Category: Data Source

The importance of tax evasion

Mr. Zucman’s tax evasion numbers are big enough to upend common assumptions, like the notion that China has become the world’s “owner” while Europe and America have become large debtors. The idea of the rich world’s indebtedness is “an illusion caused by tax havens,” Mr. Zucman wrote in a paper published last year. In fact, if offshore assets were properly measured, Europe would be a net creditor, and American indebtedness would fall from 18 percent of gross domestic product to 9 percent.

There is more here, interesting throughout. You will find some of the related research here.

What is the “sticker shock” for ACA reform?

There is a new NBER Working paper on that topic, by Mark Pauly, Scott Harrington, and Mark Leive, here is the abstract:

This paper provides estimates of the changes in premiums, average or expected out of pocket payments, and the sum of premiums and out of pocket payments (total expected price) for a sample of consumers who bought individual insurance in 2010 to 2012, comparing total expected prices before the Affordable Care Act with estimates of total expected prices if they were to purchase silver or bronze coverage after reform, before the effects of any premium subsidies. We provide comparisons for purchasers of self only coverage in California and in 23 states with minimal prior state premium regulation before the ACA now using federally managed exchanges. Using data from the Current Population Survey, we find that the average prices increased by 14 to 28 percent, with similar changes in California and the federal exchange states; we attribute the increase primarily to higher premiums in exchanges associated with insurer expectations of a higher risk population being enrolled. The increase in total expected price is similar for age-gender population subgroups except for a larger than average increases for older women. A welfare calculation of the change in risk premium associated with moving from coverage that prevailed before reform to bronze or silver coverage finds small changes.

You will find an ungated version here. The general point is that you hear enormous amounts of talk, including from economists, about what a success ACA has been. This talk does not in general consider trade-offs or welfare calculations, as could be illustrated by these results.

America fact of the day

…people in the United States now make more [phone] calls to India than to Western Europe…

Part of the background is this:

Traffic between the United States and Europe, both of which have high broadband availability, has shifted to substitutable services over the Internet (e.g. VoIP). India still has a low broadband penetration, meaning people in the United States call mobile telephones.

There is more here, via @internetthought.

What turns students away from political moderation?

…the more engaged students are with faculty members and academics, the more their views moderate toward the center. But the more students become engaged in student activities, the more the liberals become more committed as liberals and conservatives become more committed as conservatives.

There is more information here.

China fact of the day

Average capacity utilization is now below 60 percent.

The article is scary throughout.

Women, wealth, and mobility

Lena Edlund and Wojciech Kopczuk have an AER paper from 2009, the abstract is this:

Using estate tax returns data, we observe that the share of women among the very wealthy in the United States peaked in the late 1960s at nearly one-half and then declined to one-third. We argue that this pattern reflects changes in the importance of dynastic wealth, with the share of women proxying for inherited wealth. If so, wealth mobility decreased until the 1970s and rose thereafter. Such an interpretation is consistent with technological change driving long-term trends in mobility and inequality, as well as the recent divergence between top wealth and top income shares documented elsewhere.

The article is ungated here (pdf). Perhaps this is relevant to some current debates…?

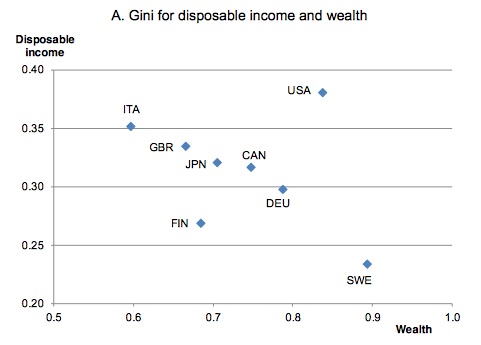

How is income inequality correlated with wealth inequality?

From the OECD, Kaja Bonesmo Frederiksen writes on “More income inequality and less growth” and presents this table:

If you were to fit that with a curve, the overall slope would be negative, suggesting a negative empirical correlation between income inequality and wealth inequality. Now do not leap to a conclusion here, as there are points to be made:

1. This scatter plot is not based on a model with adjustments for confounding factors.

2. These may not be the right or best data on wealth inequality.

3. There are not many data points on this graph in the first place.

4. Lots of other stuff.

The point is that everyone is talking about wealth inequality lately, yet it is not always recognized that the relationship between wealth and income inequality is complex, as illustrated for instance by the case of Sweden. (There is nothing in this post by the way which should be construed as criticism of Piketty, I’m just trying to lay out some basic expository principles.)

