Category: Data Source

*How to Win a Trade War: An Optimistic Guide to an Anxious Global Economy*

That is the new Soumaya Keynes book, out today. I was happy to have blurbed this book, and here is an essay, on export restrictions, based on the book.

India fertility facts of the day

Ten notable facts from India’s new SRS Statistical Report 2024 published two days ago:

1) India’s total fertility rate (TFR) has dropped to 1.88 (rounded up to 1.9 in the figures) in 2024 from 1.92 in 2023.

2) This drop is roughly the historical speed of the last few decades. India’s TFR was 4.3 in 1985 and it has been falling around 0.06 per year since then.

3) For those who think “smartphones are the reason for the fall of TFR,” there is not much change in India’s TFR after their introduction. Of course, this might only apply to India.

4) India’s sex ratio at birth continues moving toward natural levels. It has grown from 907 girls per 1000 boys in 2018-2020 to 918 in 2022-2024. Without sex selection (e.g., selective abortions), it should be around 952.

5) Nonetheless, this bias still means that India’s replacement rate is around 2.15, not 2.1 as in other advanced economies.

6) Hence, India is already 0.27 children below the replacement rate and the gap continues growing.

7) However, this figure hides large regional differences. Kerala is at 1.3, well below the U.S. and approaching Italian and Spanish levels (Delhi is even lower, at 1.2, but it is a peculiar case), while Bihar remains at 2.9.

8) In terms of the rural/urban divide, rural India is at 2.1 and urban India at 1.5.

9) From everything I can see, India’s TFR will continue to fall, and it should reach 1.57 (the current level of the U.S.) around 2031 unless something significant changes.

10) Having said that, India’s data has a non-trivial margin of error, and a new Census might change our reading of the situation. In summary, India is following the same path as everyone else. No Indian fertility Sonderweg!

That is all from Jesús Fernández-Villaverde.

Tajikistan fact of the day

Tajikistan’s remittances are worth nearly half the country’s GDP—

In Tajikistan, remittances — the money sent or brought back by migrants — amounted to 48% of GDP in 2024. The chart places this figure in context by comparing it with other countries with data for the same year. Nicaragua and Honduras receive remittances worth around a quarter of their GDP — high by global standards, but still far below Tajikistan’s level. Remittances here include two types of flows: money migrants abroad send home to their families, and money cross-border workers bring home from short-term jobs abroad.

Both of these flows play a role in Tajikistan, where most remittances come from labor migrants in Russia. In addition to the roughly 400,000 Tajiks settled there, hundreds of thousands more cross the border for seasonal and short-term work.

According to a report from the International Organization for Migration, about 1.2 million Tajiks were in Russia in mid-2024, which is more than a tenth of Tajikistan’s total population.

The World Bank’s latest Tajikistan Economic Update says that much of the country’s recent rapid economic growth (above 8% since 2021) was supported by these remittance inflows.

That is from Our World in Data, with a picture at the link.

Who is losing out in marriage market competition?

Over the past half-century, U.S. four-year colleges have shifted from enrolling mostly men to enrolling mostly women, while the economic position of non-college men has weakened markedly. We examine how these changes correspond with the evolving structure of marriage markets across cohorts and places. As college men have become increasingly scarce, college women have maintained stable marriage rates by marrying high-earning non-college men. This shift—combined with the broader economic decline of non-college men—has sharply reduced the pool of economically stable partners available to non-college women: the share of non-college men who earn above the national median and are not married to college women has fallen by more than 50%. Cross-area evidence shows that education gaps in marriage are smaller where non-college men face lower rates of joblessness and incarceration. Taken together, the evidence suggests that deteriorating outcomes for men have primarily undermined the marriage prospects of non-college women.

That is from a new NBER working paper by

Why I am skeptical on the relationship between smart phones and fertility

That is from Alex Nowrasteh. And for some country by country graphs:

Here is that link. There might be some connection to smart phones, but it just does not seem that strong? Perhaps the phones give a fillip and a modest acceleration to an already in place trend? And are Kenya’s phones really all that “smart,” even today?

