Category: Data Source

Rent Control: The Ceiling Trap

Rent control is in the news again. Check out my new website, Rent Control: The Ceiling Trap. Here is just one bit:

Norway abolished its rent control in 1982, and the economist Are Oust realized the newspapers had been quietly recording the whole experiment. He collected housing classifieds from Oslo’s Aftenposten from 1970 to 2008 and watched the market turn inside out.

Under rent control, Oslo’s listings pages looked nothing like a housing market. It was tenants who advertised, pleading their qualities to landlords — “housing wanted” ads outnumbered “housing for rent.” Ten to fifteen percent of those ads were placed by the tenant’s employer, vouching for them the way a bank vouches for a borrower. Tenants offered babysitting, gardening, snow-shoveling, and janitorial work on the side to sweeten the deal. Landlords, for their part, could demand a tenant of a particular gender, age, occupation, region of origin — some ads specified “strong Christian beliefs.” Deposits commonly ran to 50 or 60 months’ rent, occasionally 100 or more: tenants effectively lent the landlord the equity of the flat, interest free. And only about 20 percent of “for rent” ads dared print the rent, much of which would have been illegal.

Then the ceiling lifted. Within a few years the page flipped: landlords advertised to tenants, roughly 80 percent of listings printed an asking rent, the mega-deposits vanished, and the demands for snow-shoveling Christians of specified gender dwindled to nothing. The price went back to doing the rationing — so nothing else had to.

Check out the whole thing–it’s fabulous.

Differentiation drives the erosion of positivity on social media

We live in a digital age, where billions of people engage in dialogue within topic-bound communities and threads. In an archival analysis of over 2 billion Reddit comments and an experiment, we show that this dialogue becomes more negative over time. Further analyses suggest that negativity rises over time because social media users seek to make unique comments on the same topic, and it is easier to differentiate oneself through negative comments than through positive comments. As threads and communities evolve, and it becomes more difficult to make unique observations, users turn to negativity. Our studies show how basic human motives interact with the structure of social media platforms, posing an acute challenge for sustaining healthy online dialogue.

Here is the article by Hongkai Mao, et.al. Via the excellent Kevin Lewis. For some of you commenters, how does it feel to be a puppet in the unfolding of this game?

Azeem Azhar (and others) on the state of the AI economy

Due to travel I have not had time to read this detailed report, but it is getting very good reviews

Does fasting harm cognitive performance?

More than 2 billion people participate annually in Ramadan fasting, making its potential effects on cognitive performance important for workplaces, education and high-stakes decision-making. We study these effects in tournament chess, an incentivised, real-world cognitive task in which move quality can be evaluated objectively by a strong chess engine. We analyse nearly 300,000 games and more than 25 million moves played by almost 10,000 expert players from 178 countries over 10 years. Two validation exercises support our Muslim-status classification, covering almost 11% of the sample and survey evidence indicates substantial Ramadan fasting compliance among Muslim chess players. In the preferred intention-to-treat specification, using pre-game controls, player fixed effects and year-month fixed effects, we find no impact of Ramadan fasting on Muslim players’ overall move quality or shares of optimal and nearly optimal moves, with tightly bounded estimates around zero. Muslim players make 0.13 additional percentage points of large errors during Ramadan, but this small estimate is fragile across alternative measures, samples, Muslim-status definitions, fasting-compliance adjustments and event-study diagnostics, with no evidence of heterogeneous effects, selection bias, or compensatory behavioural adjustments. We conclude there is little robust evidence that Ramadan fasting broadly impairs cognitive performance among expert chess players.

That is from a recently published paper by Samuel Buckland and David Smerdon. Some claim that people think best when they are just a wee bit hungry?

Via the excellent Kevin Lewis.

