Category: Economics

How Much Has Shale Gas Saved U.S. Consumers?

It may seem like a distant memory now, but as of the mid-2000s, U.S. natural gas production had been flat for a decade, and the U.S. was importing liquefied natural gas (LNG), with plans to import much more. Then shale gas happened. Advances in hydraulic fracturing and horizontal drilling caused U.S. natural gas production to increase significantly, and the U.S. went from being a net importer of natural gas to being the world’s largest exporter. This paper calculates how much shale gas has saved U.S. natural gas consumers. Using price differences between the United States, Europe and Japan, we calculate that U.S. natural gas consumers have saved $3.1-$4.3 trillion between 2007 and 2025, equivalent to $164-$227 billion annually. Access to low-price U.S. natural gas has been particularly valuable during major supply shocks such as the war in Ukraine, and the benefits of shale gas have been experienced broadly across sectors and states.

That is from a new NBER working paper by Lucas W. Davis.

AI in gdp

- Quality-adjusted AI production in the United States grew at over 2,000 percent per year in 2024 and 2025, driven by three compounding forces: expanding data-center capacity, hardware efficiency gains, and—the largest of the three—algorithmic progress.

- Treating the AI sector as a coherent economic entity yields preliminary estimates of nominal AI GDP at approximately $250 billion in 2025, growing at roughly 2,600 percent per year in quality-adjusted real terms.

- National economic statistics accounts were not designed to track this kind of activity. Statistics agencies should begin developing AI-focused satellite accounts now, before the measurement gap becomes a policy gap.

Here is much more from Anton Korinek and Patrick McKelvey. Via the excellent Samir Varma.

Seven ways to avoid losing your job to AI

That is the theme of my latest Free Press column, here is one excerpt:

Principle five: Run experiments.

This is a more general version of the healthcare point. AI will generate so many new ideas and hypotheses, including for drugs and medical devices, but not only. Become a tester. Test new battery designs, new educational techniques, or new methods of conserving valued wildlife.

The demand for experiments will rise sharply, and most of those cannot be done by robots, at least not anytime soon.

Principle six: Gather data.

AI is a marvelous tool, but it relies on knowing lots about the world. That can stem from reading the internet, watching videos of people folding clothes, and hearing recordings of voices, among many other ways of absorbing information.

The more powerful the AI, the higher the returns from feeding it data, because it will make smart and useful inferences from those data. But most data in our world have never been put into AI models. Just consider corporate records, historical archives, referee reports for failed scientific papers, accounts of lab procedures, and much more. Most of that remains virgin territory.

The next few decades will bring an immense investment in feeding more data into the AIs. So there will be new jobs in gathering environmental data, job safety data, construction site data, corporate and management data, public health data, agricultural data, education data, and much more. Those jobs could be yours.

Recommended.

A Beautiful Theory Falls to Ugly Data

My latest paper, A Test of the Coase Conjecture Using Prices of Electronic Books, with the excellent Tim Groseclose, has just been published. The Coase Conjecture is another one of Coase’s little ideas — the original paper is six pages — that has spawned hundreds of follow-up papers and thousands of citations.

The idea is simple. A monopolist of a durable good has a time-inconsistency problem. Set the monopoly price in period 1 and he will be tempted in period 2 to cut the price and mop up the customers whose valuations sit between the period-1 price and MC. But the same logic applies in period 2, and again in period 3, and so on — eventually the price unravels to MC. Consumers see this coming, the monopolist knows the consumers see it coming, and so the monopolist cuts price to MC in period 1. And since a “period” is just the interval between price changes, the whole unraveling happens — in Coase’s phrase — “in the twinkling of an eye.”

The theorists, most notably Gul, Sonnenschein and Wilson and Fudenberg, Levine and Tirole, formalized Coase’s insight and showed that under quite general conditions the logic goes through. Which is rather surprising, since, as Tim and I point out, Coase’s conjecture implies that many patents and copyrights are essentially worthless — a prediction wildly at variance with the facts. Other theorists, including Stokey, Ausubel and Deneckere, and Board and Pycia, have offered variants under which the Coase outcome does and does not obtain.