Wealth inequality and income inequality may diverge for at least three reasons. First, savings rates may differ across societies. Second, locally available rates of return may differ. Third, the ups and downs of mobility may mean high income inequality in a given year but overall lower levels of wealth inequality.

By the way, here is a good sentence from the abstract:

Wealth dispersion [inequality] is especially high in the United States and Sweden

The support document is here, I have reproduced Figure 3a. Hat tip goes to Luis Pedro Coelho.

Sweden has lots of wealth inequality

Sweden is viewed as an egalitarian utopia by outsiders, but reality is complex. In some ways Sweden has less social equality than the United States. While the American upper class is largely meritocratic, the upper class in Sweden are still mostly defined by birth.

Historically, Sweden, Norway and Finland alone in Europe never developed Feudalism (Denmark was closer to continental Europe). The Nordic nobility was a small share of the population and not as powerful as the nobility in continental Europe, though still influential. The upper class in Sweden today consists of the nobility and of wealthy bourgeoisie families that socially merged with them. Wealthy bourgeois families live in the same neighborhoods and have adopted similar behavior and identity as the nobility. Despite long Social Democratic dominance they remain a coherent social group, with a distinct and recognizable accent, way of dressing, values etc.

Belonging to the upper-class is not defined merely by wealth, depending more on blood. Just as in historical times, a Nouveau riche member of the middle class will not automatically be accepted as a member of the upper-classes, unless they actively adapt their behavior and are accepted by the upper-classes socially.

The upper classes in Sweden retain a disproportional hold on wealth and power. The formal nobility in Sweden constitutes around 0.2% of the population. A couple of years ago I looked through the list of the wealthiest Swedes. Fully 10% of the richest Swedes are members of the nobility. By contrast not a single one of the richest Swedes was a non-European immigrant. Of Sweden’s prime-ministers Sweden during the modern era 20% belonged to the nobility.

Sweden is known for income equality. Increasingly, studies also point to Sweden as a country characterized by high intergenerational mobility of income. Income-distribution and wealth distribution are however not the same thing. What some may not know is that wealth-inequality is relatively high in Sweden. The top one percent own around 35% of wealth in the United States. In Sweden, because of extensive tax evasion, the number is harder to calculate. When including estimates of wealth held outside of Sweden, Roine and Waldenström estimate that the top one percent richest Swedes own 25-40% of total wealth, not far from American inequality levels, and increasing more rapidly.

At the same time, the intergenerational mobility of top wealth is chokingly low. A recent studyfound that a astonishing 80-90% of inequality of top wealth is transmitted to the next generation in Sweden!

According to one studythe share of the richest Swedes who inherited their wealth is around, 2/3 with 1/3 being entrepreneurs, while in the United States it was the opposite, with 1/3 of the wealthiest inherited their wealth while around 2/3 are entrepreneurs.

Thus while the Swedish middle class is large and has a compressed earning distribution, at the very top you have a small number of aristocratic families controlling much of the wealth. Mobility into this group is rare, probably rares than it is in the United States. One reason are stronger informal class-barriers, merely earning wealth is not enough to be accepted a member of the aristocratic upper-class. Another more interesting reason may be the unintended effect of welfare-state economic policies.

During the era of Social Democratic dominance, they wondered how to deal with wealth inequality. The dilemma facing the Social Democrats was this: The upper-class business families did a very good job managing Swedish export industry, the key to Sweden’s wealth. This is especially true for the Wallenberg family, the leading industrial family in Sweden, controlling amongst others ABB, Ericsson, Electrolux, Atlas Copco, SKF, AstraZeneca and Saab and doing an excellent job.

The Social Democrats decided to accept the unequal distribution of assets, but simply make these assets worth less using punitive high tax rates. Because of high inflation capital taxes were often 80-100%.

