Results for “age of em” 17235 found

Assorted links

1. Memoir of an internet troll.

2. Photo of Iceland, via GH.

{kind=link}

3. Restrictions on doctor-owned hospitals.

4. How Laura and John Arnold wish to give away their money (recommended, and cameo by Steve Levitt).

5. “…the Colorado cannabis industry is purely cash-based…” You also can take on-line classes about how to grow marijuana.

6. Ben Bernanke gives a whole speech discussing the great stagnation and the “grandma test.”

Karl Smith on the liquidity leak

What Tyler calls a liquidity leak, I call markets at work. The ECB provides enough stimulus to get all of the Eurozone going but it all leaks to Germany. Fine. The German market heats up. German wages and rents rise. Retired German doctors start considering the virtues of a flat in Lisbon overlooking the harbor. German consultancies hold seminars on “How to make your Mediterranean town competitive in the new German Outsourcing Model.”

This is the way things are supposed to work. The idea that a more competitive and efficient Germany should not command higher wages and rents is bizarre; and is only called inflation because the Eurozone, in its heart-of-hearts, doesn’t actually believe its one monetary union where the richer parts are distinguished principally by the fact that they have more money.

The link is here. The analysis of course is correct, but I think this illustrates rather than solves the problem.

First, Portugal and Germany are not directly competing in so many export markets to a high degree. So raising German wages and prices helps Portugal only somewhat. Furthermore, the marginal propensity of Germans to spend, or the marginal propensity of German banks to lend, is not mainly directed toward the periphery. Therefore the gradient of “how much inflation are Germans tolerating to get some real output effects in Portugal” is a steep one, much steeper than you would find within a traditional, one-nation, single currency area with geographically mobile money.

Imagine telling Americans that they must endure a good deal of inflation to help solve some aggregate demand problems in Ecuador and El Salvador. No one doubts there is spillover, but if the banking system in Ecuador is falling apart, many of the possible transmission effects may not easily stick, or would not if Ecuador used more bank money and less pure currency. (Just fyi, right now inflation in Ecuador is higher than in the U.S.; here are numbers for El Salvador. It doesn’t look like a tight belt of monetary transmission to me, and those countries do not have the same bank insolvency problems which we are seeing in the eurozone periphery).

Second, this mechanism solves (at best) only one of the core problems of the eurozone, namely incorrect relative prices between Portugal and Germany. It helps less with the “Portuguese nominal wages are too high” problem, the “Portuguese banks are not sound” problem, and the “Portugal badly needs structural reform” problem, among other difficulties. The inflation would be an easier sell to the German public if it really would set the rest of the eurozone right, but that is a difficult case to make. Just try uttering this sentence vor dem Publikum: “It’s the leak that will make this work.”

Third, one effect of this policy would be that Germans buy up a lot of Portuguese assets. “Not that there is anything wrong with that” I hear you saying and indeed that is right. Still, solving the crisis by selling a lot of the country to the Germans is not exactly a popular policy in a lot of the periphery and we could expect political resistance from that side as well.

You can think of this all as a rather odd and stunted “price-specie flow mechanism,” where the specie itself has limited geographic mobility. To be sure, this means the inflation would have worked much better had it been applied in earlier years, before various periphery banking systems saw so much trouble.

My initial post on the liquidity leak was here.

Bayonne business practice of the day

The most expensive hospital in America is not set amid the swaying palm trees of Beverly Hills or the luxury townhouses of New York’s Upper East Side.

It is in a faded blue-collar town 11 miles from Midtown Manhattan.

Based on the bills it submits to Medicare, the Bayonne Medical Center charged the highest amounts in the country for nearly one-quarter of the most common hospital treatments, according to a New York Times analysis of 2011 data, the most recent available. No other hospital was at the top of the price list more often.

Bayonne Medical typically charged $99,689 for treating each case of chronic lung disease, five times as much as other hospitals and 17 times as much as Medicare paid in reimbursement. The hospital also charged on average of $120,040 to treat transient ischemia, a type of small stroke that has no lasting effect. That was six times the national average and 24 times what Medicare paid.

