Results for “age of em” 17238 found

From the comments, on the value of management consultants

As a retired management consultant, some views on their stated value (as stated by clients, which is not necessarily the same as “value” as seen by other observers, e.g. Douglas Adams). 1. Consultants as temps. Keep own planning staff small, hire consultants when surge capacity needed. 2. New views. Yes, the young consultants may not know your industry well. This fresh look may actually be desired. In my own experience clients oscillated between “Give me people who actually know something about my business!” and “Stop giving me people from inside my world, they just tell me what I already know!” 3. Cowardice. Client knows he must lay off 5,000, call in consultants to figure that out, blame them for it. 4. Sounding boards. Senior executives believe it or not often have no one to talk to, who is not scheming to take their job or playing other politics. Consultants play politics of course, but they are at least transparent: “If I give you advice you find valuable you will hire me again.” 5. Pollination. The client cannot go and ask 5 rival firms what they think about developments in the industry, at least not easily. If the consultants have worked for many clients in the industry, they can transfer best ideas. If you like this, you call it “dissemination of best practices;” if you don’t like it, you call it “stealing and re-selling trade secrets to rivals”. 6. Complexity. A client on its own may not want to invest in learning all it needs about AI, IOT, Bitcoin, on and on. The consultant invests in this knowledge (McKinsey’s research budget is in at least 8 digits, including opportunity costs) and can deliver it packaged up for easy access by the client.

That is from Glenn Mercer.

Covid-19 age demographics and countries

Here is an excellent document, best material I have seen on this topic so far, by the excellent Elad Gil and Shin Kim.

Macroeconomic Implications of COVID-19: Can Negative Supply Shocks Cause Demand Shortages?

There is a new NBER paper by Veronica Guerrieri, Guido Lorenzoni, Ludwig Straub, Iván Werning:

We present a theory of Keynesian supply shocks: supply shocks that trigger changes in aggregate demand larger than the shocks themselves. We argue that the economic shocks associated to the COVID-19 epidemic—shutdowns, layoffs, and firm exits—may have this feature. In one-sector economies supply shocks are never Keynesian. We show that this is a general result that extend to economies with incomplete markets and liquidity constrained consumers. In economies with multiple sectors Keynesian supply shocks are possible, under some conditions. A 50% shock that hits all sectors is not the same as a 100% shock that hits half the economy. Incomplete markets make the conditions for Keynesian supply shocks more likely to be met. Firm exit and job destruction can amplify the initial effect, aggravating the recession. We discuss the effects of various policies. Standard fiscal stimulus can be less effective than usual because the fact that some sectors are shut down mutes the Keynesian multiplier feedback. Monetary policy, as long as it is unimpeded by the zero lower bound, can have magnified effects, by preventing firm exits. Turning to optimal policy, closing down contact-intensive sectors and providing full insurance payments to affected workers can achieve the first-best allocation, despite the lower per-dollar potency of fiscal policy.

All NBER papers on Covid-19 are open access, by the way.

Is U.S. average body temperature decreasing?

In the US, the normal, oral temperature of adults is, on average, lower than the canonical 37°C established in the 19th century. We postulated that body temperature has decreased over time. Using measurements from three cohorts–the Union Army Veterans of the Civil War (N = 23,710; measurement years 1860–1940), the National Health and Nutrition Examination Survey I (N = 15,301; 1971–1975), and the Stanford Translational Research Integrated Database Environment (N = 150,280; 2007–2017)–we determined that mean body temperature in men and women, after adjusting for age, height, weight and, in some models date and time of day, has decreased monotonically by 0.03°C per birth decade. A similar decline within the Union Army cohort as between cohorts, makes measurement error an unlikely explanation. This substantive and continuing shift in body temperature—a marker for metabolic rate—provides a framework for understanding changes in human health and longevity over 157 years.

That is from a new paper by Protsiv, Ley, Lankester, Hastie, and Parsonnet. Via the excellent Kevin Lewis.

