Category: Economics

Rent Control: The Ceiling Trap

Rent control is in the news again. Check out my new website, Rent Control: The Ceiling Trap. Here is just one bit:

Norway abolished its rent control in 1982, and the economist Are Oust realized the newspapers had been quietly recording the whole experiment. He collected housing classifieds from Oslo’s Aftenposten from 1970 to 2008 and watched the market turn inside out.

Under rent control, Oslo’s listings pages looked nothing like a housing market. It was tenants who advertised, pleading their qualities to landlords — “housing wanted” ads outnumbered “housing for rent.” Ten to fifteen percent of those ads were placed by the tenant’s employer, vouching for them the way a bank vouches for a borrower. Tenants offered babysitting, gardening, snow-shoveling, and janitorial work on the side to sweeten the deal. Landlords, for their part, could demand a tenant of a particular gender, age, occupation, region of origin — some ads specified “strong Christian beliefs.” Deposits commonly ran to 50 or 60 months’ rent, occasionally 100 or more: tenants effectively lent the landlord the equity of the flat, interest free. And only about 20 percent of “for rent” ads dared print the rent, much of which would have been illegal.

Then the ceiling lifted. Within a few years the page flipped: landlords advertised to tenants, roughly 80 percent of listings printed an asking rent, the mega-deposits vanished, and the demands for snow-shoveling Christians of specified gender dwindled to nothing. The price went back to doing the rationing — so nothing else had to.

Check out the whole thing–it’s fabulous.

What should I ask Daron Acemoglu?

Yes, I will be doing a Conversation with him. Obviously Acemoglu has published plenty, but likely this chat will focus on his recent writings and pronouncements on AI, and most of all his forthcoming book What Happened to Liberal Democracy? Remaking a Politics of Shared Prosperity. So what should I ask him?

Politically Incorrect Paper of the Day: The US Racial Wealth Gap

Writing in the QJE, Derenoncourt, Kim, Kuhn, & Schularick argue that today’s black-white wealth gap can be explained by differences in initial conditions from over a hundred and fifty years ago, i.e. slavery. But there is an important, and glaring objection: in the age of immigration (1850–1924) millions of whites immigrated to the United States with essentially no wealth and yet they caught up to the “heritage” whites quite quickly and indeed today are richer than heritage whites.

Brian Marein collects and carefully analyzes the data:

Persistent racial wealth inequality in the United States is often attributed to the intergenerational transmission of historical wealth disparities. However, inferring the determinants of long-run inequality from group-level data is complicated by the arrival of 30 million Europeans during the Age of Mass Migration (1850–1924), who are by construction included in average white wealth despite having no direct claim to the wealth accumulated by earlier Americans. This paper accounts for this compositional change in the white population by documenting wealth dynamics among European immigrants and their descendants. Cash-on-arrival data show that immigrants began with substantial wealth deficits relative to the native-born. Yet by the late twentieth century, these deficits had closed, as indicated by comparisons between the descendants of later-arriving Southern and Eastern Europeans and those of longer-established Northwestern Europeans. This pattern implies rapid intraracial wealth convergence, in contrast to the slower convergence observed across racial groups. A stylized model shows that these differences can be largely accounted for by income. These findings demonstrate that large wealth disparities do not mechanically persist when groups have access to comparable economic opportunities.

If initial conditions don’t explain the wealth gap then the most likely explanation is an income and/or savings gaps. I am reminded of an earlier politically incorrect paper of the year by Nathaniel Hilger and see also my review of his book The Parent Trap.

Will future biomedical advances be low marginal cost?

Most pharmaceuticals involve high upfront costs, to discover and test the drug, and very low marginal costs. Another pill can be printed almost for free.

That cost structure favors health systems, such as that of Britain, that try to pay lower for services. They can end up getting a relatively good deal from price discrimination. After all, they can be served at low marginal cost, at least for those ttreatments.

Now imagine a biomedical future where many more treatments are based on the sequencing of your individual genome, and then the development of specific treatments personalized to you. Obviously it will depend on developments, but very likely those remedies will have relatively high marginal costs.

In that setting the British approach to health care procurement and pricing will work less well. It is the well-capitalized, “overspending” systems, such as the United States, that will have an easier time making the adjustment.