For those prices, the quality of care at Bayonne Medical is no better — or worse — than that at most other New Jersey hospitals.

The back story is this:

Bayonne Medical, which was founded in 1888, was losing nearly $1.5 million a month before it filed for bankruptcy in 2007. By 2011, under new ownership and a new financial model [sic], its patient revenue had nearly tripled and its operating income had reached $9.3 million, according to the American Hospital Directory, a publication that compiles data from Medicare and other sources about health care facilities.

Here is one commentary:

“Their model is to charge exorbitant rates, particularly for emergency room services, and if the insurance companies don’t pay them, they threaten to go after the member for the balance of billing,” said Carl King, head of national networks for Aetna, whose in-network contract was also ended by Bayonne in 2008.

You can read more here, interesting throughout.

Assorted links

1. Does parenting suffer from a cost-disease?

2. Ezra Klein interviews Bill Gates about public health and development. Excellent piece. Gates, by the way, is now the world’s richest man once again.

3. College enrollment is falling more than had been expected.

4. “The french fries arrive soggy.”

5. John Lanchester on Google Glass.

Does the eurozone have a monetary policy transmission mechanism? Or rather a liquidity leak?

What would happen if the ECB immediately and directly ran a helicopter drop of money to the periphery? I don’t find that an easy question to answer. Here is one recent report:

But the indicator [interest rate spreads] has since risen again and reached a record of 3.7 percentage points in January, indicating companies in southern Europe were paying significantly higher interest rates than northern rivals.

“Market segmentation remains, divergence in bank lending rates persists and, as a result, immediate growth prospects in the periphery are bleak,” said Huw Pill, European economist at Goldman Sachs, who was previously a senior monetary policy official at the ECB in Frankfurt.

Or read this update. Here is a more specific story about how small to mid-sized Italian banks are contracting.

Would the new helicopter drop money be kept in periphery banks and lent out to stimulate business investment? Or does the new money flee say Portugal because Portuguese banks are not safe enough, Portuguese loans are not lucrative and safe enough, and Portuguese mattresses are too cumbersome?

The former scenario implies that monetary policy should be potent. The latter scenario implies that the helicopter drop will be for naught and the fiscal policy multiplier also will be low, on the upside at the very least (fiscal cuts still might cause a lot of damage on the downside). I call this the liquidity leak, rather than the liquidity trap.

So which scenario is it?

Does it matter who gets the helicopter drop? Perhaps a granny gets the money first and sticks it in the local bank. Alternatively, a financial manager in Lisbon would transfer that same euro rather seamlessly to his second account in Frankfurt. Under this differential scenario, changes in the distribution of wealth also have nominal and eventually real effects.

Is the flow of marginal deposits the problem or the flow of marginal loans? Or both?

Ryan Avent suggests allowing banks to swap their risky commercial loans for safer assets. Other ideas propose running QE on packages of small to mid-sized loans or accepting those loans as collateral at the ECB. Of course these assets are difficult to price and also moral hazard problems would loom. If the ECB is not “overpaying” for the small loans, they won’t be encouraged. If the ECB is overpaying, there are plenty of Sicilian businessmen who have friends at the local bank. The mere lending isn’t enough, the projects also need to be good ones, because in these cases we are talking about tackling issues in the real economy. Can a long-distance ECB collateral support operation spur good, growth-inducing projects? It is easy to see why the Germans might be skeptical.

In some regards these problems will look like liquidity traps, because monetary policy will not always work. But in the periphery lending rates are high (albeit with restricted credit), and standard liquidity trap models will not in general apply. Again, I call it the liquidity leak.

Liquidity trap approaches will encourage you to think in terms of raising expectations of inflation (which is indeed the correct question in many settings), but here the geographic distribution of credit and economic activity is instead the crux of the matter. Our current macroeconomic tools are not well-suited for integration with spatial economics, I am sorry to say.

Addendum: On some related issues, read Scott Sumner.