The upper-class families still owned most of private industry, but because of taxes those assets were simply not worth much. Paradoxically the high taxes and capital regulations which prevented foreign investments seem to have helped freeze the asset distribution into place, with the share of wealth owned by the rich being fairly constant between 1970 to the 1990s.

The OECD also reports that Sweden is quite unequal in wealth, hat tips go to Old Whig and Luis Pedro Coelho.

Piketty responds to critics

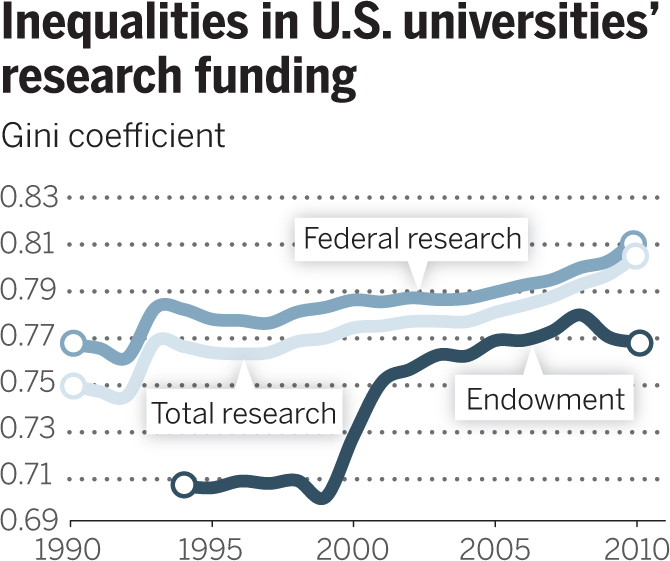

Gini coefficient for U.S. universities

For the pointer I thank J.O.

Very good sentences to ponder

“We all know that wealth inequality has gone up”

That is a response to the Piketty criticisms from Paul Krugman, and also mentioned by Matt Yglesias. Phiip Pilkington also has a useful treatment. This point however doesn’t do the trick as a defense. Keep in mind that the “new and improved numbers,” as produced by Chris Giles, are showing doubts about the course of measured wealth inequality in the UK. Maybe wealth inequality hasn’t gone up.

Now maybe that does “have to be wrong.” But if the “new and improved” numbers are wrong, it is hard to then argue Piketty’s wealth inequality numbers can be trusted. In which case we are back to knowing that income inequality has gone up, but not knowing so much concrete about wealth inequality. (That is one reason why my own Average is Over focuses on income, and on labor income in particular, because that is where the main action has been.) The data section of Piketty’s book, which has gathered so much praise, then is not so useful, though by no fault of Piketty’s. We might think it likely that wealth inequality has gone up, but if we are going to do these selective overrides of the best available data, we cannot trust the data so much period or otherwise cite it with authority. We also could not map wealth inequality into particular measures of the r vs. g gap at various periods of time.

If there is one big lesson of the FT/Piketty dust-up, it is that we don’t have reliable numbers on wealth inequality.

Now do we in fact “know” that wealth inequality has gone up? See this piece by Allison Schrager. Intuitions about wealth vs. income inequality are trickier than you might think. And on what we actually do and do not know, here is a very good comment on Mian and Sufi’s blog (for U.S. data):

What do the Piketty data problems really mean?

In some ways the new FT criticisms may not matter much, although I think not in a way which is reassuring for Piketty. There were already several major problems with Piketty’s analysis and also empirics, including what Alex has called the asset price problem. He wrote:

According to four French economists, Piketty’s measure of the capital stock is greatly influenced by the Europe-US housing bubble that preceded the financial crisis.

Adjusting for that factor seems to make the main results go away, and that is a purely empirical problem which has not been answered, at least not yet.

Another pre-existing empirical problem is that 19th century data seem to indicate that a “Piketty world,” even if we take it on its own terms, far from being a disaster, would likely be accompanied by rising real wages and declining consumption inequality, albeit rising wealth inequality.

That hasn’t been answered either, although a few people have suggested (without serious back-up) that if wealth inequality is going up that has to lead to political problems, or problems of some kind or another, and thus it can’t be something we can approve of or accept with equanimity, because inequality is really really bad, and therefore Piketty is somehow right anyway. That’s a weak response to begin with and furthermore it doesn’t fit the available data.

