I don’t think at current margins is going to be anything other than an unmitigated disaster. Literally.

I see it this way. If you are postulating a stagnation across the longer run, ultimately it will have to boil down to supply side deficiencies. The simple way to explain the mediocre recovery is to tack on slow growth assumptions to the underlying demand deficiencies. But that would constitute a big concession to real business cycle theory and it would put Thiel-Mandel-Gordon-Cowen stagnationist views in the driver’s seat, all the more so over time. The look back to Alvin Hansen is an effort to work in some (very much needed) stagnationist ideas, while at the same time doubling down on a demand-side perspective.

That just isn’t going to work.

*Fortune Tellers: The Story of America’s First Economic Forecasters*

The author is Walter A. Friedman and the Amazon link is here. It is a good and readable look at a neglected corner of the history of economic thought, covering Roger Babson, Irving Fisher, John Moody, Warren Persons, Wesley Mitchell, and others. Here is one bit:

At Yale, [Irving] Fisher conducted dietary experiments with student athletes in ways that no university today would allow. These included one test that compared athletes who chewed their food thoroughly against those who did not and one that pitted the endurance of meat eaters against vegetarians. He gained enough authority as a nutrition expert for the makers of the cereal grape-Nuts to include his endorsement in a 1907 advertisement. It mentioned Fisher’s experiments on yale students “to determine the effects of the thorough mastication of food.” Fisher, the ad claimed, found that their endurance was increased 50 percent, although they took no more exercise than before and has reduce their consumption of “flesh foods” by five-sixths. Fisher also chaired a nationwide Committee of One Hundred on National Health that wrote reports and built a network of experts and public figures to agitate for “increased federal regulation of public health” — specifically, a cabinet-level department of health.

…Health, according to Fischer, deserved as much attention from economists as import and export totals.

This is a book that John P. Cullity would have enjoyed.

Getting rid of old regulations is much too hard

That is the topic of my latest New York Times column, which is entitled “More Freedom on the Airplane, if Nowhere Else.” It opens with this example:

It is sometimes the small events that reveal the really big problems lurking beneath the surface. That’s the case with the Federal Aviation Administration’s recent decision to grant airlines the liberty of allowing the use of electronic devices during takeoff and landing.

You still won’t be able to call on your cellphone during those times, but, if the airline allows it, you will be able to read on your Kindle or play Angry Birds throughout the flight.

That’s the good news. What’s the deeper problem? Our new Kindle freedoms, however minor they may seem, show how hard it is to clear away the old, unnecessary regulations that are impeding the economy.

After all, the previous restriction on electronics during flights was broadly unpopular in a way that cut across partisan lines. Yet, for many years, the public’s complaints did not bring concrete change, mostly because of regulatory inertia. (If you’re worried about safety, by the way, the airlines can still, at their discretion, demand that these devices be turned off when deemed necessary.)

Here is another bit from the piece:

Many regulations, when initially presented, can sound desirable. The problem is that, taken in their entirety, excess rules divert attention from pressing issues like the need for innovation and new jobs.

Michael Mandel, an economist at the Progressive Policy Institute, compares many regulations to “pebbles in a stream.” Individually, they may not have a big impact. But if there are too many pebbles, a river’s flow can be thwarted. Similarly, too many regulations can limit business activity. When the number of rules mounts, it can become hard for a business to know whether it is operating within the law’s confines. The issue is all the more problematic when federal, state and local constraints all apply.

Our public sector is overregulated, too. For instance, the tangle known as government procurement has exacerbated problems with the Affordable Care Act’s health insurance exchanges. The required formal processes made it difficult to hire the best possible talent, led to nightmare organizational charts and resulted in blurred lines of accountability. It’s hard to turn on a dime and fix such problems overnight, no matter how pressing the need.

Read the whole thing.

How to fix (some of) the Obamacare mess

Ross Douthat writes:

…it does seem like there is a semi-plausible policy response to the rate shock issue, which wouldn’t roll back the ongoing plan cancellations but might make cheaper plans available to buyers going forward: Obamacare’s regulations could be rewritten to allow insurers to sell less comprehensive plans on the exchanges. This wouldn’t require doing away with every new regulation, or rolling back the pre-existing condition guarantee, which is what liberals argue the Upton bill currently being considered in the House would do. But it could involve heeding the recent hint from the University of Chicago’s Harold Pollack, a card-carrying Obamacare advocate, that perhaps in the wake of the last month’s developments the government should ”revisit just how minimal the most minimal insurance packages should be,” which in turn could open the door to allowing many more people to buy the kind of high-deductible catastrophic plans that the law currently allows insurers to only sell to twentysomethings.