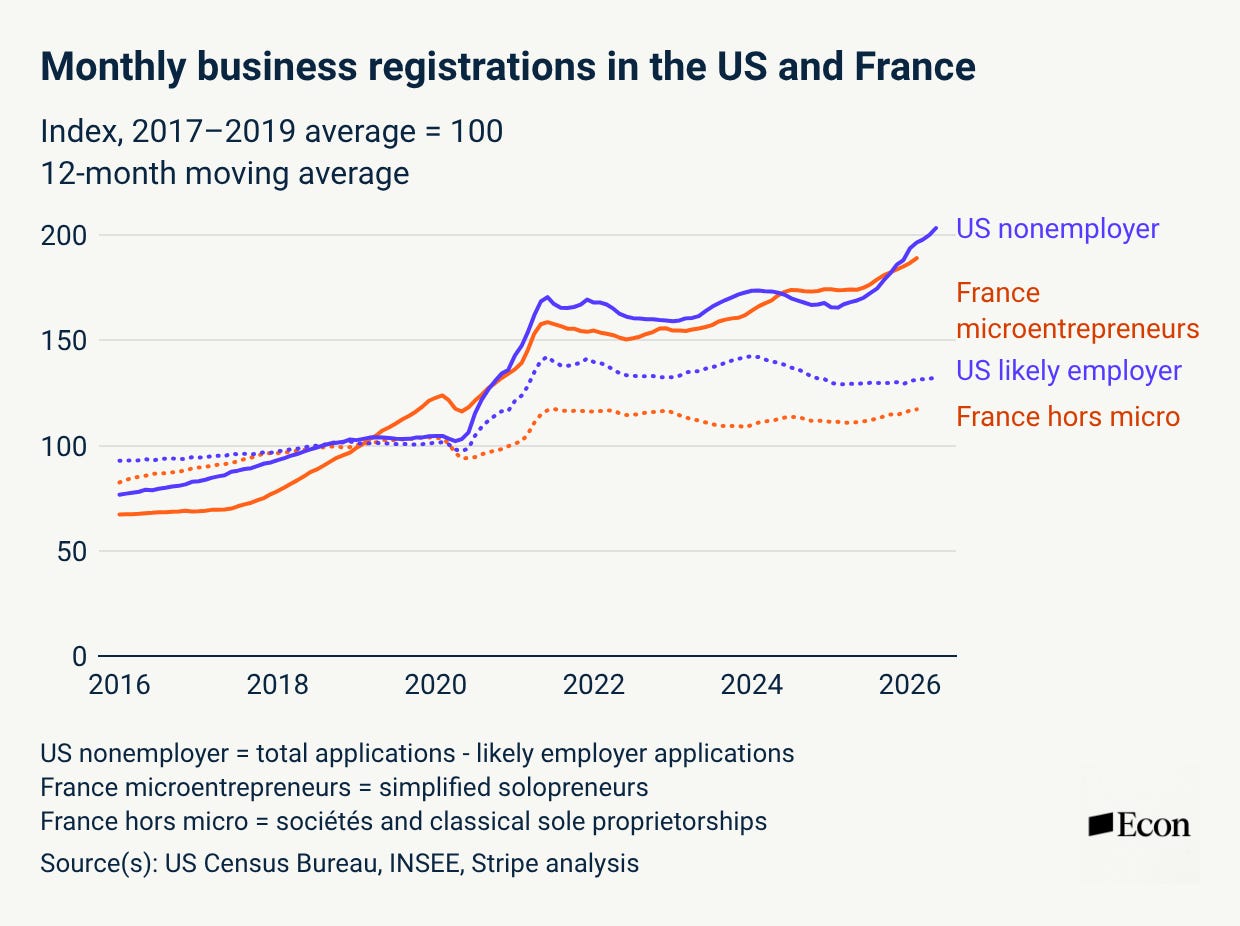

New Business Formation is Surging–Again.

New business formation is surging–again.

Business formation first jumped in 2020 as the pandemic reorganized work, shopping and logistics. After the pandemic ended, business formation leveled off, but it did not return to its old path. It remained historically high. Moreover, in the past 18 months or so business formation has surged again. Registered Agents Inc tracks new Articles of Organization or Incorporation filed in the 50 states and they report:

Every month in 2026 has set a new formation record, including March, which stands as the highest single-month total in the history of the Business Formation Report. Through May, 2.9 million new businesses have been formed nationwide, the strongest five-month start on record.

