Category: Data Source

How women are perceiving the economics profession

Fewer women reported being satisfied with the climate in the economics profession in 2023 compared to five years ago, despite efforts during that time to improve conditions for women in the field, according to a new survey.

About 17% of women in economics said they strongly agreed or agreed with a statement about being satisfied in the profession, down from 20% in 2018, according to the topline results of a survey conducted in the fall. The preliminary findings were presented by University of Chicago Booth School of Business economist Marianne Bertrand Friday at the American Economic Association’s annual meeting in San Antonio.

The gap between women and men’s experience in economics widened slightly over the past five years, with 39% of men saying they were satisfied with the profession’s climate, compared to 40% in 2018.

Women made up just 17.8% of full economics professors in 2022. While representation is higher among students and associate professors, the share of new economics doctoral degree recipients that were women fell in 2023, Bertrand said Friday.

The culture that was East German

This paper studies important determinants of adult self-control using population-representative data and exploiting Germany’s division as quasi-experimental variation. We find that former East Germans have substantially more self-control than West Germans and provide evidence for government surveillance as a possible underlying mechanism. We thereby demonstrate that institutional factors can shape people’s self-control. Moreover, we find that self-control increases linearly with age. In contrast to previous findings for children, there is no gender gap in adult self-control and family background does not predict self-control.

That is from the Economic Journal by Deborah A Cobb-Clark, Sarah C Dahmann, Daniel A Kamhöfer, and Hannah Schildberg-Hörisch, via the excellent Kevin Lewis.

The economic returns to psychological interventions

That is the topic of my Bloomberg column, here is one excerpt:

One study of Ethiopia looked at the psychological impact of raising aspirations. The researchers created a randomized control trial, showing one group of people short films about business and entrepreneurial success in the community. Six months later, those who had seen the films had worked more, saved more and invested more in education, relative to those who had not seen the films. Even five years later, households that had seen the films had accumulated more wealth, and their children had on average 0.43 more years of education, which typically is considered an impressive effect.

Not all the results are so positive:

Sometimes psychological interventions produce only temporary effects. One research design taught self-efficacy lessons to women in India. The likelihood of employment rose 32% in the short run — but within a year the effects had dissipated…

None of these results demonstrates that there is a “psychology of poverty” to be overcome by external interventions. They do imply, however, that poorer economies can make marginal gains by investing in what might be called psychological and psychotherapeutic infrastructure. These research designs can be applied to hundreds or thousands of people, but it will never be easy to use them for entire citizenries. Nonetheless, countries can make therapeutic help more accessible and affordable, and foster a culture in which people feel comfortable seeking it out.

Are we in the west at the margins where more counseling and therapy are of zero value, or perhaps negatives? Perhaps the only choice is either to have too little or too much self-reflection of a particular kind.

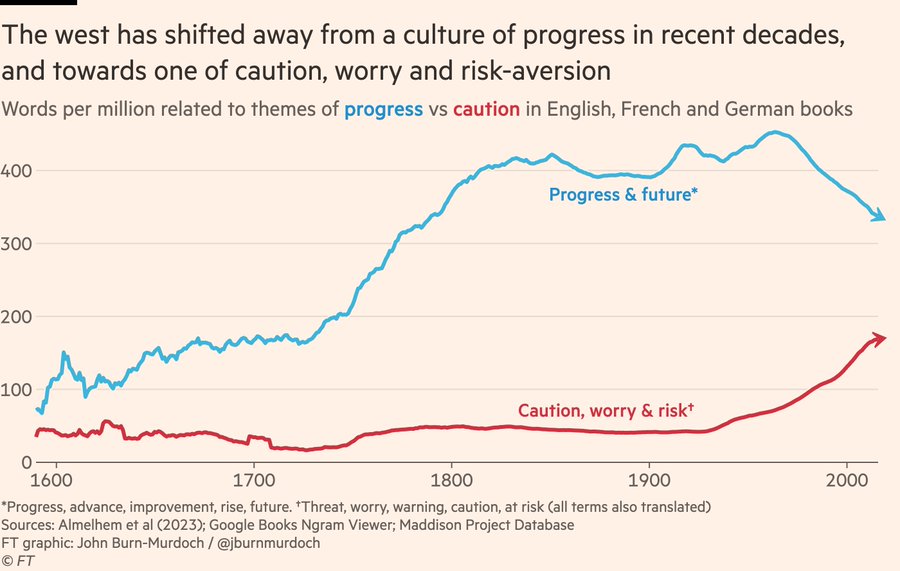

We need more talk of progress

Here is the underlying John-Burn Murdoch FT piece, pointer here. And a text excerpt:

Ruxandra Teslo, one of a growing community of progress-focused writers at the nexus of science, economics and policy, argues that the growing scepticism around technology and the rise in zero-sum thinking in modern society is one of the defining ideological challenges of our time.