Dwarkesh in the Datacenter

Dwarkesh tours one of Jane Street’s datacenters. It’s extraordinary how much compute goes into finance. (I once predicted that the finance AIs would be the first to become conscious, since they have the most compute.) More generally, however, this is a peek inside the remarkable economics, technology and physics of a datacenter. Did you know the electrical signal in a copper wire can travel faster than light in fiber…and that matters! Amazing.

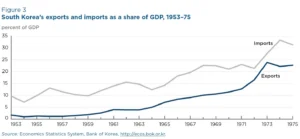

South Korea facts of the day

When I was young, the South Korean model was generally lumped in with places like Taiwan, Singapore and Hong Kong as a case of “export-led growth”. Even in the early 1970s, South Korea was still poorer than the North. There was no consensus that East Asia would do better than Latin America (or indeed that America would do better than the Soviet Union.)

I hate the term “export-led growth”, as on its face it would seem to imply that South Korea got rich by running trade surpluses. But exactly the opposite is true. During the three and a half decades of near double-digit growth (roughly 1963-97), Korea ran almost nonstop trade deficits, apart from a few years in the 1980s. This graph is from an excellent Doug Irwin paper that discusses the Korean reforms of 1964-65…

Here is more from Scott Sumner.

Revealing Life Preferences Through LLMs

Here is some Weberian verstehen (or is it?), but from unexpected quarters:

Large Language Models (LLMs) are trained on a prodigious corpus of human writing and may reveal human preferences over characteristics of life courses, such as income, longevity, and working conditions. We present OpenAI’s GPT-5.4 and a broadly representative sample of Americans with pairs of life stories and ask them to choose the life they would prefer for themselves. A person’s choice is better predicted by the LLM’s choice than by another person’s choice over the same stories, and LLM valuations of several life attributes are similar to those derived from human responses. Our results suggest that LLM responses offer a scalable and cost-effective complement to existing methods for studying human preferences.

That is from a new NBER working paper by

One way to benefit adolescents

Have school start later:

We examine the impact of California’s Senate Bill 328 (SB 328), the first statewide mandate requiring later school start times for middle and high schools, on adolescent sleep, mental health, and academic outcomes. Using difference-in-differences and eventstudy designs across five data sources, we find that SB 328 increased the share of students sleeping at least 8 hours per night by 13%, meeting the CDC-recommended minimum for this age group. Average mental health effects are imprecisely estimated, but boys show significant reductions in sadness, hopelessness, and suicidal ideation, and Hispanic students, who experienced the largest sleep-timing shifts, show parallel reductions in difficulty concentrating; together these patterns are consistent with a dose-response relationship between sleep improvement and mental well-being. Math and English scores in grade 8 improved by approximately 0.08–0.10 standard deviations, with the largest gains among Hispanic and economically disadvantaged students. A within-state analysis using teachers’ commute arrival times as a proxy for pre-policy school start times corroborates these findings, and shows academic gains accumulating over 2023–2025 alongside a suggestive decline in high school dropout rates. The absence of effects on chronic absenteeism rules out an attendance-driven mechanism, pointing instead to the direct cognitive benefits of aligning school schedules with adolescents’ biological rhythms.

That is from a new NBER working paper by

The Impact of AI-Generated Text on the Internet

The proliferation of AI-generated and AI-assisted text on the internet is feared to contribute to a degradation in semantic and stylistic diversity, factual accuracy, and other negative developments. We find that by mid-2025, roughly 35% of newly published websites were classified as AI-generated or AI-assisted, up from zero before ChatGPT’s launch in late 2022. We also find evidence suggesting that increases in AI-generated text on the internet bring about a decrease in semantic diversity and an increase in positive sentiment. We do not, however, find statistically significant evidence supporting the hypothesis that an increased rate of AI-generated text on the internet decreases factual accuracy or stylistic diversity. Notably, our findings diverge from public perception of AI’s impact on the internet.

That is from a new paper by Jonas Dolezal, Sawood Alam Mark Graham, and Maty Bohacek. Via Glenn Mercer.