For all this theory, there have been almost no direct tests of the Coase Conjecture apart from a handful of lab experiments. Ours is one of the first papers to take the conjecture to the real world. We look at e-books, an unusually clean setting: digital goods are durable, marginal costs are low, resale is limited, and prices can be changed quickly. Using the prices of e-books that are in the public domain as a proxy for marginal cost, we ask: (a) do prices rapidly fall to MC, and (b) does the market clear in the first period? The answer to both is no. E-book prices begin well above MC, sales continue over many periods, and prices don’t even decline monotonically.

We reject the Coase Conjecture decisively.

The paper has an interesting history. The theorists (or the referees we guessed were theorists) praised the paper for taking the theory seriously but inevitably had a fillip to offer, distinguishing the world of pure theory from empirical tests. The empiricists, on the other hand, said our tests were too simple since no one takes the theory that seriously. It’s good to see the paper find a home!

We reject the Coase Conjecture decisively, but it remains to say why. We can rule out some explanations — it’s not rising MC, and it’s not the finiteness of buyers (which can support a perfectly price-discriminating Pac-Man equilibrium).

Two theories remain: 1) sellers can commit not to lower prices, and 2) the outside-options model of Board and Pycia. I prefer the former, my co-author prefers the latter. To me, commitment just isn’t that hard. The standard story is that profits are like cookies on the table and the monopolist can’t resist — but at least the people tempted by cookies get to eat the cookies! The Coase profits are illusory: the monopolist races to MC in period 1 precisely because they know they won’t resist later and as a result they don’t even get a taste of profit! Too clever by half. I say, show some backbone. Firms are *all about* commitment — to workers, consumers, contractors. Why not to a price? My co-author points out, however, that this is more Tabarrok-vibe than carefully laid out theory.

Tim likes the Board and Pycia model which begins with the plausible idea that consumers have outside options — if they don’t buy the book today, they will buy another book, rent the movie, or borrow from the library — and crucially, once they take the outside option, the consumer never returns to the market. You might think outside options would make it *harder* for the firm to set a high price, but Board and Pycia show in a very clever but extended argument that when you carefully work out the full equilibrium the opposite holds: outside options give firms a time-consistent incentive to set and keep a high price. Tim explains the argument further here (see also our paper for an intuitive breakdown).

In any case, the Coase Conjecture — at least as modelled by the theorists — fails in an environment most conducive to it.

A beautiful theory falls to ugly data.

The corporate tax rate really matters

Three findings emerge. First, improvements in aggregate tax competitiveness are positively and significantly associated with real GDP per capita growth, robust to a wide range of controls. Second, this aggregate effect is driven entirely by the corporate tax pillar; no other component displays a significant growth effect. Third, the corporate tax effect materializes contemporaneously and accumulates over time, with a statistically significant three-year cumulative effect of approximately 0.16 percentage points per one-point improvement in the corporate tax score. These results suggest that the full architecture of the corporate tax system, not merely the headline statutory rate, is what matters for growth.

That is from a recent paper by Michael Christla and Monika Köppl–Turyna. Via the excellent Samir Varma.

The carousel trade (arbitrage)

Imagine two companies which are secretly controlled by the same people. If company A imported some phones, then sold them to company B, it charged VAT on the deal. If company B then exported the phones, it reclaimed — from the government — the VAT it had paid to company A. the integrity of the VAT system depends on the two totals balancing out. The money that A pays in is equl to the money that B takes back. The scam lay in A disappearing and not handing over the money it owed, but B till claiming it. The hidden owners of the two firms therefore earned for themselves 17.5 per cent (the rate at which VAT was then charged) of the value of the shipment of the phones. The more phones you sold to yourself, the more money you made.

That is John Lanchester in the LRB, citing Oliver Bullough’s Everybody Loves Our Dollars: How Money Laundering Won.

Liberal Economists Score an Own Goal Against Bezos

Jeff Bezos tweeted:

Yes, the United States has the most progressive tax system in the world. The top 1% pay 40% of taxes, the bottom 50% pay 3% of taxes. We can make it even more progressive by zeroing out taxes on the bottom half. It’s a small amount of the total tax revenue but very meaningful to people in this group.