“The rising relative advantage of well-capitalized health care systems” is a neglected trend, because it makes a lot of earlier elite pronouncements about health care economics look a bit off.

My ARC talk on AI and jobs

Twelve minutes long:

“One stop shopping” for why AI will not put everyone out of work.

Azeem Azhar (and others) on the state of the AI economy

Due to travel I have not had time to read this detailed report, but it is getting very good reviews

Works in Progress: Grid Connection Auctions

The latest issue of Works in Progress is superb. Every article is interesting.

Chris Gillett points out something surprising: the US has plenty of electricity generation capacity ready to go, the problem is connecting it to the grid. Grid connection is complicated because on the grid, supply must equal demand at every moment in time. Even without speeding the process, however, we could get more power connected to the grid if we rationalized the ordering of connections.

The main flaw of the interconnection process is that it uses a first-come, first-served queue. This means that high-priority requests can spend years stuck at the back of the line behind other less important ones.

In essence, we have an airport congestion problem in which small Cessnas can bump 747s. Auctions for connection rights are the solution, as pointed out for airports by Vickrey and the classic paper by Rassenti, Smith and Bulfin. Gillett also emphasizes that some loads should be allowed to connect on a flexible basis: if a data center can disconnect or use backup power during the few peak hours each year, it should not have to wait years for firm service.

Gillett also has a very nice explanation of how market prices balance electricity from different sources:

Market prices signal to power plant developers about levels of supply and demand. In the same way, prices balance different energy sources based on the strengths and weaknesses of each. For instance, as more solar panels are built, the value (and therefore price) of power during the middle of the day, when the sun is shining most, adjusts downward. From December 2020 to September 2025, maximum solar output in ERCOT increased from 4 to 29.8 gigawatts. And from 2020 to 2025, the value of power at 1pm relative to the highest-priced hour decreased from 92.9 percent to 38.7 percent. As one technology type becomes overbuilt, prices reflect that and developers react accordingly.

The evolving daily price shape in response to the abundance of solar energy was a signal that the grid needed storage capacity, and power plant developers responded. From 2020 to October 2025, ERCOT went from having almost no battery storage to a combined battery discharge of 8.6 gigawatts. The same process has played out in California and many European markets.

