Category: Law

Blame Canada! Measles Edition

Polimath has a good post on measles. The recent spike in U.S. cases has drawn alarm. As the New York Times reports:

There have now been more measles cases in 2025 than in any other year since the contagious virus was declared eliminated in the United States in 2000, according to new data released Wednesday by the Centers for Disease Control and Prevention.

The grim milestone represents an alarming setback for the country’s public health and heightens concerns that if childhood vaccination rates do not improve, deadly outbreaks of measles — once considered a disease of the past — will become the new normal.

But as Polimath notes, U.S. vaccination rates remain above 90% nationally. The problem isn’t broad domestic anti-vax sentiment but rather concentrated gaps in coverage, often within insular religious communities. These local shortfalls do explain how outbreaks spread once they begin—but how do they begin in the first place, given these communities are islands within a largely vaccinated country? Polimath says blame Canada! (and Mexico!)

The greater concern in my mind is not the problem of low measles vaccination coverage in the United States, but among our immediate neighbors. In Ontario, the MMR vaccination rate among 7-year-olds is under 70%. As in the examples above, this rate seems to be particularly low “in specific communities”, whatever that is supposed to mean. This has resulted in the ongoing spread of measles such that Ontario’s measles infection rate is 40 times higher than the United States. Canada officially “eliminated” measles in 1998. But with vaccine rates as low as they are, it seems like Canada is at risk for losing that “elimination” status and becoming an international source for measles.

Similarly, Mexico is having a measles outbreak that is substantially worse than the US outbreak. Importantly, the Mexican outbreak has been the worst in the Chihuahua province (over 3,000 cases), which borders Texas and New Mexico.

I’m less interested in blame than in the useful reminder that not all politics is American politics. Vaccination rates have dipped worldwide and not in response to U.S. politics or RFK Jr. In fact, despite RFK Jr. the U.S. is doing better than some of its North American and European peers. Outbreaks here may be triggered by cross-border exposure, not failures in U.S. public health alone. Not all politics is American—and not all American outcomes are made in America.

Hat tip: the excellent Stephen Landry.

Surveillance is growing

California residents who launched fireworks for the 4th of July have tickets coming in the mail, thanks to police drones that were taking note. One resident, for example, racked up $100,000 in fines last summer due to the illegal use of fireworks. “If you think you got away with it, you probably didn’t,” said Sacramento Fire Department Captain Justin Sylvia. “What may have been a $1,000 fine for one occurrence last year could now be $30,000 because you lit off so many.” Homeowners who weren’t even present at the property also have tickets coming in the mail due to the social host ordinance.

Here is the source. Elsewhere (NYT):

Hertz and other agencies are increasingly relying on scanners that use high-res imaging and A.I. to flag even tiny blemishes, and customers aren’t happy…

Developed by a company called UVeye, the scanning system works by capturing thousands of high-resolution images from all angles as a vehicle passes through a rental lot’s gates at pickup and return. A.I. then compares those images and flags any discrepancies.

The system automatically creates and sends damage reports, Ms. Spencer said. An employee reviews the report only if a customer flags an issue after receiving the bill. She added that fewer than 3 percent of vehicles scanned by the A.I. system show any billable damage.

I await the next installment in this series.

What does one hundred percent reserves for stablecoins mean?

I asked o3 pro about the Genius Act, and it gave me this answer (there is more at the link), consistent with other responses I have heard:

The statute’s policy goal is to keep a payment‑stablecoin issuer from morphing into a fractional‑reserve bank or a trading house while still giving it enough freedom to:

-

hold the specified reserve assets and manage their maturities;

-

use overnight Treasuries repo markets for cash management (explicitly allowed);

-

provide custody of customers’ coins or private keys.

Everything else—consumer lending, merchant acquiring, market‑making, proprietary trading, staking, you name it—would require prior approval and would be subject to additional capital/liquidity rules.

Recall also that the stablecoins are by law prohibited from paying interest, though the backing assets, such as T-Bills, will pay interest to the stablecoin issuer. Thus when nominal interest rates are high, the issuer will earn a decent spread and have no problem covering costs. When nominal interest rates are low or zero, fees on stablecoin issuance might be required, otherwise there is no way to cover the basic costs of operation.

