Results for “age of em” 17234 found

The importance of cognitive endurance

Schooling may build human capital not only by teaching academic skills, but by expanding the capacity for cognition itself. We focus specifically on cognitive endurance: the ability to sustain effortful mental activity over a continuous stretch of time. As motivation, we document that globally and in the US, the poor exhibit cognitive fatigue more quickly than the rich across field settings; they also attend schools that offer fewer opportunities to practice thinking for continuous stretches. Using a field experiment with 1,600 Indian primary school students, we randomly increase the amount of time students spend in sustained cognitive activity during the school day—using either math problems (mimicking good schooling) or non-academic games (providing a pure test of our mechanism). Each approach markedly improves cognitive endurance: students show 22% less decline in performance over time when engaged in intellectual activities—listening comprehension, academic problems, or IQ tests. They also exhibit increased attentiveness in the classroom and score higher on psychological measures of sustained attention. Moreover, each treatment improves students’ school performance by 0.09 standard deviations. This indicates that the experience of effortful thinking itself—even when devoid of any subject content—increases the ability to accumulate traditional human capital. Finally, we complement these results with quasi-experimental variation indicating that an additional year of schooling improves cognitive endurance, but only in higher-quality schools. Our findings suggest that schooling disparities may further disadvantage poor children by hampering the development of a core mental capacity.

Here is the full paper by Christina Brown, Supreet Kaur, Geeta Kingdon, and Heather Schofield, via the excellent Kevin Lewis.

I should note that I view this as one of the areas where I feel I have trained myself best. I recall last year having serious airport travel problems, and a trip that should have taken two hours ended up being almost twelve hours, with uncertainty along the way and two different last-minute improvised airport stops and no lounges. But I still was able to read, concentrate, and work for the entire period without feeling any major drain. As for this paper, it is yet another way that schooling teaches the median student something, even though he/she cannot regurgitate any particular lesson on demand.

India fact of the day

India’s state capacity recently has surpassed the global average.

Pinch yourself! Here are various Berggruen governance indices. Here is the interactive site.

More persistence and propagation than you might think?

Macroeconomic cycles are much more self-reinforcing and correspondingly resistant to shocks and hence longer-lasting than what is commonly thought…

The key idea is that economic developments feature strong endogenous propagation mechanisms which yield endogenous cyclical behavior ala limit cycles.

And:

What is at heart of this behavior? There are three factors that the authors point towards. First is strategic complementarity between economic agents’ behavior, such as the fact that firms want to invest when other firms are investing. Second, you need inertia in individual behavior, so that rapid changes in behavior are costly. And finally, you need dependence on some stock variable such as aggregate amount of capital or durable goods. All of these requirements seem very realistic assumption about the real world.

What are the implications of such model? Among other things this means that in certain periods of time the economy is very robust to negative shocks, because these shocks do not have the power to overturn the forces (resulting from the strategic complementarity between agents) that are pushing economic activity higher. They might push us slightly lower for some period of time, but they don’t turn things completely around. And once their effect fades the economy continues in its previous trajectory. In a sense, this view suggests that economic cycles are more like a titanic.

It also means that there is certain dichotomy in terms of shocks. Shocks ranging in size from “small” to “large-but-not-gigantic” proportions do not change the underlying trajectory of the economy, unless we are already close to turning point in the limit cycle. Meanwhile, truly gigantic shocks, like the global financial crisis, are not just deviation from the medium-term trend defined by the limit cycle, but a change in the medium-term trend.

And in conclusion:

To summarize, the limit cycle view suggests that a powerful enough shock, such as the rebound when economies re-opened after the pandemic recession, can put us on a upward spiral, and that such spiral features such a strong self-reinforcing mechanisms that even large negative shocks cannot derail us. This in contrast to standard DSGE models that feature only relatively weak propagation of shocks, and, crucially, do not feature any medium-term cyclical behavior.

Here is much more from Kamil Kovar, a good and important post.