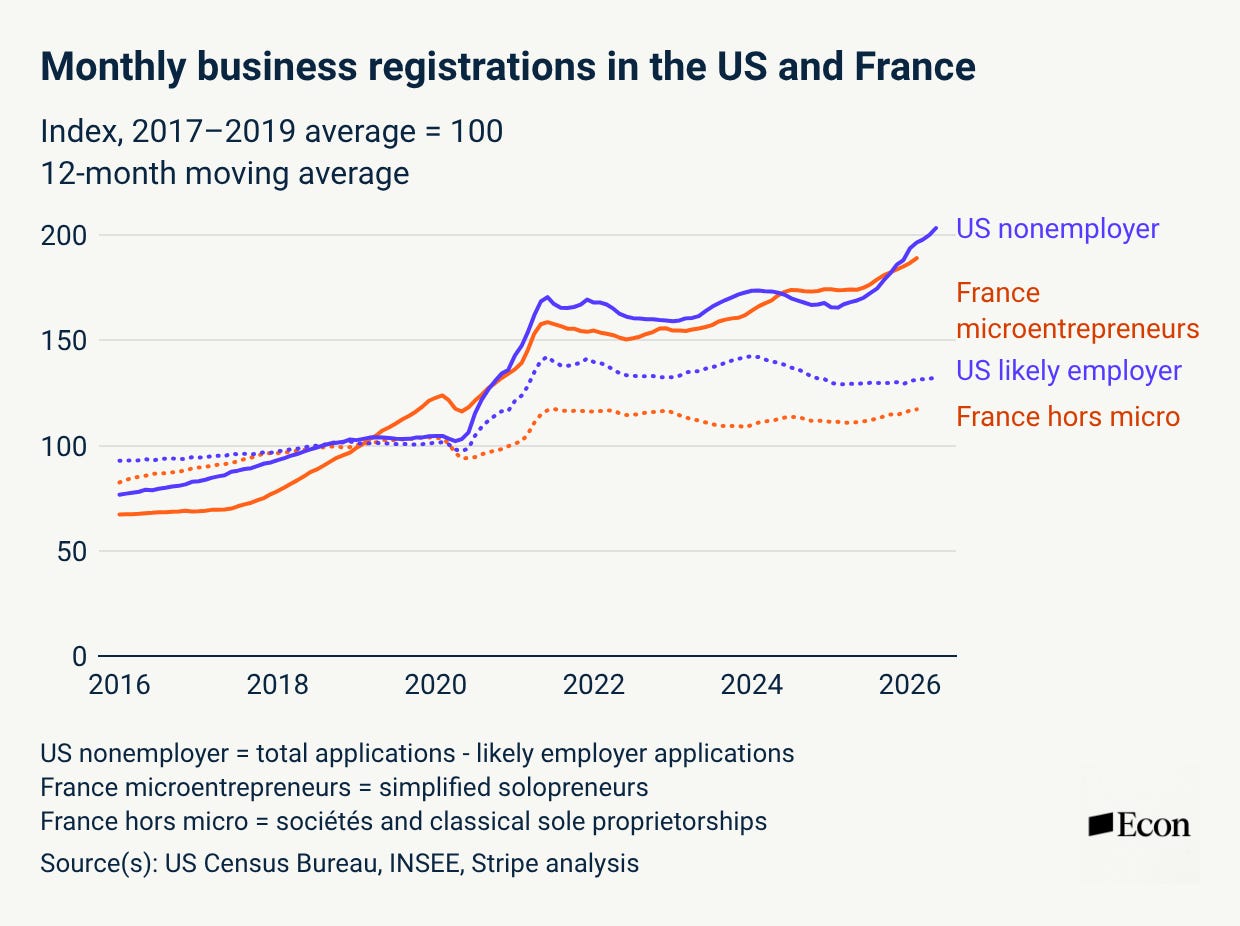

New Business Formation is Surging–Again.

New business formation is surging–again.

Business formation first jumped in 2020 as the pandemic reorganized work, shopping and logistics. After the pandemic ended, business formation leveled off, but it did not return to its old path. It remained historically high. Moreover, in the past 18 months or so business formation has surged again. Registered Agents Inc tracks new Articles of Organization or Incorporation filed in the 50 states and they report:

Every month in 2026 has set a new formation record, including March, which stands as the highest single-month total in the history of the Business Formation Report. Through May, 2.9 million new businesses have been formed nationwide, the strongest five-month start on record.

Stripe Economics agrees and calls this the age of the solopreneur. Among businesses using Stripe, recent cohorts are reaching serious transaction volumes faster than earlier cohorts.

The share of businesses (not just solopreneurs) reaching $1 million in cumulative revenue within a year after going live on Stripe was roughly 30% higher for the 2025 cohort as it was for the 2023 cohort, and it was roughly 3x higher for the 2025 cohort than the 2019 cohort.

Furthermore, the trend is not just in the United States. France, where, as the story goes, they have no word for entrepreneur, has also seen business creation reach record levels, driven heavily by micro-entrepreneurs.

The most likely explanation is the devolution of power. A single person armed with Stripe, Shopify, cloud software, automated bookkeeping, and now AI can do what once required a small staff. Dynamism had been on a long secular decline, but we may now be seeing the early stages of an experimental economy—one in which far more people can test ideas, reach customers, and launch firms, some of which will grow very large, very fast.

I am told James Mill is buried there also

Translated from the Chinese

I think this is the Cursor moment for academia.

The Stanford REAP team has made their move, CoPaper.AI is mass-terminating the manual labor of traditional empirical papers. Link: copaper.ai/landing

If using large models to write papers before was just about polishing and compiling references for you, then this Project from Professor Ross Griebenow’s team at Stanford is like dropping a nuclear bomb in the empirical circles of social sciences and economics.

The greatest truth is the simplest; the heaviest sword has no edge. Its functions are straightforward. Feed in the raw dataset, and within 30 minutes, it can generate a complete DOCX paper complete with full Stata/R code and publication-quality charts.

It chains together EDA, variable definition, econometric model building (from OLS to advanced DID, regression discontinuity, causal forests) all using an Agent workflow.

