What I’ve been reading

Michael Wachtel, Viacheslav Ivanov: A Symbolist Life. 615 pp. of what Russian/Soviet cultural life was like in the early 20th century. Focuses on broader strands, rather than just the most famous names. Ivanov today is largely forgotten, but he was at the time arguably the most influential figure of that period. “They were mostly a bunch of nuts” is one of my takeaways.

Herbert Breslin and Anne Midgette, The King and I: The Uncensored Tale of Luciano Pavarotti’s Rise to Fame by his Manager, Friend, and Sometime Adversary. Usually people tell me books like this are “delightful,” and then they bore me to tears. This one actually is fantastically fun. “To tell the truth, though, Luciano didn’t care about the money at the beginning. In the early years, he never asked me how much he was going to get paid for a recital. He had only one condition: it had to be sold out.”

Alan Manning, Why Immigration Policy is Hard and How to Make it Better is a thoughtful and balanced look at its topic, recommended.

Alex Mayyasi, Planet Money: A Guide to the Economic Forces that Shape Your Life is a useful introduction to economic concepts.

Nicolas Niarchos, The Elements of Power: A Story of War, Technology, and the Dirtiest Supply Chain on Earth is a good treatment of minerals issues as they relate to the Congo today. It will not make you more bullish on Rwanda, or for that matter the Congo.

Eve MacDonald, Carthage: A New History covers what we do know about those people. That isn’t much at the conceptual level, and I wonder why archaeology has not taught us more there.

I expect I will very much agree with Brink Lindsey, The Permanent Problem: The Uncertain Transition from Mass Plenty to Mass Flourishing.

Saturday assorted links

1. How to improve nursing homes in America.

3. On Nietzsche (Zarathustra always bored me).

5. LLMs describing the best very long-term investment you could have made in 1300 A.D. Excellent answers, I like the GPT one best.

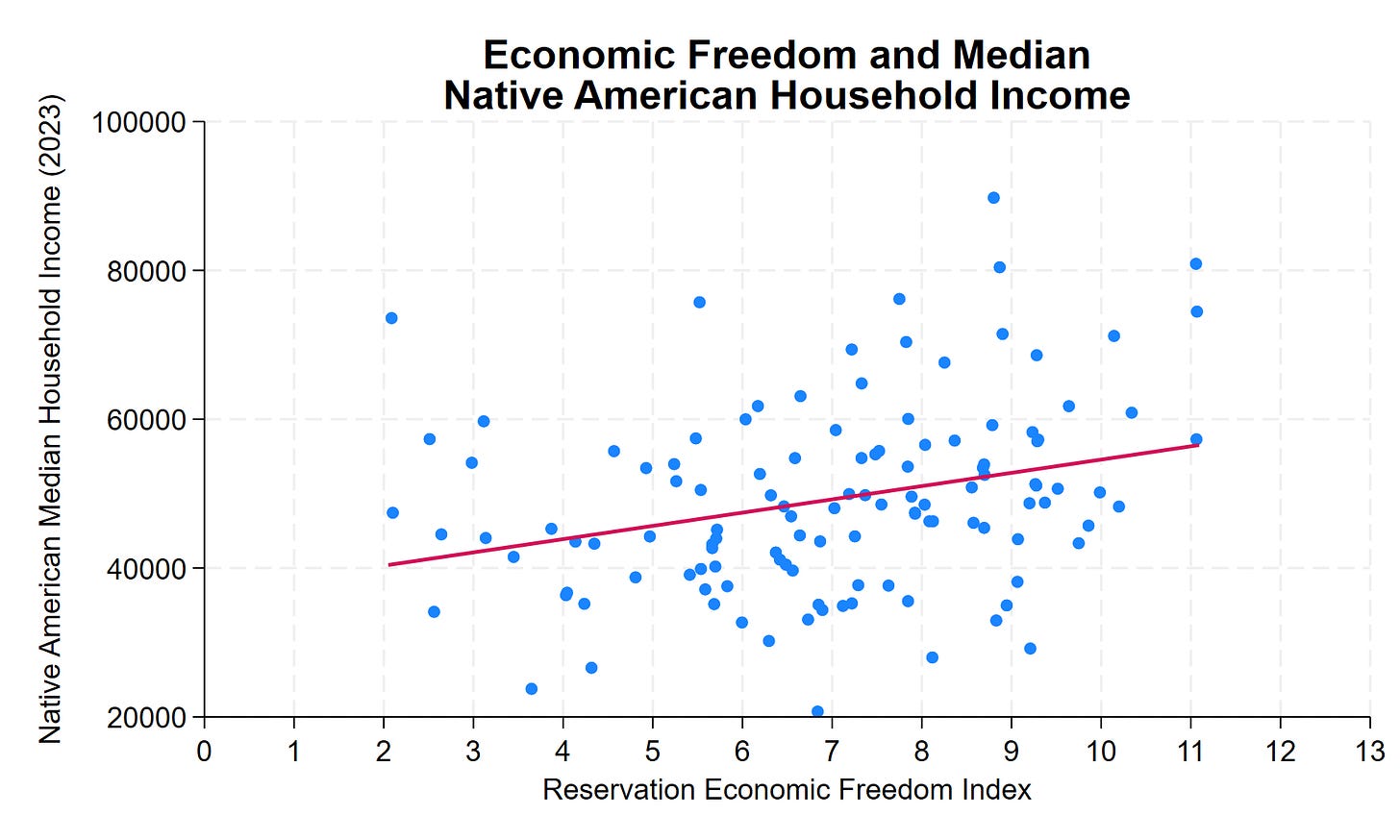

Why Some US Indian Reservations Prosper While Others Struggle

Our colleague Thomas Stratmann writes about the political economy of Indian reservations in his excellent Substack Rules and Results.