Friday assorted links

1. Tymofiy Mylovanov on foreign aid in Ukraine.

2. The most beautiful post offices? Why are none of them recently built? Recommended.

3. The contrarian case for Pakistan’s upside.

4. AI girlfriends markets in everything. And LLM liability for financial advising — what is the right approach?

5. Florida insurance carrier update.

Substitutes Are Everywhere: The Great German Gas Debate in Retrospect

In March of 2022 a group of top economists released a paper analyzing the economic effects on Germany of a stop in energy imports from Russia (Bachmann et al. 2022). Using a large multi-sector mathematical model the authors concluded that if prices were allowed to adjust, even a substantial shock would have relatively low costs. In contrast, the German chancellor warned that if the Russians stopped selling oil to Germany “entire branches of industry would have to shut down” and when asked about the economic models he argued that:

[the economists] get it wrong! And it’s honestly irresponsible to calculate around with some mathematical models that then don’t really work. I don’t know absolutely anyone in business who doesn’t know for sure that these would be the consequences.

The Chancellor was not alone in predicting big economic losses; some studies estimated reductions in output of 6-12% and millions of unemployed workers. The key distinction between the economists and the others was in their understanding of elasticities of substitution. When the Chancellor and the average person think about a 40% reduction in natural gas supplies, they implicitly assume that each natural gas-dependent industry must cut its usage by 40%. They then consider the resulting decline in output and the cascading effects on downstream industries. It’s easy to get very worried using this framework.

When the economists replied that there were opportunities for substitution they were typically met with disbelief and misunderstanding. The disbelief stemmed from a lack of appreciation of the many opportunities for substitution that permeate an economy. In our textbook, Modern Principles, Tyler and I explain how the OPEC oil shock in the 1970s led to an increase in brick driveways (replacing asphalt) and the expansion of sugar cane plantations in Brazil (for ethanol production). Amazingly, the oil shock also prompted flower growers to move production overseas, as the reduction in heating oil costs from growing in sunnier climates outweighed the increase in transportation fuel expenses. While these examples highlight long-term changes, short-term substitutions are also possible, though their precise details are usually hidden from central planners and economists.

The misunderstanding came from thinking that we need every user of fuel to find substitutes. Not at all! In reality, as fuel prices rise, those with the lowest substitution costs will switch first, freeing up fuel for users who have more difficulty finding alternatives. Just one industry with favorable substitution possibilities, combined with a few moderately adaptable industries, can produce a significant overall effect. Moreover, there are nearly always some industries with viable substitution options. To see why reverse the usual story and ask, if fuel prices fell by 50% could your industry use more fuel? And if fuel prices fell by 50% are their industries that could switch into the now cheaper fuel?

The misunderstanding came from thinking that we need every user of fuel to find substitutes. Not at all! In reality, as fuel prices rise, those with the lowest substitution costs will switch first, freeing up fuel for users who have more difficulty finding alternatives. Just one industry with favorable substitution possibilities, combined with a few moderately adaptable industries, can produce a significant overall effect. Moreover, there are nearly always some industries with viable substitution options. To see why reverse the usual story and ask, if fuel prices fell by 50% could your industry use more fuel? And if fuel prices fell by 50% are their industries that could switch into the now cheaper fuel?