What will be the costs of intermediation? In the financial sector as a whole, they are arguably about two percent. For money market funds, however, they are closer to 0.2 percent. (Since these entities will be strictly regulated, we cannot estimate fees by looking at current major stablecoin issuers. Across some different inquiries, o3 pro gave me intermediation cost estimates ranging from 0.8 percent to 3 percent.) Whatever number will be the case here, the intermediaries may need to resort to fees if market interest rates are very low, in order to break even. That may in turn induce individuals to yank money out of the accounts — who wants to keep paying those fees?

Perhaps a more likely problem would stem from interest rates that are fairly high. In that case, why hold zero-yielding stablecoins? The sector will again contract, though in an orderly fashion.

Perhaps the sector and its intermediaries are most stable for some band of interest rates “in the middle”?

Inspections of the backing assets are supposed to take place every month, though the regulator can take a look any time. I am not sure what is the optimal frequency. But I worry there is sometimes no “efficiency wage profit margin” to induce responsible behavior. After all, the issuers have no other lines of business and no other sources of revenue. Non-pecuniary competition for deposits might reduce profits further (“come get your free toaster!”). Thus being kicked out of the sector is no major penalty (for those parameter values), which puts a significant burden on the possibility of legal and felony punishments. It can be hard to pull the trigger on those, however.

If interest rates are somewhat higher though, the desire to keep that profit will create an economic incentive for responsible behavior, above and beyond the fear of legal penalties.

As I understand the legislation, the level of interest rates seems important for sector stability and also for the size of the sector. That is because there are no interest payments on stablecoins that can adjust with the underlying rates on the T-Bills. Perhaps that feature of the legislation should be reconsidered? Or perhaps issuer competition across non-pecuniary yields on the accounts will serve a sufficiently comparable purpose?

GAVI’s Ill-Advised Venture Into African Industrial Policy

GAVI, the Vaccine Alliance has saved millions of lives by delivering vaccines to the world’s poorest children at remarkably low cost. It’s frankly grotesque that RFK Jr. cites “safety” as a reason to cut funding—when the result of such cuts will be more children dying from preventable diseases. Own it.

You can find plenty of RFK Jr. criticism elsewhere, however, and GAVI is not above criticism. Thus, precisely because GAVI’s mission is important, I want to focus on a GAVI project that I think is ill-motivated and ill-advised, GAVI’s African Vaccine Manufacturing Accelerator (AVMA).

The motivation behind the AVMA is to “accelerate the expansion of commercially viable vaccine manufacturing in Africa” to overcome “vaccine inequity” as illustrated during the COVID crisis. The problem with this motivation is that most of Africa’s delay in receiving COVID vaccines was driven by funding issues and demand rather than supply. Working with Michael Kremer and others, I spent a lot of time encouraging countries to order vaccines and order early not just to save lives but to save GDP. We were advisors to the World Bank and encouraged them to offer loans but even after the World Bank offered billions in loans there was reluctance to spend big sums. There were supply shortages in 2021 in Africa, as there were elsewhere, but these quickly gave way to demand issues. Doshi et al. (2024) offer an accurate summary:

Several reasons likely account for low coverage with COVID-19 vaccines, including limited political commitment, logistical challenges, low perceived risk of COVID-19 illness, and variation in vaccine confidence and demand (3). Country immunization program capacity varies widely across the African Region. Challenges include weak public health infrastructure, limited number of trained personnel, and lack of sustainable funding to implement vaccination programs, exacerbated by competing priorities, including other disease outbreaks and endemic diseases as well as economic and political instability.

Thus, lack of domestic vaccine production wasn’t the real problem—remember, most developed countries had little or no domestic production either but they did get vaccines relatively quickly. The second flaw in the rationale for the AVMA is its pan-African framing. Africa is a continent, not a country. Why would manufacturing capacity in Senegal serve Kenya better than production in India or Belgium? There’s a peculiar assumption of pan-African solidarity, as if African countries operate with shared interests that go beyond those observed in other countries that share a continent.

