Category: History

*Duty: Memoirs of a Secretary at War*

That is the new Robert M. Gates book, which of course has been widely reviewed. I was very impressed with this work. I read it as a meditation on the question of what kinds of martial virtue (or lack thereof) are possible in our contemporary age, updating Herodotus, Thucydides, and Plutarch through the medium of the reigns and rules of the two Bushes, Cheney, Rice, Obama (most of all), Hillary, Biden, and of course Gates himself with a bit of Petraeus tossed in.

Here is one excerpt:

I was put off by the way the president closed the meeting. To his very closest advisers, he said, “For the record, and for those of you writing your memoirs, I am not making any decisions about Israel or Iran, Joe [Biden], you be my witness.” I was offended by his suspicion that any of us would ever write about such sensitive matters.

And this:

As is usual when the president makes a momentous decision, the White House wanted key cabinet members blanketing the Sunday talk shows…As I was flying back to Washington on March 25, the White House communications gurus proposed I go on all three network shows the next Sunday to defend the president’s decision on Libya. Exhausted by the trip, I agreed to do two of the three. then I took a call from Bill Daley, who pushed me hard to do the third show. I told Daley I’d make him a deal — I would do the third show if he’s agree to get funding for the Libya operation included in the Overseas Contingency Operations (OCO) appropriation (the war supplemental). I said, “I’ll do Jake Tapper if you’ll do OMB.” Daley whined, “I thought it would cost me a bottle of vodka.” I shot back, “Bullshit. It’s going to cost you $1 billion.” Daley had the last laugh. The president and OMB director Jack Lew refused to approve moving the Libya funding into the OCO. The Defense Department had to eat the entire cost of the Libya operation.

And finally, this:

As I had told President Bush and Condi Rice early in 2007, the challenge of the early twenty-first century is that crises don’t come and go — they seem to come and stay.

The book has come under a good deal of criticism for its revelations about a sitting president and commander-in-chief and for its communication of inside discussions, which presumably at the time were considered to be confidential. I am not sufficiently informed about the appropriate norms to make a final judgment here, but I can readily imagine that Gates is in this regard quite in the wrong. Good books are not always based on good behavior. Furthermore, the overall portrait of Obama is, in my view, quite a favorable one and indeed I would say a profound one (the same cannot be said for Biden or for Congress).

Unified China and Divided Europe

There is a new paper on economic development by Chiu Yu Ko, Mark Koyama, and Tuan-Hwee Sng, the abstract is this:

This paper studies the persistence and consequences of political centralization and fragmentation in China and Europe. We argue that the severe and unidirectional threat of external invasion fostered political centralization in China while Europe faced a wider variety of external threats and remained politically fragmented. Our model allows us to explore the economic consequences of political centralization and fragmentation. Political centralization in China led to lower taxation and hence faster population growth during peacetime than in Europe. But it also meant that China was relatively fragile in the event of an external invasion. We argue that the greater volatility in population growth during the Malthusian era in China can help explain the divergence in economic development that had opened up between China and Europe at the onset of the Industrial Revolution.

Claims about coal

Counterfactual estimates of city population sizes indicate that our estimated coal effect explains at least 60% of the growth in European city populations from 1750 to 19o0.

That is from a new NBER working paper by Alan Fernihough and Kevin Kevin Hjortshøj O’Rourke. There is an ungated version of the paper here.

Upward mobility in the United States is not declining as many citizens think

Here is the new Raj Chetty paper that everyone is talking about (pdf);

We use administrative records on the incomes of more than 40 million children and their parents to describe three features of intergenerational mobility in the United States. First, we characterize the joint distribution of parent and child income at the national level. The conditional expectation of child income given parent income is linear in percentile ranks. On average, a 10 percentile increase in parent income is associated with a 3.4 percentile increase in a child’s income. Second, intergenerational mobility varies substantially across areas within the U.S. For example, the probability that a child reaches the top quintile of the national income distribution starting from a family in the bottom quintile is 4.4% in Charlotte but 12.9% in San Jose. Third, we explore the factors correlated with upward mobility. High mobility areas have (1) less residential segregation, (2) less income inequality, (3) better primary schools, (4) greater social capital, and (5) greater family stability. While our descriptive analysis does not identify the causal mechanisms that determine upward mobility, the new publicly available statistics on intergenerational mobility by area developed here can facilitate future research on such mechanisms.