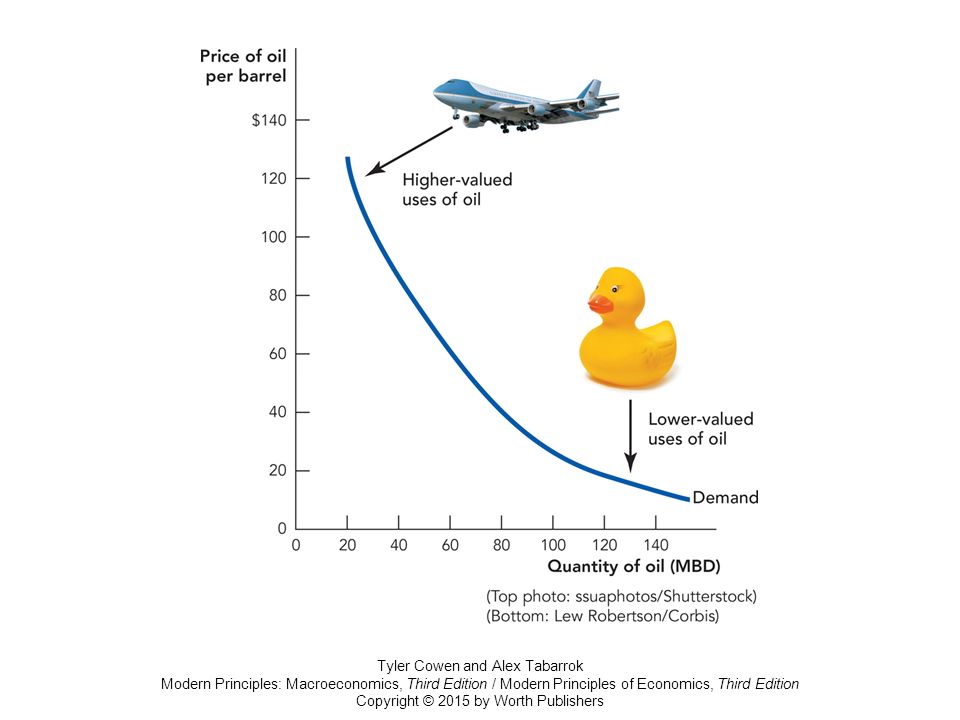

People often find it easier to imagine new uses rather than ways to reduce existing consumption. However, it is typically the new uses that are scaled back first. Tyler and I illustrate this with our jet and rubber ducky graph. Although jet aircraft won’t shift away from oil even at high prices, rubber (actually plastic) duckies, which are made from oil, can find substitutes–wood, for example–when oil prices rise. And if plastic ducky manufacturers cannot find substitutes, they go out of business, freeing up more oil for other uses. In this way, the market identifies the least valuable goods to cease production, another kind of substitution.

Substitution is a more nuanced concept than many people imagine. Here’s another example. Imagine that an economy has an energy-intensive goods producing sector and that there are few substitutes for the fuel used in this sector. Disaster? Not at all. We don’t need a fuel substitute, if we can substitute imports of the energy-intensive goods for domestically produced versions. Storage is also a substitute and notice that the more you substitute away from a fuel in final uses the greater the effective storage. If you use 1 gallon a day a 10 gallon tank lasts 10 days. If you use a quarter gallon a day it lasts 40 days. Everything is connected.

All of these myriad changes happen under the guidance of the invisible hand, i.e. the price system. Remember, a price is a signal wrapped up in an incentive. Thus Bachmann et al. wisely recommended letting energy prices rise to convey the signal and not insuring energy users so the incentive effects were fully felt on the margin.

So what happened? Gas from Russia was indeed cut very substantially but the German economy did not collapse and instead proved as robust as predicted, perhaps even more so. (The Chancellor’s predictions were off the mark but, to be fair, the government also did do a good job in sourcing new supplies and building reserves.) Moll, Schularick, and Zachmann have revisited the analysis and conclude:

The economic outcomes confirm the core theoretical argument that macro elasticities are larger than micro elasticities and that “cascading effects” along the supply chain would be muted as opposed to destroying the economy’s entire industrial sector. As foreseen, producers partly switched to other fuels or fuel suppliers, imported products with high energy content, while households adjusted their consumption patterns….Market economies have a tremendous ability to adapt that was widely underestimated. In addition, the German economics ministry (BMWK) was very successful in quickly sourcing gas supplies from third countries and building LNG capacity. Finally, it probably helped that German policymakers refrained from imposing a price cap on natural gas (like in many other European countries) and instead opted for lumpsum transfers based on households’ and firms’ historical gas consumption.

Hat tip: Alex Wollman.

Is it good to say “um”?

Disfluencies such as pauses, “um”s, and “uh”s are common interruptions in the speech stream. Previous work probing memory for disfluent speech shows memory benefits for disfluent compared to fluent materials. Complementary evidence from studies of language production and comprehension have been argued to show that different disfluency types appear in distinct contexts and, as a result, serve as a meaningful cue. If the disfluency-memory boost is a result of sensitivity to these form-meaning mappings, forms of disfluency that cue new upcoming information (fillers and pauses) may produce a stronger memory boost compared to forms that reflect speaker difficulty (repetitions). If the disfluency-memory boost is simply due to the attentional-orienting properties of a disruption to fluent speech, different disfluency forms may produce similar memory benefit. Experiments 1 and 2 compared the relative mnemonic benefit of three types of disfluent interruptions. Experiments 3 and 4 examined the scope of the disfluency-memory boost to probe its cognitive underpinnings. Across the four experiments, we observed a disfluency-memory boost for three types of disfluency that were tested. This boost was local and position dependent, only manifesting when the disfluency immediately preceded a critical memory probe word at the end of the sentence. Our findings reveal a short-lived disfluency-memory boost that manifests at the end of the sentence but is evoked by multiple types of disfluent forms, consistent with the idea that disfluencies bring attentional focus to immediately upcoming material. The downstream consequence of this localized memory benefit is better understanding and encoding of the speaker’s message.

