Where to dine in London

Sunday assorted links

1. Obama at night (NYT).

2. MIE experiment: “Who would go to a restaurant to eat Frosted Flakes—and pay $6, maybe even $8 for it? What if the bowl was topped with a sprinkle of lemon zest, toasted pistachios and fresh thyme, and was singularly delicious?” New York will soon find out.

3. One dad’s story on confirmation and availability bias.

4. Why are NBA stars paid more than NFL stars?

5. “In 2013, there were 166 black-owned radio stations and 68 black-owned radio companies, compared with 250 stations and 146 companies in 1995…” Black media companies are now fighting for survival (NYT). I would say the returns to scale have been going up in the sector, though at much smaller levels the returns to scale are down, witness “Black Twitter.” This is perhaps another example of the hollowing out of the middle.

6. The magical thinking of pro-Brexit conservatives. And put the referendum aside, constituency-by-constituency, most of the support is for Leave. Sobering. And here is an excellent John Kay piece: “As one student of Scottish politics, explaining the UK Independence party’s lack of traction north of the border, put it to me two years ago: “People in Scotland who are disgruntled and suspicious of foreigners [the English] already have a party they can vote for.””

Paul Krugman on Brexit and falling investment

I think there is a pretty simple story here. Brexit increases uncertainty, both in the mean-preserving sense, and in the “very bad outcomes are now more likely” sense, and that lowers investment. That in turns shifts back the aggregate demand and aggregate supply curves, and a recession may result. Less than a year ago, MIT economist Olivier Blanchard published a major paper on capital inflows being expansionary, and now of course we are seeing the reverse. Toss in some negative wealth effects for further transmission. I was at an event in The City a few days ago where the anecdotal data about postponed or cancelled deals seemed pretty overwhelming, and this is consistent with what one reads in the papers as well, not to mention with basic economic theory. It is true of course that we don’t know how large these effects will be, but the more purely British measures of equity value are still down quite a bit.

Krugman is usually an exponent of the “don’t make things too complicated” approach, but here in this blog post he wants to…make things too complicated:

Second, doesn’t this argument imply a later investment boom once the uncertainty is resolved in either direction? That is, once Prime Minster Farage and President Le Pen have engineered the demise of the EU, there’s no reason to wait, and all the pent-up investment comes roaring back, right? But I haven’t heard anyone arguing that the contractionary effect of Brexit will be followed by a compensating boom once things settle down.

Third, doesn’t this argument suggest essentially the same effects from any policy negotiation whose end result isn’t known? Why don’t we say that the possibilities of TPP or TTIP are contractionary, because firms have an incentive to postpone investment decisions until they know whether these agreements actually happen? Somehow, though I’ve never heard anyone argue for the depressing effects of pending trade liberalization.

It is true investment might bounce back if Brexit were essentially undone, but that is hardly an argument for Brexit. The UK economy is about 85 percent services, those are currently “passported” into the rest of the EU, and it is very very hard to negotiate a new free trade agreement for services in anything like a timely manner, even when passions are not inflamed and there are no considerations of punishing other possible EU-defecting countries. So if you read someone writing “…after Brexit, the UK will face an average tariff rate of only xxx…” that is a sign they are not thinking hard enough about how trade agreements for services really work.

(Note also the subtle point that when financial and business services are being sold, the difference between “FDI falling” and “trade and exports falling” is quite a subtle one. Most of all, the traders of these services are investing in ongoing relationships. The decline of trade and the decline of investment are two ways of talking about the same contractionary process, it is not as if FDI falls, the exchange rate falls, and then trade then rises to pick up the slack, at least not in the UK-EU context. What is happening is that a negative shock to both trade and investment is coming up front, and then the British pound falls; the second-order response to that currency decline won’t undo the initial problem.)

On whether the same macroeconomic logic applies to other trade agreements, many investors may be playing “wait and see” before doing more FDI in say Vietnam. But still the very prospect of TPP in the meantime should not be lowering the chance of such investment in Vietnam because TPP represents some chance of a positive-sum advance. The potential loser is more plausibly China, and one does read about this effect. Investors may be less likely to set up plants in China because they are waiting on news about the options in lower-cost Vietnam. Of course given the relative sizes of China and Vietnam, this is unlikely to be a very large effect, but it does exist and it is already discussed. In contrast to that example, the EU is by far the biggest trading and FDI partner for the United Kingdom, and the prospective trade change is negative-sum rather than positive-sum.