I am pleased that Ruxandra is now also an Emergent Ventures winner.

A textual analysis of Enlightenment ideals

Using textual analysis of 173,031 works printed in England between 1500 and 1900, we test whether British culture evolved to manifest a heightened belief in progress associated with science and industry. Our analysis yields three main findings. First, there was a separation in the language of science and religion beginning in the 17th century. Second, scientific volumes became more progress-oriented during the Enlightenment. Third, industrial works—especially those at the science-political economy nexus—were more progress-oriented beginning in the 17th century. It was therefore the more pragmatic, industrial works which reflected the cultural values cited as important for Britain’s takeoff.

That is from a new research paper by Ali Almelhem, Murat Iyigun, Austin Kennedy, and Jared Rubin.

Police work at the private margin

We study how public sector workers balance their professional motivations with private economic concerns, focusing on police arrests. Arrests made near the end of an officer’s shift typically require overtime work, and officers respond by reducing arrest frequency but increasing arrest quality. Days in which an officer works a second job after their police shift have higher opportunity cost, also reducing late-shift arrests. Combining our estimates in a dynamic model identifies officer preferences over workplace activity and overtime work. Our results indicate that officers’ private costs of arrests have a first-order impact on the quantity and quality of enforcement.

That is from a new NBER working paper by Aaron Chalfin and Felipe M. Gonçalves.

Censorship of U.S. Movies in China

We introduce a structural econometric model to estimate the extent to which the Chinese government bans U.S. movies. According to our estimates, if a movie has characteristics similar to the median movie in our sample, then the probability is approximately 0.91 that the Chinese government will ban it. During our sample period, 1994-2019, U.S. movies comprised about 28 percent of the Chinese market and sales were about $22.6 billion. However, according to our estimates, if the Chinese government had not banned any U.S. movies, then the latter numbers would have risen to 68 percent and $45.1 billion.

As for what gets banned:

…, two factors that have very high statistical significance are: (i) whether the movie contains occult content, and (ii) whether the movie

receives an R rating from the Motion Picture Association of America (MPAA). The factors also have very high substantive significance. For instance, suppose two movies, A and B, are identical except that movie A contains occult content, while B does not. Suppose movie B’s probability of being banned is 50%. Then, according to our results, the occult content in movie A causes its probability of being banned to rise to 67%. A similar thought experiment implies that, if a movie has an R rating, then this raises its probability of being banned from 50% to 70%.Three other factors seem to be important but come just short of reaching statistical significance. These are whether the movie contains themes related to (i) anti-communism, (ii) individualism, or (iii) Tibet. A fourth factor is similar. This is whether the actor Richard Gere

appears in the movie.

That is a new paper by XUHAO PAN, Tim Groseclose, and yours truly, forthcoming in the Journal of Cultural Economics.

Vincent Geloso says “Ouch!” to PSZ

Okay, I had the time to read this over. In the past, I did not mince words much. I do not see the reason to do any mincing now.

There are six replies that must be made to this piece.

First: Zucman (I am assuming he also speaks for the other two musketeers) is… https://t.co/SldXUFXZU7 pic.twitter.com/tGksxSHcxb

— Vincent Geloso (@VincentGeloso) December 17, 2023

The Piketty-Saez-Zucman response to Auten and Splinter

A number of you have asked me what I think of their response. The first thing I noticed is that Auten and Splinter make several major criticisms of PSZ, and yet PSZ respond to only one of them. On the others they are mysteriously silent.

The second thing I noticed is that PSZ have been trying to deploy the slur of “inequality deniers” against Auten and Splinter. I take that as a bad epistemic sign.

I was in the midst of writing a longer post, but then I received the following from Splinter, and I cannot come close to his efforts or authority:

Here is a short response to yesterday’s comments by Piketty, Saez, and Zucman (PSZ) on Auten and Splinter (forthcoming in JPE). These are variations on prior comments that Jerry and I addressed in 2019 and 2020.