Further results on hypergamy

This paper, by Marianne Bertrand, Jessica Pan, and Emir Kamenica, was pointed out by Matt Yglesias on Twitter, the abstract is this:

We examine causes and consequences of relative income within households. We establish that gender identity – in particular, an aversion to the wife earning more than the husband – impacts marriage formation, the wife’s labor force participation, the wife’s income conditional on working, marriage satisfaction, likelihood of divorce, and the division of home production. The distribution of the share of household income earned by the wife exhibits a sharp cliff at 0.5, which suggests that a couple is less willing to match if her income exceeds his. Within marriage markets, when a randomly chosen woman becomes more likely to earn more than a randomly chosen man, marriage rates decline. Within couples, if the wife’s potential income (based on her demographics) is likely to exceed the husband’s, the wife is less likely to be in the labor force and earns less than her potential if she does work. Couples where the wife earns more than the husband are less satisfied with their marriage and are more likely to divorce. Finally, based on time use surveys, the gender gap in non-market work is larger if the wife earns more than the husband.

Their title is “Gender Identity and Relative Income within Households.” There is a non-gated copy here.

U.S. clothing chains do not support pact on Bangladesh reforms

From Brad Plumer:

Nearly all U.S. clothing chains, citing the fear of litigation, declined to sign an international pact ahead of a Wednesday deadline, potentially weakening what had been hailed as the best hope for bringing about major reforms in low-wage factories in Bangladesh.

Companies including Wal-Mart, Gap, Target and J.C. Penney had been pressed by labor groups to sign the document in the wake of last month’s factory collapse in Bangladesh that killed at least 1,127 people. More than a dozen European retailers did so. But U.S. companies feared the agreement would give labor groups and others the basis to sue them in court.

…Wal-Mart reiterated Wednesday that it would not sign the accord at this time, because it “introduces requirements, including governance and dispute resolution mechanisms, on supply chain matters that are appropriately left to retailers, suppliers and government, and are unnecessary to achieve fire and safety goals.”

…Most U.S. companies, however, balked at the language in the accord. Some said it would would expose them to excessive legal liability — particularly in America’s litigious courts. Written by labor groups, the agreement would require retailers who source clothing from Bangladesh to commit to pay for inspections, building upgrades and training — all enforced by binding arbitration.

Here is more. Most likely, the damage done to Bangladesh will continue. Note that the prospect of successful litigation was not what drove FDI into the 19th century United States, or twentieth century Singapore, to the point where wages rose significantly.

Have we seen self-defeating austerity in the United States?

Everyone has been talking about the revised CBO deficit forecast, which suggests the short-term U.S. fiscal picture is more favorable than had been realized. It can be said that in the short- to medium-term, the deficit is no longer an issue (in my view that was the case anyway, but that is a different story.)

But I am puzzled as to how the whole story is supposed to fit together, at least from an Old Keynesian perspective.

For instance, we have been told that the United States has been engaged in a good deal of fiscal austerity in the last few years.

We also were told that fiscal self-austerity was quite possibly self-defeating (or here, pdf) or at the very least fairly close to self-defeating. That is, it would make budget balance harder rather than easier.

The amount of attention, and the fervor of the rhetoric, also suggest that this was seen as a major issue, not one minor to moderate factor with seven other significant confounding factors operating on top of it. Admittedly this latter point is more of a subjective impression, but I believe many people have shared it.

OK, now here goes the potential story. We did fiscal austerity, it was self-defeating, that was a major factor, and we ended up in…a better budget situation than we had been expecting?

It is fine to say “our budget situation could have been better yet,” but then the fiscal austerity story then seems to collapse into one factor among many confounding factors. Which is fine by me, but it is not the story we seem to have been receiving.

I am myself comfortable arguing something like “when underlying fundamentals are sound, and/or there is monetary accommodation, an economy can withstand fiscal consolidation just fine.” That is simply a more specific variant of the above.

Another “way out” is to question whether “austerity” is always to easy to measure, given the associated modalities and baselines involved in its current definitions, and given the multiple dimensions of fiscal policy, and so perhaps the degree of austerity has not been nearly as high as we were told. I can buy that too, but still it would be news to the Old Keynesian accounts we have been reading.

So what’s up?