Across 123 tribal nations in the lower 48 states, median household income for Native American residents ranges from roughly $20,000 to over $130,000—a sixfold difference. Some reservations have household incomes comparable to middle-class America. Others face persistent poverty.

Why?

The common assumption: casino revenue. The data show otherwise. Gaming, natural resources, and location explain some variation. But they don’t explain most of it. What does? Institutional quality.

The Reservation Economic Freedom Index 2.0 measures how property rights, regulatory clarity, governance, and economic freedom vary across tribal nations. The correlation with prosperity is clear, consistent, and statistically significant. A 1-point improvement in REFI—on a 0-to-13 scale—correlates with approximately $1,800 higher median household income. A 10-point improvement? Nearly $18,000 more per household.

Many low-REFI features aren’t tribal choices—they’re federal impositions. Trust status prevents land from being used as collateral. Overlapping federal-state-tribal jurisdiction creates regulatory uncertainty. BIA approval requirements add months or years to routine transactions. Complex jurisdictional frameworks can deter investment when the rules governing business activity, dispute resolution, and enforcement remain unclear.

This is an important research program. In addition to potentially improving the lives of native Americans, the 123 tribal nations are a new and interesting dataset to study institutions.

See the post for more details amd discussion of causality. A longer paper is here.

The Venezuela conflict

Comments are open, in case you have intelligent insight or useful facts to add…

Luis Garicano career advice

Take the messy job:

The other option is to go for a messy job, where the output is the product of many different tasks, many of which affect each other.

The head of engineering at a manufacturing plant I know well must decide who to hire, which machines to buy, how to lay them down in the plant, negotiate with the workers and the higher ups the solutions proposed, and mobilise the resources to implement them. That task is extraordinarily hard to automate. Artificial intelligence commoditizes codified knowledge: textbooks, proofs, syntax. But it does not interface in a meaningful way with local knowledge, where a much larger share of the value of messy jobs is created. Even if artificial intelligence excelled at most of the single tasks that make up her job, it could not walk the factory floor to cajole a manager to redesign a production process.

A management consultant whose job consists entirely of producing slide decks is exposed. A consultant who spends half of her time reading the room, building client relationships, and navigating organizational politics has a bundle AI cannot replicate.

Here is the full letter.

Direct and Indirect Effects of Vaccines: Evidence from COVID-19

Sorry people, but the verdict on this one continues to come in:

We estimate direct and indirect vaccine effectiveness and assess how far the infection-reducing externality extends from the vaccinated, a key input to policy decisions. Our empirical strategy uses nearly universal microdata from a single state and relies on the six-month delay between 12- and 11-year-old COVID vaccine eligibility. Vaccination reduces cases by 80 percent, the direct effect. This protection spills over to close contacts, producing a household-level indirect effect about three-fourths as large as the direct effect. However, indirect effects do not extend to schoolmates. Our results highlight vaccine reach as important to consider when designing policy for infectious disease.

That is from American Economic Journal: Applied Economics, by Seth Freedman, Daniel W. Sacks, Kosali Simon, and Coady Wing. So many different methods and papers are pointing in the same direction…

What should I ask Henry Oliver?

Yes, I will be doing a Conversation with him. We will focus on our mutual readings of Shakespearer’s Measure for Measure, with Henry taking the lead. But I also will ask him about the value of literature, Jane Austen, Adam Smith, Bleak House, his book on late bloomers, and more.

Here is Henry’s (free) Substack. Here is Henry on Twitter.

So what should I ask him?

Friday assorted links

*Pluribus*

The show is very good, noting that very few television series satisfy me. It is conceptual, philosophical, and multi-sided. Episode two I thought was one of the best TV episodes I have seen. So many of you should try it, noting that at first Episode one feels excessive, implausible, and “too fruity.”

AEA: Honoring Milton Friedman

Looks like a good AEA session on Sunday in Philly:

“Honoring Milton Friedman on his 50th Anniversary of Winning the Nobel Prize”

Mark Skousen: “My Friendly Fights with Milton Friedman”

Jeremy Siegel: “Milton Friedman’s contributions to financial markets and the influence of money on the business cycle.”

James K. Galbraith: “Milton Friedman’s Critique of Keynesian Economics and Fiscal Policy: A Response”

Michael Bordo: “The Future of Monetarism After Friedman: What Works, What Doesn’t.”

Judy Shelton: “Milton Friedman and Robert Mundell: Who Won the Nobel Money Duel?”