Here is summary coverage from David Leonhardt. The highly reliable David starts with this: “The odds of moving up — or down — the income ladder in the United States have not changed appreciably in the last 20 years, according to a large new academic study that contradicts politicians in both parties who have claimed that income mobility is falling.”

Confusing issues of equality and mobility remains rife in current discourse.

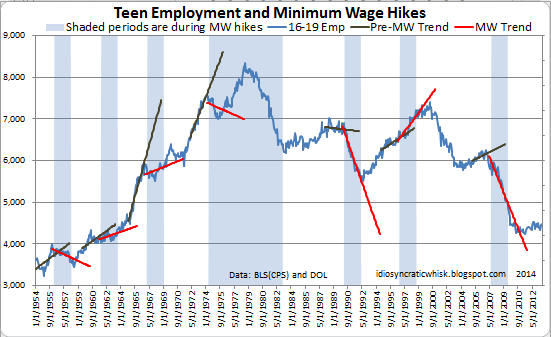

Teen employment and the minimum wage: sixty years of experience

Kevin Erdmann relates:

There is much more here. Kevin concludes: “Is there any other issue where the data conforms so strongly to basic economic intuition, and yet is widely written off as a coincidence?”

Is technology driving us apart? And are there more women in public spaces?

It seems the answer is no. There is an interesting new NYT piece by Mark Oppenheimer, here is one excerpt:

Hampton found that, rather than isolating people, technology made them more connected. “It turns out the wired folk — they recognized like three times as many of their neighbors when asked,” Hampton said. Not only that, he said, they spoke with neighbors on the phone five times as often and attended more community events. Altogether, they were much more successful at addressing local problems, like speeding cars and a small spate of burglaries. They also used their Listserv to coordinate offline events, even sign-ups for a bowling league. Hampton was one of the first scholars to marshal evidence that the web might make people less atomized rather than more. Not only were people not opting out of bowling leagues — Robert Putnam’s famous metric for community engagement — for more screen time; they were also using their computers to opt in.

And:

According to Hampton, our tendency to interact with others in public has, if anything, improved since the ‘70s. The P.P.S. films showed that in 1979 about 32 percent of those visited the steps of the Met were alone; in 2010, only 24 percent were alone in the same spot.

And finally:

…this was Hampton’s most surprising finding: Today there are just a lot more women in public, proportional to men. It’s not just on Chestnut Street in Philadelphia. On the steps of the Met, the proportion of women increased by 33 percent, and in Bryant Park by 18 percent. The only place women decreased proportionally was in Boston’s Downtown Crossing — a major shopping area. “The decline of women within this setting could be interpreted as a shift in gender roles,” Hampton writes. Men seem to be “taking on an activity that was traditionally regarded as feminine.”

Across the board, Hampton found that the story of public spaces in the last 30 years has not been aloneness, or digital distraction, but gender equity. “I mean, who would’ve thought that, in America, 30 years ago, women were not in public the same way they are now?” Hampton said. “We don’t think about that.”

The piece is interesting throughout.

Scottish independence: the bottom line

Christopher Pissarides, professor of economics at the London School of Economics, said being part of the Union gives a small economy like Scotland assurance that help will be forthcoming if something goes wrong.

“The last thing any Scot should wish is to give up the support potentially available from the UK (England?) for support from the European Union under Germany’s rules,” he said.

Here are related opinions:

Philip Rush, chief economist at Nomura investment bank, said: “Higher taxes on income would push many wealthy individuals and some companies they work for south of the Border, harming Scotland’s economy.”

Keith Wade, chief economist and strategist at Shroders, said “massive wrangling” between Holyrood and Westminster over tax and spending would be required for a currency union to work “to avoid a rerun of the euro crisis”.