Emmanuel Todd, *Lineages of Modernity*

Sadly I had to read this book on Kindle, so my usual method of saving passages and ideas by the folded page is failing me. I can tell you this is one of the most interesting (but also flawed) books I read this year, with “family structure is sticky and it determines the fate of your nation” as the basic takeaway.

Todd suggests that the United States actually has a fairly “backward” and un-evolved family structure — exogamy and individualism — not too different from that of hunter-gatherer societies. That makes us very flexible and also well-suited to handle the changing conditions of modernity. Much of the Arab world, in contrast, has a highly complex and evolved and in some ways “more advanced” family structure, involving multiple alliances, overlapping networks, and often cousin marriages. The mistake is to think of those structures as under-evolved outcomes that simply can advance a bit, “loosen up with prosperity,” and allow their respective countries to enter modernity. Rather those structures are stuck in place, and they will interact with the more physical features of globalization and liberalization in interesting and not always pleasant ways. Many of those societies will end up in untenable corners with no full liberalization anywhere in sight. Much of Todd’s book works through what the various options are here, and how they might apply to different parts of the world.

To be clear, half of this book is unsupported, or sometimes just trivial. There were several times I was tempted to just stop reading, but then it became interesting again. Todd covers a great deal of ground (the subtitle is A History of Humanity from the Stone Age to Homo Americanus), not all of it convincingly. But when he makes you think, you really feel he might be on to something.

Todd describes Germany as having a complex, multi-tiered, somewhat authoritarian family structure, and one that does not mesh well with the norms of feminism and individualism that have been entering the country. That family structure is also part of why Germany was, relative to its size, militarily so strong in the earlier part of the twentieth century. He also argues that the countries that stayed communist longer have some common features to their family structure, Cuba being the Latin American outlier in this regard.

Todd makes the strongest bullish case for Russia I have seen. He reports that TFR is back up to 1.8 after an enormous post-communist plunge, migration into the country is strongly positive, and Russia is very good at producing strong, productive women (again due to family structure). If you think human capital matters, the positives here are significant indeed.

Here is some related work by my colleagues Jonathan Schulz and Jonathan Beauchamp on cousin marriage.

You can order Todd’s book here. Recommended, though with significant caveats, mainly for lack of evidence on some of the key propositions.

The new Ben Horowitz management book

What You Do Is Who You Are: How to Create Your Own Business Culture. It is the best book on business culture in recent memory, here is one bit:

When Tom Coughlin coached the New York Giants, from 2004 to 2015, the media went crazy over a shocking rule he set: “If you are on time, you are late.” He started every meeting five minutes early and fined players one thousand dollars if they were late. I mean on time…”Players ought to be there on time, period,” he said. “If they’re on time, they’re on time. Meetings start five minutes early.”

And:

Two lessons for leaders jump out from Senghor’s experience:

-

Your own perspective on the culture is not that relevant. Your view or your executive team’s view of your culture is rarely what your employees experience.

You can pre-order the book here, due out in October.

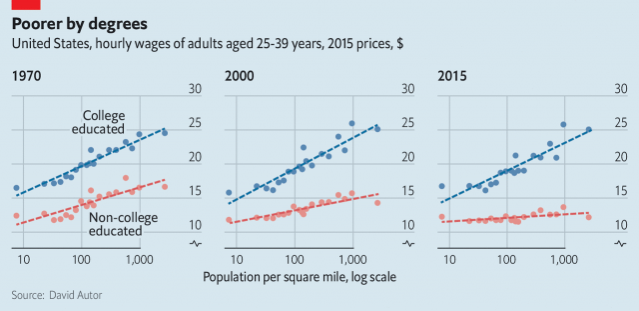

No Urban Wage Premium for Non-College Educated Workers

The Economist has a nice graph and article on the urban wage premium based on David Autor’s work. The graphs shown that in the past both college and non-college educated workers earned higher wages in more densely populated areas but today only college-educated workers experience an urban wage-premium.

Housing costs eat a large share of the college wage-premium so even college educated workers are not as better off in cities as the graphs make it appear. Autor’s point, however, is that wages for the non-college educated aren’t higher in cities so they might not move to cities even with lower housing costs. That could be true but I also suspect that the urban wage premium for the non-college educated is endogenous–firms employing these workers have moved out of the city but could move back in with lower housing and land costs.