Both problems with the rationale for AVMA are illustrated by South Africa’s Aspen pharmaceuticals. Aspen made a deal to manufacture the J&J vaccine in South Africa but then exported doses to Europe. After outrage ensued it was agreed that 90% of the doses would be kept in Africa but Aspen didn’t receive a single order from an African government. Not one.

Now to the more difficult issue of capacity. Africa produces less than .1% of the world’s vaccines today. The African Union has what it acknowledges is an “ambitious goal” to produce over 60 percent of the vaccines needed for Africa’s population locally by 2040. To evaluate the plausibility of this goal do note that this would require multiple Serum‑of‑India‑sized plants.

More generally, vaccines are complex products requiring big up-front investments and long lead times:

Vaccine manufacturing is one of the most demanding in industry. First, it requires setting up production facilities, and acquiring equipment, raw materials, and intellectual property rights. Then, the manufacturer will implement robust manufacturing processes and manage products portfolio during the life cycle. Therefore, manufacturers should dispose of an experienced workforce. Manufacturing a vaccine is costly and takes seven years on average. For instance, it took about 5–10 years to India, China, and Brazil to establish a fully integrated vaccine facility. A longer establishment time can be expected for African countries lacking dedicated expertise and finance. Manufacturing a vaccine can costs several dozens to hundreds of million USD in capital invested depending on the vaccine type and disease indication.

All countries in Africa rank low on the economic complexity index, a measure of whether a country can produce sophisticated and complex products (based on the diversity and complexity of their export basket). But let us suppose that domestic production is stood up. We must still ask, at what price? If domestic manufacturing ends up being more expensive than buying abroad (as GAVI acknowledges is a possibility even with GAVI’s subsidies), will African countries buy “locally” and pay more or will solidarity go out the window?

Finally, even if complex vaccines are produced at a competitive price, we still haven’t solved the demand problem. GAVI again has a rather strange acknowledgment of this issue:

Secondly, adequate country demand is another critical enabler. For AVMA to be successful, African countries will need to buy the vaccines once they appear on the Gavi menu. The Secretariat is committed to ongoing work with the AU and Member States on demand solidarity under Pillar 3 of Gavi’s Manufacturing Strategy.

So to address vaccine inequity, GAVI is investing in local production….but the need to manufacture “demand solidarity” among African governments reveals both the flaw in the premise and the weakness of the plan.

Keep in mind that the WHO only recognizes South Africa and Egypt as capable of regulating the domestic production of vaccines (and Nigeria as capable of regulating vaccine imports). In other words, most African governments do not have regulatory systems capable of evaluating vaccine imports let alone domestic production.

GAVI wants to sell the AVMA as if were an AMC (Advance Market Commitment) but it isn’t. It’s industrial policy. An AMC would offer volume‑and‑price guarantees open to any manufacturer in the world. An AMC with local production constraints is a weighted down AMC, less likely to succeed.

None of this is to imply that GAVI has no role to play. In addition to a true AMC, GAVI could arrange contracts to pay existing global suppliers to maintain idle capacity that can pivot to African‑priority antigens within 100 days. GAVI could possibly also help with regulatory convergence. There is an African Medicines Agency which aims to operate like the EMA but it has only just begun. If the AMA can be geared up, it might speed up vaccine approval through mutual recognition pacts.

The bottom line is that the $1.2 billion committed to AVMA would likely better more lives if it was directed toward GAVI’s traditional strengths in pooled procurement and distribution, mechanisms that have proven successful over the past two decades. Instead, AVMA drags GAVI into African industrial policy. A poor gamble.

Labour considers fast-tracking approval of big projects

There are a few modest signs of progress in the UK (and Canada):

Ministers are exploring using the powers of parliament to cut the time it takes to approve new railways, power stations and other infrastructure projects.

In an attempt to promote growth, the government is examining whether it could pass legislation that would allow transport, energy and new town housing projects to circumvent swathes of the planning process.

The move could limit the ability of opponents to challenge projects in the courts and reduce scrutiny of some developments. It is loosely modelled on a Canadian scheme that was the brainchild of Mark Carney, the new prime minister and a former governor of the Bank of England.

The One Canadian Economy Act was passed by Canada’s parliament in June and gives Carney’s government powers to fast-track national projects. The Treasury is understood to be examining how a UK version could speed up the approval process for nationally significant infrastructure projects, such as offshore wind farms or even a third runway at Heathrow.