What is most striking about Krugman’s post is how many Krugmanisms are completely absent from it. I mean recent Krugmanisms, this isn’t some kind of 1990s nostalgia (not today at least). Here are a few Krugmanisms which appear to be missing in action:

1. The EU is quite indecisive, it just kicks the can down the road and doesn’t resolve much uncertainty. Why not expect the same when dealing with the uncertainty from Brexit?

2. Just apply the AD-AS model quite simply, and follow it where it leads you.

3. How about increasing returns to scale? A lot of the UK exports to the EU are finance and business services, both areas which are plausibly based on clustering and scale economies. An initial whack to a clustered IRS sector can have quite significant long-run consequences, even if some or maybe even all of the initial penalty is reversed. This is part of what Krugman won a Nobel Prize for, admittedly I am hearkening back to the 90s and indeed 80s here but Krugman has cited this argument many times much more recently. This is also another reason why higher trade won’t make up for the investment shortfall, because the investment shortfall stifles the prospects for future high value-added trade.

4. The gravity equation. The pound has depreciated, but the EU is the UK’s natural trading partner, for reasons of distance, and the UK is unlikely to make up the difference by exporting more to the rest of the world. Export adjustment from currency depreciation won’t in general neutralize the impact of investment-destroying and EU-trade-destroying policy changes.

5. What about the multiplier? Isn’t the multiplier HUUGE in economies at the zero bound? And isn’t that the UK? And Cameron already has announced, plausibly in my view, that the UK won’t be meeting its forthcoming revenue targets. Won’t that result in a form of additional austerity sooner or later? With yet further multiplier-based negative macroeconomic consequences?

Where is the multiplier? I want my Paul Krugman back!

Going broader lens here, and moving away from Krugman, what I notice is many of the less academic Keynesians becoming less and less comfortable making arguments about deficient or contracting investment. C + I + G + X is ever so slowly morphing into C + G + X, at least in popular discourse. That is odd, because Keynes himself was most concerned with the instability of investment. It seems that these days however to worry about investment is to sympathize with capitalists, and perhaps to even wish to keep more resources in their hands.

I want my investment back! It is no accident that Keynes’s solution was to nationalize investment, not to redistribute away from capital per se. But nationalizing investment isn’t very popular these days, and so the vitality of capitalism and capitalists once again becomes — or should become — an important issue.

DisUnited Kingdom fact of the day

Looking at the impact of housing costs on living standards among different groups, the report shows from the start of the income slowdown in 2002 to 2015:

- Over half of households across the working age population have seen falling or flat living standards – equivalent to almost 11 million households;

- Two-thirds of the growth in average working age income has been wiped out by rising housing costs;

- More than all of the growth in private renter income has been wiped out by rising housing costs; and,

- The same is true for households headed by someone aged 25-44 who will also have seen all of the growth in average income wiped out by rising housing costs.

The report shows that while London is a standout case in terms of how housing costs have dragged down living standards – the share of income spent on housing has risen by almost a third in the capital since the early 2000s – it is wrong to see this as a southern problem. It finds that the North is catching up with the South – Scotland, the North West and the East Midlands have all experienced sharper increases in housing costs as a proportion of income than the South East and South West.

That is from the Resolution Foundation.

Saturday assorted links

1. Communist Youth League short propaganda video about China, Straussian.

2. “Despite a long-term decline in the size of the working class to just 25%, the proportion of the [British] public who identify themselves as working class has remained stable over time, says the survey. Significantly, it finds that people with middle class occupations who still regard themselves as working class are more likely to be socially conservative on issues such as immigration.” Link here.

Claims about clutter

Tidy by category, not by location

One of the most common mistakes people make is to tidy room by room. This approach doesn’t work because people think they have tied up when in fact they have only shuffled their things around from one location to another or scattered items in the same category around the house, making it impossible to get an accurate grasp of the volume of things they actually own.

The correct approach is to tidy by category. This means tidying up all the things in the same category in one go. For example, when tidying the clothes category, the first step is to gather every item of clothing from the entire house in one spot. This allows you to see objectively exactly how much you have. Confronted with an enormous mound of clothes, you will also be forced to acknowledge how poorly you have been treating your possessions. It’s very important to get an accurate grasp of the sheer volume for each category.