Engagement with “fake news” on Facebook is declining

In recent years, there has been widespread concern that misinformation on social media is damaging societies and democratic institutions. In response, social media platforms have announced actions to limit the spread of false content. We measure trends in the diffusion of content from 569 fake news websites and 9,540 fake news stories on Facebook and Twitter between January 2015 and July 2018. User interactions with false content rose steadily on both Facebook and Twitter through the end of 2016. Since then, however, interactions with false content have fallen sharply on Facebook while continuing to rise on Twitter, with the ratio of Facebook engagements to Twitter shares decreasing by 60 percent. In comparison, interactions with other news, business, or culture sites have followed similar trends on both platforms. Our results suggest that the relative magnitude of the misinformation problem on Facebook has declined since its peak.

That is from a new NBER working paper by Allcott, Gentzkow, and Yu.

Twentieth-century cousin marriage rates explain more than 50 percent of variation in democracy across countries today.

That is the last sentence of the abstract in this job market paper, from Jonathan F. Schulz:

Political institutions vary widely around the world, yet the origin of this variation is not well understood. This study tests the hypothesis that the Catholic Church’s medieval marriage policies dissolved extended kin networks and thereby fostered inclusive institutions. In a difference-in-difference setting, I demonstrate that exposure to the Church predicts the formation of inclusive, self-governed commune cities before the year 1500CE. Moreover, within medieval Christian Europe,stricter regional and temporal cousin marriage prohibitions are likewise positively associated with communes. Strengthening this finding, I show that longer Church exposure predicts lower cousin marriage rates; in turn, lower cousin marriage rates predict higher civicness and more inclusive institutions today. These associations hold at the regional, ethnicity and country level. Twentieth-century cousin marriage rates explain more than 50 percent of variation in democracy across countries today.

Here is Jonathan’s (co-authored) working paper on “The origins of WEIRD psychology.“

Is innovation democracy’s unique advantage?

I say yes, though I don’t think it is easy to prove. Here is part of the abstract, from Rui Tang and Shiping Tang:

We contend that the channel of liberty‐to‐innovation is the most critical channel in which democracy holds a unique advantage over autocracy in promoting growth, especially during the stage of growth via innovation. Our theory thus predicts that democracy holds a positive but indirect effect upon growth via the channel of liberty‐to‐innovation, conditioned by the level of economic development. We then present quantitative evidence for our theory.

Via the excellent Kevin Lewis.

*Troublemakers: Silicon Valley’s Coming of Age*

That is the new and excellent history by Leslie Berlin, substantive throughout, here is one good bit of many:

In March 1967, Robert and Taylor, jointly leading a meeting of ARPA’s principal investigators in Ann Arbor, Michigan, told the researchers that ARPA was going to build a computer network and they were all expected to connect to it. The principle investigators were not enthusiastic. They were busy running their labs and doing their own work. They saw no real reason to add this network to their responsibilities. Researchers with more powerful computers worried that those with less computing power would use the network to commandeer precious computing cycles. “If I could not get some ARPA-funded participants involved in a commitment to a purpose higher than “Who is going to steal the next ten percent of my memory cycles?”, there would be no network,” Taylor later wrote. Roberts agreed: “They wanted to buy their own machines and hide in the corner.”

You can buy the book here, here is one good review from Wired, excerpt:

While piecing together a timeline of the Valley’s early history—picture end-to-end sheets of paper covered in black dots—Berlin was amazed to discover a period of rapid-fire innovation between 1969 and 1976 that included the first Arpanet transmission; the birth of videogames; and the launch of Apple, Atari, Genentech, and major venture firms such as Kleiner Perkins and Sequoia Capital. “I just thought, ‘What the heck was going on in those years?’ ” she says.

The problem with The Process, toward a theory of management

Re: the rebuilding attempts of the Philadelphia 76ers:

[John] Wall shed light on an underrated issue when he said: “The toughest thing you have is two young players that want to be great. Sometimes it might work, and sometimes it might not work.”