Every chart it produces comes with 100% reproducible Stata, R, EViews source code underneath. How many low-quality paper mills and data drones’ jobs will this smash?

Data drones and paper ghostwriters are collectively facing unemployment countdown. Because from now on, for social science papers, AI handles all the entropy-increasing drudgery—humans only need to define the problem.

Here is the link. Mostly that is not true, so perhaps the Chinese are trying to demoralize us. But will it never ever be true? In two years be true? Less?

Two Roads to Fast Clinical Trials, and the US Takes Neither

The HHS (FDA, NIH, ARPA-H and related agencies) is moving to speed clinical trials in what they are calling Operation TrialBlazer (kudos on the pun). The motivator, of course, is China:

China has made biotechnology a strategic national priority, systematically expanding its clinical research infrastructure with government backing, streamlined regulatory pathways, and sustained investment. In 2021, China’s global share of Phase 1 trials surpassed the United States’ share for the first time, a milestone that would have seemed unlikely just a decade earlier. And in 2024, China surpassed the United States in the total number of clinical trials registered, with over 7,100 registered, representing 39% of global trials…. For certain cutting edge modalities, including cell and gene therapy, radioligand therapy, and stem cell therapy, China uses investigator-initiated trials to provide additional flexibility, though with some tradeoffs around oversight and quality control. This means that drugs can move into human testing if a researcher has an interest and funding. In the U.S., comparable trials might wait years to start.

I am also pleased to see that they mention Australia, another advanced democracy, as a leader in clinical trial regulation:

Australia’s Clinical Trial Notification System allows trials to begin in fewer than 70 days after a final protocol is submitted, with regulatory approval granted in as little as 21 to 28 days and sites activated within 6 to 12 weeks.

Keep those comparisons in mind. Operation TrialBlazer proposes some good reforms such as CMC clarification. CMC is Chemistry, Manufacturing, and Controls–and it deals with the basics of manufacturing a drug. The FDA, however, is very risk averse and companies know that so they have often gone overboard in CMC: for example, proving stability of a formula at 6+ months when the trial is to last only a few weeks or documenting their full commercial manufacturing process before they even know if the drug works and knowing full-well that the process will be changed many times before a drug actually gets to market. In short, a lot of cost for very little benefit. The FDA is now clarifying that this kind of thing is not necessary. Good, that is low-hanging fruit. There are other good ideas as well.

But note what they are not proposing. Despite using China and Australia as exemplars they are not going down either path. Where China is fastest is in cell therapy, gene therapy, radioligand, and stem cell work and in these areas, China lets trials proceed on an investigator-initiated basis: as the TrialBlazer document puts it, a drug can move into humans “if a researcher has an interest and funding.” China then combines this open (or lax) front end (for these products) with an all-of-government industrial policy to accelerate winners.

The US is declining to go down that path. Ok, not my call, but I get it. But they are also declining to follow Australia. In Australia there is also no government prospective regulatory evaluation of most early-phase clinical trials. Under the Clinical Trial Notification (CTN) scheme, the sponsor submits their protocol package to a Human Research Ethics Committee (HRECs)–Australia’s IRBs–and once the ethics committee approves, the sponsor notifies the regulator, the Therapeutic Goods Administration (TGA), and pays a fee. The TGA does not read and clear the package before the trial starts. The roughly 21-to-28-day “approval” and sub-70-day start figures in the document are fast precisely because the regulatory step is not an evaluation. The government regulator stays out of the front end for most clinical trials, although in direct contrast with China it does step in for the highest risk biologicals. China has decided, high-risk, high-reward.

Australia does certify the certifiers, the HRECs. Europe uses a similar system for medical device approval. It’s a system proposed by former medical officer at the FDA Henry Miller and one I have long supported for the US. China is more laissez-faire.

The US architecture in contrast rests on the “gold standard” FDA reviews and the “FDA will retain full regulatory authority and decision-making.” In short, all of the TrialBlazer reforms are about making the gatekeeper faster, cheaper to prepare for, and less uncertain. None of it is about getting rid of the gatekeeper.