First, PSZ say audit data suggest adding underreported income implies little change in top 1% shares. We agree. But their approach increases recent top 1% shares about 1.5 percentage points, with about 50% of underreported business income going to the top 1% by reported income. However, Johns and Slemrod (2012) found only 5% of underreporting went to the top 1% by reported income. This discrepancy is because PSZ allocate underreported income proportional to reported positive income, which ignores that a substantial share of business underreporting (about 40%) goes to individuals with reported negative total income, where misreporting rates are the highest (Table B3 here). The concentration of underreporting at the bottom of the reported distribution causes substantial upward re-ranking when adding underreported income, but that’s mostly ignored in the PSZ approach. The PSZ approach also implies that someone who decreases their underreporting rate by increasing their reported income is allocated more underreporting. That’s backwards.

In contrast, our approach fits prior estimates from audit data, makes use of many years of audit data, and improves upon prior approaches. We find that underreported income slightly lowers top 1% pre-tax income shares and slightly increases after-tax income shares (Figure B6 here), which is consistent with the audit data. For example, 16% of underreporting is in our top 1% ranked by true income, far less than PSZ’s near 50%-allocation and a bit under the 27% in Johns and Slemrod because we improve upon prior approaches that misallocate undetected underreporting (discussion here). Contrary to the assertions and approach of PSZ, our Figure B5 (bottom panel, here) shows that re-ranking between reported and true (reported plus underreported) income matters substantially. PSZ appear confused about the difference between ranking by reported versus true income. Our underreporting allocations (as are theirs) must be based on reported income because that is all one observes with the primary tax data we both use. But, unlike their method, our allocations are done such that we match the re-ranking implied by audit data. Therefore, we match both the distributions by reported and true income after re-ranking (top two panels of Figure B5, here).

Second, income missing from individual tax returns has shifted from the top to outside the top. The shift from the top was from movements out of closely-held C corporations, whose income is missing from individual tax returns, to passthrough businesses, whose income is on individual tax returns. This created growth in the top share of taxed business income. The growth in PSZ’s top share of untaxed business income, however, is due to their skewed allocation of underreported income that re-allocates underreported income to the top of the distribution. Outside the top, the growth of missing income is from increasing tax-exempt employee compensation, especially from health insurance (see Figure B16 here).

Third, PSZ suggest that top wealth and capital income shares should run parallel over the long run. This is a problematic assumption. Economic changes can push down capital income shares relative to wealth shares. For example, interest rates fell dramatically between 1989 and 2019—the federal funds effective rate fell from 9 to 2 percent. This tends to decrease the ratio of interest-income to bond-wealth and therefore falling interest rates likely increased the gap between top income and wealth shares. Also, much of top wealth patterns are driven by passthrough business, but this is fully or two-thirds excluded from PSZ’s definition of “capital” income here. When fully including passthrough business, the Auten–Splinter top 1% non-housing “capital” income share increased by 5 percentage points between 1989 to 2019, about two-thirds the Federal Reserve’s estimated increase in top 1% wealth shares. Therefore, the Auten-Splinter estimates are broadly consistent with increasing top wealth shares.

The Auten–Splinter approach is fundamentally a data-driven approach (Table B2 here). Based on Saez and Zucman’s (2020) suggestions and conversations, our more recent work adds new uses of data to account for high-income non-filers, flexible spending accounts, and depreciation issues from expensing. Where we rely on assumptions, alternative ones suggest top 1% shares change little, see Table 5. Our headline finding of relatively flat long-run top 1% after-tax income shares is robust.

Auten and Splinter had presented versions of those points previously, as they note. Yet PSZ present them as naive fools who somehow forgot to think about these issues at all, and PSZ do not, in their reply, consider these more detailed presentations of the point and defenses of the Auten-Splinter estimates. So I don’t think of the PSZ response as especially strong.

Here are relevant Auten and Splinter points from back in 2020. Phil Magness offers commentary.

Do people trust humans more than Chat GPT?

We explore whether people trust the accuracy of statements produced by large language models (LLMs) versus those written by humans. While LLMs have showcased impressive capabilities in generating text, concerns have been raised regarding the potential for misinformation, bias, or false responses. In this experiment, participants rate the accuracy of statements under different information conditions. Participants who are not explicitly informed of authorship tend to trust statements they believe are human-written more than those attributed to ChatGPT. However, when informed about authorship, participants show equal skepticism towards both human and AI writers. There is an increase in the rate of costly fact-checking by participants who are explicitly informed. These outcomes suggest that trust in AI-generated content is context-dependent.

That is from a new paper by Joy Buchanan and William Hickman.