Empirically, inheritances aren’t nearly as important as Piketty seems to suggest.

On Twitter Clive Crook wrote of the:

…distance between treacherous data and super-bold conclusions an issue at the outset. This underlines the point.

Now, when you cut through the small stuff, the new empirical problem seems to be that UK revisions, combined with a population-weighted series for Europe, contradicts Piketty’s claim of rising wealth inequality for Europe. I would call that a serious problem. I am not impressed by the “downplaying” responses which focus on coding errors, Swedish data points, and the other small stuff. Let’s face up to the real (new) problem, namely that robustness suddenly seems much weaker. You can’t argue that population-weighting is “the right way to do it,” but it is an entirely plausible way to estimate the wealth inequality trend. If Piketty’s results don’t survive population weighting (and what are apparently the superior UK numbers), that suggests the overall rise in European wealth inequality is not very robust to how the pie is carved up and also that it is not backed by dominant, “rule the roost” sorts of forces.

It should be noted that Piketty’s response to the new criticisms was quite weak. Maybe he’s not to be blamed for what was surely a rapid and caught-off-guard response, and perhaps there is more to come, but it doesn’t reassure me either. He also should have run it by a PR person first (for instance, don’t start your response with a sentence ending in an exclamation point.)

That said, don’t focus on Piketty. When evaluating debates of this kind, never ever confuse a) is he right? with b) “how much should we raise/lower the relative status of the author as a result of the new exchange”? So responses like “he made all his data freely available,” or “he admits all along how complicated this all is,” address b) but not the more important a). And if you are seeing people focus on b) rather than a), they have a problem themselves. On empirical grounds it does seem we have another reason for thinking Piketty’s central claim isn’t quite right, at least not for the reasons he sets out, and perhaps not quite right altogether.

Addendum: Ryan Avent has a good survey of some key issues and responses.

Piketty update

…according to a Financial Times investigation, the rock-star French economist appears to have got his sums wrong.

The data underpinning Professor Piketty’s 577-page tome, which has dominated best-seller lists in recent weeks, contain a series of errors that skew his findings. The FT found mistakes and unexplained entries in his spreadsheets, similar to those which last year undermined the work on public debt and growth of Carmen Reinhart and Kenneth Rogoff.

The central theme of Prof Piketty’s work is that wealth inequalities are heading back up to levels last seen before the first world war. The investigation undercuts this claim, indicating there is little evidence in Prof Piketty’s original sources to bear out the thesis that an increasing share of total wealth is held by the richest few.

Prof Piketty, 43, provides detailed sourcing for his estimates of wealth inequality in Europe and the US over the past 200 years. In his spreadsheets, however, there are transcription errors from the original sources and incorrect formulas. It also appears that some of the data are cherry-picked or constructed without an original source.

For example, once the FT cleaned up and simplified the data, the European numbers do not show any tendency towards rising wealth inequality after 1970. An independent specialist in measuring inequality shared the FT’s concerns.

The full FT story is here.

Addendum: Here is the in-depth discussion. Here is Piketty’s response.

The inequality that matters

Brenda Cronin reports:

Recent hand-wringing about income inequality has focused on the gap between the top 1% and everyone else. A new paper argues that the more telling inequities exist among the 99%, primarily driven by education.

“The single-minded focus on the top 1% can be counterproductive given that the changes to the other 99% have been more economically significant,” says David Autor, a Massachusetts Institute of Technology economist and author of the study.

His paper, “Skills, Education and the Rise of Earnings Inequality Among the ‘Other 99 Percent’,” comes as something of riposte to French economist Thomas Piketty, whose bestselling “Capital in the 21st Century” has ignited sales and conversation around the world with its historical look at the fortunes of the top 1%.

Mr. Autor estimates that since the early 1980s, the earnings gap between workers with a high school degree and those with a college education has become four times greater than the shift in income during the same period to the very top from the 99%.

Between 1979 and 2012, the gap in median annual earnings between households of high-school educated workers and households with college-educated ones expanded from $30,298 to $58,249, or by roughly $28,000, Mr. Autor says. During the same period, he argues, 99% of households would have gained about $7,000 each, had they realized the amount of income that shifted during that time to the top 1%.

There is more here, including good graphs.

I could not have said it better myself.