Month: May 2014

How is income inequality correlated with wealth inequality?

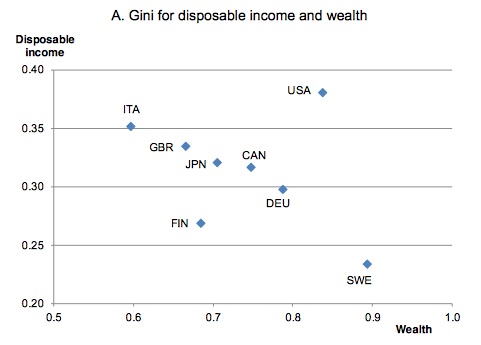

From the OECD, Kaja Bonesmo Frederiksen writes on “More income inequality and less growth” and presents this table:

If you were to fit that with a curve, the overall slope would be negative, suggesting a negative empirical correlation between income inequality and wealth inequality. Now do not leap to a conclusion here, as there are points to be made:

1. This scatter plot is not based on a model with adjustments for confounding factors.

2. These may not be the right or best data on wealth inequality.

3. There are not many data points on this graph in the first place.

4. Lots of other stuff.

The point is that everyone is talking about wealth inequality lately, yet it is not always recognized that the relationship between wealth and income inequality is complex, as illustrated for instance by the case of Sweden. (There is nothing in this post by the way which should be construed as criticism of Piketty, I’m just trying to lay out some basic expository principles.)

Wealth inequality and income inequality may diverge for at least three reasons. First, savings rates may differ across societies. Second, locally available rates of return may differ. Third, the ups and downs of mobility may mean high income inequality in a given year but overall lower levels of wealth inequality.

By the way, here is a good sentence from the abstract:

Wealth dispersion [inequality] is especially high in the United States and Sweden

The support document is here, I have reproduced Figure 3a. Hat tip goes to Luis Pedro Coelho.

Pi.rate

The latest example of Intellectual Privilege running out of control is a guy who trademarked the symbol Pi with a period afterwards. Here is Jez Kemp:

Designers are in uproar and filing counter notices after print company Zazzle upheld a man’s claim to own the pi symbol on clothing.

Paul Ingrisano, a pirate living in Brooklyn New York, filed a trademark under “Pi Productions” for a logo which consists of this freely available version of the pi symbol π from the Wikimedia website combined with a period (full stop). The conditions of the trademark specifically state that the trademark includes a period.

The trademark was granted in January 2014 and Ingrisano has recently made trademark infringement claims against a massive range of pi-related designs on print-on-demand websites including Zazzle and Cafepress.

Surprisingly, Zazzle accepted his claim and removed thousands of clothing products using this design, emailing designers that their work was infringing Pi Productions’ intellectual property – even designs not using a full stop.

At first Zazzle’s Content Review team responded to their very angry designers and store keepers with generic emails, suggesting they file counter notices if they felt aggrieved.

But now Zazzle’s latest response is that they are acting to protect Paul Ingrisano’s “intellectual property” from “confusingly similar” designs as under the Lanham Act 1946 – including designs which do not even contain the pi symbol, but just the word “pi” in their design name.

I don’t expect this particular outrage to last but as with absurd patents the real outrage is that this does accurately represent the law as it exists today.

Should Scotland leave the UK?

I very much agree with the recent FT columns by Martin Wolf and Simon Schama. The Union of 1707 was one of the great events of the eighteenth century for Britain, and it paved the way for the Industrial Revolution, Adam Smith, David Hume, John Stuart Mill, and much much more, including the later United States and many of the Founding Fathers. And yes some of the excesses of imperialism, exploration too. That union truly was a cornerstone of the modern world, of the sort they might put into a book subtitle in a corny way and yet it would be quite justified.

Maybe you think the partnership hasn’t been as fruitful in recent years. Still, I view it this way. For all its flaws, the UK remains one of the very best and most successful countries the world has seen, ever. And there is no significant language issue across the regions, even though I cannot myself understand half of the people in Scotland. Nor do the Scots have a coherent or defensible answer as to which currency they will be using, or how they would avoid domination by Brussels and Berlin. If a significant segment of the British partnership wishes to leave, and for no really good practical reason, it is a sign that something is deeply wrong with contemporary politics and with our standards for loyalties.

I find this entire prospect depressing, and although it is starting to pick up more coverage in the United States and globally, still it is an under-covered story relative to its importance.