Here is more from The Times.

Tom Tugendhat on British economic stagnation

Second, and even more detrimental to younger generations, is a set of policies that have artificially created a highly damaging cult of housing. For many decades, too few houses have been built in the UK. Thanks in part to the tax system, housing has been transformed from a place to live and raise a family into a de facto tax free retirement fund that excludes the young. More than 56 per cent of the UK’s total housing wealth is owned by those over 60, while home ownership among those under 35 has collapsed to just 6 per cent. This has had profound social and economic consequences as fewer people marry and have children, further impairing long-term demographic regeneration. The result? More than 80 per cent of the growth in real per capita wealth over the past 30 years has come from appreciation of real estate, not from the financial investment that powers the economy.

Michael Tory, co-founder of Ondra Partners, has argued that this capital misallocation has created a self-reinforcing cycle, weakening our national and economic security. Without productive capital, we are wholly dependent on foreign investment and imported labour, straining housing supply and public services. These distortions can only be corrected through a rebalancing of our national capital allocation that puts long-term national interest above narrow electoral calculation. That means levelling the investment playing field to reduce the taxes on those whose long-term savings and investments in Britain’s future actually employ people and generate growth. Along with building more houses and stricter migration controls, this would bring home ownership into reach for younger generations.

British pension funds should invest more in British businesses as well. Here is more from the FT.

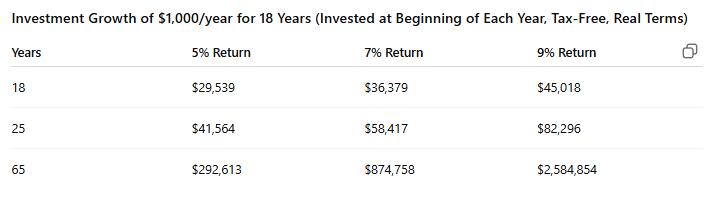

Trump Accounts are a Big Deal

Trump’s One Big Beautiful Bill Act was signed into law on July 4, 2025. It’s so big that many significant features have been little discussed. Trump Accounts are one such feature under which every newborn citizen gets $1000 invested in the stock market. These accounts could radically change social welfare in the United States and be one important step on the way to a UBI or UBWealth. Here are some details:

- Government Contribution: A one-time $1,000 contribution per eligible child, invested in a low-cost, diversified U.S. stock index fund.

- Eligibility: U.S. citizen children born between January 1, 2025, and December 31, 2028 (with a valid Social Security number and at least one parent with a valid Social Security number).

- Employer Contributions: Employers can contribute up to $2,500 annually per employee’s child, and these contributions are excluded from the employee’s gross income for tax purposes. These are subject to the overall $5,000 annual contribution limit (indexed for inflation) per child (which includes parental contributions).

The employer contribution strikes me as important. Suppose that in addition to the initial $1000 government payment that on average $1000 is added per year for 18 years (by a combination of parent and parent employer contributions). Note that this is below the maximum allowed annual contribution of $5000. At a historically reasonable 7% real rate of return these accounts will be worth ~36k at age 18 (when the money can be fully withdrawn), $58k at age 25 and $875k at age 65 subject to uncertainty of course as indicated below.

The $1000 initial payment is available only for newborns but, as I read the text, the parent and employer donations can be made for any child under the age of 18 so this is basically an IRA for children. It’s slightly complicated because if the child or parents put after-tax money into the account that is not taxed at withdrawal (you get your basis back) but everything else is taxed on withdrawal as ordinary income like an IRA. There are approximately 3.5 million citizen births a year so the program will have direct costs of $3.5 billion plus indirect costs from reduced taxes due to the tax-free yearly contribution allowance, which as noted could be quite large as it can go to any child. Thus the program could be quite expensive. On the other hand, it’s clear that the accounts could reduce reliance on social security if held for long periods of time. The $1000 initial contribution is limited to four years but once 14 million kids get them, the demand will be to make them permanent.

BBB on drug price negotiations

The sweeping Republican policy bill that awaits President Trump’s signature on Friday includes a little-noticed victory for the drug industry.