Finland education fact of the day

Finland: pic.twitter.com/i3PQKyhWWI

— Simon Sarris (@simonsarris) December 12, 2023

Earth fact of the day

This week, the International Institute for Strategic Studies in London published the latest edition of its authoritative annual Armed Conflict Survey, and it’s not predicting much peace for the holidays. It paints a grim picture of rising violence in in many regions, of wars chronically resistant to broking of peace. The survey — which addresses regional conflicts rather than the superpower confrontation between China, Russia, the US and its allies — documents 183 conflicts for 2023, the highest number in three decades…

The intensity of conflict has risen year on year, with fatalities increasing by 14% and violent events by 28% in the latest survey. The authors describe a world “dominated by increasingly intractable conflicts and armed violence amid a proliferation of actors, complex and overlapping motives, global influences and accelerating climate change.”

Here is more from Max Hastings at Bloomberg.

Differential fertility makes society more conservative on family values

“Family values” conservatives in the United States have more children and more siblings than their compatriots. These patterns reflect the tendency of the more religious and less educated to have larger families and more conservative views on the family. Among Protestants, denominational differences play a role, with fundamentalist groups exhibiting larger families, less education, and greater conservatism. The causal pathways are unclear, but the patterns reshape society: Traditional-family conservatism is more prevalent than it would have been if each person had the same population share as his or her parents. This demographic phenomenon raises opposition to same-sex marriage and abortion by 3 to 4 percentage points. It accounts for 7.9 million of the nation’s 54.8 million opponents to same-sex marriage.

That is a new paper by Tom S. Vogl and Jeremy Freese, from brandonrox.

European inflation was more painful for the elderly

That is the topic of my latest Bloomberg column, here is one bit:

As recent research indicates, the recent inflation has been very costly. The 2021-2022 inflation cost more than 3% of national income in France, Germany and Spain, and about 8% of national income in Italy, higher costs than what a typical recession would bring.

It is striking how much those costs fall on the elderly, which is one reason that lowering inflation rates has been such a priority. The elderly usually have the most accumulated savings, and less time to make up for inflationary losses by subsequent compounding. Older people are also more likely to own homes, so face higher home heating bills when energy prices rise. Overall, in the last several years, a low-income retired household in Italy might have taken income cuts of up to 20%, while a middle-aged household in the euro area might have seen a typical income cut of 5%.

…Not everyone lost from the inflation. Young households in Spain, for instance, gained more than 5% in income. The simplest way a household might gain from inflation is that its debt liabilities decline in real, inflation-adjusted value. On average, the young are more likely to be in debt than the elderly, and own fewer assets. Inflation also tends to lower the value of tenured jobs, such as in academia, and younger people are less likely to hold such posts. The young also tend to have more time in their lives to adjust to negative economic shocks, by for instance geographic or career migration.

Overall, an estimated 30% of the households in the euro area gained from the inflationary shock. Almost half of 25- to 44-year-olds benefited.

On net, the inflation remains a clear negative. But how many other eurozone policies manage to favor the young?

Here is the underlying research by Filippo Pallotti, Gonzalo Paz-Pardo, Jiri Slacalek, Oreste Tristani, and Giovanni L. Violante.

Trading on terror

Recent scholarship shows that informed traders increasingly disguise trades in economically linked securities such as exchange-traded funds (ETFs). Linking that work to longstanding literature on financial markets’ reactions to military conflict, we document a significant spike in short selling in the principal Israeli-company ETF days before the October 7 Hamas attack. The short selling that day far exceeded the short selling that occurred during numerous other periods of crisis, including the recession following the financial crisis, the 2014 Israel-Gaza war, and the COVID-19 pandemic. Similarly, we identify increases in short selling before the attack in dozens of Israeli companies traded in Tel Aviv. For one Israeli company alone, 4.43 million new shares sold short over the September 14 to October 5 period yielded profits (or avoided losses) of 3.2 billion NIS on that additional short selling. Although we see no aggregate increase in shorting of Israeli companies on U.S. exchanges, we do identify a sharp and unusual increase, just before the attacks, in trading in risky short-dated options on these companies expiring just after the attacks. We identify similar patterns in the Israeli ETF at times when it was reported that Hamas was planning to execute a similar attack as in October. Our findings suggest that traders informed about the coming attacks profited from these tragic events, and consistent with prior literature we show that trading of this kind occurs in gaps in U.S. and international enforcement of legal prohibitions on informed trading. We contribute to the growing literature on trading related to geopolitical events and offer suggestions for policymakers concerned about profitable trading on the basis of information about coming military conflict.

That is from a new paper by Robert J. Jackson, Jr. and Joshua Mitts. Via the excellent Jordan Schneider.

Debunked?: Possibly the study is quite wrong.