These moves would not let everyone keep their existing plans, as the Upton and Landrieu bills aspire to do — but there is really nothing that the White House can responsibly do, given the law’s underlying design, that would resolve that problem. What partial deregulation would accomplish, though, is to allow some of the lower-cost plans the law abolishes to be actually revived and made available on the exchanges as “bronze” options in 2014 and 2015, rather than just temporarily grandfathered for a year or so outside them.

The post has other points of interest as well.

A life well-lived

This is from the obituary of economist Alexander L. Morton:

At 42, Mr. Morton was well on pace in the ascension of his chosen career ladder. He had a doctorate in economics from Harvard, had taught at the Harvard Business School and was finishing a four-year assignment as director the office of policy and analysis at the Interstate Commerce Commission.

He then quit.

He had made enough money in real estate deals and investments to guarantee an independent income for himself. For his remaining 28 years, he was almost constantly on the move, visiting dozens of countries and often going off the expected paths from Western travelers.

And this:

He rarely spoke about himself and never discussed in detail his reasons for retiring in mid-career as an economist to pursue a life of travel. But his sister said he was ready for a change, had the savings to and had done as much as he wished to in the field of transportation deregulation.

To continue along the same path, would have been a case of “been there, done that,” she said.

Here is Alex’s earlier post on traveling more. Maybe Alexander L. Morton had some really good lunch partners.

Should the U.S. destroy its stockpile of ivory?

Here is one of the latest developments in economic policy:

The US government hopes to send a crushing message to anyone involved in the illegal ivory trade — by decimating a 6-ton stockpile of seized elephant ivory.

In an announcement posted online, the US Fish and Wildlife Services (FWS) describes plans to “pulverize” a cache of ivory on November 14th. All of the ivory was obtained, the agency notes, from law enforcement efforts to crack down on trafficking over the last two decades. “Destroying this ivory tells criminals who engage in poaching and trafficking that the United States will take all available measures to disrupt and prosecute those who prey on, and profit from, the deaths of these magnificent animals,” reads a statement on the FWS website.

There is more here, via Viktor Brech and Bruce Ryan and Kaushal Desai.

Bruce suggests the government announce it has created an artificial form of ivory, to lower expected prices and discourage future poaching. If they can get away with that lie, great. Otherwise, we all know the 2000 Kremer and Morcom piece entitled simply “Elephants”:

Many open-access resources, such as elephants, are used to produce storable goods. Anticipated future scarcity of these resources will increase current prices and poaching. This implies that, for given initial conditions, there may be rational expectations equilibria leading to both extinction and survival. The cheapest way for governments to eliminate extinction equilibria may be to commit to tough antipoaching measures if the population falls below a threshold. For governments without credibility, the cheapest way to eliminate extinction equilibria may be to accumulate a sufficient stockpile of the storable good and threaten to sell it should the population fall.

That emphasis is added. Sell it, not destroy.

The (gated) AER version of the paper is here. The Montclair State version is here. A few comments and responses are here.

In other words, our government is pursuing symbolic value but at the same time implementing the wrong incentives.

Here is a piece on elephant music-making.

IBM’s Watson will be made available in a more powerful form on the internet

Companies, academics and individual software developers will be able to use it at a small fraction of the previous cost, drawing on IBM’s specialists in fields like computational linguistics to build machines that can interpret complex data and better interact with humans.

That is a big deal, obviously. The story is here.

What are some of the biggest problems with a guaranteed annual income?

Maybe this isn’t the biggest problem, but it’s been my worry as of late. Must a guaranteed income truly be unconditional? Might there be circumstances when we would want to pay some individuals more than others? Many critics for instance worry that a guaranteed income would excessively reduce the incentive to work. So it might be proposed that the payment be somewhat higher if low income individuals go get a job. That also will make the system more financially sustainable. But wait — that’s the Earned Income Tax Credit, albeit with modifications.

Might we also wish to pay more to some individuals with disabilities, perhaps say to help them afford expensive wheelchairs? Maybe so. But wait — that’s called disability insurance (modified, again) and it is run through the Social Security Administration.

As long as we are moving toward more cash transfers, why don’t we substitute cash transfers for some or all of Medicare and Medicaid health insurance coverage benefits, especially for lower-value ailments? But then we are paying more cash to the sick individuals. That doesn’t have to be a mistake, but it does mean that an initially simple, “dogmatic” payment scheme now has multiplied into a rather complex form of social welfare assistance, contingent on just about every relevant factor one might care to cite.