This is a referendum on the modern nation-state, an institution that has done very well since the late 1940s but which is indeed often ethnically heterogeneous at its core. While I expect Scottish independence to be voted down, if it passes I will feel the world’s risk premium has gone up, even if the Scots manage to make independence work.

Addendum: Is this the sort of debate that the great British Parlamentarians of history would have approved of?:

Alex Salmond, Scotland’s first minister who is leading the campaign for independence, said on Wednesday that each household would receive an annual “independence bonus” of £2,000 – or each individual £1,000 – within the next 15 years if the country votes to leave the UK.

The UK government, in contrast, claimed that if Scots rejected independence each person would receive a “UK dividend of £1,400 . . . for the next 20 years”.

Was that the sort of discourse you wanted? Was “being British” simply not good enough for you?

Economics and Religion, at Econ Journal Watch

The new issue of Econ Journal Watch is online at http://econjwatch.org

In this issue:

A symposium co-sponsored by the Acton Institute:

Does Economics Need an Infusion of Religious or Quasi-Religious Formulations?

The Prologue to the symposium suggests that mainstream economics has unduly flattened economic issues down to certain modes of thought (such as ‘Max U’); it suggests that economics needs enrichment by formulations that have religious or quasi-religious overtones.

Robin Klay helps to set the stage with her exploration “Where Do Economists of Faith Hang Out? Their Journals and Associations, plus Luminaries Among Them.”

Seventeen response essays are contributed by authors, representing a broad range of religious traditions and ideological outlooks:

Pavel Chalupníček:

From an Individual to a Person: What Economics Can Learn from Theology About Human Beings

Victor V. Claar:

Joyful Economics

Charles M. A. Clark:

Where There Is No Vision, Economists Will Perish

Ross B. Emmett:

Economics Is Not All of Life

Daniel K. Finn:

Philosophy, Not Theology, Is the Key for Economics: A Catholic Perspective

David George:

Moving from the Empirically Testable to the Merely Plausible: How Religion and Moral Philosophy Can Broaden Economics

Jayati Ghosh:

Notes of an Atheist on Economics and Religion

M. Kabir Hassan and William J. Hippler, III:

Entrepreneurship and Islam: An Overview

Mary Hirschfeld:

On the Relationship Between Finite and Infinite Goods, Or: How to Avoid Flattening

Abbas Mirakhor:

The Starry Heavens Above and the Moral Law Within: On the Flatness of Economics

Andrew P. Morriss:

On the Usefulness of a Flat Economics to the World of Faith

Edd Noell:

What Has Jerusalem to Do with Chicago (or Cambridge)? Why Economics Needs an Infusion of Religious Formulations

Eric B. Rasmusen:

Maximization Is Fine—But Based on What Assumptions?

Rupert Read and Nassim Nicholas Taleb:

Religion, Heuristics, and Intergenerational Risk Management

Russell Roberts:

Sympathy for Homo Religiosus

A. M. C. Waterman:

Can ‘Religion’ Enrich ‘Economics’?

Andrew M. Yuengert:

Sin, and the Economics of ‘Sin’

Assorted links

The Invisible Hand of Eco-nomics

Cap and trade is going nowhere at the federal level but the California program is large and expanding and the CA program allows for properly monitored and regulated offsets to be purchased from anywhere in the United States. As a result, a price on carbon is being established nationally. As the NYTimes indicates in a very good article, once a market and a price have been established, contentious politics turns into mutually beneficial economics.

Experts who support cap and trade contend that a market mechanism can reach more deeply into the economy than any other approach, changing the behavior even of people and companies that might not necessarily care about global warming.

The Wisconsin dairymen perhaps serve as an example of that.

Even as the methane-powered generator roared on his property, John T. Pagel said he was not convinced that the climatic changes happening in the United States were a result of human emissions. He suspects they might be part of a natural cycle. But with Californians dangling cash in exchange for his willingness to cut emissions, he jumped at the chance to build his digester.

“We are doing exactly what they asked us to do to get paid to reduce carbon,” Mr. Pagel said. “If somebody else believes in it enough to put up the money, that’s all I need to know.”

What does low volatility in asset prices mean?

The excellent Gillian Tett has some interesting (and speculative) thoughts on this question, putting a new twist on Hayek:

But there is a second, less benign possible reason for low volatility: markets have been so distorted by heavy government interference since 2008 that investors are frozen. One issue that may account for the pattern, for example, is that tougher regulations have prompted banks to stop trading some assets. Another is that ultra-low interest rates have made investors reluctant to deploy their cash in public, liquid markets.

