Category: Data Source

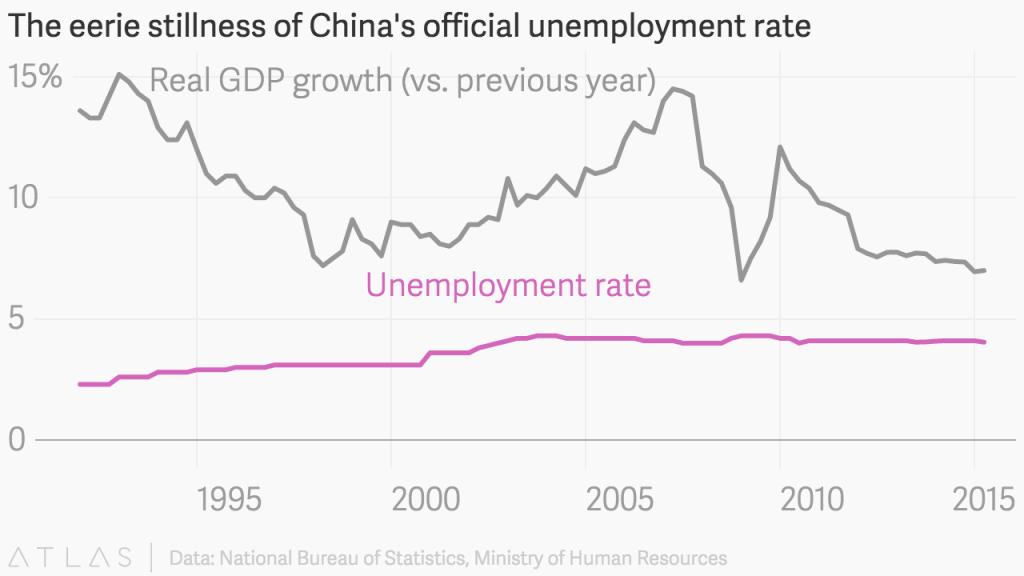

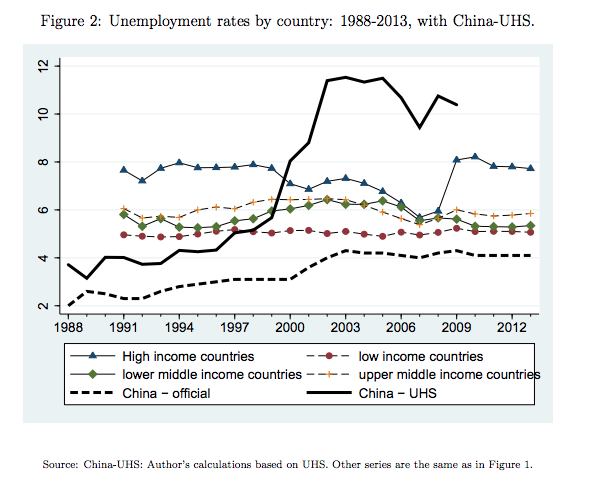

What is China’s Unemployment Rate?

What is China’s Unemployment Rate? 4.1% For what month, what year? Doesn’t matter the answer is still 4.1%. That’s a slight exaggeration but for the last 3 years the unemployment rate has been 4.1% almost every month. Indeed, since 2002 the official unemployment rate has varied between 3.9% and 4.3%, an absurdly smooth series.

In contrast to the unemployment rate, China’s GDP growth rate has had massive swings. As a piece in Quartz puts it the unemployment rate exhibits an eerie stillness.

A new NBER working paper uses a newly available household survey and finds a very different series–the China-UHS series shown in black below. According to these estimates China’s unemployment rate shot up to around 11% in 2002 and has been nearly that high at least until 2009 when unfortunately the new series ends.

So how high is Chinese unemployment today? No one knows but it could well be closer to 10% than to 4.1%.

Keep an eye on China and don’t be surprised by the unexpected. In China it’s not just the unemployment rate that is more volatile than it appears.

China fact of the day

New Jersey facts of the day

I was startled by these calculations for New Jersey, for example: Cutting in half the number of people sent to prison for drug crimes would reduce the prison population at the end of 2021 by only 3 percent. By contrast, cutting the effective sentences, or time actually served, for violent offenders by just 15 percent would reduce the number of inmates in 2021 by 7 percent — more than twice as much, but still hardly the revolution many reformers seek.

New Jersey could reduce its prison population by 25 percent by 2021. But to do it, it would have to take the politically fraught step of cutting in half the effective sentences for violent offenders.

