Category: Current Affairs

Is America ruled by an oligarchy?

Any time you hear claims about American government, a sanity-inducing response is to ask whether they also are true of state and local governments. Here is an excerpt from my latest piece at The Free Press:

First, in people’s daily lives, they typically interact with their state and local governments more than with the feds. And if you look at what state and local governments do, most of it is driven by voter demand, and I do not mean billionaire or oligarchic voters.

Most state and local government spending goes toward schools, roads, and increasingly, Medicaid. None of those reflect the agendas of most billionaires. For example, Medicaid dollars flow particularly to lower-income recipients. Hospitals and doctors receive income from this program, but reimbursement rates are relatively low, and many of the best doctors do not accept Medicaid patients and don’t make a living from the program.

Somehow the oligarchy saw fit to leave these expenditures alone. Looking at the state and local level also suggests that America — with some notable exceptions — is better governed than before.

Words of wisdom on Chinese AI and our responses

The strategy for China is obvious: commoditize your complements. Note that Xi explicitly ties openness to AI “moving from the digital world into the physical world”; the physical world is the world dominated by China, and the country’s lead in areas like robotics is going to massively benefit from widely available AI models.

Along the same lines, China does not want the U.S. to gain an asymmetric advantage in AI; to the extent that China can weaken the U.S. frontier labs while strengthening any and all potential U.S. adversaries so much the better, and it can benefit from the innovation that will attach itself to an open ecosystem.

And in sum:

The better course is clear: first, loosen Fable and Sol restrictions on cybersecurity, and second, ensure that U.S. open weight model makers are on an equal playing field with China. Yes, the frontier labs will kick and scream about this, but the Administration should realize that listening to their histrionics has led the U.S. to a position where U.S. companies are dependent on China for their defenses. Let the frontier labs win by being better; don’t let them define safety or security, or pull up the ladder of humanity’s collective knowledge. China is already hard enough to compete with; letting them carry the standard for openness and innovation is simply giving away our biggest advantage.

That is from Ben Thompson’s Stratechery (gated, but ungated link here).

The small business boom

Across the country, founders like Ms. Winkler are powering an entrepreneurial renaissance.

Jump-started by the pandemic, when a confluence of factors including mass layoffs and remote work led to a flood of business creation, and supercharged by the rise of artificial intelligence, start-up activity is booming after a decades-long slump.

Americans filed 5.7 million applications last year to start new businesses, according to the Census Bureau, the most in the two decades the government has kept track. New business applications through the first half of this year continued to climb…

More recently, there are signals that A.I. is adding fuel.

A recent paper from economists at the University of British Columbia and the Stockholm School of Economics found that generative A.I. was “spurring entrepreneurial activity” in the United States, both by giving rise to new ventures built around the technology and by making it cheaper to start enterprises.

“A.I. tools can do very many different things very well,” said Jan Bena, an associate professor at the University of British Columbia and one of the study’s authors. “That’s the reason why you see so much entry.”

According to a recent report from Gusto, a small-business payroll and benefits service, nearly 60 percent of founders on its platform who started businesses last year said they used A.I., and half said the technology made it cheaper and faster.

Here is more from Sydney Ember at the NYT. Via Josef.

The Equal Pay Madness Just Got Madder

In my post Equality Act 2010 I discussed the UK’s absolutely insane wage policy:

In short, supply and demand have been replaced by judges and labor boards with the authority to deem which jobs are “equal” and therefore should be paid equally….No one is alleging that male and female warehouse workers were paid unequally or that male and female retail workers were paid unequally or that there was any direct or indirect discrimination. The only claim is that warehouse workers, who are less likely to be female than retail workers, earn more than retail workers. And since these jobs have been judged “equal,” the company has violated Equality Act 2010.

…The warehouse workers were almost 50% female (47.25%). So females were not barred from the higher paying jobs. The fact that 77.5% of the retail workers were female suggests that retail work has special appeal to females relative to males and thus that there are compensating differentials. Any of the three female plaintiffs could have taken jobs in the warehouse. If the jobs are equal and the warehouse jobs pay more this is, on the plaintiffs’ theory, “puzzling”. [Or, as Ayn Rand would say, blank out.]