Data centers are good

Data centers are the physical infrastructure behind cloud computing, artificial intelligence, and enterprise software. The rapid diffusion of artificial intelligence (AI) is intensifying demand for compute, accelerating investment in data centers, and raising concerns about the local economic and environmental footprint of these facilities. Their expansion creates a local policy tradeoff. A data center can bring capital investment, construction activity, and specialized employment, but it can also increase demand for electricity, land, and grid capacity. This paper studies these effects at the U.S. county level. We assemble a facility-level panel of global data centers with precise coordinates, scale metrics, and annualized revenue. We map facilities to U.S. counties and combine them with County Business Patterns, county-level IRS income, county-level house prices, and electricity prices. To address endogenous siting, we instrument for data center growth using two shift-share instruments, which leverage pre-existing proximity to InterTubes long-haul fiber nodes and the 1980 county share of U.S. urban college population as shares, and both Chinese and rest-of-the-world data center revenue growth as shifts. The IV estimates show positive effects on total employment, data-processing employment, construction employment, establishments, house prices, and electricity prices at different horizons after data center growth. We also find positive effects on tax returns, adjusted gross income, and wages, while annual payroll responds less robustly. The results suggest that data centers create measurable local activity, increase house prices, and affect local electricity markets through higher prices.

That is from a new NBER working paper by

Early evidence on school smartphone bans and mental health

The word “early” is appropriate here and is to be stressed, nonetheless I am not surprised by these results, given the relative impotence of treatment effects in so many settings:

To provide causal evidence of the effects of these bans, I rely on synthetic difference-in-difference models and the National Survey of Children’s Health (NSCH) from 2016 to 2024. Currently, there are data for only one state with two post-ban periods and two states with one post-ban period, which makes the results preliminary evidence only. The outcome variables are screentime and measures of psychological wellbeing. Overall, these early results provide no clear evidence that the school ban policy reduced screentime or improved psychological wellbeing.

That is from a recent NBER working paper by Henry Saffer.

Using agents to build economic datasets

Constructing datasets from primary sources is one of the costliest tasks in empirical economics. We propose Deep Research on a Loop (DRIL), a methodology that uses AI agents to assemble datasets from publicly available sources. DRIL applies a fixed research instrument across a mapped unit space (e.g., countries by years), with a two-stage architecture separating design from implementation. The instrument specifies variables and coding rules, an evidence policy governs sources and citations, and data quality mechanisms track gaps and uncertainty explicitly. We exercise DRIL on a 2025 update of the Global Tax Expenditures Database for eight Latin American and Caribbean countries. The run produces 129 sources and 136 evidence records, covering 22 qualitative fields fully and 6 quantitative estimate types with documented gaps, at the cost of a standard LLM subscription comparable to a few hours of research-assistant work. We argue that even partial automation of dataset construction can shift the production function of empirical economics.

That is from a new NBER working paper by

USA sectoral shift fact of the day

Healthcare and Social Assistance have added nearly 1.8 million private-sector jobs in the US since the end of 2023 while all of other industries combined have lost 127,800 jobs.

Here is the source (Charlie Bilello) and a graph. In relative terms, is this good or bad for men?

The social media ban in Australia, how is it going?

In December 2025, Australia became the first country to ban youth under 16 years old from holding accounts on major social media platforms, a policy now under consideration in more than a dozen countries and in numerous states. Because social media use is inherently social, the effectiveness of a ban that is easy to circumvent may depend on whether compliance reaches a tipping point: a share of compliant peers high enough to make it optimal for individuals to comply themselves. We surveyed 835 Australian teenagers four months after the ban took effect and find that only about one in four 14–15-year-olds comply. The social environment around use has barely moved: most banned teens believe that their peers are still using banned platforms and cite social reasons for continuing use. Sustaining high compliance requires two ingredients: the share of compliers must be high enough and those who comply must find it preferable to continue complying. The current ban achieves neither. Teenagers report that they require roughly two-thirds of peers to stop using social media to stop themselves, far above the share currently complying. They also perceive compliers as less popular than non-compliers, so the more influential teens disproportionately stay on the platforms. Together, these patterns suggest that compliance is more likely to diminish than to rise. Sustaining higher compliance will likely require pairing the ban with instruments that act on social norms and individual incentives directly.

That is from a new NBER working paper by

A few days ago I was talking with a very smart fifteen year old in Australia (really). He was of the opinion that it was quite ineffective, though he noted he could no longer access LinkedIn. I would note there are more stringent measures, requiring more governmental monitoring and control of the internet, that perhaps could have a greater effect.