To be held Sunday Jan. 4, 8-10 am ET at the Philadelphia Marriott Hotel, Grand Ballroom Salon B.

Economic inequality does not equate to poor well-being or mental health

A meta-analysis of 168 studies covering more than 11 million people found no reliable link between economic inequality and well-being or mental health. In other words, living in a place that has large gaps between the rich and poor does not affect these outcomes, with implications for policy.

Here is the Nature link, this claim has been bad science all along.

One bad trend from 2025, diminution of the dollar’s safe haven status

It used to be that if you were worried about the future, you would move into dollars as the safe haven—in finance terms a countercyclical asset, which stays resilient when higher-risk assets fall. But if the United States’ own government and policies are unpredictable, and its economy is volatile, you will look for some other hedges instead. Chaos in the U.S., and particularly in the White House, is pushing investors to find alternatives to the dollar.

And so investment funds have been pouring into the precious metals, boosting their prices. While the current high price of silver reflects many factors, some of them technical and quite specific, the shift in risk attitudes has become pronounced over the last year.

The bottom line is that America is less of a safe haven than it used to be. When President Donald Trump announced his heavy tariff plan on “Liberation Day,” the dollar fell. That’s contrary to ordinary economic theory, which suggests that as Americans send fewer dollars abroad to buy imported goods, the dollar should rise. Traders, though, started to view the United States itself as a source of risk. It felt as if the right thing to do was to run away from the dollar. As a result, the dollar is down nearly 10 percent this year.

Here is more from me at The Free Press.

Thursday assorted links

1. How a research trip to Antarctica deals with time zones (NYT).

3. What kind of books did people buy in 2025? (NYT)

4. Notes on Taiwan.

6. What Shruti has been reading, including about India but not only.

7. On the compute theory of everything.

Dan Wang 2025 letter

Self-recommending, here is the link, here is one excerpt:

People like to make fun of San Francisco for not drinking; well, that works pretty well for me. I enjoy board games and appreciate that it’s easier to find other players. I like SF house parties, where people take off their shoes at the entrance and enter a space in which speech can be heard over music, which feels so much more civilized than descending into a loud bar in New York. It’s easy to fall into a nerdy conversation almost immediately with someone young and earnest. The Bay Area has converged on Asian-American modes of socializing (though it lacks the emphasis on food). I find it charming that a San Francisco home that is poorly furnished and strewn with pizza boxes could be owned by a billionaire who can’t get around to setting up a bed for his mattress.

And:

One of the things I like about the finance industry is that it might be better at encouraging diverse opinions. Portfolio managers want to be right on average, but everyone is wrong three times a day before breakfast. So they relentlessly seek new information sources; consensus is rare, since there are always contrarians betting against the rest of the market. Tech cares less for dissent. Its movements are more herdlike, in which companies and startups chase one big technology at a time. Startups don’t need dissent; they want workers who can grind until the network effects kick in. VCs don’t like dissent, showing again and again that many have thin skins. That contributes to a culture I think of as Silicon Valley’s soft Leninism. When political winds shift, most people fall in line, most prominently this year as many tech voices embraced the right.

Interesting throughout, plus Dan writes about the most memorable books he read in 2025.

Autism Hasn’t Increased

Autism diagnoses have increased but only because of progressively weaker standards for what counts as autism.

The autistic community is a large, growing, and heterogeneous population, and there is a need for improved methods to describe their diverse needs. Measures of adaptive functioning collected through public health surveillance may provide valuable information on functioning and support needs at a population level. We aimed to use adaptive behavior and cognitive scores abstracted from health and educational records to describe trends over time in the population prevalence of autism by adaptive level and co-occurrence of intellectual disability (ID). Using data from the Autism and Developmental Disabilities Monitoring Network, years 2000 to 2016, we estimated the prevalence of autism per 1000 8-year-old children by four levels of adaptive challenges (moderate to profound, mild, borderline, or none) and by co-occurrence of ID. The prevalence of autism with mild, borderline, or no significant adaptive challenges increased between 2000 and 2016, from 5.1 per 1000 (95% confidence interval [CI]: 4.6–5.5) to 17.6 (95% CI: 17.1–18.1) while the prevalence of autism with moderate to profound challenges decreased slightly, from 1.5 (95% CI: 1.2–1.7) to 1.2 (95% CI: 1.1–1.4). The prevalence increase was greater for autism without co-occurring ID than for autism with co-occurring ID. The increase in autism prevalence between 2000 and 2016 was confined to autism with milder phenotypes. This trend could indicate improved identification of milder forms of autism over time. It is possible that increased access to therapies that improve intellectual and adaptive functioning of children diagnosed with autism also contributed to the trends.

The data is from the US CDC.

Hat tip: Yglesias who draws the correct conclusion:

Study confirms that neither Tylenol nor vaccines is responsible for the rise in autism BECAUSE THERE IS NO RISE IN AUTISM TO EXPLAIN just a change in diagnostic standards.

Earlier Cremieux showed exactly the same thing based on data from Sweden and earlier CDC data.

Happy New Year. This is indeed good news, although oddly it will make some people angry.