In fact, the court case reveals that Next was struggling to fill the warehouse positions and offered any retail employee—including the plaintiffs—the opportunity to switch to warehouse work. On cross-examination, one of the plaintiffs admitted that, given the unpleasant conditions in the warehouse—described by the court as “the drone of machinery,…vibration, alarm sirens and the screeching of machinery, wheels and rollers, continuously present in all areas”—the warehouse job “did not seem particularly attractive” compared to the greater autonomy and more appealing environment of the retail job. The plaintiff added that she would only have considered the warehouse job if it paid “a lot more money.”

Well, here is the update. The outgoing Keir Starmer government is trying to massively expand these laws. The “equal value” framework previously applied only to sex discrimination; under the proposed law, employees could also bring equal-value claims based on race and disability. Remember, these laws have nothing to do with discrimination—they are about demanding, at the point of a gun, that apples and oranges sell for the same price because they’re both fruit.

The new law would also establish an Equal Pay Regulation and Enforcement Unit. As I said, Orwellian.

See also my post, How Britain Become as Poor as Mississippi.

Toward a theory of uni-context

Here is a good dialogue between Derek Thompson and Agnes Callard, excerpt:

Callard: In general, goodness is more context-dependent than badness. There isn’t really anything that’s good all the time for everyone independent of context. Happiness depends on your context and who you are. There isn’t anything that will always make a person happy. But there are reliable ways to make people unhappy. There’s a set of evils that are close to universal: death, pain, illness, violence. Even if someone’s in very different circumstances from yours, if you see they’re being subjected to one of those, you can interpret it as suffering and understand it.

So we should predict that what we see on the internet, insofar as people are trying to be legible to large groups, is that they focus their attention on things that show up to everyone. Take two strangers on the internet trying to talk to each other. What are they going to coordinate on as a topic they can both care about? It’s likely going to be something bad.

And here is from Derek:

Here are some questions that I consider self-evidently compelling about the modern world:

- Why is the news media so interested in telling you how much the world sucks all the time?

- Why are so many of us obsessed with distraction and managing our attention?

- Why is it so hard to stop comparing ourselves to others?

- And why does everything in art and design seem the same these days?

And more from Agnes:

With identity categories like woman, disabled, gay, Jewish, or American, the striking thing is that you are a member of those categories in every circumstance. There is no circumstance in which I stop being a woman. Identity is a hat you never take off. So identity is well suited to a uni-contextual world.

Worth pondering, interesting throughout.

The wisdom of Conor Sen

The age 20-24 unemployment rate is now ~unchanged since the AI boom began…

Link and picture here.

New space policy Substack from Mercatus

We are Rebecca, Max, and Aakrith. We are researchers at The Mercatus Center, a research organization dedicated to classical liberal ideas. Rebecca is a philosopher, Max is an economist, and Aakrith is a political scientist. Together, we are the Space Team, and this is our Substack.

We’re here to persuade you that space policy is increasingly important. And that getting space policy right offers humankind astonishing opportunities. In particular, we’re currently thinking hard about innovation, competition, federalism, property rights, and life in space.

Here is the link.

Andrew Hall is on a roll

He is one of the new(ish) thinkers on the rise, here is his latest piece. Excerpt:

For most of the past decade, anti-billionaire language was a niche product. Democratic emails invoked billionaires in the mid-single digits through 2017 and 2018, spiked briefly to around 14 percent during the Warren and Sanders primary surge in 2019, and then settled back down—through the entire Biden presidency, the billionaire appeared in roughly one of every twenty to twenty-five Democratic fundraising emails, barely more than in Republican ones.

Then came January 2025. In the weeks after an inauguration that seated tech CEOs in the front row and the dizzying drama of Elon Musk’s ill-fated DOGE experiment, billionaire mentions in Democratic emails quadrupled, peaking above 20 percent of all emails sent and holding around 15 percent ever since. Anti-billionaire fundraising tactics are now a mainstay of Democratic messaging.

Yes, billionaire derangement syndrome is now a thing. As a side note, I was told that Andrew is the son of the great economist Robert E. Hall of Stanford.

Just wondering what the correct model of Iran is here

Prior to the war, I linked to a tweet from Matt Yglesias which explained why Matt opposed the war, and I expressed my agreement with his stance. While I feel plenty has gone on which I do not observe, I can report that the course of the war did not change my initial assessment.

Then I read many, many commentators saying how good the final deal was for Iran, and what a major loss it was for Trump. I was never sure I understood all of the parameters of the full deal, but still I did not hold any directly contrary opinion to that.