The legislation allows more medications to be exempt from Medicare’s price negotiation program, which was created to lower the government’s drug spending. Now, manufacturers will be able to keep those prices higher.

The change will cut into the government’s savings from the negotiation program by nearly $5 billion over a decade, according to an estimate by the nonpartisan Congressional Budget Office.

…the new bill spares drugs that are approved to treat multiple rare diseases. They can still be subject to price negotiations later if they are approved for larger groups of patients, though the change delays those lower prices.

This is the most significant change to the Medicare negotiation program since it was created in 2022 by Democrats in Congress.

Here is more from the NYT. Knowledge of detail is important in such matters, but one hopes this is the good news it appears to be.

Genetic Counseling is Under Hyped

In an excellent interview (YouTube; Apple Podcasts, Spotify) Dwarkesh asked legendary bio-researcher George Church for the most under-hyped bio-technologies. His answer was both surprising and compelling:

What I would say is genetic counseling is underhyped.

What Church means is that gene editing is sexy but for rare diseases carrier screening is cheaper and more effective. In other words, collect data on the genes of two people and let them know if their progeny would have a high chance of having a genetic disease. Depending on when the information is made known, the prospective parents can either date someone else or take extra precautions. Genetic testing now costs on the order of a hundred dollars or less so the technology is cheap. Moreover, it’s proven.

Since the early 1980s the Jewish program Dor Yeshorim and similar efforts have screened prospective partners for Tay-Sachs and other mutations. Before screening, Tay-Sachs struck roughly 1 in 3,600 Jewish births; today births with Tay-Sachs have fallen by about 90 percent in countries that adopted screening programs. As more tests are developed they can be easily integrated into the process. In addition to Tay-Sachs, Dor Yeshorim, for example, currently tests for cystic fibrosis, Bloom syndrome, and spinal muscular atrophy among other diseases. A program in Israel reduced spinal muscular atrophy by 57%. A study for the United States found that a 176 panel test was cost-effective compared to a minimal 5 panel test as did a similar study on a 569 panel test for Australia.

A national program could offer testing for everyone at birth. The results would then be part of one’s medical record and could be optionally uploaded to dating websites. In a world where Match.com filters on hobbies and eye color, why not add genetic compatibility?

Do it for the kids.

Addendum: See also my paper on genetic insurance (blog post here).

The anti-alcohol campaign in the USSR

Although alcohol consumption remains high in many countries, causal evidence on its effects at the societal level is limited because sustained, society-wide reductions in alcohol consumption rarely occur. We take advantage of a country-wide 1985-1990 anti-alcohol campaign in the Soviet Union that resulted in immediate, substantial and sustained reductions in alcohol consumption. We exploit regional differences in precampaign alcohol related mortality in the Russian republic and show immediate declines in male and female adult mortality in urban and rural areas across the entire age distribution, which translate into a rise in life expectancy. The campaign led to a substantial decline in deaths that are both directly (alcohol poisoning, homicides and suicides) and indirectly linked to alcohol consumption (respiratory and infectious). We find a decline in infant mortality rates among boys and girls due to causes most affected by post-natal parental behavior (choking and respiratory). Finally, both divorce and fertility rates rose, while abortions and maternal mortality due to abortions declined. This study provides novel evidence that alcohol consumption not only directly affects the mortality of drinkers but can have spillover effects on family outcomes.

That is from a recent paper by Elizabeth Brainerd and Olga Malkova.

*Breakneck: China’s Quest to Engineer the Future*

Austin Vernon on taxes on solar (from my email)

I think your question about new taxes on solar and wind is an interesting one, and increasing taxation has been an ongoing process for years.

Some of these tax increases are normal, like ending property tax exemptions. These taxes don’t impact project economics too severely, and the breaks create a lot of ill will at the local level.

Solar has seen constant tax increases and quotas on imported panels. Uncompetitive domestic producers, other competing energy sources, anti-trade folks, and China hawks all favor these taxes. The important metric is that buying panels in the US is 2x-3x more expensive per watt than in the rest of the world.