Strangely, a chorus of liberal economists rushed to attack Bezos. Gabriel Zucman replied:

Contrary to what you claim, working-class people contribute significantly to funding American society today. Payroll taxes and consumption taxes absorb a high fraction of their income.

Justin Wolfers piled on:

If you only count the progressive taxes the U.S. levies, then the U.S. system is quite progressive. But if you also count regressive taxes (payroll taxes, sales taxes, etc), it’s not very progressive.

Bezos called for cutting taxes on the bottom half to make the tax system more progressive and the redistributionists came out swinging–to argue he was wrong about how progressive the current system already is. Own goal. Heretics are worse than unbelievers.

But there’s a second, more interesting thing going on. To make the regressivity case, Zucman and Wolfers have to count payroll payments as taxes. That cuts directly against eighty years of liberal doctrine. Beginning with FDR, the argument on the liberal side has always been that payroll taxes are not taxes but contributions or premiums entitling the payer to benefits as an “earned right.” Here’s FDR to Luther Gulick in 1941:

We put those payroll contributions there so as to give the contributors a legal, moral, and political right to collect their pensions and their unemployment benefits. With those taxes in there, no damn politician can ever scrap my social security program.

That framing isn’t a historical curiosity. It runs straight through liberal social security stalwarts like Arthur Altmeyer, Wilbur Cohen, and Robert Ball, and it’s alive today in Nancy Altman and Eric Kingson’s Social Security Works!, which attacks billionaires and insists Social Security benefits are “earned compensation.” The whole political durability of the program–the third rail–rests on this framing.

So the modern left wants it both ways. When the question is whether to cut Social Security, FICA is a premium and benefits are earned compensation. When the question is whether the tax system is progressive, FICA is suddenly a regressive tax. Pick a lane.

Is there a principled way to resolve this? Yes, and it follows Jim Buchanan (see my earlier post here) and Larry Summers who laid out the economics in his classic paper Some Simple Economics of Mandated Benefits. The principled test is whether a payment reduces labor supply. The wedge between marginal product and the worker’s reservation wage isn’t the statutory rate–it’s the gap between the mandated payment and the worker’s marginal benefit. Sylvain Catherine made exactly this point in reply to Wolfers:

Payroll taxes are not regressive! They are mandatory contributions to a retirement system that offers higher rates of returns at the bottom than at the top.

Consider a forced savings program: everyone must pay 12.4% of income into a 401(k). Is this a tax? For someone who was going to save 15% anyway, not at all. For someone who was going to save 10%, only the extra 2.4% bites. Mandatory does not mean tax. The marginal valuation of the mandated benefit is the key.

Now apply this to the two payroll taxes.

Medicare (HI): Every marginal dollar buys zero marginal benefit. Thus, it’s a tax. Part A eligibility is binary–40 quarters gets you in–and once in, your benefit is whatever Medicare spends on your care. No relationship on the margin. (Moreover, the raw HI schedule is unambiguously progressive: 2.9% flat, rising to 3.8% above $200K/$250K thresholds, plus the NIIT.)

Social Security (OASDI): The 90/32/15 Primary Insurance Amount bend points mean a low earner gets a much better return than a high earner. So the gross statutory rate is flat-then-regressive; but the net rate is progressive. In short, OASDI isn’t a tax for low earners but it is a tax for higher earners, thus the tax is progressive.

So: HI is a progressive tax. OASDI is a contribution at the bottom and a tax at the top. Either way, the Zucman-Wolfers framing—payroll payments as straightforward regressive taxes—is wrong and rhetorically it abandons the framing the left has spent eighty years building to protect these programs.

Personally, I’d prefer a system truer to the old rhetoric–a forced savings program with a closer connection between marginal payments and benefits. But if the left wants to reframe Social Security contributions as taxes, and thus make Social Security all about redistribution to the poor, rather than a wise savings program, roll the dice. Just remember that Altmeyer, Cohen, and Ball spent decades building the “earned right” framing precisely because they understood it was the program’s structural defense against means-testing and privatization. Drop the framing and you drop the defense. I suspect the privatizers at AEI and Cato will happily take that trade but the left may come to regret making it for them.