In other words, the real debate over how to deal with criminals has hardly begun.

The low-hanging fruit on this issue seems to be in Kentucky, Missouri, and Texas most of all. But keep in mind another point: to the extent prison overcrowding eases, many judges will be giving longer sentences to many of the more violent offenders.

Measuring innovation by job quantities

From Greg Ip:

Quantifying innovation is difficult: Government statistics don’t adequately measure activities that only recently came into existence. Mr. Mandel circumvents this problem by surmising that innovation leaves its mark in the sorts of skills employers demand. For example, the shale oil and gas revolution is apparent in the soaring numbers of mining, geological and petroleum engineers, whereas the ranks of biological, medical, chemical, and materials scientists have slipped since 2006-07.

Screening job postings on Indeed, a job website, Mr. Mandel finds that the proportion mentioning “Android” (Google’s mobile operating system), “fracking” and “robotics” has risen notably in the past four to six years. But the proportion mentioning “composite materials,” “biologist,” “gene” or “nanotechnology” has trended down. His conclusion: Today’s economy is “unevenly innovative.”

You can find the whole article here. Does anyone have a link to the study itself?

Women like free trade less

Or so it seems. Mansfield, Mutz, and Silver write:

In this paper, we provide one of the first systematic analyses of gender’s effect on trade attitudes. We draw on a unique representative national survey of American workers that allows us to evaluate a variety of potential explanations for gender differences in attitudes toward free trade and open markets more generally. We find that existing explanations for the gender gap, most notably differences between men and women in economic knowledge and differing material self-interests, do not explain the gap. Rather, the gender difference in trade preferences and attitudes about open markets is due to less favorable attitudes toward competition among women, less willingness to relocate for jobs among women, and more isolationist non-economic foreign policy attitudes among women.

The pointer is from Ben Southwood, I do not see an ungated copy.

Can economists justify pre-market exclusion for pharmaceuticals?

One recurring problem in economics, and the other social sciences all the more, is that researchers will accept a lot of conventional wisdom on a topic if it suits their preexisting biases, especially if it is not an area which they have researched themselves. Yet this entire question is — surprise, surprise — largely unstudied. Social scientists love to talk about themselves, but critical self-scrutiny backed by data is less popular.

Jason Briggeman just wrote a GMU dissertation to investigate these and similar questions, here is his abstract:

In the United States and most other wealthy nations, all drugs are banned unless individually permitted. This policy, called pre-market approval, is controversial among economists; the preponderance of the economics literature that offers a judgment on pre-market approval is critical of the policy, but surveys of U.S. economists show that many, perhaps a majority, support pre-market approval. Here I analyze the results of a recent survey that asked economists who support pre-market approval to justify, with reference to the economic concept of market failure, their support of the policy. I find that, while almost all the economists surveyed could point to a market failure or failures that may plausibly exist and affect the market for pharmaceuticals, none were able to make a well reasoned connection between those market failures and the particular remedy of pre-market approval. None of the economists surveyed cited in support of their position any literature specific to pre-market approval. I supplement the survey findings with a review of relevant reading material assigned in health economics courses at top universities, searching that material for discussions of what may justify pre-market approval. I find a strong argument that the prospect of overt disasters being caused by avoidable mistakes can justify some intervention in pharmaceuticals; however, I find little to justify the other interventions that are part of pre-market approval. I suggest that future inquiry into possibilities for liberalizing reform concentrate on understanding matters such as the informational effects of product bans, the distinction between safety and efficacy, the nature of demand for drugs about which little is known, and the political economy of drug substitutes.

The upshot is that economists hold a lot of views whose justifications they cannot articulate very well. I think you would find the same when it comes to the Ex-Im Bank (are you sure it fits the model of strategic trade theory?), the mortgage agencies (what was that externalities argument for home ownership again?) or all sorts of random regulations. The relatively interventionist economists will pull some justification out of a hat, and the relatively pro-market economists will be pretty skeptical.

For the pointer I thank Daniel Klein.

India Fact of the Day

In India, for example, the number of taxpayers in relation to voters in the economy has been about 4-4.5% for a long time.

That is from an in-depth discussion about the Indian economy between Karthik Muralidharan and Arvind Subramanian (Chief Economic Adviser, Government of India). The reference is to income tax, of course. It’s a great discussion and the best place to begin if you want to understand the Indian economy today.