That is from Marie Kondo, Spark Joy: An Illustrated Guide to the Japanese Art of Tidying, a recommended book. Also never tidy the kitchen first, do not keep make-up and skin care products together, and “…the first step in tidying is to get rid of things that don’t spark joy.”

I have a related tip. If you want to do a truly significant clean-up, focus only on those problems which are not immediately visible. This will help you build efficient systems, and prepare the way for more systematic solutions to your clutter problems. You’ll then be prompted to take care of the visible problems in any case. If you focus on the visible problems instead, you will solve them for a day or two but they will rapidly reemerge because the overall quality of your systems has not improved.

Auckland, New Zealand markets in everything

Officials announced that they will now offer families up to NZ$5,000 (about $3,500 US dollars) to relocate to another area of the country.

The relocation grant is specifically for Auckland residents who meet the low-income requirements that make them eligible for social housing, or the city’s subsidized public housing program. The move comes at a time when there are more than 3,500 eligible people in the city waiting to be matched to a home. Forty-two percent of those people identified as Māori, according to the city’s most recent quarterly statement.

Here is the full story, via Richard Kuo. Auckland has for some while been the world’s largest and most splendid Polynesian city, but perhaps that will not last forever.

The Surprisingly Swift Decline of US Manufacturing Employment

There is a new AER paper by Justin R. Pierce and Peter K. Schott, here is the abstract:

This paper links the sharp drop in US manufacturing employment after 2000 to a change in US trade policy that eliminated potential tariff increases on Chinese imports. Industries more exposed to the change experience greater employment loss, increased imports from China, and higher entry by US importers and foreign-owned Chinese exporters. At the plant level, shifts toward less labor-intensive production and exposure to the policy via input-output linkages also contribute to the decline in employment. Results are robust to other potential explanations of employment loss, and there is no similar reaction in the European Union, where policy did not change.

Here are various ungated versions.

Florida alligator attack facts

The activities of victims at the time of attack in the Florida cases were distributed as follows: 17.4 percent were related to trying to capture/pick up/exhibit the animal; 16.7 percent involved swimming; 9.9 percent involved fishing; 9.5 percent related to retrieving golf balls; and 5.3 percent involved wading/walking in water.

Here is more information. Staying away from alligators — and golf — would seem to eliminate most but not all of these attacks.

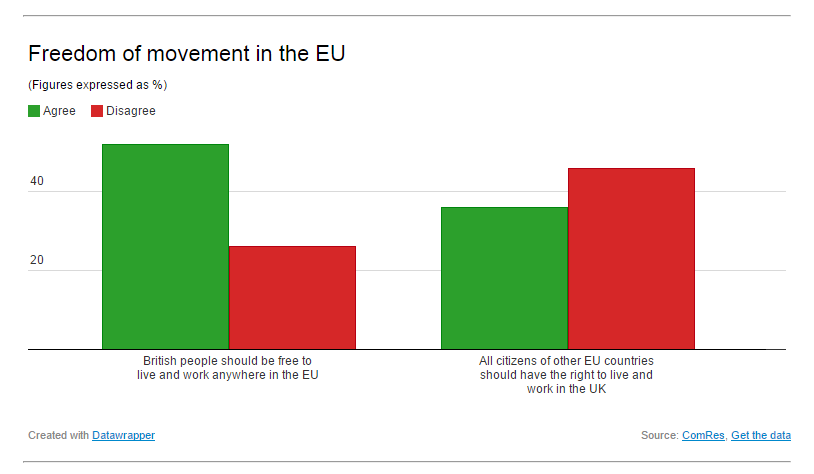

Sorry, but you Kant have that

The British public wants the right to work in the EU but they don’t want EU citizens to have the right to work in the UK.

This was from a poll taken in 2014 that presciently illustrated some of today’s confusions and misgivings.

Hat tip: Lones Smith.

Friday assorted links

1. New Tate Watkins eBook, market-oriented approach to understanding Haiti.

2. “I sought one ring to rule them all.”