That is from a recent paper by Diachek, E., & Brown-Schmidt, S., via Ethan Mollick.

*The Middle Kingdoms: A New History of Central Europe*

An excellent book by Martyn Rady, here is the passage most relevant to the history of economic thought:

A Norwegian economist and his wife have published a line of bestsellers in the field of economics written before 1750. Top is Aristotle’s Economics. Composed in the fourth century BCE, it is still available in paperback. Martin Luther’s denunciation of usury (1524) is number three. But there, in the top ten, is an unfamiliar name — Veit Ludwig von Seckendorff (1626-1692), who was a government official in the duchy of Saxe-Gotha in Thuringia. Seckendorff’s German Princely State (Teutscher Fürsten-Staat, 1656) is a thousand-page blockbuster that went through thirteen editions and was in continuous print for a century. Although only ever published in German, it was influential throughout Central Europe, shaping policy from the Banat to the Baltic.

I enjoyed this sentence:

Besides his distinctive false nose (the result of a duelling accident), Tycho Brahe kept an elk in his lodgings as a drinking companion.

And yes the book does have an insightful discussion of Laibach, the Slovenian hard-to-describe musical band. You can buy it here.

How to improve education

We present results from large-scale randomized trials evaluating the provision of education in emergency settings across five countries: India, Kenya, Nepal, Philippines, and Uganda. We test multiple scalable models of remote instruction for primary school children during COVID-19, which disrupted education for over 1 billion schoolchildren worldwide. Despite heterogeneous contexts, results show that the effectiveness of phone call tutorials can scale across contexts. We find consistently large and robust effect sizes on learning, with average effects of 0.30-0.35 standard deviations. These effects are highly cost-effective, delivering up to four years of high-quality instruction per $100 spent, ranking in the top percentile of education programs and policies.

That is from a new NBER working paper by Noam Angrist, et.al.

The FDA Still Doesn’t Trust Women

The FDA has a long history of antipathy towards personal testing. The FDA has opposed personal pregnancy tests, HIV tests, genetic tests, and COVID tests, as I discussed in my article Testing Freedom. Well, the FDA is at it again:

NYTimes: At a hearing Tuesday to consider whether the Food and Drug Administration should authorize the country’s first over-the-counter birth control pill, a panel of independent medical experts advising the agency was left to reckon with two contradictory analyses of the medication called Opill.

During the eight-hour session, the manufacturer of the pill, HRA Pharma, which is owned by Perrigo, and representatives of many medical organizations and reproductive health specialists said that data strongly supported approval. They said that Opill, approved as a prescription drug 50 years ago, was safe, effective and easy for women of all ages to use appropriately — and that over-the-counter availability was sorely needed to lower the country’s high rate of unintended pregnancies.

In contrast, F.D.A. scientists questioned the reliability of company data that was intended to show that consumers would take the pill at roughly the same time every day and comply with directions to abstain from sex or temporarily use other birth control if they missed a dose. The agency seemed especially concerned about whether women with breast cancer or unexplained vaginal bleeding would correctly choose not to take Opill and whether adolescents and people with limited literacy would use it accurately.

Note carefully: The FDA isn’t worried that women won’t take the pill at the same time every day they are worried that women who get the pill without a prescription won’t take it at the same time every day. I guess in the FDA’s view women need some mansplaining to take birth control or at least some doctorplaining.

Dr. Westhoff suggested that for most women, there is no advantage to a doctor prescribing the pills because doctors don’t typically monitor patient adherence and often only see such patients once a year.

Similarly, I suspect that women with breast cancer will be concerned enough about their health to read the warning, Don’t Take This Pill if You Have Breast Cancer. Who knows, women with breast cancer might even ask their cancer physician or Google or their GP(T) about what foods and drugs to take and which to avoid.

If I didn’t know the FDA’s long history of opposing personal testing, I would think this simply bizarre but not trusting people with their own health decisions is practically in the FDA’s DNA.