Solar panel factories are easy to build, and technology changes quickly. There is a Dutch boy and the dam effect. We constantly have to add new tariffs on different countries and new technologies (although foreign production from US-owned companies has generally been exempt). These tariffs have to get stiffer to maintain the balance.

A recent change was that the IRA finally led everyone to start building factories in the US. An absolute avalanche of panel factories is/was on the way with less activity for cells, wafers, and polysilicon. These factories might be viable without subsidies considering US panel prices. Most of the interest groups listed don’t appreciate this outcome, especially because many are Chinese-owned factories. Foreign Entity of Concern content and ownership penalties are the obvious solution as the next hole to put a finger in because many subcomponents would still be imported and the general kludge laws like that add.

The solar installation lobby has been satisfied with tax credits that counteract some of the high panel costs. These rules tend to discourage new technology in the fine print and skew incentives. Simpler, denser solar farm designs make sense once panels are cheap. There is no reason to make the switch if panels are expensive and the tax credit is based on the total install cost. Roughly 90% of US utility-scale installations have trackers that add cost but increase per panel output. In China, there are almost no trackers. There are also some nasty effects in the residential business that encourage complex financial products over streamlining construction and permitting.

It is an interesting crossroads where the tax credits are gone, and there is now a reason to have a more direct confrontation on panel cost. The battery industry is in the early stages of a similar conflict, but it seems like they might retain the deal with the devil and keep tax credits for now.

Privatize Federal Land!

I’ve long advocated selling off some federal land—an idea that reliably causes mass fainting spells among the enlightened. How could we possibly part with our national patrimony, our land, our sacred wilderness? Calm down. Most of this “public land” is never used by the public. Selling some of it would actually make it more accessible and useful to real people.

Moreover, most of you wailing about selling some Federal land are probably very happy we sold the “public” airwaves for your private cell phone use. Privatizing the airwaves made them much more useful to the public. (Thank you Reed!).

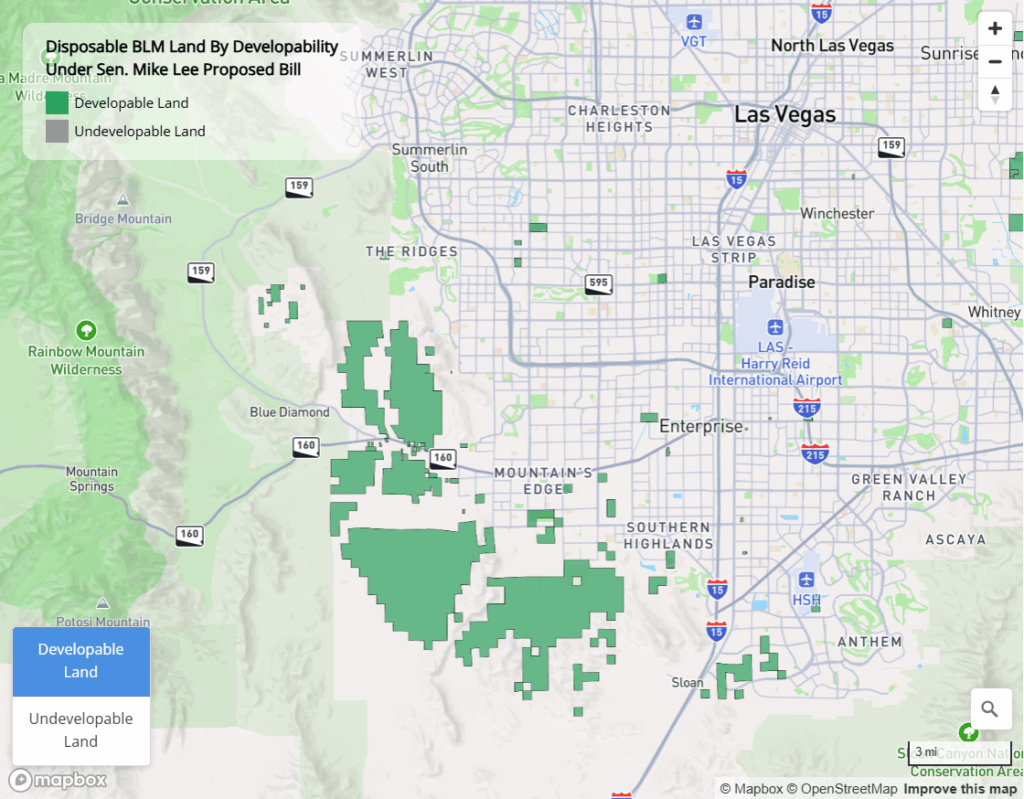

AEI has an excellent map of the lands that could be sold and developed in the Mike Lee bill. Here’s their conclusion:

The data show a significant opportunity. Our analysis finds that developing just 135-180 square miles of the most suitable BLM land, a minuscule fraction of the total, could yield approximately 1 million new homes over ten years. This would substantially address the West’s housing shortage while generating an estimated $15 billion for the U.S. Treasury from land sales.

Here’s an example of the some of the land potentially developable around Las Vegas.

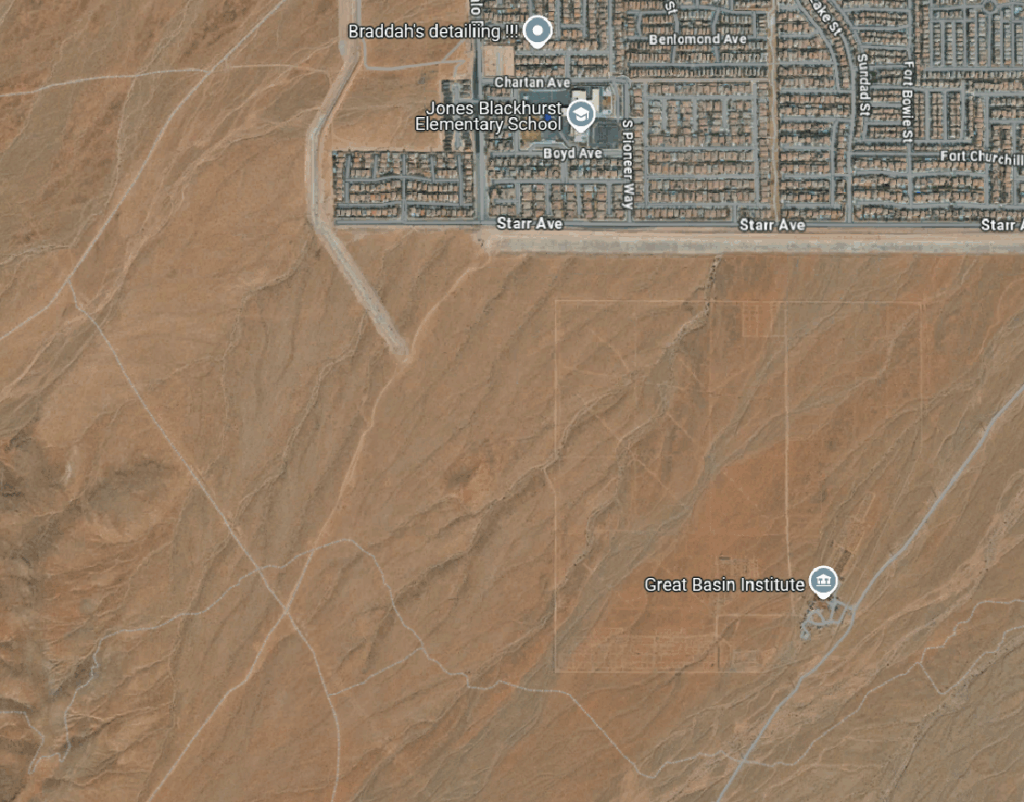

Here’s a Google satellite image of the bit around Mountain’s Edge. Enjoy your fishing on these public lands!