Matt Yglesias appreciates *Star Trek*

You will find his essay here, and I have many points of agreement with him, but I think he undervalues the first series. Characters and script were excellent in about sixty percent of the original episodes. It is also noteworthy that the original characters have entered popular culture for an enduring period of time and we are still making movies about them forty-five years later. It’s not absurd to think of someone saying “Beam me up, Scotty” fifty years from now. I don’t see Data or any other later character receiving the same treatment, nor do I think that any of the later installments would have, on their own, generated an entire franchise of installments, spin-offs, sequels, and the like, where Matt can tweet something like “Animated series is non-canon, people. Get with the program.” If you’d like a treat, watch some of the D.C. Fontana-scripted Star Trek episodes, noting that “Tomorrow is Yesterday” is one of the funniest and most profound takes on “the great stagnation” to be found in popular culture or anywhere else for that matter. And it was written before the great stagnation even started, and by Roddenberry’s office assistant at that. Magic was in the air. As for “Spock’s Brain,” well, that is another matter.

Our improving short-term budget picture

You will find summaries here from Annie Lowrey and also Ezra Klein. I like Ross Douthat’s remarks:

…almost nobody is willing to break out the champagne on these estimates. The Keynesians think our shrinking deficit is a sign of the White House’s foolish surrender to austerity at a time when the economy still needs more government spending, not less, to achieve real lift-off. The deficit hawks think a dropping deficit will only encourage Washington’s fatal short-term thinking, by persuading policymakers to ignore the still-yawning gap between our long-term commitments and our revenues. Conservatives don’t like the extent to which we’re taxing our way to temporary fiscal stability (some of the unexpected deficit reduction reflected high-income tax filers paying extra for 2012 to avoid higher rates for 2013), while liberals have reason to fret that the White House’s “fiscal cliff” strategy squandered an important opportunity to raise upper-income taxes even more. And anyone who worries about the American political system’s ability to do structural reform can’t be that encouraged by the path we’ve taken to this point – the crude cuts to discretionary spending that leave entitlements untouched, the higher marginal tax rates rather than a rate-lowering, deduction-capping tax reform, and of course the general inability to compromise in the absence of artificial deadlines and self-created crises.

I don’t drink champagne but I’ll break out the dark chocolate instead. One way to put it is that “yapping” — on all sides of the political spectrum — is overrated, most of all by the yappers themselves.

A slightly different take would be this. Voters are getting more or less what they want, which is some spending restraint, mostly holding the line on taxes, not too much trust in government as a way of moving forward, and a love of entitlements. One can find that objectionable, and indeed I do across a number of fronts, but there you go. We are not going to elect a new people anytime soon, and in this odd sense you can see all the recent political gridlock as reasonably democratic, more so than its critics would like to admit (I know I’ll generate a bunch of criticisms citing poll data about how Americans really want this, that, or the other but I’ll hold my ground on this one). Relative to the quality of the preference inputs, we are getting a better outcome than one might otherwise have expected. After all, isn’t that what this country is really all about? We may not have the world’s best farinata, but let’s raise a toast to America once again.

Whose entire body of work is worth reading?

I’d be curious to see Tyler’s “completist” list. In other words, authors whose entire body of work merits reading. If this does get a response, I’m most interested in seeing the list begin with literature.

I’ll repeat my earlier mention of Geza Vermes. And to make the exercise meaningful, let’s rule out people who wrote one or two excellent books and then stopped. Adam Smith is too easy a pick. I won’t start with literature, however, but here are some choices:

1. Fernand Braudel.

2. George Orwell. Plato. Nietzsche and Kierkegaard. Hume. William James.

3. Franz Kafka, he died young.

4. T.J. Clark, historian of art and European thought.

5. J.C. D. Clark, the British historian.

Let’s stop here and take stock. Many historians will make the list, because if they are good they will find it difficult to produce crap. Without research, they cannot put pen to paper, and with research a careful, thoughtful historian is likely to be interesting. With thought you could come up with a few hundred historians who were consistently interesting and never wrote a bad book. Then you have a few extreme geniuses, and J.S. Mill might make the list if not for System of Logic, which by the way Mill himself thought stood among his best works. Timon of Athens hurts Shakespeare but he also comes very close.