Regulation, imperfect competition, and the U.S. abortion market

There is a newly published paper by Andrew Beauchamp:

The U.S. abortion market has grown increasingly concentrated recently, while many states tightened abortion laws. Using data on abortion providers, I estimate an equilibrium model of demand, price competition, entry and exit, to capture the effect of regulation on industry dynamics. Estimates show regulations played an important role in determining the abortion market structure and evolution. Counterfactual simulations reveal increases in demand-aimed regulation were the most important observed factor in explaining recent abortion declines. Simulating Utah’s regulatory regime nationally shows tightening abortion restrictions can increase abortions in equilibrium, mainly through tilting the competitive landscape toward low-price providers.

There are ungated versions here, and for the pointer I thank the excellent K.

Balkans fact of the day

Which three economies in Europe have the lowest employment to population ratio, circa 2013?

Greece, Croatia, and Serbia comes in last.

That is from the World Bank and ultimately Eurostat, see p.5 (pdf).

You will note of course that Croatia and Serbia have their own floating rate currencies. In Serbia the measured unemployment rate is about nineteen percent and a few years ago was above twenty-five percent.

While I do usually favor floating currencies, there are limits to what they can accomplish when other policies are bad. If you are wondering, the rate of inflation in Serbia has been falling from an average of about seven percent to about two percent. Wages in the country are often sticky and public sector jobs on average pay higher than private sector jobs (see the first link). Exports and productivity are weak.

By the way, here is my earlier post which covers unemployment in Jamaica.

The highest-ranking rooster has priority to announce the break of dawn

Tsuyoshi Shimmura, Shosei Ohashi, and Takashi Yoshimura have a new paper:

The “cock-a-doodle-doo” crowing of roosters, which symbolizes the break of dawn in many cultures, is controlled by the circadian clock. When one rooster announces the break of dawn, others in the vicinity immediately follow. Chickens are highly social animals, and they develop a linear and fixed hierarchy in small groups. We found that when chickens were housed in small groups, the top-ranking rooster determined the timing of predawn crowing. Specifically, the top-ranking rooster always started to crow first, followed by its subordinates, in descending order of social rank. When the top-ranking rooster was physically removed from a group, the second-ranking rooster initiated crowing. The presence of a dominant rooster significantly reduced the number of predawn crows in subordinates. However, the number of crows induced by external stimuli was independent of social rank, confirming that subordinates have the ability to crow. Although the timing of subordinates’ predawn crowing was strongly dependent on that of the top-ranking rooster, free-running periods of body temperature rhythms differed among individuals, and crowing rhythm did not entrain to a crowing sound stimulus. These results indicate that in a group situation, the top-ranking rooster has priority to announce the break of dawn, and that subordinate roosters are patient enough to wait for the top-ranking rooster’s first crow every morning and thus compromise their circadian clock for social reasons.

In case you had any doubts. The pointer is from Michelle Dawson.

A long look at short-termism

That is the title of a working study from Credit Suisse (pdf), here is one excerpt:

The problem is that short-termism is very difficult to prove. As we will see, many of the common perceived symptoms of short-termism don’t hold up to scrutiny, and there are some legitimate reasons for the shortening of time horizons. While there remains plenty of room for improvement, especially when it comes to incentives, the issue of short-termism deserves more care than it has received in the popular discourse. With little exception, the debate appears to be very one-sided.

Here is another good bit of many:

Were compensation the simple root of the problem, then correction through regulation or other market forces would be relatively straightforward. But a link between pay and termism is difficult to establish. Academic research shows that CEO pay has closely followed the size of the firms in the economy independent of the form of remuneration. Further, executive compensation has moved toward long term incentives, boards of directors are more independent than in the past, and governance committees are “nearly universal.” Reviewing the challenges of conclusively demonstrating short-termism, one scholar wrote, “[I am] aware of no empirical evidence establishing that executive pay term is inadequately focused on long-term performance from either a shareholder or societal perspective, systematically.”

And:

To summarize, a proper test of short-termism should address the micro-macro problem by relying on the outcome of the market pricing process rather than the views of individuals. While many constituents feel the market is short-term oriented—a feeling that has been expressed through the decades—asset prices don’t support this sense.

In fact there is a good deal of evidence that the sectors which require the most long-term attention attract investors and boards who understand that need. Here is my previous post on this issue.

For the pointer I thank Michael Mauboussin.

Does Fair Trade Help Poor Workers?