Think about that. Here’s what Wall is saying: It’s easier for stars to coexist when there is more separation of age and aspiration and an understanding of the hierarchy. Wall and Beal figured it out. The Sixers have three young potential all-stars trying to mix individual accolades and team success at once.

Wizards center Marcin Gortat cited asymmetric information:

“You know what the hardest thing for the young man is?” Gortat said during a recent interview. “We all enjoy diamonds. We all enjoy women. We all enjoy cars and beautiful houses, trips, the best parties and the life. The hardest thing is to come at 6 o’clock in the morning to the gym when nobody watches you. It’s easy to play when you have 20,000 people in the stands — women, cheerleaders, actresses, models, front-row celebrities — but it’s really hard to wake up at 6 o’clock in the morning and go to the gym and work on your left hand. This is the hardest part, when nobody’s watching.”

Here is the full Jerry Bewer story. I watched two games with Philadelphia and Milwaukee, to update my knowledge of the NBA a bit, and now I’ll return to my rabbit hole for a while.

Email exchange on bank leverage, regulation, and economic growth

Emailed to me:

What do you think would happen if we returned to a world where commercial bank leverage was much reduced? (E.g. 2X max.) Or, maybe equivalently, if central banks didn’t act as a lender of last resort? Is that “necessary” for a modern economy?

Asset prices would fall a lot (presumably). What else? How much worse off would current people become? (Future people are presumably somewhat better off, growth implications notwithstanding—they are less burdened with the other side of all these out-of-the-money puts that central banks have effectively issued.) > > How should we think about the optimization space spanning growth rates, banking capital requirements, and intergenerational fairness?

My response:

First, these questions are in those relatively rare areas where even at the conceptual level top people do not agree. So maybe you won’t agree with my responses, but don’t take any answers on trust from anyone else either.

I think of the liquidity transformation of banks in terms of two core activities:

a. Transforming otherwise somewhat illiquid activities into liquid deposits. That boosts risk-taking capacities, boosts aggregate investment, and makes depositors more liquid in real terms. Those are ex ante gains, though note that more risk-taking, even when a good thing, can make economies more volatile.

b. Giving private depositors more nominal liquidity, but in a way that raises prices and thus doesn’t really increase real, inflation-adjusted liquidity for depositors as a whole. There is thus a rent-seeking component to bank activity and liquidity production.

Less bank leverage, you get less of both. In my view a) is usually much more important than b). For those who defend narrow banking, 100% fractional reserves, or just extreme capital requirements, a) is usually minimized. Nonetheless b) is real, and it means that some partial, reasonable regulation won’t wreck the sector as much as it might seem at first.

There is however another factor: if bank leverage gets too high, bank equity takes on too much risk, to take advantage of bank creditors and possibly taxpayers too. Or too much leverage can make a given level of bank manager complacency too socially costly to bear. This latter factor seems to have been very important for the 2007-2008 crisis.

So bank leverage does need to be regulated in some manner, and the better it is regulated the more the system can dispense with other forms of regulation.

That said, the delta really matters. Requiring significantly less bank leverage, at any status quo margin, probably will bring a recession. The recession itself may make banks riskier than the lower leverage will make them safer. In this sense many economies are stuck with the levels of leverage they have, for better or worse. It is not easy to pop a “leverage bubble.”

I don’t find the idea of 40% capital requirements, combined with an absolute minimum of regulation, absurd on the face of it. But I don’t see how we can get there, even for the future generations. We’ll end up doing too many stupid things in the meantime; Dodd-Frank for all its excesses could have been much worse.

I also worry that 40% capital requirements would just push leverage elsewhere in the economy. Possibly into safer sectors, but I wouldn’t be too confident there. And reading any random few books on “bank off-balance sheet risk” will scare the beejesus out of anyone, even in good times.

Now, you worded your question carefully: “commercial bank leverage was much reduced.”