You can see the issue. Whether on grounds of justice, practicality, or just public choice considerations (“you can keep your current welfare payments if you like them”), we should not expect everyone to be paid the same under a guaranteed annual income. And with enough tweaks, this version of the guaranteed income suddenly starts resembling…the welfare state, albeit the welfare state plus. Unemployment insurance benefits wouldn’t end. More people could get on disability, and without those pesky judges asking so many questions.

The potential problem is that we inherit and in some ways magnify the problems with the current welfare state, rather than doing away with those problems.

Or we could be truly dogmatic about it, and simply pay each person the same amount of money no matter what. But then do we take away the various forms of in-kind aid which are already in place? And what about all those former EITC recipients, whose incentive to work is now lower than ever?

Part of the original appeal of the guaranteed income idea, especially as expressed by Milton Friedman, is that it would substitute for welfare programs and bureaucracies, not all of which work well. On first hearing, the guaranteed income proposal sounds quite “clean.” In reality, that is unlikely to be the case.

And once we recognize the proposal may be “the current welfare state plus some extra and longer-term payments,” one has to ask whether this is really what we had in mind in the first place. It seems that if you wanted to reform current programs and also pay people more (debatable, of course), there may be better and easier ways of doing that than reforms which have to fit under the umbrella of “a guaranteed annual income.”

I still think the core idea is a good one, but perhaps “what the core idea is” is less pinned down than I might have wished.

Here is again Annie Lowrey’s very useful piece, which provides an overview of current proposals.

Inefficient forms of aid

A group of Occupy Wall Street activists has bought almost $15m of Americans’ personal debt over the last year as part of the Rolling Jubilee project to help people pay off their outstanding credit.

Rolling Jubilee, set up by Occupy’s Strike Debt group following the street protests that swept the world in 2011, launched on 15 November 2012. The group purchases personal debt cheaply from banks before “abolishing” it, freeing individuals from their bills.

By purchasing the debt at knockdown prices the group has managed to free $14,734,569.87 of personal debt, mainly medical debt, spending only $400,000.

There is more here, and here. One question is how many of these people will go into bankruptcy anyway. Another is why not just send the money to even poorer individuals? The low market value of the debt, of course, means these individuals (mostly) would not have paid anyway, so the leveraged return on this investment is not as high as is being claimed.

For pointers I thank Mitch Berkson and Samir Varma.

Attempting to insure against your own destruction, enslavement, and cultural abnegation

A new finance product has been proposed:

Funding the Search for Extraterrestrial Intelligence with a Lottery Bond

(Submitted on 11 Nov 2013)I propose the establishment of a SETI Lottery Bond to provide a continued source of funding for the search for extraterrestrial intelligence (SETI). The SETI Lottery Bond is a fixed rate perpetual bond with a lottery at maturity, where maturity occurs only upon discovery and confirmation of extraterrestrial intelligent life. Investors in the SETI Lottery Bond purchase shares that yield a fixed rate of interest that continues indefinitely until SETI succeeds—at which point a random subset of shares will be awarded a prize from a lottery pool. SETI Lottery Bond shares also are transferable, so that investors can benefact their shares to kin or trade them in secondary markets. The total capital raised this way will provide a fund to be managed by a financial institution, with annual payments from this fund to support SETI research, pay investor interest, and contribute to the lottery fund. Such a plan could generate several to tens of millions of dollars for SETI research each year, which would help to revitalize and expand facilities such as the Allen Telescope Array. The SETI Lottery Bond is a savings product that only can be offered by a financial institution with authorization to engage in banking and gaming activities. I therefore suggest that one or more banks offer a lottery-linked savings product in support of SETI research, with the added benefit of promoting personal savings and intergenerational wealth building among individuals.

The pointer is from Mark Rodeghier.

Firearms and Suicides in US States

Suicides outnumber homicides in the United States by 3:1. (In 2010 there were 38,364 suicides and 12, 996 homicides.) Lots of studies have investigated the relationship between firearms and homicide but the potential for reverse causality makes this a difficult problem. More homicides in a region, for example, might cause an increase in gun ownership so a positive correlation between guns and homicide doesn’t tell you which is cause and which is effect. Reverse causality is less of a problem for understanding the guns to suicide link because it’s less likely that a rash of suicides would encourage gun ownership.

In my latest paper, Firearms and Suicides in US States, (written with the excellent Justin Briggs) we examine the easier question, what is the relationship between firearms and suicide? Using a variety of techniques and data we estimate that a 1 percentage point increase in the household gun ownership rate leads to a .5 to .9% increase in suicides.* (n.b. slight change in language from earlier version for clarity.)