The Gender Well-being Gap

Overall, are men or women happier? It is complicated, and it depends on what you mean exactly:

Given recent controversies about the existence of a gender wellbeing gap we revisit the issue estimating gender differences across 55 subjective well-being metrics – 37 positive affect and 18 negative affect – contained in 8 cross-country surveys from 167 countries across the world, two US surveys covering multiple years and a survey for Canada. We find women score more highly than men on all negative affect measures and lower than men on all but three positive affect metrics, confirming a gender wellbeing gap. The gap is apparent across countries and time and is robust to the inclusion of exogenous covariates (age, age squared, time and location fixed effects). It is also robust to conditioning on a wider set of potentially endogenous variables. However, when one examines the three ‘global’ wellbeing metrics – happiness, life satisfaction and Cantril’s Ladder – women are either similar to or ‘happier’ than men. This finding is insensitive to which controls are included and varies little over time. The difference does not seem to arise from measurement or seasonality as the variables are taken from the same surveys and frequently measured in the same way. The concern here though is that this is inconsistent with objective data where men have lower life expectancy and are more likely to die from suicide, drug overdoses and other diseases. This is the true paradox – morbidity doesn’t match mortality by gender. Women say they are less cheerful and calm, more depressed, and lonely, but happier and more satisfied with their lives, than men.

That is from a new NBER working paper by David G. Blanchflower and Alex Bryson. Those results are broadly consistent with my intuitions and anecdotal observations, noting that men and women probably mean different things when they say they are/are not satisfied with their lives.

Private ownership sentences to ponder

Anyone keen to understand how should look at Brookfield Renewable Partners’ recent investment of up to $2 billion in Scout Clean Energy and Standard Solar. B.R.P. is a vehicle of Brookfield Asset Management, a leading global asset management firm, with around $800 billion of assets under management, and it purchased two American developers and owner-operators of wind and solar power-generating facilities. This took place six weeks after President Biden signed the I.R.A. into law.

The I.R.A. will help accelerate the growing private ownership of U.S. infrastructure and, in particular, its concentration among a handful of global asset managers like Brookfield. This is taking the United States into risky territory. The consequences for the public at large, whose well-being depends on the quality and cost of a host of infrastructure-based services, from energy to transportation, are unlikely to be positive.

A common belief about both the I.R.A. and 2021’s Infrastructure Investment and Jobs Act, President Biden’s other key legislation for infrastructure investment, is that they represent a renewal of President Franklin Roosevelt’s New Deal infrastructure programs of the 1930s. This is wrong. The signature feature of the New Deal was public ownership: Even as private firms carried out many of the tens of thousands of construction projects, almost all of the new infrastructure was funded and owned publicly. These were public works. Public ownership of major infrastructure has been an American mainstay ever since…

So it would be truer to say that in political-economic terms, Mr. Biden, far from assuming Roosevelt’s mantle, has actually been dismantling the Rooseveltian legacy. The upshot will be a wholesale transformation of the national landscape of infrastructure ownership and associated service delivery.

That is from Brett Christophers (NYT), who is disapproving. For an alternative view, see this WSJ Op-Ed by Katherine Boyle and David Ulevitch.

Lessons from the COVID War

In preparation for a National Covid Commission a group of scholars directed by Philip Zelikow (director of the 9/11 Commission) began interviewing people and organizing task forces (I was an interviewee). The Covid Commission didn’t happen, a fact that illustrates part of the problem:

The policy agenda of both major American political parties appear mostly undisturbed by this pandemic. There is no momentum to fix the system….The Covid war revealed a collective national incompetence in governance….One common denominator stands out to us that spans the political spectrum. Leaders have drifted into treating this pandemic as if it were an unavoidable national catastrophe.

The results of this early investigation, however, are summarized in Lessons from the COVID WAR. Overall, a good book, not as pointed or data driven as I might have liked (see my talk for a more pointed overview), but I am in large agreement with the conclusions and it does contain some clarifying tidbits such as this one on the Obama playbook.

Innumerable speeches, books, and articles have stated that the Obama administration gave the incoming Trump administration a “playbook” on how to confront a pandemic and that this playbook was ignored. The Obama administration did indeed prepare and leave behind the “Playbook for Early Response to High-Consequence Emerging Infectious Disease Threats and Biological Incidents.”

But this playbook did not actually diagram any plays. There was no “how.” It did not explain what to do…when it came to the job of how to contain a pandemic that was headed for the United States in January 2020, the playbook was a blank page.

I also appreciated that Lessons has some some unheralded success stories from the state and local level. You may recall Tyler and I blogging repeatedly in 2020 about the advantages of pooled tests. Eventually pooled testing was approved but I haven’t seen data on how widely pooling was adopted or the effective increase in testing capacity that was produced. Lessons, however, offers an anecdote:

In San Antonio, a local charitable foundation paired with a blood bank to create a central Covid PCR testing lab (antigen tests were not yet readily available) that could combine samples (pooling) for efficiency and cost reduction, but also determine which individual in a pool was positive. Importantly, results were available within about twelve hours. That meant results were available before the start of school the new day.