And there could be a more subtle issue at work too: investors are so unsure what to make of this level of government interference that they are unwilling to take any big bets. Far from being a sign of sunny confidence in the future, ultra-low volatility may show that investors have lost faith that markets work.

In reality, nobody knows which of these explanations holds true; I suspect that government meddling and low interest rates are the key factors here, but academic research on this issue is thin. However, one thing that is clear is that the longer this pattern remains in place, the more wary investors and policy makers should be.

The rest of the FT article is here.

Giving away money well can be harder than earning it

Northwestern has a new class method trying to teach that skill:

Vinay Sridharan must make it through microeconomic theory and the writings of Proust before the end of his senior year at Northwestern in June. But in one course, the final project is far less abstract: give away $50,000.

It is also far more difficult than it may seem.

This course in philanthropy, endowed with a grant from a Texas hedge fund manager, requires students to find and investigate nonprofit organizations and, if they stand up to scrutiny, give them a portion of the five-figure cash pot.

But did the backing donor give his money away well? I am not so sure. There is more here.

Sweden has lots of wealth inequality

Sweden is viewed as an egalitarian utopia by outsiders, but reality is complex. In some ways Sweden has less social equality than the United States. While the American upper class is largely meritocratic, the upper class in Sweden are still mostly defined by birth.

Historically, Sweden, Norway and Finland alone in Europe never developed Feudalism (Denmark was closer to continental Europe). The Nordic nobility was a small share of the population and not as powerful as the nobility in continental Europe, though still influential. The upper class in Sweden today consists of the nobility and of wealthy bourgeoisie families that socially merged with them. Wealthy bourgeois families live in the same neighborhoods and have adopted similar behavior and identity as the nobility. Despite long Social Democratic dominance they remain a coherent social group, with a distinct and recognizable accent, way of dressing, values etc.

Belonging to the upper-class is not defined merely by wealth, depending more on blood. Just as in historical times, a Nouveau riche member of the middle class will not automatically be accepted as a member of the upper-classes, unless they actively adapt their behavior and are accepted by the upper-classes socially.

The upper classes in Sweden retain a disproportional hold on wealth and power. The formal nobility in Sweden constitutes around 0.2% of the population. A couple of years ago I looked through the list of the wealthiest Swedes. Fully 10% of the richest Swedes are members of the nobility. By contrast not a single one of the richest Swedes was a non-European immigrant. Of Sweden’s prime-ministers Sweden during the modern era 20% belonged to the nobility.

Sweden is known for income equality. Increasingly, studies also point to Sweden as a country characterized by high intergenerational mobility of income. Income-distribution and wealth distribution are however not the same thing. What some may not know is that wealth-inequality is relatively high in Sweden. The top one percent own around 35% of wealth in the United States. In Sweden, because of extensive tax evasion, the number is harder to calculate. When including estimates of wealth held outside of Sweden, Roine and Waldenström estimate that the top one percent richest Swedes own 25-40% of total wealth, not far from American inequality levels, and increasing more rapidly.

At the same time, the intergenerational mobility of top wealth is chokingly low. A recent studyfound that a astonishing 80-90% of inequality of top wealth is transmitted to the next generation in Sweden!

According to one studythe share of the richest Swedes who inherited their wealth is around, 2/3 with 1/3 being entrepreneurs, while in the United States it was the opposite, with 1/3 of the wealthiest inherited their wealth while around 2/3 are entrepreneurs.

Thus while the Swedish middle class is large and has a compressed earning distribution, at the very top you have a small number of aristocratic families controlling much of the wealth. Mobility into this group is rare, probably rares than it is in the United States. One reason are stronger informal class-barriers, merely earning wealth is not enough to be accepted a member of the aristocratic upper-class. Another more interesting reason may be the unintended effect of welfare-state economic policies.

During the era of Social Democratic dominance, they wondered how to deal with wealth inequality. The dilemma facing the Social Democrats was this: The upper-class business families did a very good job managing Swedish export industry, the key to Sweden’s wealth. This is especially true for the Wallenberg family, the leading industrial family in Sweden, controlling amongst others ABB, Ericsson, Electrolux, Atlas Copco, SKF, AstraZeneca and Saab and doing an excellent job.

The Social Democrats decided to accept the unequal distribution of assets, but simply make these assets worth less using punitive high tax rates. Because of high inflation capital taxes were often 80-100%.