A lot of commercial bank leverage can be replaced by leverage from other sources, many less regulated or less “establishment.” Overall, on current and recent margins I prefer to keep leverage in the commercial banking sector, compared to the relevant alternatives. It may be less efficient but it is socially safer and held within the Fed’s and FDIC regulatory safety net, probably the best of the available politicized alternatives. That said, there is a natural and indeed mostly desirable trend for the commercial banking sector to become less important over time, in part because it is regulated and also somewhat static in basic mentality. (Note that the financial crisis interrupted this process, for instance Goldman taking up a bank charter. I would still bet on it for the longer run.)

Obviously, VC markets are a possible counterfactual. This all gets back to Ed Conard’s neglected and profound point that “equity” is what is scarce in economies, and how many troubles stem from that fact. Ideally, we’d like to organize much more like VC markets, partly as a substitute for bank leverage and the accompanying distorting regulation, and maybe we will over time, but there is a long, long way to go.

One big problem with attempts to radically restrict bank leverage is that they simply shift leverage into other parts of the economy, possibly in more dangerous forms. Should I feel better about commercial credit firms taking up more of this risk? Hard to say, but the Fed would not feel better about that, it makes their job harder. This gets back to being somewhat stuck with the levels of leverage one already has, until they blow up at least. There are pretty much always ways to create leverage that regulators cannot so easily control or perhaps not even understand. Again this bring us back to “off-balance risk,” among other topics including of course fintech.

I view central banks as “lenders of second resort.” The first resort is the private sector, the last resort is Congress. I favor empowering central banks to keep Congress out of it. Central banks are actually a fairly early line of defense, in military terms. And I almost always prefer them to the legislature in virtually all developed countries.

I fear however that we will have to rely on the LOLR function more and more often. Consider how it interacts with deposit insurance. If everything were like a simple form of FDIC-insured demand deposits, FDIC guarantees would suffice.

But what if a demand deposit is no longer so well-defined? What about money market funds? Repurchase agreements? Derivatives and other synthetic positions? Guaranteeing demand deposits is a weaker and weaker protection for the aggregate, as indeed we learned in 2008. The Ricardo Hausmann position is to extend the governmental guarantees to as many areas as possible, but that makes me deeply nervous. Not only is this fiscally dangerous, I also think it would lead to stifling regulation being applied too broadly.

But relying more and more on LOLR also makes me nervous. So I view this as a major way in which the modern world is headed for recurring trouble on a significant scale, no matter what regulators do.

I am never sure how much of the benefits of banking/finance are “level effects” as opposed to “growth effects.” It is easy for me to believe that good banking/finance enables more consumption at a sustainably higher level, in part because precautionary savings motives can be satisfied more effectively and with less sacrifice. I am less sure that the long-term growth rate of the economy will rise; if so, that does not seem to show up in the data once economies cross over the middle income trap. That said, if there were an effect, since growth rates slow down with high levels in any case, I don’t think it would be easy to find and verify.

Tesla’s Damaged Goods Problem

TechCrunch: Tesla has pushed an over-the-air update to some of its vehicles in Florida that lets those cars go just a liiiittle bit farther, thus helping their owners get that much farther away from the devastation of Hurricane Irma.

Tesla owners in Florida may be grateful for this mileage boost as they escape the ravages of Irma but I suspect that some of them will be upset when they have more time to reflect. How could Tesla increase the mileage at the flick of a switch? The answer is that owners of the Tesla 60kWh version of its Model S and Model X actually have the same battery as the 75kWh vehicles but the battery has been purposely limited or “damaged” to provide only 60KWh of mileage. But why would Tesla damage its own vehicles?