3. George Borjas on peer review and the recent brouhaha.

4. First fatality with a self-driving car. The NYT article has more detail: “Neither autopilot nor the driver noticed the white side of the tractor-trailer against a brightly lit sky, so the brake was not applied.”

Thwarted China markets in everything

Chinese Taylor Swift fans hoping to hedge their heartbreak by insuring against the downturns in the pop star’s love life are now out of luck.

Taobao, China’s largest online marketplace, has cracked down on vendors who were offering “insurance policies” on Swift’s reported relationship with British actor Tom Hiddleston.

The Hiddleswift plan offered double your money if the couple split up. According to China’s state-run Xinhua News Agency, Taobao vendors had begun taking bets on the pop star’s romantic fortunes last week, with the minimum wager set at 1 yuan (15 cents).

Here is the link, via Christopher Balding.

The division of labor is limited by the extent of the market, installment #1437

We heard about a lawyer who focuses on cases about malfunctioning automatic garage door openers.

Here is the story and link, via Samir Varma.

Why did the Stars Wars and Star Trek worlds turn out so differently?

That question came up briefly in my chat with Cass Sunstein, though we didn’t get much of a chance to address it. In the Star Trek world there is virtual reality, personal replicators, powerful weapons, and, it seems, a very high standard of living for most of humanity. The early portrayals of the planet Vulcan seem rather Spartan, but at least they might pass a basic needs test of sorts, plus there is always catch-up growth to hope for. The bad conditions seem largely reserved for those enslaved by the bad guys, originally the Klingons and Romulans, with those stories growing more complicated as the series proceeds.

In Star Wars, the early episodes show some very prosperous societies. Still, droids are abused, there is widespread slavery, lots of people seem to live at subsistence, and eventually much of the galaxy falls under the Jedi Reign of Terror.

Why the difference? Should we consult Acemoglu and Robinson? Or is it about economic geography? I can find think of a few factors differentiating the world of Star Wars from that of Star Trek:

1. The armed forces in Star Trek seem broadly representative of society. Compare Uhura, Chekhov, and Sulu to the Imperial Storm troopers.

2. Captains Kirk and Picard may be overly narcissistic, but they do not descend into true power madness, unlike various Sith leaders and corrupted Jedi Knights.

3. In Star Trek, any starship can lay waste to a planet, whereas in Star Wars there is a single, centralized Death Star and no way to oppose it, short of having the rebels try to blow it up. That seems to imply stronger checks and balances in the world of Star Trek. No single corrupt captain can easily take over the Federation, and so there are always opposing forces.

4. Star Trek embraces analytical egalitarianism, namely that all humans consider themselves part of the same broader species. There is no special group comparable to the Jedi or the Sith, with special powers or with special whatevers in their blood. There are various species of aliens, but they are identified as such, they are not in general going to win human elections, and furthermore humans are portrayed as a kind of galactic hegemon, a’ la the United States circa the postwar era.

5. The single individual is much more powerful in the world of Star Wars, due to Jedi and Sith powers, which seems to lower stability. In the Star Trek world, some of the biggest trouble comes from super-human Khan and his clan, but fortunately they are put down.

6. Star Trek replicators are sufficiently powerful it seems slavery is highly inefficient in that world. In Star Wars the underlying depreciation rate, as you would find it measured in a Solow model, seems to be higher. More forced labor is drafted into use to repair all of that wasting capital.

What else?

Addendum: Here is Cass on Star Wars vs. Star Trek.

*Continental Drift*

The author is Benjamin Grob-Fitzgibbon and the subtitle is Britain and Europe from the End of Empire to the rise of Euroscepticism. It is maybe the best book to read on Britain’s earlier relations with the European Union. Here is one bit:

The vast majority of the Labour Party was anti-EEC, believing that it was a capitalist conspiracy that would undermine Britain’s control of its own industry.

That was during the 1960s. And this:

When it awoke on the morning of 1 January 1973 as a full member of the European Economic Community (EEC), the British public was deeply ambivalent. In a poll taken 3-7 January 1973, 36 percent of the public reported being ‘quite or very pleased’; 33 percent were ‘quite or very displeased’ and an astonishing 20 percent purported to be ‘indifferent’ (the remaining 11 p cent were undecided, but not indifferent.

By August 1973, 52 per cent were opposed and only 32 per cent still in favor.

Definitely recommended, a book for our times.