The economics of unions

My best read of the evidence is that a union raises wages by around 7% for currently unionized employees. The wage gains from a redistribution of rents evenly across workers. Wage compression exists, but redistribution from worker to worker is only a small part. These are the current effects – unionizing more of the economy will have declining marginal returns, and will likely turn negative quickly.

I do not believe that unionization is efficient. While precise figures are lacking, it is unlikely to be a better method of supporting the poor or working class, both because union workers are not disproportionately poor, and also because their methods of extracting surplus are not restricted to just wages. I will note that the best paper on the effects of unions of productivity finds a positive partial equilibrium effect, but that is only for some markets, does not benefit the consumer, and the aggregate effects are likely negative.

Here is much more from Nicholas Decker. It would be a much simpler — and better — world if everyone understood this. This issue, above many others, is a good test for whether someone is willing to think more analytically and confront the issue of economics vs. mood affiliation. Because pro-trade union sentiment has literally centuries of mood affiliation behind it.

Repugnant Economics

I spoke on a panel at AEI with Nobelist Al Roth about his new book, Moral Economics, which covers “repugnant markets,” from prostitution to surrogacy to kidney exchange. A fun book!

My case study was acting. Acting was considered repugnant for over 2,000 years. In Rome, actors could not vote, hold office, or be trusted to give an oath in legal proceedings. So why don’t we find acting repugnant today?

One lesson: weighing costs and benefits is not enough. Roth discusses empirical research showing that legalizing prostitution cut STDs and sexual assaults—against prostitutes and others. But evidence alone won’t shift a repugnance norm. You also have to reframe the activity. Acting, for example was reframed from body rental to a skill requiring intelligence, training and ability. So I went out of my way to say that I am a fan of Aella—though not her only fan—and that I see no reason why escorting should not be considered a skill, requiring intelligence, training, and ability. I can think of few better ways of raising social welfare than making sex 10% better!

I also spoke on human challenge trials. Roth and I agree: challenge trials could have sped up COVID vaccines and saved tens of thousands of lives. We should be angry this didn’t happen. Why didn’t it? Even though most people think human challenge trials are a good idea, there was a repugnance bottleneck because the minority who did find human challenge trials repugnant were in charge. I discuss how to change this.

Al leads the discussion. My comments start at 25:15.

What else is special about southeastern Michigan? (from my email)

Thanks for swinging by Southeastern Michigan. He are two things other things that this area continues to produce and export at scale that don’t get as much notice:

* Mortgages – The two largest residential mortgage lenders are located in Detroit: United Wholesale Mortgage ($164B of mortgage originations for 2025) and Rocket Mortgages ($113B). It’s a fragmented industry, but to give you a sense of their comparative scale, Chase is #3 lender @ $66B in originations. Detroit continues to be the home of financial services for many Americans’ largest purchase.

* Food – Michigan, not NY or Italy, is responsible for the scaling of pizza. Domino’s, Little Caesar’s, and Jet’s were all founded in Southeastern Michigan. Domino’s is the largest pizza company in the world, and in many global markets, Domino’s defines “pizza.” For instance, Domino’s market share of pizza in the UK is over 50%. So, the UK has adopted Michigan’s, not Italy’s, understanding of pizza.

One narrative for Michigan should be that it has continued to shape global culture, through scaled production of mortgages and pizza. It doesn’t get more American than cars + mortgages + pizza, does it?

That is from Jeff Withington.

Dwarkesh in the Datacenter

Dwarkesh tours one of Jane Street’s datacenters. It’s extraordinary how much compute goes into finance. (I once predicted that the finance AIs would be the first to become conscious, since they have the most compute.) More generally, however, this is a peek inside the remarkable economics, technology and physics of a datacenter. Did you know the electrical signal in a copper wire can travel faster than light in fiber…and that matters! Amazing.