Stripe Economics agrees and calls this the age of the solopreneur. Among businesses using Stripe, recent cohorts are reaching serious transaction volumes faster than earlier cohorts.

The share of businesses (not just solopreneurs) reaching $1 million in cumulative revenue within a year after going live on Stripe was roughly 30% higher for the 2025 cohort as it was for the 2023 cohort, and it was roughly 3x higher for the 2025 cohort than the 2019 cohort.

Furthermore, the trend is not just in the United States. France, where, as the story goes, they have no word for entrepreneur, has also seen business creation reach record levels, driven heavily by micro-entrepreneurs.

The most likely explanation is the devolution of power. A single person armed with Stripe, Shopify, cloud software, automated bookkeeping, and now AI can do what once required a small staff. Dynamism had been on a long secular decline, but we may now be seeing the early stages of an experimental economy—one in which far more people can test ideas, reach customers, and launch firms, some of which will grow very large, very fast.

GLP-1 drugs and marriage

GLP-1 medications generate large weight loss and may also alter social and economic outcomes. Using the Understanding America Study, I compare women starting GLP-1s for weight loss with matched women who would like to start a GLP-1 but have not. Single women’s marriage/cohabitation rates rise by 29 percentage points and employment among baseline non-employed women rises 27 percentage points after six or more quarters. Existing partnerships do not dissolve, and already-employed women show no upward job mobility. The pattern suggests that part of the female obesity penalty operates at new-match formation rather than only through health or incumbent productivity.

Here is the paper by Rebecca Diamond. And here is a thread on the paper. And not everyone believes the size of these estimates. I do not find them so crazy? Here is Steven’s dialogue with GPT.

Elderly Health and Longevity in the US

Rising elderly life expectancy is a well-known source of fiscal pressure on Social Security and Medicare – but how have declining mortality and morbidity affected the two programs’ relative finances? Using nearly three decades of Medicare Current Beneficiary Survey data (1992-2019), we estimate that these demographic changes raised expected lifetime Social Security spending by over twice as much as expected lifetime Medicare spending: 14% compared to 6%. The slower growth of elderly lifetime health care spending than annuity spending reflects two features of how longevity has increased: the additional 2.4 years of remaining life expectancy were entirely healthy – free of physical or cognitive limitations – while the expected amount of time spent with severe health limitations fell by about 30%, reducing expected lifetime nursing-home and home-health use. We then write down a stylized life-cycle model of a risk-averse retiree facing stochastic mortality and health to illuminate the key forces that affect the optimal allocation of a fixed amount of public funds across Medicare and Social Security.

That is from a new NBER working paper by Liran Einav and Amy Finkelstein. In general I wish to switch resources from Medicare to Social Security, or at least give individuals the option to do so. You can use dollars to buy health care, but it is not always so easy to make the transformation in the opposite direction.

Music markets remain deglobalized

It might seem surprising, in a world of global stars, that the 6m Danes, many of whom are fluent in English, listen mainly to homegrown music. And until fairly recently they did not. In 2019 only five songs in Denmark’s top 20 were in Danish. By last year the figure was 18.

A similar trend is under way in other countries—and in other forms of entertainment. From Asia to the Americas, music charts are increasingly dominated by local sounds. Hollywood television-streaming companies are commissioning more local productions in foreign markets, causing consumption of American shows to fall. Social networks are connecting the whole world, but so far people are mainly using them to consume local content. And as video gaming expands, it too is becoming increasingly tailored to local cultures…

In 2023 Will Page and Chris Dalla Riva noted in a London School of Economics paper that a number of European countries including France, Germany, Italy and Poland had seen rising domestic shares of their top tens in the preceding decade. Since then the phenomenon seems to have spread. Mr Page, formerly chief economist at Spotify, finds that 55% of streams of songs in Sweden’s top 20 last year were in Swedish, up from 29% in 2019. Norway’s figure rose from 13% to 38% in the same period.