And now I see Iran is attacking ships in the Strait again, talking openly and brazenly about building nuclear weapons, and making plans to have tolls/fees on the Strait. To be clear, only the first of those surprises me, the latter two do not.

But given their reckless behavior in what is supposedly a wonderful war outcome for them, what is the correct way to model what they would have done had Trump and Netanyahu not attacked? And what is the correct way to model our optimal response to that? The terrible things that are happening now, do they not reflect an underlying equilibrium that would have emerged anyway within a few years’ time, or do we hold some hypothesis here of extreme path-dependence, suggesting the Iranian government would have been less bellicose on more or less a permanent basis? To cite one particular example of a possible equilibrium, if drones permanently alter the balance of power in the region, the ways in which their current position is now more aggressive might have emerged in any case. Or if the military have the strength to be the natural successors to the mullahs, might that not have happened over time anyway?

I do not see many war critics engaging with these questions openly and explicitly. It seems to me that the war critics implicitly are relying on a model of extreme path-dependence for Iran’s behavior. Had Trump not attacked, they might have stayed in a more peaceful groove for some while to come. That model might be true, but I do not feel I know enough about Iranian politics to make that judgment. Why are the others so convinced that model is true? Are they such well-informed experts? Is it that they have the properly sunny sense of the underlying Iranian disposition? Inquiring minds wish to know.

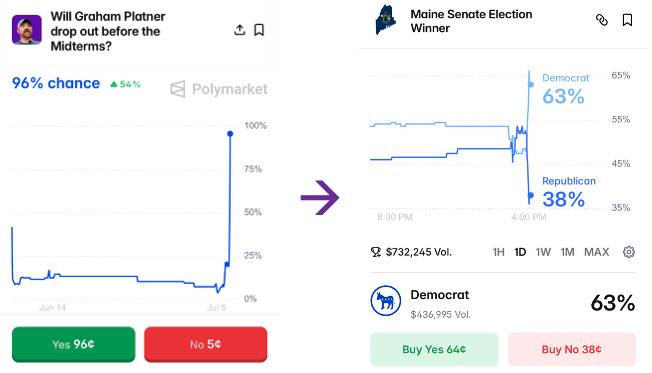

From Prediction Markets to Decision Markets and Beyond!

Arin Dube points to a great illustration of the power of prediction markets. Yesterday due to a new scandal the probability that Graham Platner would drop out of the Maine Democratic primary exploded from 9% to 96% (+87 percentage points). At the same time, the probability that the Democrats would win the election jumped by about 9 percentage points, from 54% to 63%. What does this tell you?

The market is signaling that Platner reduces the Democrats’ chances of victory. We can be more precise. If an 87-point increase in the probability of dropping out gets you 9 points of winning, then a 100% chance of dropping out implies a gain of 9/0.87 ≈ 10.3 percentage points.

The market is signaling that Platner reduces the Democrats’ chances of victory. We can be more precise. If an 87-point increase in the probability of dropping out gets you 9 points of winning, then a 100% chance of dropping out implies a gain of 9/0.87 ≈ 10.3 percentage points.

Thus the market’s best estimate is that Platner is reducing the Democrats’ chance of winning by about 10 percentage points (compared to an unknown replacement). That’s a pretty big number! Democrats should surely use this information to make better decisions.

Now, I have been a bit loose. We have implicitly assumed that the news mainly moved the probability of Platner dropping out, rather than independently changing the Democrats’ general-election prospects. The issue is we are trying to reverse engineer two conditional prices, P(win|drop) and P(win|stay), from one unconditional price, P(win), and its comovement with P(drop). It works pretty well here as an illustration but Robin Hanson’s idea is that we can do better yet by trading the conditionals instead of inferring them.

Hanson’s decision markets would run contracts of the form “pays $1 if Democrats win, conditional on Platner dropping out — bet refunded if he stays.” Plus the mirror contract conditioned on staying. The refund provision makes the price a conditional probability: a trader pricing the first contract doesn’t need any view on whether Platner drops out, only on how the race goes if he does. With this structure we would get cleaner estimates of the conditional probabilities–in this case whether the Democrats do better with Platner in or out–which is exactly what a decision maker needs.

We were able to plausibly reverse engineer our estimate because the market happened to move 87 points in a single day. But a decision market would have posted the number continuously, no scandal required. In other words, with decision markets in play, not just prediction markets, we could have seen how much Platner was costing the Democrats before the latest scandal hit—which is precisely when the information would have been most useful.