Does Fair Trade help poor workers? Probably not says Don Boudreaux in this excellent, short video from the Everyday Economics series at Marginal Revolution University.

As is well known, however, Don is a rabid, free-market economist with ideological blinders who has been captured by corporate interests. So let’s ignore what Don says and consider what William MacAskill, author of Doing Good Better (reviewed earlier this week) has to say. No one can fault MacAskill’s charitable bona-fides:

MacAskill’s own pledge is to donate everything he earns above about $35,000 per year, adjusted using standard economic measures for inflation and cost of living, to the organizations that he believes will do the most good. Since his bar is roughly at the UK median income—such that half the population earns more each year, and half the population earns less—he’s certainly not condemning himself to a life of hardship; rather, he is pre-committing to staying roughly in the middle of the national income distribution even as his earnings go up over time.

That said, his pledge means giving away 60 percent of his expected lifetime earnings.

When I ask him the inevitable questions about whether this isn’t rather a lot to sacrifice for one person, MacAskill shrugs modestly and smiles broadly. “Imagine you’re walking down the street and see a building on fire,” he says. “You run in, kick the door down—smoke billowing—you run in and save a young child. That would be a pretty amazing day in your life: That’s a day that would stay with you forever. Who wouldn’t want to have that experience? But the most effective charities can save a life for $4,000, so many of us are lucky enough that we can save a life every year through our donations. When you’re able to achieve so much at such low cost to yourself…why wouldn’t you do that? The only reason not to is that you’re stuck in the status quo, where giving away so much of your income seems a little bit odd.”

So what are MacAskill’s views on Fair Trade? Why they are the same as Don’s!

…when you buy fair-trade, you usually aren’t giving money to the poorest people in the world. Fairtrade standards are difficult to meet, which means that those in the poorest countries typically can’t afford to get Fairtrade certification. For example, the majority of fair-trade coffee production comes from comparatively rich countries like Mexico and Costa Rica, which are ten times richer than the very poorest countries like Ethiopia.

….In buying Fairtrade products, you’re at best giving very small amounts of money to people in comparatively well-off countries. You’d do considerably more good by buying cheaper goods and donating the money you save to one of the most cost-effective charities…

The world trade slowdown continues, and worsens

The latest World Trade Monitor showed the volume of world trade falling in May by 1.2 per cent. It slid in four out of five months in 2015 and risen just 1.5 per cent in the past 12 months — less than the growth in global output and far below the long-term average of about 7 per cent a year.

The problem has been getting worse for some time. Trade bounced back fairly well in 2010 after the global recession but it has disappointed ever since, growing by barely 3 per cent in 2012 and 2013. Now it seems the world cannot manage even that.

That is from Stephanie Flanders.

China estimate of the day

Annual real growth in gross capital formation hit 6.6 per cent in 2014, down from 10.2 per cent in 2013 and a peak of 25 per cent in 2009.

Thomas Gatley, China corporate analyst at Gavekal Dragonomics, a research firm, estimates that so far this year GFCF may be running at around 4 to 5 per cent.

That is from James Kynge at the FT. Here is from Ambrose Evans-Pritchard:

David Cui, from Bank of America, said $1.2 trillion of stock holdings are being carried on margin debt. This is 34pc of the free float of the Shanghai and Shenzhen stock markets. “When the market ultimately settles at a level that can be sustained on fundamental reasons, we expect that the financial system may wobble, due to high contagion risk,” he said.

Mr Cui said the brokers and trusts have barely 1.6 trillion yuan ($260bn) to absorb losses and may be overrun. “Given the particularly thin front line of the financial institutions, we suspect that it’s a matter of time before banks may have to face the music,” he said.

This in turn risks setting off a “bank run” on the shadow banking system as investors lose trust in wealth management funds, fearing that their deposits in the $2.1 trillion industry no longer have an implicit guarantee.

As Arnold Kling would say, have a nice day…

China fact of the day

Around 97% of existing yuan-denominated bonds hold ratings of double-A to triple-A—the best a company can get.

That is from Fiona Law, cited by Christopher Balding, and ultimately Alex Frangos, those are ratings from Chinese sources. Law reports:

With nine Chinese ratings firms to choose among, “bond issuers are encouraged to pick the highest ratings among agencies,” said Guan Jianzhong, chairman of Dagong Global, the country’s third-biggest ratings company in terms of market share. The fact that the bonds are rated double-A-minus or above, they “are not without risks,” he said.

By the way, the Shanghai Composite Index closes down 8.5%.