That is from The Economist, and of course it echoes themes from my earlier Creative Destruction: How Globalization is Changing the World’s Cultures. And Brazil most of all?

Latin America has gone the same way (see chart 1), Brazil astonishingly so: in the first week of June 96 of the top 100 artists on YouTube Music in the country were Brazilian (foreigners included Justin Bieber and Michael Jackson). Last year Thailand had a solidly local top ten, while Indonesia and the Philippines each had eight local tracks in their respective charts; Nigeria’s top ten were all local, as were nine of South Africa’s, according to the IFPI, which represents the recorded-music industry.

The same trends are happening for television as well, albeit less radically.

AI-Native Firms

Very important work from Hyunjin Kim and Rembrand Koning. Insead and HBS respectively:

We study how firms built around AI capabilities-“AI-native” firms-are organized. Drawing on Y Combinator batches W20-F24 and U.S. venture-backed startups whose first financing closed between 2020 and 2024, we classify each firm’s AI-native status and link it to workforce microdata on team size, function, seniority, and hierarchy. Relative to non-AI startups in the same industry-cohort, AI-native firms are 25% smaller. Their share of engineers is 13% greater, and the shares of entry-level workers and managers are each roughly 15% lower. Their hierarchies are half a seniority level flatter-yet valuations are comparable, implying more value created per employee. We argue these patterns reflect two channels: a process channel, in which AI changes how people work inside the firm, and a product channel, in which AI capabilities are built into what the firm sells. Using text from product descriptions and job postings, we find that embedding AI into the product, beyond layering on AI tools into existing workflows, is a primary way startups are scaling “knowledge work” without large teams of knowledge workers.

The tweet storm on the new paper is especially useful. Via Luis Garicano. And note those results predate the very latest and best tools.

A Cohort Perspective on Latin America’s Fertility Transition

Latin America’s momentous fertility transition is now in the domain of history, allowing a cohort perspective on the decline of completed fertility. Using census microdata from 17 Latin American countries, we track female birth cohorts from the 1920s to the 1970s by subnational region to document the extent to which cohort fertility decline coincided with other demographic and socioeconomic processes. Across cohorts within subnational regions, children ever born fell one-for-one with mortality decline. Expansions in urbanization, multigenerational living, women’s and husbands’ education, women’s employment, and the non-agricultural sector all predicted declines in ever-born and surviving fertility, but women’s education and sectoral composition were the dominant forces after covariate adjustment. Fertility decline was not systematically linked with improvements in children’s outcomes, including school enrollment, literacy, primary completion, and non-employment. These cohort facts challenge theories of fertility decline centered on women’s work and children’s education but support others emphasizing women’s education.

I fear that means the women think they are finding better and more fun things to do? Which is hardly bad per se, but…

That is from a new NBER working paper by Regina Calles and Tom Vogl.

Facts about American men and women

Much of what looks like changing marriage preferences over the twentieth century is actually demographics. Exploiting plausibly exogenous variation in sex ratios across U.S. birth cohorts (1870, 1930, 1950), we jointly identify preferences, match quality dynamics, and the costs of marriage and divorce. Demographics alone explain two-thirds of cross-cohort differences. Women’s premium for older husbands collapsed across cohorts; men’s preferences barely changed. Love that survives its early years becomes permanent, but the odds of surviving fell from 97% to 44%. Divorce costs fell six-fold and depend on life stage. A horse race across behavioral channels shows that the match quality process—not mate-age preferences—is the primary dimension of generational change. Declining divorce costs and fragile match quality are substitutes: either alone fits the data, but together they reveal two independent dimensions of social change. The model validates out of sample on the 1910 and 1970 cohorts.

That is from a recent paper by Jose-Victor Rıos-Rull, Shannon Seitz, and Satoshi Tanaka. Via the excellent Samir Varma.