“When combined with the considerable uncertainty over whether Scotland can remain in the EU, Scottish businesses would start to head south,” he said.

There is more here.

*Capital in the 21st Century*

Many of you have been asking me about the forthcoming Thomas Piketty book. I am writing a 2500-word review of it for…elsewhere…so mum’s the word until then. For now I’ll just say it is a book to buy, read, and indeed study. Here is one good piece on the book from The Economist. It’s already a splendid year for the published word.

Books Average Previous Decade of Economic Misery

That is the new paper by Bentley, Acerbi, Ormerod, and Lampos, and here is the abstract:

For the 20th century since the Depression, we find a strong correlation between a ‘literary misery index’ derived from English language books and a moving average of the previous decade of the annual U.S. economic misery index, which is the sum of inflation and unemployment rates. We find a peak in the goodness of fit at 11 years for the moving average. The fit between the two misery indices holds when using different techniques to measure the literary misery index, and this fit is significantly better than other possible correlations with different emotion indices. To check the robustness of the results, we also analysed books written in German language and obtained very similar correlations with the German economic misery index. The results suggest that millions of books published every year average the authors’ shared economic experiences over the past decade.

Here is NYT coverage of that paper. Here are some related papers by Bentley and co-authors, note that American English is diverging from British English by its greater use of emotional words.

For the pointer I thank Mark Thorson.

Jewish persecutions and weather shocks

There is a recent paper by Robert Warren Anderson, Noel D. Johnson, and Mark Koyama, and the abstract is this:

What factors caused the persecution of minorities in medieval and early modern Europe? We build a model that predicts that minority communities were more likely to be expropriated in the wake of negative income shocks. Using panel data consisting of 1,366 city-level persecutions of Jews from 936 European cities between 1100 and 1800, we test whether persecutions were more likely in colder growing seasons. A one standard deviation decrease in average growing season temperature increased the probability of a persecution between one-half and one percentage points (relative to a baseline probability of two percent). This effect was strongest in regions with poor soil quality or located within weak states. We argue that long-run decline in violence against Jews between 1500 and 1800 is partly attributable to increases in fiscal and legal capacity across many European states.

In the Matt-Ezra debate over whether too hot or too cold is worse, this Irishman has to side against the blustery winter.

Law and Literature syllabus 2014

The first class is today! Here is my reading list:

The New English Bible, Oxford Study Edition

Glaspell’s Trifles, available on-line.

Billy Budd and Other Tales, by Hermann Melville.

The Metamorphosis, In the Penal Colony, and Other Stories, by Franz Kafka, edited and translated by Joachim Neugroschel.

In the Belly of the Beast, by Jack Henry Abbott.

Conrad Black, A Matter of Principle.

Sherlock Holmes, The Complete Novels and Stories, Sir Arthur Conan Doyle, volume 1.

I, Robot, by Isaac Asimov.

Moby Dick, by Hermann Melville, excerpts, chapters 89 and 90, available on-line.

Year’s Best SF 9, edited by David G. Hartwell and Kathryn Cramer.

Death and the Maiden, Ariel Dorfman.

The Pledge, Friedrich Durrenmatt.

Haruki Murakami, Underground.

Honore de Balzac, Colonel Chabert.

Thomas Pynchon, The Crying of Lot 49.

M.E. Thomas, Confessions of a Sociopath.

Alan Moore, V for Vendetta.

Gillian Flynn, Gone Girl.

Some additions to this list will be made as we proceed. We also will view a few movies on legal themes, I will be back in touch on these.

I am likely to use A Separation and Memories of Murder as two of the movies, along with a new release depending on schedule.

Fertility decisions and the escape from slavery

Hope really does matter, as outlined in a recent paper (pdf) by Treb Allen of Northwestern, with the formal title “The Promise of Freedom”:

This paper examines the extent to which the fertility of enslaved women was affected by the promise of freedom. Because women derived greater pleasure from children when they were free, increases in the distance to freedom (which lowered the probability of escape) should reduce fertility. Exploiting the Fugitive Slave Law of 1850 and the particularity of U.S. geography, I demonstrate a strong negative correlation between fertility and the distance to freedom. This negative correlation is stronger on larger plantations, but disappears when the father of the child is white. The correlation varies with the difficulty of the route, and a similar correlation is not present for white children or for slave children born prior to the Fugitive Slave Law. The negative correlation suggests that despite the small number of successful escapes, the promise of freedom played an important role in the everyday lives of slaves.