The answer to the second question is price discrimination! Tesla knows that some of its customers are willing to pay more for a Tesla than others. But Tesla can’t just ask its customers their willingness to pay and price accordingly. High willing-to-pay customers would simply lie to get a lower price. Thus, Tesla must find some characteristic of buyers that is correlated with high willingness-to-pay and charge more to customers with that characteristic. Airlines, for example, price more for the same seat if you book at the last minute on the theory that last minute buyers are probably business-people with high willingness-to-pay as opposed to vacationers who have more options and a lower willingness-to-pay. Tesla uses a slightly different strategy; it offers two versions of the same good, the low and high mileage versions, and it prices the high-mileage version considerably higher on the theory that buyers willing to pay for more mileage are also more likely to be high willingness-to-pay buyers in general. Thus, the high-mileage group pay a higher price-to-cost margin than the low-mileage group. A familiar example is software companies that offer a discounted or “student” version of the product with fewer features. Since the software firm’s costs are mostly sunk R&D costs, the firm can make money selling a low-price version so long as doing so doesn’t cannibalize its high willingness-to-pay customers–and the firm can avoid cannibalization by carefully choosing to disable the features most valuable to high willingness-to-pay customers.

The answer to the second question is price discrimination! Tesla knows that some of its customers are willing to pay more for a Tesla than others. But Tesla can’t just ask its customers their willingness to pay and price accordingly. High willing-to-pay customers would simply lie to get a lower price. Thus, Tesla must find some characteristic of buyers that is correlated with high willingness-to-pay and charge more to customers with that characteristic. Airlines, for example, price more for the same seat if you book at the last minute on the theory that last minute buyers are probably business-people with high willingness-to-pay as opposed to vacationers who have more options and a lower willingness-to-pay. Tesla uses a slightly different strategy; it offers two versions of the same good, the low and high mileage versions, and it prices the high-mileage version considerably higher on the theory that buyers willing to pay for more mileage are also more likely to be high willingness-to-pay buyers in general. Thus, the high-mileage group pay a higher price-to-cost margin than the low-mileage group. A familiar example is software companies that offer a discounted or “student” version of the product with fewer features. Since the software firm’s costs are mostly sunk R&D costs, the firm can make money selling a low-price version so long as doing so doesn’t cannibalize its high willingness-to-pay customers–and the firm can avoid cannibalization by carefully choosing to disable the features most valuable to high willingness-to-pay customers.

The classic paper in this literature is Damaged Goods by Deneckere and McAfee who write:

Manufacturers may intentionally damage a portion of their goods in order to

price discriminate. Many instances of this phenomenon are observed. It may

result in a Pareto improvement.

Note the last sentence–damaging goods can be beneficial to everyone! Consider: Without selling to the high willingness-to-pay customers at the high price the good might not be produced at all because the profit from customers who are only willing to buy at a discount aren’t enough to support the R&D. Thus, the high willingness-to-pay customers aren’t worse off from the existence of a discounted version and the low willingness to pay customers and the firm are clearly better off.

Unfortunately, I fear that Tesla may have made a marketing faux-pas. When it turns off the extra mileage boost are Tesla customers going to say “thanks for temporarily making my car better!” Or are they going to complain, “why are you making MY car worse than it has to be?”

Hat tip: Monique van Hoek.

Robin Hanson updates his forager vs. farmer schema

The post is interesting throughout, here are the closing paragraphs:

The left is more okay with people forming distinct subgroups, even as it thinks more in terms of treating everyone equally, even across very wide scopes, and including wide scopes in more divisive debates. The right wants to make redistribution more conditional, more wants to punish free riders, and wants norm violators to be more consistently punished. The left tends to presume large scale cooperation is feasible, while right tends to presume competition more. The left hopes for big gains from change while the right worries about change damaging things that now work.

Views tend to drift leftward as nations and the world gets richer. Left versus right isn’t very useful for prediction individual behavior outside of politics, even as it is the main parameter that robustly determines large scale political ciliations. People tend to think differently about politics on what they see as the largest scales; for example, there are whole separate fields of political science and political philosophy, which don’t overlap much with fields dealing with smaller scale politics, such as in clubs and firms.

I shouldn’t need to say it but I will anyway: it is obvious that a safe playful talky collective isn’t always the best way to deal with things. Its value varies with context. So sometimes those who are more reluctant to invoke it are right to be wary, while at other times those who are eager to apply it are right to push for it. It is not obvious, at least to me, whether on average the instincts of the left or the right are more helpful.

Do read the whole thing.