Do any producers of “ideas books” make this list? Other than those listed under #2 of course. And are there truly consistent (and excellent) authors of fiction, other than those with a small number of works? I’m not thinking of many. How about Virginia Woolf or John Milton or Jane Austen?

One also could make an “opposite” of this list, namely important authors whose works are mostly not worth reading, and you could start with Conan Doyle, H.G. Wells, and Aldous Huxley. The existence of Kindle makes it easier to discover who these people really are.

Assorted links

1. Google flu trends, and Google dengue trends.

2. Against empathy?

4. Japanese butter grater, and the standing restaurant (Japan also, coming to New York), and more Edward Hugh on Abenomics.

6. The place names of Orkney and the Shetlands.

7. The wisdom of Steven Pearlstein, on austerity.

8. Geza Vermes has passed away, read all of his books.

Markets in everything, the culture that is Manhattan

Some wealthy Manhattan moms have figured out a way to cut the long lines at Disney World — by hiring disabled people to pose as family members so they and their kids can jump to the front, The Post has learned.

The “black-market Disney guides” run $130 an hour, or $1,040 for an eight-hour day.

“My daughter waited one minute to get on ‘It’s a Small World’ — the other kids had to wait 2 1/2 hours,” crowed one mom, who hired a disabled guide through Dream Tours Florida.

“You can’t go to Disney without a tour concierge,’’ she sniffed. “This is how the 1 percent does Disney.”

That is by the way much cheaper than Disney’s own “VIP service,” which costs over $300 an hour. Here is more, and I thank Neal and also Adam Cohen for the pointer.

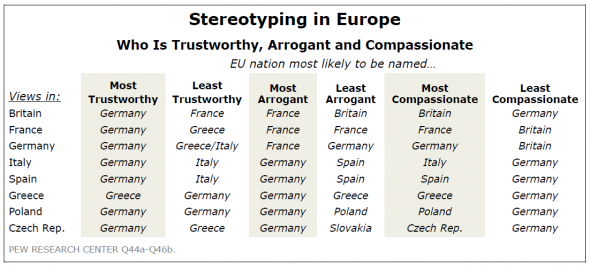

Stereotyping in Europe

Each column is interesting, for instance read down for “Most Compassionate.” It’s funny how many individuals do the same for themselves, I might add, in what has to be one of the simplest and most common of all intellectual mistakes.

Those results are from the new Pew report, summarized by David Keohane here. The French are growing increasingly disillusioned with the European project, and on key questions the French see the world as the Italians or Spanish do, not the Germans. And there is this: “The report also takes down a few German stereotypes. Apparently, Germans are among the least likely of those surveyed to see inflation as a very big problem and the most likely among the richer European nations to be willing to provide financial assistance to other European Union countries that have major financial problems.”

Save the World Bank’s *Doing Business* report

Yesterday I received an email from Michael Klein:

We are writing to you about the World Bank’s Doing Business report. Published since 2003 the report benchmarks 185 countries annually on key dimensions of the legal and regulatory environment for small businesses. It has supported numerous reforms all over the world helping small businesses and employment.

There is currently a serious risk that the report may be abolished or severely curtailed as part of an ongoing review that will be finished in the next few weeks. The report has always been subject to controversy as it highlights shortcomings that countries may not appreciate. The World Bank’s President and its Board of Executive Directors will consider the future of the report in the next few months.

We would like to ask you to support an open letter to the World Bank’s President and its Executive Directors supporting the Doing Business project and recommending general directions for the future. The letter (see below) is informed by our review of the arguments about Doing Business (attached).

This is our private initiative and without any institutional affiliation.

Please, reply by return email, if you agree to support the open letter. If you wish, indicate in which capacity you want to be mentioned. If you want to forward this email to ask others also to support the letter, please, ask them to reply to this email address ([email protected]) so that we can keep an accurate record of support.

I support the report very much and I have found it useful in my own work. It is one of the best things the World Bank does, and you can read more about the report here. Please do email at the above address if you think your support can be useful. Here is some back story on how China is seeking to push around the Bank on the ratings. Here is FT coverage of the same.