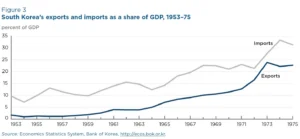

South Korea facts of the day

When I was young, the South Korean model was generally lumped in with places like Taiwan, Singapore and Hong Kong as a case of “export-led growth”. Even in the early 1970s, South Korea was still poorer than the North. There was no consensus that East Asia would do better than Latin America (or indeed that America would do better than the Soviet Union.)

I hate the term “export-led growth”, as on its face it would seem to imply that South Korea got rich by running trade surpluses. But exactly the opposite is true. During the three and a half decades of near double-digit growth (roughly 1963-97), Korea ran almost nonstop trade deficits, apart from a few years in the 1980s. This graph is from an excellent Doug Irwin paper that discusses the Korean reforms of 1964-65…

Here is more from Scott Sumner.

Ned Phelps, RIP

Here is a brief appreciation from Olivier Blanchard, link now corrected.

Hayek in Jacobin

Here’s something I never expected to write: Jacobin, the magazine of the DSA-aligned left, has a good article on central planning. In an interview, Vivek Chibber lays out essentially the Mises–Hayek–Kornai critique of central planning. Information problems, incentive problems and the consequent failures are laid bare. Moreover, Chibber refuses to lay the blame at the feet of Stalin, poverty, or the Russians. Nor does he wave hopefully at supercomputers and AI, as is fashionable today on the planning-curious left:

The dilemma is this. There is a problem of information. Supercomputers will in fact help process information better. But if the information coming in is junk, and if that junk is built into the system because of the incentives that operators have in workplaces to lie, you will not have a planning system that can be put on its feet through the advent of computers or artificial intelligence or anything like that. I don’t see any reason to think that that strategic misalignment of incentives is simply there because of Russian backwardness or poverty.

Even the pedestrian is shocking coming from Jacobin:

Normally in capitalism, what do managers do? They want to make profits. The way to make a profit is by trying to sell, at the lowest price possible, the best-quality good that you can.

A vivid conclusion:

Melissa Naschek: What do you think leftists should learn from the failure of fully planned economies?

Vivek Chibber: What they should learn is that the burden of proof is on us, on the Left, if we want to continue with this slogan of replacing the market with the plan. The burden of proof is on us to show that it can work. You might say that along with this ought to come a kind of humility about facts and about the world.…it would be criminally negligent to ignore the experience of decades upon decades of planning and say to yourself, “Well, that wasn’t what my vision of socialism is, so I’m going to ignore it.” Because if you do that, I can guarantee 100 percent you will end up repeating many of the mistakes and falling into the same dilemmas that the planners did.

I could offer critiques. Stalin was not an impediment to central planning but a consequence of it. And to warn that ignoring the experience of central planning risks repeating “the same dilemmas that the planners did” is a bloodless way to describe dictatorship, famine, and mass murder. But that would be churlish. Let me end instead by saying that I agree with this:

If we’re actually serious about changing the world, people on the Left … should be the most remorseless and the most merciless when it comes to facts.

Replace “people on the Left” with “we” and the line is exactly right.

How Much Has Shale Gas Saved U.S. Consumers?

Every US president since Nixon has called for freeing the US from ‘dependence on foreign oil’ (within ten years!). Every president has failed. Fracking, however, has delivered the goods. Fracking has reduced the price of energy, reduced net emissions of greenhouse gases and turned the US into an energy exporter.

In How Much Has Shale Gas Saved U.S. Consumers? Lucas Davis compare LNG prices in the US ($5.3 Mcf), Europe ($14.4 Mcf) and Japan ($16.1 Mcf) to offer some plausible back of the envelope calculations:

Advances in hydraulic fracturing and horizontal drilling caused U.S. natural gas production to increase significantly, and the U.S. went from being a net importer of natural gas to being the world’s largest exporter. This paper calculates how much shale gas has saved U.S. natural gas consumers. Using price differences between the United States, Europe and Japan, we calculate that U.S. natural gas consumers have saved $4.5-$5.3 trillion between 2007 and 2025, equivalent to $237-$276 billion annually. Access to low-price U.S. natural gas has been particularly valuable during major supply shocks such as the war in Ukraine, and the benefits of shale gas have been experienced broadly across sectors and states.