Even if one thinks that suicides don’t cause gun ownership one might imagine that they are correlated due say to a third factor such as social anomie. We have an interesting test of this in the paper. If suicides and gun ownership were being driven by a third factor we would expect gun ownership to be correlated with all suicides not just gun-suicide. What we find, however, is that an increase in gun ownership decrease non-gun suicide. From an economics perspective this makes perfect sense. As gun ownership increases, the cost of gun-suicide falls because guns are easier to access and as the cost of gun-suicide falls there is substitution away from non-gun suicide.

Put differently, when gun ownership decreases other methods of suicide increase. Substitution among methods is not perfect, however, so when gun ownership decreases we see a big decrease in gun-suicide and a substantial but less than fully compensating increase in non-gun suicide so a net decrease in the number of suicides.

Our econometric results are consistent with the literature on suicide which finds that suicide is often a rash and impulsive decision–most people who try but fail to commit suicide do not recommit at a later date–as a result, small increases in the cost of suicide can dissuade people long enough so that they never do commit suicide.

The results in the paper appear to be robust but the data on gun ownership is frustratingly sparse due to political considerations.

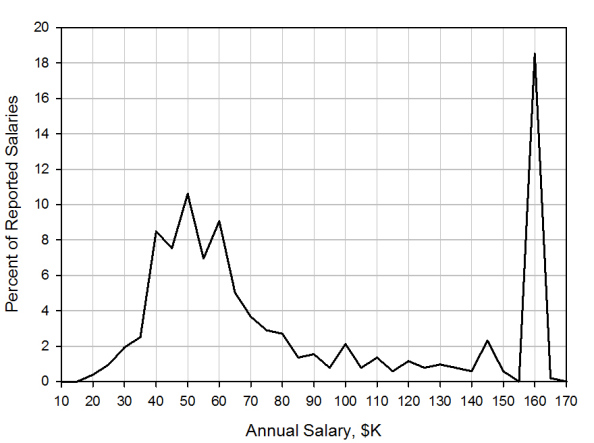

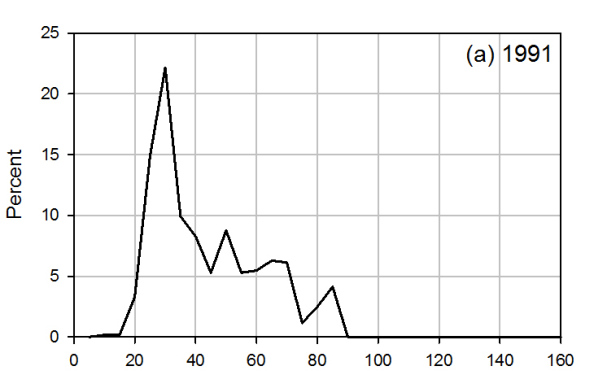

The changing income distribution for lawyers (Average is Over)

As of 2010, a graph of starting salaries looks like this:

As of 1991, it looked like this:

That is from Peter Turchin. Here is a WSJ article by Ben Casselman on the widening job market gap more generally.

*Deliberating American Monetary Policy: A Textual Analysis*

The author is Cheryl Schonhardt-Bailey and that is a new book published by MIT Press. The Amazon link is here. Here is a bit from the book’s home page:

In this book, Cheryl Schonhardt-Bailey provides a systematic examination of deliberation on monetary policy from 1976 to 2008 by the Federal Reserve’s Open Market Committee (FOMC) and House and Senate banking committees. Her innovative account employs automated textual analysis software to study the verbatim transcripts of FOMC meetings and congressional hearings; these empirical data are supplemented and supported by in-depth interviews with participants in these deliberations. The automated textual analysis measures the characteristic words, phrases, and arguments of committee members; the interviews offer a way to gauge the extent to which the empirical findings accord with the participants’ personal experiences.

The new “carry trade”?

Loosely regulated non-bank lenders have emerged as among the biggest beneficiaries of the Federal Reserve’s ultra-low interest rates with three specialist categories increasing their assets by almost 60 per cent since the height of the financial crisis.

Such lenders, widely considered part of the “shadow banking” system, have expanded rapidly on the back of investors who are clamouring for the higher returns on offer from financing riskier types of lending.

From the FT, there is more here.

Markets in everything

The words on the website say it all:

Monetize without ads

Let your visitors help you mine Bitcoins

The pointer is from the excellent Ashok Rao.