The upper-class families still owned most of private industry, but because of taxes those assets were simply not worth much. Paradoxically the high taxes and capital regulations which prevented foreign investments seem to have helped freeze the asset distribution into place, with the share of wealth owned by the rich being fairly constant between 1970 to the 1990s.

The OECD also reports that Sweden is quite unequal in wealth, hat tips go to Old Whig and Luis Pedro Coelho.

From the comments

Mesa wrote:

I would suspect that successful research institutions don’t feel obliged to redistribute their funding to less fortunate institutions. I think the point that is interesting here is that successful academic institutions are probably deemed to have earned their support, while successful business people are not, they having generally thought to have earned their success through luck or inheritance. From the endowment and research funding data it seems universities have both high income inequality and wealth inequality, to use terminology from the current debate.

Score one for the signaling model of education

In the new AER there is a paper by Melvin Stephens Jr. and Dou-Yan Yang, the abstract is this:

Causal estimates of the benefits of increased schooling using US state schooling laws as instruments typically rely on specifications which assume common trends across states in the factors affecting different birth cohorts. Differential changes across states during this period, such as relative school quality improvements, suggest that this assumption may fail to hold. Across a number of outcomes including wages, unemployment, and divorce, we find that statistically significant causal estimates become insignificant and, in many instances, wrong-signed when allowing year of birth effects to vary across regions.

In other words, those semi-natural experiments for the return to education, when some regions move with extra doses of compulsory schooling before others and we estimate differential wage effects, maybe don’t show as much as we used to think. As I’ve remarked to Bryan Caplan, if there is a criticism of a famous or politically correct result (or better yet both) getting published in the AER, you can up your Bayesian priors on that criticism being on the mark.

There are ungated copies of the paper here.

Piketty responds to critics

Assorted links

1. Scott Sumner on how to think about France.

2. Three revolutions from Miles Kimball.

3. Why the Germans are still in charge. And Italy’s real problem, in one picture.

4. What is the longest disambiguation page on Wikipedia?

5. My 2011 column on driverless cars.

6. Asian small-clawed otters celebrate enrichment at the Smithsonian.

7. McArdle on Piketty. And check out the cover (!).

A libertarian case for expanding Medicaid

Currently health care is very expensive in the United States, especially if you have to buy hospital care without formal insurance. Under ideal institutions, it would be much cheaper, maybe a third of the current price or lower yet (not for everything, though). For instance in Singapore health care expenditures are about four percent of gdp. A libertarian may think that laissez-faire or near laissez-faire is the way to go, while others might favor single payer with price controls, and so on. In any case, in the meantime we are stuck with expensive health care, and for reasons related to bad and coercive government policy.

Now, would a libertarian think that we should cut health care services in prisons, simply because tax dollars are in play? No, the prisoners — many of whom are morally innocent — have nowhere else to go for treatment. When it comes to health care, many potential Medicaid recipients are in essence prisoners, locked into a policy-deficient environment and so they cannot buy quality care at affordable prices. So if we favor health care expenditures for prisoners we might also favor Medicaid expansions.

That said, expanding the current version of Medicaid is unlikely to be a first-best solution, no matter what your broader political stance.

Addendum: Jacob Levy offers comment.

Machines vs. lawyers

We all know the market for lawyers is shrinking, but not every part of the legal services sector is in retreat. John O. MacGinnis writes:

The job category that the Bureau of Labor Statistics calls “other legal services”—which includes the use of technology to help perform legal tasks—has already been surging, over 7 percent per year from 1999 to 2010.

Much of the rest of the piece details how various legal functions can be taken only, if only slowly, by smart software. Here is a bit more:

Until now, computerized legal search has depended on typing in the right specific keywords. If I searched for “boat,” for instance, I couldn’t bring up cases concerning ships, despite their semantic equivalence. If I searched for “assumption of risk,” I wouldn’t find cases that may have employed the same concept without using the same words. IBM’s Watson suggests that such limitations will eventually disappear. Just as Watson deployed pattern recognition to capture concepts rather than mere words, so machine intelligence will exploit pattern recognition to search for semantic meanings and legal concepts. Computers will also use network analysis to assess the strength of precedent by considering the degree to which other cases and briefs rely on certain decisions. Some search engines, such as Ravel Law, already graphically display how much a particular precedent affected the subsequent course of law. As search progresses, then, machine intelligence not only will identify precedents; it will also guide a lawyer’s judgment about where, when, and how to cite them.

The entire piece is here, interesting throughout, via B.A.