Do teens regret their social media use?

A new study by Irish researcher Eoin Whelan attempts to answer this. Dr. Whelan told me he was specifically inspired by Haidt’s 2024 claims and sought to examine them rigorously and in the context of other regrets. This is a great use of science…testing dramatic public claims. So…do they hold up?

In Dr. Whelan’s study, 389 young adult participants (20-24) who were social media users as teens were asked about their regrets regarding their teenage years. A list of 20 possible teenage regrets was asked of all participants, with degree of regret marked on a 7-point Likert scale. This is an interesting design…testing social media regrets against other possible regrets, putting them in better context than the crude survey Haidt relied on.

So how did social media regrets hold up? Out of 20 possible regrets, too much time on social media ranked 13th. The top regrets were 1.) not sticking up for oneself, 2.) being too self-conscious, 3.) not documenting memories, 4.) not learning practical life skills and 5.) not getting help with mental health. Girls were slightly more likely to regret time on social media than boys (ranking 11th vs 13th) though this effect was very small (I estimated it at about r = .11) so hardly the big “vulnerable girls” narrative some have peddled.

Further, regrets over time spent on social media as a teen did not predict current young adult life satisfaction for either boys or girls. Thus such regrets may be more a symptom of current panics over social media than anything of actual life importance2. Of the regrets, only not working harder in school and not exercising negatively predicted young adult life satisfaction. Interestingly, having regrets over socializing with friends positively predicted life satisfaction.

As Dr. Whelan noted in his study, “The objective of this study was to critically examine the commonly held belief that social media use during teenage years is a significant source of regret and a predictor of diminished well-being in early adulthood…Contrary to dominant narratives in the public domain, our results suggest that regrets over time spent on social media are not among the most potent regrets reported by young adults…As such, these results align with prior research indicating that the harmful effects of social media may be overstated.”

Here is the full Chris Ferguson Substack.

Can Online Activity Be Regulated? Evidence from Adult Websites

The consequences of online regulations depend on the extent to which users can circumvent restrictions or substitute toward noncompliant platforms. Since 2023, 25 U.S. states have implemented age verification laws that caused prominent adult websites (including Pornhub) to restrict local access for all users. We study how these restrictions affected browsing activity using individual-level panel data. Access restrictions reduced overall time spent on adult sites by roughly 10%. Specifically, for every 100 hours spent on top adult sites before restrictions, about 50 hours remained accessible at noncompliant sites that never restricted access, 30 hours persisted through VPN-based circumvention, 10 hours were substituted from compliant sites to noncompliant sites, and 10 hours were no longer spent on adult sites.

That is from a new NBER working paper by Matthew Brown, Emily J. Davis, and Devin G. Pope.

Who Leads? Relative Age Effects on Social Capital

A fascinating paper and result:

This paper studies the causal effect of being the oldest within a school cohort on social capital. Using a fuzzy regression discontinuity design and data from Facebook, we find that boys who are older than their classmates make 11% more friends in high school. This social advantage is associated with leadership roles, with relatively older boys 42% more likely to become class president than their relatively younger peers. Men who were relatively older during childhood have larger social networks in adulthood, and disproportionately sort into management and entrepreneurship. Our findings suggest that small age differences in peer composition can have persistent effects on social and economic outcomes.

That is from Matthew Jacob of Harvard and Michael Bailey of Facebook. Via the excellent Kevin Lewis.

General-purpose large language models outperform specialized clinical AI tools on medical benchmarks

This result does not surprise me at all. Here is part of the abstract:

Frontier LLMs outperformed clinical AI tools in all three evaluations. Clinical AI tools performed comparably to auto-enabled Google Search AI Overview on the RCQ. These findings highlight the need for independent, real-world evaluation of AI tools before they enter clinical settings.

From Krithik Viswanath, et.al. As a side note, this (and the more general version of the point) is one big reason why some fairly large number of Emergent Ventures proposals are rejected rather quickly.