Addendum: Full disclosure, I did some consulting with ARPA-H on related work. See also my previous post on the a radical deregulatory approach, Montana’s SB535 and a Potential Biotech Renaissance in America

Elderly Health and Longevity in the US

Rising elderly life expectancy is a well-known source of fiscal pressure on Social Security and Medicare – but how have declining mortality and morbidity affected the two programs’ relative finances? Using nearly three decades of Medicare Current Beneficiary Survey data (1992-2019), we estimate that these demographic changes raised expected lifetime Social Security spending by over twice as much as expected lifetime Medicare spending: 14% compared to 6%. The slower growth of elderly lifetime health care spending than annuity spending reflects two features of how longevity has increased: the additional 2.4 years of remaining life expectancy were entirely healthy – free of physical or cognitive limitations – while the expected amount of time spent with severe health limitations fell by about 30%, reducing expected lifetime nursing-home and home-health use. We then write down a stylized life-cycle model of a risk-averse retiree facing stochastic mortality and health to illuminate the key forces that affect the optimal allocation of a fixed amount of public funds across Medicare and Social Security.

That is from a new NBER working paper by Liran Einav and Amy Finkelstein. In general I wish to switch resources from Medicare to Social Security, or at least give individuals the option to do so. You can use dollars to buy health care, but it is not always so easy to make the transformation in the opposite direction.

Alan Greenspan, RIP at 100

Here is a NYT obituary. Here is a WSJ obituary.

California’s Gay Certification Program

Chris Rufo and Austen Hufford have a good piece on California’s Gay Certification program. Yes, you read that right.

In 1986, Governor George Deukmejian signed Assembly Bill 3678, which required certain CPUC-regulated utilities to submit annual “plans” for buying goods and services from woman- and minority-owned companies. Two years later, CPUC created its “Supplier Diversity Program,” which would enforce the law and set contracting “goals” for large utilities.

Under a series of Democratic governors, the program has expanded to include gay-owned businesses. In September 2014, then-Governor Jerry Brown signed legislation requiring CPUC to recognize “LGBT-owned businesses” as eligible for supplier-diversity benefits. Five years later, Governor Gavin Newsom expanded the program further, “encouraging” other companies involved in the energy sector to award contracts to gay-owned firms.

…This scheme raises an obvious question: How does a business qualify as officially gay? Paperwork. Supplier Clearinghouse, a group that certifies firms for the CPUC program, features a list of qualifications linked on its website. Applicants can secure certification by providing a letter from an “LGBT organization” attesting to their sexual preferences; proof that a newspaper identified them as “LGBT”; or three letters from “personal contacts” written “on company letterhead” attesting to their homosexual orientation. Corporate officials who “falsely represent” their business as gay face up to a year in county jail.

So there you have it. Under the logic of ever increasing privileges for pretty much anyone except white males we now certify whether someone is gay or not.

This is an economics blog, however, so let’s turn from the culture war and ask, following Luke Froeb at Managerial Economics, what these set-asides cost the taxpayer:

A set-aside moves price through two separate channels, and they push the same direction.

- First, it shrinks the number of bidders, so the second-lowest cost is higher (or the second-highest value is lower).

- Second, the set-aside bidders themselves may be higher-cost or lower-value than the bidders they replace.

Both channels move price against the government….The lesson applies to California. Fewer, weaker bidders mean a worse deal for the government.

Brannman and Froeb estimate that set asides for small businesses reduce revenues in timber auctions by 15%, a substantial amount.

Addendum: It is worth noting that optimal auction theory tells us that it can sometimes be in the seller’s interest to handicap a strong bidder in order to make them increase their bids. Thus, in theory, an “affirmative action” program (not a set-aside) that deemed a bid from a minority firm as say 5% higher (so a minority bid at 100 can beat a non-minority bid at 104) could raise revenues. Note, however, that this optimal auction story only works when the minority firm loses the bid! In practice, even these sorts of schemes are money losers for the taxpayer.

Bastiat’s telephone?

- Oakland has seen a 37% decrease in car break-ins over the last year.

- What’s good news for car owners is less so for repair shops that specialize in window and windshield replacements.

- Multiple businesses have reported a sharp decline in their income as a result.

Here is the article, via Air Genius Gary Leff.