The program helped San Antonio get kids back into the schools.

More generally, it’s striking that US schools were closed for far longer than French, German or Italian schools. See data at right on the number of weeks that “schools were closed, or party closed, to in-person instruction because of the pandemic (from Feb. 2020-March 2022)”. (South Korea, it should be noted, had some of the most advanced online education systems in the world.)

One general point made in Lessons that I wholeheartedly agree with this is that the school closures and many of the other controversial aspects of the pandemic response such as the lockdowns and mask mandates “were really symptoms of the deep problem. Without a more surgical toolkit, only blunt instruments were left.” With better testing, biomedical surveillance of the virus and honest communication we could have done better with much less intrusive and costly policies.

Addendum: See my previous reviews of Gottlieb’s Uncontrolled Spread, Michael Lewis’s The Premonition, Slavitt’s Preventable and Abutaleb and Paletta’s Nightmare Scenario.

Addendum 2: A typo in Lessons had France closing schools for 2 weeks instead of 12 weeks. Corrected.

Data on diversity, equity, and inclusion

Beware the unobserved heterogeneity, but here goes:

This paper measures diversity, equity, and inclusion (DEI) using proprietary data on survey responses used to compile the Best Companies to Work For list. We identify 13 of the 58 questions as being related to DEI, and aggregate the responses to form our DEI measure. This variable has low correlation with gender and ethnic diversity in the boardroom, in senior management, and within the workforce, suggesting that DEI captures additional dimensions missing from traditional measures of demographic diversity. DEI is also unrelated to general workplace policies and practices, suggesting that DEI cannot be improved by generic initiatives. However, DEI is higher in small growth firms and firms with high financial strength. DEI is associated with higher future accounting performance across a range of measures, higher future earnings surprises, and higher valuation ratios, but demographic diversity is not. DEI perceptions among professional workers, such as R&D employees, are significantly correlated with the number and quality of patents. However, DEI exhibits no link with future stock returns.

That is from a new NBER working paper by Alex Edmans, Caroline Flammer, and Simon Glossner.

The rising tide of housing quality

This study analyzes patterns of housing consumption and expenditures among social safety net recipients since 1985. For safety net recipients, including Supplemental Security Income (SSI), Supplemental Nutrition Assistance Program (SNAP) and cash welfare (AFDC/TANF), monthly housing expenditures have risen from $692 to $1,341. However, these increased expenditures partially reflect housing quantity improvements, including more square footage, more rooms, and larger lot sizes. The data also show a marked improvement in housing quality, such as fewer sagging roofs, broken appliances, rodents, and peeling paint. The housing quality for social safety net recipients improved across 35 indicators. These quality improvements equate to a 35 to 44 percent increase in housing consumption and suggest that a typical safety net recipient in 2021 experiences housing consumption equivalent to the average national household in 1985. Though relative housing consumption has remained similar for safety net recipients, this “rising tide” of housing quality may have additional benefits for the health and well being of families and children living in better housing.

That is from a new paper by Erik Hembre, J. Michael Collins, and Samuel Wylde. Via the excellent Kevin Lewis.

What do LLMs expect for the economy?

I introduce a survey of economic expectations formed by querying a large language model (LLM)’s expectations of various financial and macroeconomic variables based on a sample of news articles from the Wall Street Journal between 1984 and 2021. I find the resulting expectations closely match existing surveys including the Survey of Professional Forecasters (SPF), the American Association of Individual Investors, and the Duke CFO Survey. Importantly, I document that LLM based expectations match many of the deviations from full-information rational expectations exhibited in these existing survey series. The LLM’s macroeconomic expectations exhibit under-reaction commonly found in consensus SPF forecasts. Additionally, its return expectations are extrapolative, disconnected from objective measures of expected returns, and negatively correlated with future realized returns. Finally, using a sample of articles outside of the LLM’s training period I find that the correlation with existing survey measures persists – indicating these results do not reflect memorization but generalization on the part of the LLM. My results provide evidence for the potential of LLMs to help us better understand human beliefs and navigate possible models of nonrational expectations.

That is from a new paper by J. Leland Bybee, via Paul Goldsmith-Pinkham.