There are more interesting papers by Allen here., including on the gravity equation and location theory. Allen is one of the most interesting young economists today, yet he remains undercovered. Here is Treb on “Equilibrium distribution of population if the surface of the world was shaped like a cow.”

Cihan Artunç is studying legal pluralism in the Ottoman Empire

Here is the abstract from his job market paper, he is from Yale:

Throughout the eighteenth and nineteenth centuries, non-Muslim Ottomans paid large sums to acquire access to European law. These protégés came to dominate Ottoman trade and pushed Muslims and Europeans out of commerce. At the same time, the Ottoman firm remained primarily a small, family enterprise. The literature argues that Islamic law is the culprit. However, adopting European law failed to improve economic outcomes. This paper shows that the co-existence of multiple legal systems, “legal pluralism,” explains key questions in Ottoman economic history. I develop a bilateral trade model with multiple legal systems and first show that legal pluralism leads to underinvestment by creating enforcement uncertainty. Second, there is an option value of additional legal systems, explaining why non-Muslim Ottomans sought to acquire access to European law. Third, in a competitive market where a subpopulation has access to additional legal systems, agents who have access to fewer jurisdictions exit the market. Thus, forum shopping explains protégés’ dominance in trade. Finally, the paper explains why the introduction of the French commercial code in 1850 failed to reverse these outcomes.

There is further interesting work at the link.

Do Americans prefer hand-held foods?

Are there any dishes or foods that you would classify as typically, or even exclusively, “American?”

A number of iconic foods—hot dogs and hamburgers, snack food—are hand-held. They’re novelties associated with entertainment. These are the kinds of food you eat at the ballpark, buy at a fair and eventually eat in your home. I think that there is a pattern there of iconic foods being quick and hand-held that speaks to the pace of American life, and also speaks to freedom. You’re free from the injunctions of Victorian manners and having to eat with a fork and knife and hold them properly, sit at the table and sit up straight and have your napkin properly placed. These foods shirk all that. There’s a sense of independence and a celebration of childhood in some of those foods, and we value that informality, the freedom and the fun that is associated with them.

Happy public domain day!

I received this email from James Boyle at Duke:

Dear Tyler, An early Happy New Year to you and your family — I hope all is well? You may remember our annual survey of the stuff that would be entering the public domain if we had the copyright laws from 1976.

The list this year is a particularly scrumptious one. The mouseover of the book covers is another pleasure.· Samuel Beckett, Endgame (“Fin de partie”, the original French version)· Jack Kerouac, On the Road (completed 1951, published 1957)· Ayn Rand, Atlas Shrugged· Margret Rey and H.A. Rey, Curious George Gets a Medal· Dr. Seuss (Theodor Geisel), How the Grinch Stole Christmas and The Cat in the Hat· Eliot Ness and Oscar Fraley, The Untouchables· Northrop Frye, Anatomy of Criticism: Four Essays· Walter Lord, Day of Infamy· Studs Terkel, Giants of Jazz· Corbett H. Thigpen and Hervey M. Cleckley, The Three Faces of Eve· Ian Fleming, From Russia, with Love· A.E. Van Vogt, Empire of the Atomhttp://web.law.duke.edu/cspd/publicdomainday/2014/pre-1976

Movies:

The Incredible Shrinking Man, The Bridge on the River Kwai, A Farewell to Arms, Gunfight at the O.K. Corral, 3:10 to Yuma, 12 Angry Men, Jailhouse Rock, Funny Face, An Affair to Remember, Nights of Cabiria and The Seventh Seal..

(Is this list depressing when set against 2013?)

In the world of fine arts, Picasso’s Las Meninas set of paintings… only themselves legal because no copyright covered Velazquez’s.. would also be entering the public domain.