It’s been fun to see prediction markets catch on with the public but the world is still decades behind Hanson’s decision markets—let alone futarchy!

Wiesbaden notes

Who goes to Wiesbaden these days? The era of Russian nobles taking the cure here and gambling is long since gone. And yet here we are. The proximate cause of this trip is the desire to see Grigory Sokolov, one of the world’s great pianists and a cult figure of sorts. He rarely tours North America, maybe these days never as he is 76. The current program includes Beethoven’s fourth piano sonata, Beethoven’s Op.126 Bagetelles, and Schubert’s last piano sonata. How can one say no? Sokolov also was a favorite of Tom Schelling, I might add, especially his recording of The Art of the Fugue, in my view one of the best classical music recordings of all time.

Besides, I have long been a believer in semi-random excursions to mid-size, slightly neglected German cities. There remains a strong cultural federalism in Germany, and so you might see and hear wonderful things in many different parts of the country.

I perceived two difficult Wiesbadens. In one, if you walk through the cheaper part of the pedestrian zone in the evening, the city seems mostly Muslim. But if you walk around during the morning, the city seems mostly German. I might add that some of the younger Muslim women show signs of assimilating, at least based on how they dress and present themselves. The older women tend to stick with the headscarves.

Over the last twenty years, inflation-adjusted real estate prices in Wiesbaden have gone up about forty percent, an OK performance. At times the city “does not feel like Germany any more,” but I think it is holding on. The proportion of new building is roughly equal to the population growth, so I do not think this price effect is a NIMBY effect. Rather it reflects the fact that Wiesbaden is still a pretty nice place to live. that said, in some significant ways Germany in the traditional sense is failing to reproduce itself.

It was stunning to me to discover how hard it is, in most of the downtown, to find plain, ordinary German food. At any price level. There is no current equivalent of Wienerwald or Nordsee to be seen, never mind a decent Wiener Schnitzel.

Much of Wiesbaden was destroyed and rebuilt, but the best fifteen or twenty buildings show the previous wealth and splendor to good effect. You will see these gems walking around, though only periodically. There is also an old Roman wall and a moving, more recent Holocaust memorial.

Most German ice cream just isn’t that good, so try L’Art Sucre for something French.

Museum Reinhard Ernst is the new institution in town, and it specializes in color field abstract art. The building is impressive, but the collection is weak except for a few Stellas. Why organize a museum around that basis unless the underlying collection is super strong in that area? This one is not. I can forgive the absence of the expensive American Ellsworth Kelly, but no Blinky Palermo or Günther Förg?

Nonetheless their restrooms might forestall this kind of Larry David conflict:

(At Museum Ludwig in Köln, by the way, you get the discount for being disabled only if you have “fifty degrees of disability,” however they might measure that. Slight disabilities are not enough, you must be truly “schwerbehinderte,” as judged by the state, heaven forbid the museum rely on the honor system.)

Museum Wiesbaden in contrast was an unexpected delight. Although it is mainly a natural history museum, they have one of the world’s best collections of Art Nouveau and the single best Jawlensky collection, and you can have these all to yourself. Very few people seem to go there.

As for the economy, here are some Germany facts of the day. Yet Germany continues, and visits remain a source of pleasure and interest.

Sokolov, by the way, played six encores. Where should the Germany trip target next year?

The Troubled History of Government Equity in Technology

Even though Germany privatized Deutsche Telekom in 1996, the federal government retained a substantial ownership stake. This partial state ownership status, which remains to this day, presents a textbook example of how this type of arrangement distorts incentives and delays the competitive dynamism necessary for technological progress.

Through the late 1990s and into the 2000s, Deutsche Telekom was buttressed by its privileged position and implicit government backing and leveraged this support to resist infrastructure competition. Rather than aggressively deploying broadband in order to compete with rivals, the company lobbied for regulatory arrangements that protected its legacy copper network. As a result, Germany—one of the world’s largest economies and a hub of engineering excellence—consistently trailed other European competitors in broadband deployment. To see German broadband stagnate while the competitive markets in Scandinavia and other European countries surged ahead was particularly jarring, as Germany had directly linked its economy to workplace digitization.

Germany’s broadband woes did not result from a lack of capital or engineering talent at Deutsche Telekom. Instead, government ownership produced a fundamental alteration of the company’s incentive structure. With state backing, Deutsche Telekom had fewer reasons to take risks, cannibalize its own infrastructure, or accept short-term losses in favor of long-term technological leadership and more reasons to cultivate political relationships that protected their existing revenue streams. This dynamic is reliably produced by partial government ownership of private companies.