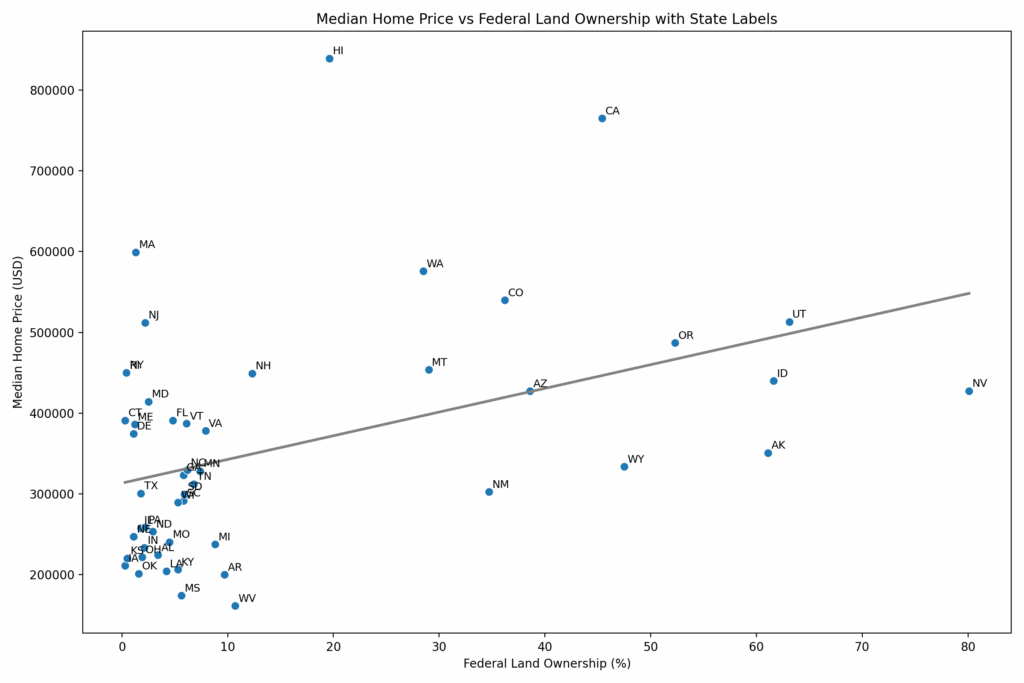

And here’s a very crude but useful scatter plot showing the correlation between median home prices in a state and Federal land ownership. Should home prices in Utah (63.1% Federally owned) really be 71% higher than in Texas (1.8% Federally owned)? Of course, Texas is famously an urban hellscape with no parks, no open space, and nowhere to hunt or fish.

C’mon British people, you can do better than this…

I’ve seen estimates that thirty people a day are arreested in the UK for things they say on social media. Other anecdotes of varying kinds continue to pile up:

Describing a middle-aged white woman as a “Karen” is borderline unlawful, a judge has said amid a bitter row at a mental health charity.

The slang term, used increasingly since the pandemic, refers to middle-aged white women who angrily rebuke those they view as socially inferior. Sitting in an employment tribunal, a judge has now said that the term is pejorative because it implies the woman is excessively and unreasonably demanding.

The woman who used the term nonetheless was acquitted, though barely. Here is the article from Times of London. And this:

The government’s new Islamophobia definition could stop experts warning about Islamist influence in Britain, a former anti-extremism tsar has warned.

Lord Walney said that a review being carried out by Angela Rayner’s department should drop the term Islamophobia, or risk “protecting a religion from criticism” rather than protecting individuals.

Ministers launched a “working group” in February aimed at forming an official definition of what is meant by Islamophobia or anti-Muslim hatred within six months.

Here is The Times link. British people, it is not just J.D. Vance who is upset. You are embarrassing yourselves with all this! Please stop. Even enemies of free speech think you are going about this in a pretty stupid way.

Who in California opposes the abundance agenda?

Labor unions are one of the culprits, environmental groups are another:

Hours of explosive state budget hearings on Wednesday revealed deepening rifts within the Legislature’s Democratic supermajority over how to ease California’s prohibitively high cost of living. Labor advocates determined to sink one of Newsom’s proposals over wage standards for construction workers filled a hearing room at the state Capitol mocking, yelling, and storming out at points while lawmakers went over the details of Newsom’s plan to address the state’s affordability crisis and sew up a $12 billion budget deficit.

Lawmakers for months have been bracing for a fight with Newsom over his proposed cuts to safety net programs in the state budget. Instead, Democrats are throwing up heavy resistance to his last-minute stand on housing development — a proposal that has drawn outrage from labor and environmental groups in heavily-Democratic California.

Here is the full story, via Josh Barro. To be clear, I am for the abundance agenda.