Why we love this country

A Free Press feature for the 250th, here is my entry:

Tyler Cowen can’t decide, so he picks about 20 things instead.

My favorite thing about America is that I do not have a single favorite thing. We have the NBA (with a Toronto team too), the world’s best AI models, Alexander Calder sculptures, a few wonderful R.E.M. albums, southern Utah, the world’s best Constitution, lots of air-conditioning, sausage in southwest Louisiana, the infield fly rule in baseball, Winslow Homer, Sioux Plains drawings and Navajo blankets, the music of Chuck Berry and Brian Wilson, cheeseburgers, deep capital markets, the world’s best universities, the Museum of Modern Art, Chattanooga, Tennessee, lots of big airports, the north rim of the Grand Canyon, red cardinals and blue jays, about two dozen cities and towns named Paris, self-driving vehicles, not just one but two Dakotas, three branches of government (I hope not four), and the best set of immigrants in the world. And that is just scratching the surface.

The other contributors are notable as expected.

The most profitable crypto investors and firms

Here is the source. Here is from the editors at The Free Press. Here is more from Mene Ukueberuwa.

How Britain Became as Poor as Mississippi

How Britain Became as Poor as Mississippi is a good piece in the Atlantic by Idrees Kahloon filled with colorful anecdotes of a nation in decline:

The health service now has to spend more money settling maternity-malpractice claims than it does on actually providing maternity care. Many Brits can neither obtain an appointment with a publicly funded dentist nor afford a private one; in a 2023 survey, one in 10 reported doing DIY dental work, in extreme cases extracting their own teeth or gluing broken crowns back together.

Incomes can be shockingly low: Junior doctors recently went on strike for the 15th time in three years over their salaries, which start at just £38,800; the median salary for British civil servants is £35,680. In April, amid the Iran conflict, the Daily Mail pounced on Prime Minister Keir Starmer for vacationing in Valencia, Spain, at what the tabloid described as a luxury hotel, costing £200 a night.

Americans are likely to come away a bit smug, especially as Independence Day approaches and Europeans are enjoying our giant stadiums and central air conditioning. Look deeper, however, and Britain’s story becomes more uncomfortable. Does this sound familiar?

Recent plans to transform the country have rested in no small part on High Speed 2, a superfast rail line intended to connect London with Birmingham, Leeds, and Manchester. But since HS2 was proposed, in 2009, its costs have tripled, to more than £100 billion. It is the most expensive rail line in the world. (A special structure to protect a rare bat species near the rail line in Buckinghamshire required 8,000 permits and was built at a cost of £216 million.) The most important sections of the proposed route have been lopped off. The rump line—going from Birmingham, Britain’s second-largest city, to not-quite-central London—may be finished by 2040…. HS2 has been delayed for so long that two swiftly built towers near the terminus now themselves look derelict and in need of demolition.

…Building infrastructure, or much of anything else, has become all but impossible in the United Kingdom. In addition to having the world’s most expensive (not yet built) train line, Britain also hosts the world’s most expensive (not yet built) nuclear-power plant, Hinkley Point C. Its environmental-impact assessment ran 31,401 pages; the plant will feature a £700 million “fish disco,” which will pulse sounds underwater to deter animals from its intake pipes.

Upon closer inspection, the United States looks a lot less like a shining city on a hill and a lot more like a declining Great Britain, appendaged with one or two dynamic sectors, most notably AI. The similarities are especially obvious in the retrograde solutions Britain has lumbered into, namely attacking immigrants and trade—Brexit being the equivalent of a high tariff regime. Nations in decline, like people, tend to lash out at others rather than deal with their real problems. Needless to say, neither immigrants nor trade explain Britain’s—or California’s—inability to build high-speed rail or other infrastructure.

It is discomforting to watch the birthplace of the Industrial Revolution, individual rights, and free speech—the nation that once built the railways, the steam engines, the factories that remade the world—lose the capacity to build much of anything, or even to tolerate people speaking their minds. In parallel, instead of dealing with our real problems—almost all of our creation—the right gets literally hysterical over symbolic culture-war questions like birthright citizenship, while the left nominates candidates with Marxist-Leninist sympathies. The abundance and progress movements are some of the few shining lights. It’s not too late. But Great Britain is a warning.